Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 13.10 Billion |

| Market Size (2026) | USD 13.79 Billion |

| Market Size (2031) | USD 17.84 Billion |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

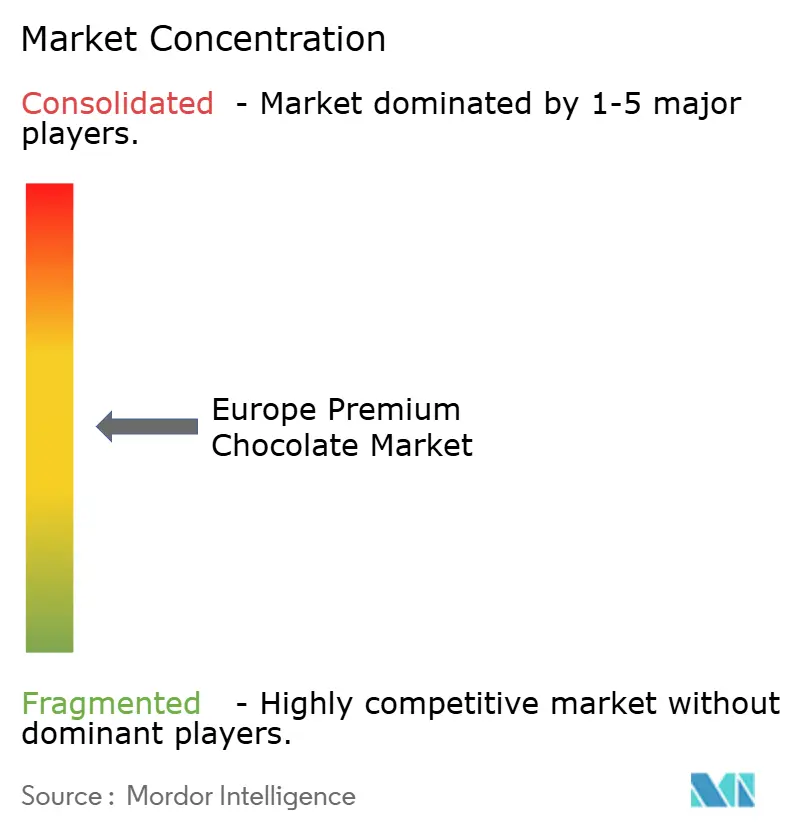

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Premium Chocolate Market Analysis by Mordor Intelligence

The Europe Premium Chocolate Market size is expected to grow from USD 13.10 billion in 2025 to USD 13.79 billion in 2026 and is forecast to reach USD 17.84 billion by 2031 at 5.29% CAGR over 2026-2031. Consumers now focus on factors like ethical sourcing, traceability, and functional ingredients alongside flavor. Online subscriptions, bean-to-bar workshops, and chef collaborations are connecting farms to consumers, sustaining price premiums despite fluctuating cocoa costs. Single-origin chocolates, high-cocoa content, and plant-based “mylk” variants appeal to health-conscious buyers. Regulatory demands for deforestation control and clear nutrition labeling are driving manufacturers toward transparent supply chains and low-sugar recipes. Brands that secure certified beans, utilize digital platforms, and highlight health benefits effectively are well-positioned to succeed.

Key Report Takeaways

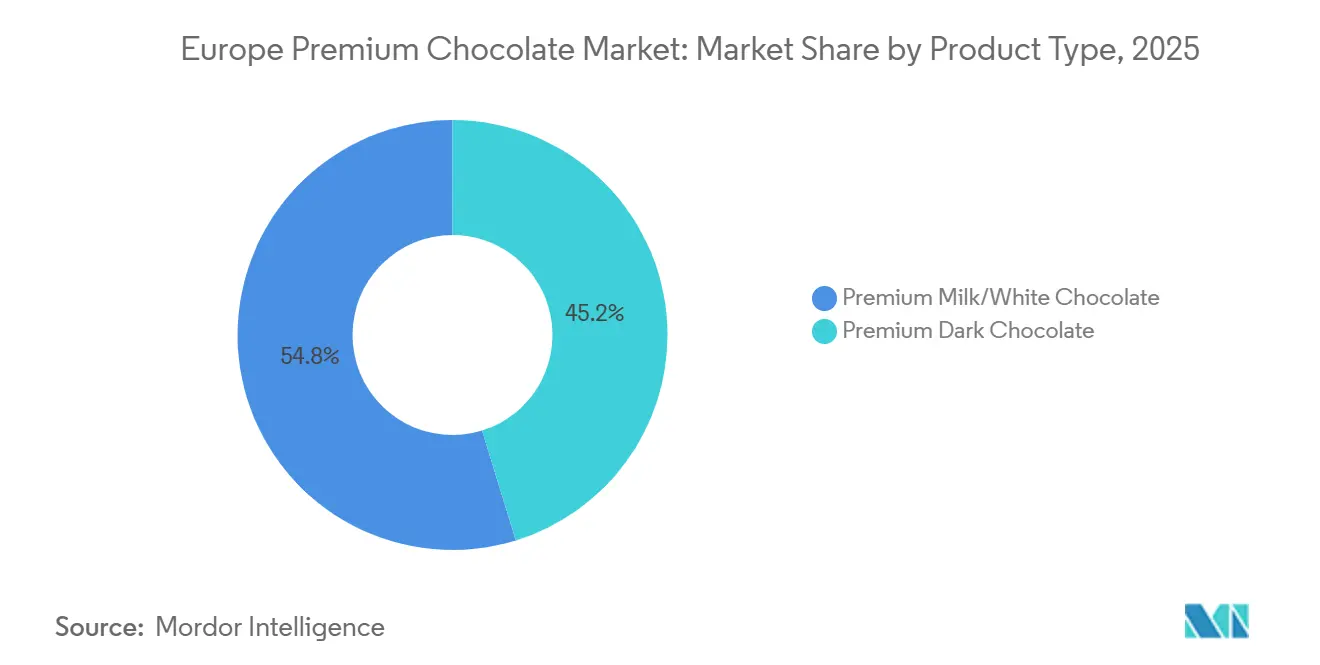

- By product type, Premium Milk/White Chocolate led with 54.78% of the Europe premium chocolate market share in 2025, whereas Premium Dark Chocolate is poised to expand at a 5.98% CAGR through 2031.

- By category, dairy formats held 90.13% of the Europe premium chocolate market size in 2025, while non-dairy or vegan chocolates are projected to climb at a 6.82% CAGR to 2031.

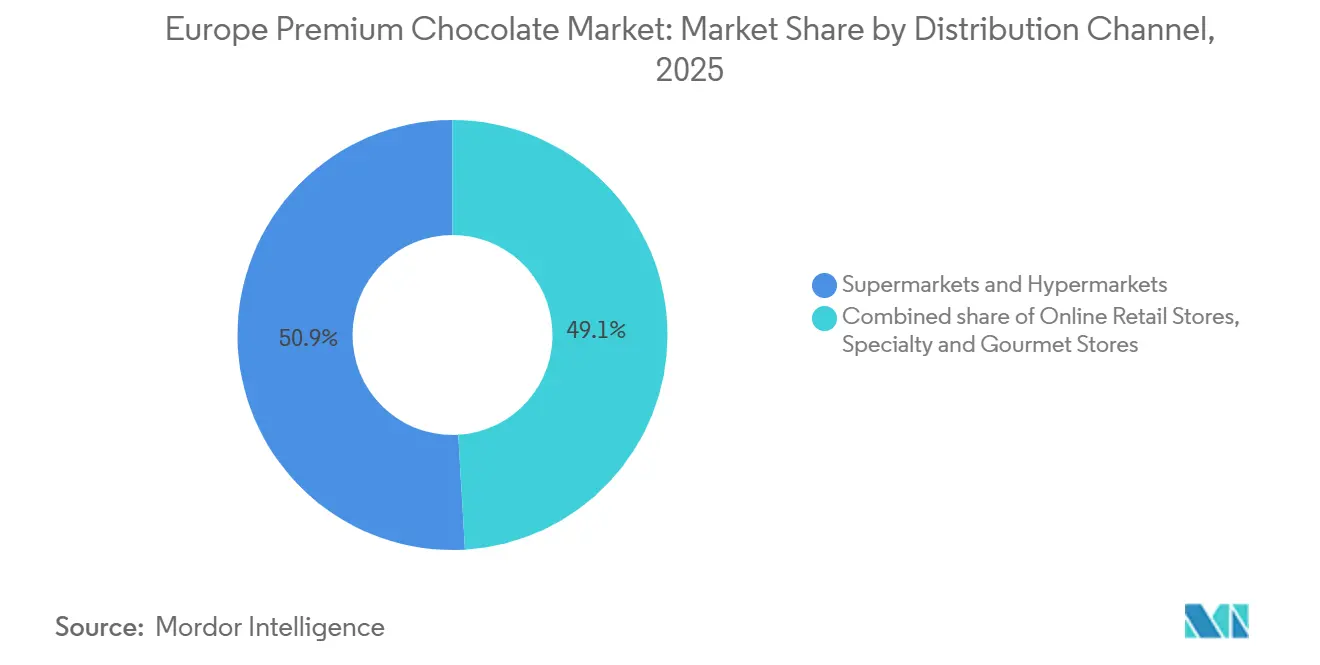

- By distribution channel, supermarkets and hypermarkets controlled 50.92% of the Europe premium chocolate market size in 2025; online retail stores represent the fastest trajectory with a 6.52% CAGR through 2031.

- By geography, Germany accounted for 27.65% of regional revenue in 2025, whereas Spain is the fastest-growing country at a 7.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Premium Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-conscious consumers prefer dark and low-sugar premium chocolates as "better-for-you" indulgences | +0.8% | Global, strongest in Germany, UK, Netherlands, Sweden | Medium term (2-4 years) |

| Functional chocolates with nuts, seeds, superfoods, or added nutrients enhance premium appeal | +0.6% | Global, early adoption in France, Belgium, Switzerland | Medium term (2-4 years) |

| Ethically sourced, fair-trade, and Rainforest Alliance/organic cocoa drive consumer loyalty | +0.9% | Global, particularly Germany, Netherlands, UK, Nordic countries | Long term (≥ 4 years) |

| E-commerce, subscription boxes, and direct-to-consumer platforms expand access to premium chocolates | +1.2% | Global, advanced penetration in UK, Netherlands, Germany | Short term (≤ 2 years) |

| Novel flavors and textural innovations fuel premium product growth | +0.7% | Global, concentrated in urban centers across France, Italy, Spain, Belgium | Medium term (2-4 years) |

| Specialty chocolatiers and café-boutiques thrive with tastings, pairing events, and cocoa education | +0.5% | Global, strongest in Belgium, France, Italy, urban Germany, Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health-Conscious Consumers Prefer Dark and Low-Sugar Premium Chocolates as "Better-for-You" Indulgences

Barry Callebaut's 2024 consumer survey reveals that most European chocolate consumers expect chocolate brands to offer wellness-focused innovations, with younger buyers favoring plant-based or reduced-sugar options. This demand drives the Premium Dark Chocolate segment's 5.98% CAGR, surpassing the category average. Manufacturers are reformulating products with over 70% cocoa and natural sweeteners like stevia and monk fruit. Germany and the Netherlands lead this trend, with Germany's per-capita dark-chocolate consumption rising 12% from 2023 to 2025, driven by urban millennials seeking guilt-free indulgences rich in polyphenols. In 2024, Lindt launched a 90% cocoa Excellence line, achieving double-digit volume growth in its first year across German and Swiss retail channels. The "better-for-you" trend also emphasizes portion control, with single-serve 20-gram dark-chocolate squares now making up 18% of premium SKU launches in Western Europe, meeting demand for mindful snacking while enabling higher per-gram pricing.

Functional Chocolates with Nuts, Seeds, Superfoods, or Added Nutrients Enhance Premium Appeal

In 2025, Puratos reported that 65% of European consumers seek "mood food" in confectionery, while 68% believe botanical ingredients offer health benefits. Manufacturers are responding by adding adaptogens, probiotics, and plant-based proteins to chocolate. Barry Callebaut's survey showed 61% of respondents value chocolate's mental health benefits, leading to launches like ashwagandha truffles and magnesium-enriched dark bars. A 2024 Nature Food study introduced whole-fruit chocolate, made with cocoa pulp and endocarp, as a sucrose-free option that boosts fiber by 20%. Swiss and Belgian artisans are piloting this innovation. France and Belgium lead in functional SKUs, with Valrhona launching its "Wellness Collection" in early 2025, featuring quinoa crisps and chia seeds for premium retailers. This mix of indulgence and nutrition allows brands to charge 30–40% higher prices, protecting margins despite rising cocoa costs.

Ethically Sourced, Fair-Trade, and Rainforest Alliance/Organic Cocoa Drive Consumer Loyalty

From December 30, 2024, the European Union Deforestation Regulation will require geolocation proof for all cocoa imports to confirm a deforestation-free origin, making traceability a legal requirement[1]Source: European Commission, "Cocoa under the Deforestation Regulation", green-forum.ec.europa.eu. Rainforest Alliance certification, which enforces agroforestry practices and bans child labor, now covers 35 percent of European cocoa imports, up from 22 percent in 2022. Between 2023 and 2025, Fairtrade International reported a 28 percent rise in certified cocoa entering the EU, with Germany, the Netherlands, and the UK accounting for 60 percent of the volume. By 2024, Lindt's Farming Program, sourcing directly from 185,000 farmers and ensuring minimum prices, achieved 100 percent cocoa sourcing, aligning with German consumers' focus on sustainability as their second priority after taste. Tony's Chocolonely, a Dutch B Corp, increased European sales by 22 percent in 2024 by publishing supply-chain maps and ensuring partners meet living-income standards. Organic certification under EU Regulation 2018/848 adds a 15–20 percent price premium but appeals to Nordic and Alpine consumers. Sweden and Switzerland lead with organic chocolate penetration rates above 12 percent, double the European average.

E-Commerce, Subscription Boxes, and Direct-to-Consumer Platforms Expand Access to Premium Chocolates

By 2031, online channels are expected to account for 6.52% of the market, with the Netherlands' share rising from 7.2% to 9.4%. Luker Chocolate reported that over 50% of premium buyers now discover brands online. Digital-native brands are growing at 13 percent annually, compared to 4% for traditional brick-and-mortar players. Subscription services like Cocoa Runners in the UK and Choco Box in Germany offer curated single-origin bars from micro-producers for EUR 30 to EUR 50 per month, creating steady revenue and reducing seasonal risks. Direct-to-consumer platforms help artisans retain 60 to 70% of the sale price, compared to 30 to 40% in traditional channels. Hotel Chocolat, acquired by Mars in 2023, combined its e-commerce platform with physical tasting clubs, increasing average basket size by 19 percent in 2024. While COVID-19 accelerated digital adoption, growth continues due to AI-driven recommendations, urgency from limited-edition releases, and carbon-neutral shipping that aligns with consumer values.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain traceability compliance costs | -0.6% | Global, disproportionate burden on SMEs in Belgium, Italy, Spain | Short term (≤ 2 years) |

| Cocoa-price volatility | -0.9% | Global, affects all manufacturers with limited hedging capacity | Short term (≤ 2 years) |

| Alternative indulgences fragment the premium treat category | -0.4% | Global, strongest in UK, Germany, Netherlands | Medium term (2-4 years) |

| EU food safety standards force costly reformulations and compliance investments | -0.5% | EU-wide, particularly impacts cross-border operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Traceability Compliance Costs

Effective December 30, 2024, the EU Deforestation Regulation requires importers to submit due-diligence statements with geolocation data for every cocoa shipment. Small and midsize chocolatiers, lacking compliance teams, face upfront costs of EUR 50,000 to EUR 150,000 for satellite monitoring, blockchain platforms, and audits. Belgian and Italian artisans, sourcing cocoa through complex intermediaries, struggle to trace farm-level origins, risking shipment rejections at EU ports. Larger companies like Lindt and Ferrero manage these costs through scale, but smaller operators either raise prices—hurting competitiveness—or exit the market. Non-compliance penalties of up to 4% of annual EU turnover further increase risks, pushing supply chains toward certified cooperatives. These challenges slow SKU innovation as manufacturers focus on compliance, while new brands face delays due to high costs of traceable cocoa.

Cocoa-Price Volatility

In April 2024, cocoa futures on ICE soared to USD 12,000 per metric ton due to a 374,000-tonne global deficit in the 2023/24 season caused by droughts and swollen-shoot disease in Ivory Coast and Ghana[2]Source: The International Cocoa Organization (ICCO). "Cocoa Daily Prices", icco.org. Prices settled between USD 9,000 and USD 10,000 per ton through 2025, still three times higher than the 2020 average, squeezing margins for manufacturers without long-term hedging. Mondelez and Nestlé, with 12- to 18-month hedging strategies, managed the spike, while smaller operators relying on the spot market saw profits decline. In January 2025, Ferrero raised prices by 6 percent across Europe, citing cocoa costs, but volume sales dropped 3 percent as inflation-hit consumers opted for cheaper products. Climate volatility, worsened by El Niño, adds uncertainty, with the International Cocoa Organization predicting deficits until 2026 unless West African yields improve. This volatility discourages premium investments and drives vertical integration, as seen in Lindt’s expanded Farming Program to secure stable supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Milk and White Formulations Retain Mass Appeal Despite Dark Chocolate's Health Halo

In 2025, Premium Milk/White Chocolate dominated 54.78% of Europe's Premium Chocolate Market, driven by consumer preference for its creamy texture and mild flavor. Germany, Switzerland, and the UK lead in milk chocolate consumption, exceeding 5 kilograms per capita annually, supported by brands like Lindt's Lindor and Milka's Alpine Milk bars. Milk chocolate's versatility in products like pralines, biscuits, and seasonal figures ensures its popularity, especially during Easter and Christmas, which account for 40% of annual sales. White chocolate, though smaller in market share, benefits from premium offerings like Valrhona's Ivoire 35 percent, favored in French pâtisseries. However, rising cocoa-butter costs, which make up 30-35% of white chocolate, have led manufacturers to adopt shrinkflation—reducing bar sizes while maintaining prices—risking consumer dissatisfaction if not communicated clearly.

Premium Dark Chocolate, while holding a smaller market share in 2025, is growing at a 5.98% CAGR through 2031, outpacing milk and white chocolate. Health-conscious consumers prefer dark chocolate for its high cocoa content and perceived health benefits, such as flavonoids and antioxidants. Lindt's Excellence range (70%, 85%, and 90% cocoa) saw an 18% volume increase in Germany and the Netherlands in 2024, driven by urban millennials. A 2024 Barry Callebaut survey found 67% of European consumers seek innovative chocolate products, with 61% of younger buyers favoring reduced-sugar options, boosting demand for dark chocolate. Ritter Sport's 2024 "Cacao Selection," featuring 74% and 81% dark chocolate with sea salt and almond, gained traction in German discounters and premium grocers. Dark chocolate's growth is further supported by its vegan and organic certifications and ethical sourcing from Rainforest Alliance or Fairtrade cooperatives, contributing 0.9 percentage points to the market's CAGR.

By Category: Dairy Dominance Persists While Vegan Alternatives Capture Flexitarian Demand

In 2025, dairy chocolates dominated 90.13% of the Europe Premium Chocolate Market, driven by their creamy texture and strong consumer preference. Countries like Switzerland, Belgium, and Germany, with annual per-capita chocolate consumption over 10 kilograms, showed loyalty rates above 85%, supported by iconic brands like Lindt, Neuhaus, and Ritter Sport. Efficient manufacturing processes, such as tempering and conching, ensure consistent quality at scale. Dairy chocolates also dominate seasonal gifting, including Easter eggs and Christmas advent calendars, as they evoke indulgence and nostalgia. However, challenges arise from lactose-intolerant consumers and sustainability concerns. Milk chocolate produces 20–25% more greenhouse-gas emissions than dark chocolate due to dairy farming. To address this, manufacturers like Lindt are sourcing milk from regenerative farms, though this increases costs by 8–12%.

Non-dairy or vegan chocolates, with a market share below 10% in 2025, are growing at a 6.82% CAGR through 2031, the fastest among all categories. Barry Callebaut introduced plant-based "mylk" chocolate in 2024, using oat, almond, and rice bases, achieving rapid growth in Germany, the UK, and the Netherlands. Lindt launched vegan oat-milk chocolate bars in the UK and Germany in 2024, targeting flexitarians, and these accounted for 4% of Lindt's UK sales by year-end. Tony's Chocolonely expanded its vegan range to six SKUs in 2025, reporting 28% annual growth in vegan sales. Vegan chocolates appeal to a broader audience, with 61% of young European consumers seeking plant-based options for perceived health and sustainability benefits. EU regulations, like the Farm to Fork Strategy, support plant-based innovation through subsidies and clear labeling. Despite challenges like higher costs from cocoa-butter supplementation to improve creaminess, advancements in ingredient technology and economies of scale are closing the gap in taste and price.

By Distribution Channel: Supermarkets Anchor Volume While Online Platforms Capture Premiumization

In 2025, Supermarkets and Hypermarkets led Europe's Premium Chocolate Market distribution with a 50.92% share. Their success stems from widespread availability, competitive pricing, and strategic placement of impulse buys near checkout lanes. In Germany, chains like Edeka, Rewe, and Aldi stock brands such as Lindt, Ritter Sport, and Milka across 15,000+ locations, ensuring visibility and repeat purchases. In France, Carrefour and Leclerc dedicate 12 to 15 meters to premium chocolates, using seasonal displays and cross-promotions with wine and coffee to boost basket sizes. Supermarkets also serve as testing grounds for new products from Ferrero, Mondelez, and Nestlé, allowing manufacturers to gauge demand before expanding to specialty stores.

Online Retail Stores, while holding a smaller share in 2025, are growing rapidly at a 6.52% CAGR through 2031, the fastest among all channels. Luker Chocolate reports that many premium buyers now discover brands online. Digital-first brands grow 13% annually, outperforming the 4% growth of traditional retailers. Subscription services like Cocoa Runners in the UK and Choco Box in Germany offer curated single-origin bars for EUR 30–50 monthly, creating steady revenue and reducing seasonal impacts. Direct-to-consumer platforms cut out intermediaries, allowing artisans to retain 60–70% of sales compared to 30–40% in traditional channels. Online platforms also drive loyalty with limited-edition releases and AI-based personalized recommendations. Venchi's "Chocolate of the Month" subscription sold out in 72 hours in Italy and Spain. Additionally, 40% of European online chocolate retailers now offer carbon-neutral shipping, aligning with consumer sustainability values and justifying delivery fees.

Geography Analysis

Germany led Europe's premium chocolate market in 2025, holding a 27.65% share, driven by the region's highest per-capita chocolate consumption of 11.9 kilograms annually and a strong cultural preference for high-quality confectionery. Major brands like Lindt, Ritter Sport, and Milka dominate the market by leveraging their heritage and extensive distribution networks through retailers such as Edeka, Rewe, and Aldi. Urban centers like Berlin, Munich, and Hamburg have premium chocolate penetration rates exceeding 35%, supported by affluent millennials who prefer single-origin chocolate bars and value ethical certifications. France and the UK follow as the second and third-largest markets, respectively.

Spain is the fastest-growing market in the region, with a projected CAGR of 7.21% through 2031. This growth is driven by increasing premiumization among urban Gen Z and millennials in cities like Madrid, Barcelona, and Valencia. Historically, Spain's chocolate consumption lagged behind Northern Europe due to lower per-capita incomes and a preference for alternative desserts. However, rising disposable incomes and exposure to Belgian and Swiss chocolate brands through tourism are boosting demand. Between 2023 and 2025, Lindt opened 12 boutiques in Spain, while Godiva expanded its presence by partnering with El Corte Inglés department stores to target gifting occasions. Vegan chocolate sales in Spain grew by 34% in 2024, the highest in Europe, as younger consumers increasingly adopt flexitarian diets. Meanwhile, mature markets like the Netherlands and Sweden maintain mid-single-digit growth, supported by a focus on sustainability. In the Netherlands, ethical sourcing ranks as the second most important purchase factor after taste, helping Tony's Chocolonely achieve a 22% sales increase in 2024.

Poland is emerging as a growing market in the region, with steady growth driven by Westernization and the impact of EU accession, which have boosted chocolate consumption. Local heritage brand Wedel, now owned by Lotte, competes with global players like Lindt and Ferrero in cities such as Warsaw and Krakow. Belgium, despite its small population, has a robust domestic chocolate market worth EUR 1.2 billion. Iconic brands like Neuhaus, Leonidas, and Guylian dominate the market and export 70% of their production to neighboring countries, highlighting Belgium's significant influence in the premium chocolate industry.

Competitive Landscape

The Europe premium chocolate market is moderately fragmented, with a combination of multinational confectionery companies, well-established regional brands, and a large number of artisanal chocolatiers competing across countries. Renowned players who held a prominent share in the market include Chocoladefabriken Lindt & Sprüngli AG, Ferrero Group, Mondelez International, and Nestlé S.A. Leading players benefit from strong brand heritage, extensive retail presence, and the ability to scale premium offerings through wide distribution in supermarkets, specialty stores, and travel retail. However, consumer preferences for origin, craftsmanship, and flavor innovation vary significantly across European markets, preventing high market concentration.

Smaller and artisanal chocolate makers play a crucial role in shaping the premium segment by emphasizing single-origin cocoa, ethical sourcing, and handcrafted production methods. These players often operate through boutique stores, specialty retailers, and direct-to-consumer channels, allowing them to maintain premium pricing and close relationships with consumers. Their focus on authenticity, unique textures, and innovative inclusions helps them compete effectively despite limited production volumes.

Competition in the European premium chocolate market is increasingly driven by quality differentiation, sustainability credentials, and storytelling rather than price. Established brands continue to expand premium and super-premium ranges with higher cocoa content, organic certifications, and limited-edition collections, while selectively acquiring niche chocolatiers to access craftsmanship and brand equity. This coexistence of global leaders and numerous specialized producers sustains the market’s moderately fragmented structure across Europe.

Europe Premium Chocolate Industry Leaders

-

Chocoladefabriken Lindt & Sprüngli AG

-

Mondelez International

-

Ferrero Group

-

Nestlé SA

-

Mars Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: German-based confectionery group Windel acquired Belgian high-end praline business, The Chocolate Family (TCF). TCF will closely collaborate with Kim’s Chocolates, which is also part of the Windel Group and one of Belgium’s largest chocolate manufacturers. This partnership will create a one-stop shop for customers seeking Belgian premium chocolates.

- October 2025: Valrhona, one of the Premium chocolate brands, has launched its new Pistachio Crispy Praliné Gift Box amid key growth within the travel retail sector. According to the brand, each piece of the French-made luxury range delivers an exquisite balance of crisp texture, intense pistachio praline, and silky milk chocolate.

- March 2025: Lindt & Sprüngli, one of the globally renowned chocolate manufacturers, has opened its brand-new flagship store in London, located beneath the iconic Piccadilly Lights. The new store boasts a range of exclusive features and indulgent offerings, including the LINDOR truffle boxes, gift tags, Lindt Dubai Style Chocolate, and more.

- September 2025: Lindt & Sprüngli has launched a new line of decadent chocolate bars. According to the brand, the new Les Grandes Fruit & Nut bar boasts high-quality ingredients, including perfectly roasted hazelnuts and succulent raisins, all enveloped in smooth Swiss milk chocolate.

- January 2024: Mars, Incorporated has acquired Hotel Chocolat, a prominent premium chocolate brand in the UK. With this acquisition, Mars aims to bolster its foothold in the premium chocolate sector and capitalize on Hotel Chocolat's established brand recognition across Europe.

Europe Premium Chocolate Market Report Scope

Premium chocolates are high-end/luxury chocolates priced higher than the other chocolates in the market due to their unique features.

Europe's Premium Chocolate Market is segmented on the basis of Product Type (Dark Premium Chocolate and White/ Milk Premium Chocolate), Distribution Channel (Hypermarkets/Supermarkets, Convenience Stores, Online Retail Stores, and Other Distribution Channels), and Geography (United Kingdom, France, Germany, Italy, Spain, Russia, Switzerland, and Rest of Europe). The report offers market size and forecasts for the market in value (USD million) for all the above segments.

By Product Type

| Premium Dark Chocolate |

| Premium Milk/ White Chocolate |

By Category

| Dairy Chocolates |

| Non-Dairy or Vegan Chocolates |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty and Gourmet Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Poland |

| Belgium |

| Rest of Europe |

| By Product Type | Premium Dark Chocolate |

| Premium Milk/ White Chocolate | |

| By Category | Dairy Chocolates |

| Non-Dairy or Vegan Chocolates | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Specialty and Gourmet Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe premium chocolate market in 2026?

The Europe premium chocolate market size stood at USD 13.79 billion in 2026.

What is the expected growth rate for premium chocolate in Europe?

The market is forecast to post a 5.29% CAGR between 2026 and 2031.

Which product segment is growing the fastest?

Premium Dark Chocolate is projected to expand at a 5.98% CAGR to 2031 on wellness demand.

Why are vegan chocolates gaining traction in Europe?

Plant-based bars satisfy flexitarian diets and align with sustainability goals, lifting non-dairy formats at a 6.82% CAGR.

Page last updated on: