Europe Sugar Confectionery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 15.05 Billion |

| Market Size (2026) | USD 17.25 Billion |

| Market Size (2031) | USD 19.28 Billion |

| Growth Rate (2026 - 2031) | 4.89% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Sugar Confectionery Market Analysis by Mordor Intelligence

The Europe sugar confectionery market size is expected to grow from USD 15.05 billion in 2025 to USD 17.25 billion in 2026 and is forecast to reach USD 19.28 billion by 2031 at 4.89% CAGR over 2026-2031. Robust household spending in Central and Eastern Europe, continuous recipe reformulation, and premium product launches in mature Western economies are the principal growth vectors supporting the European sugar confectionery market. Heightened scrutiny from nutrition regulators is accelerating the use of plant-based gelling agents and alternative sweeteners, yet indulgence remains resilient as seasonal gifting, nostalgia marketing, and experiential packaging stimulate repeat purchases. Ingredient inflation, especially in sugar and gelatin, has compressed margins, but many producers are offsetting cost pressure through smaller pack sizes, direct-to-consumer sales, and premium-tier extensions aimed at urban millennials. Capital commitments such as Mars’s EUR 1 billion manufacturing upgrade illustrate the industry’s confidence in a stable long-run demand curve despite near-term regulatory headwinds.

Key Report Takeaways

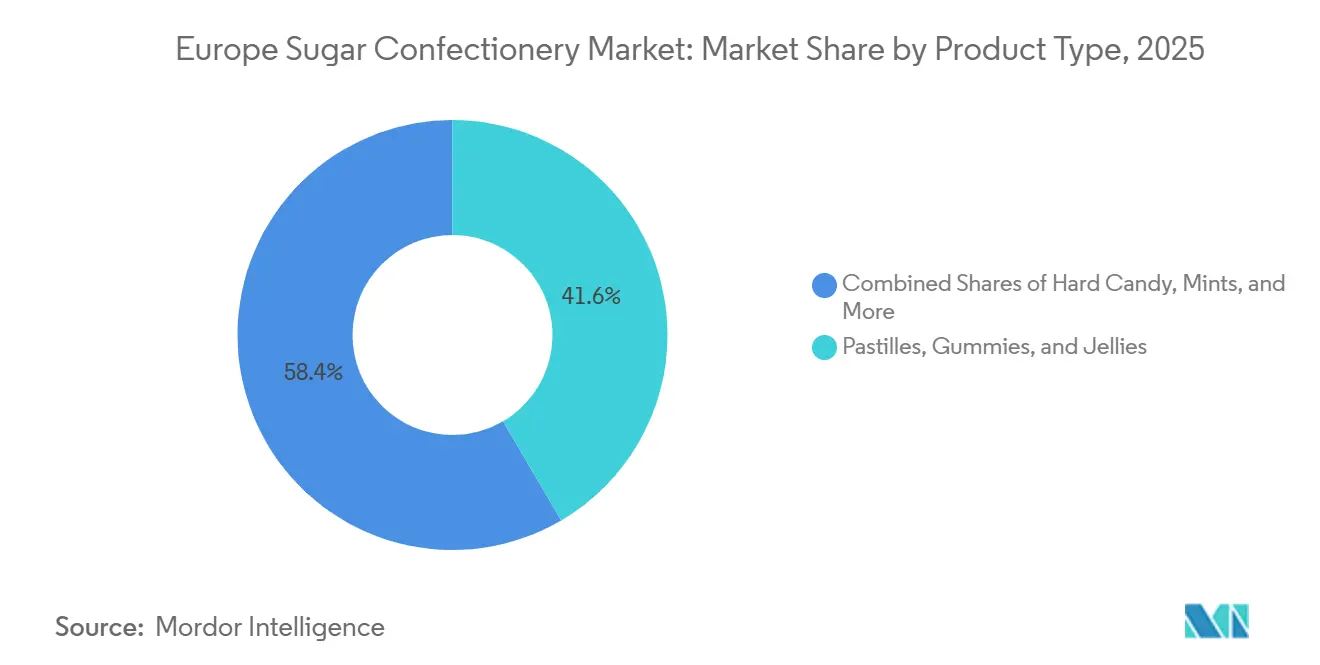

- By type, pastilles, gummies, and jellies held 41.56% of the Europe sugar confectionery market share in 2025. Lollipops are set to log the fastest 6.45% CAGR through 2031.

- By functional benefit, novelty products captured 42.60% revenue share in 2025, while fortified variants are on track for a 7.01% CAGR to 2031.

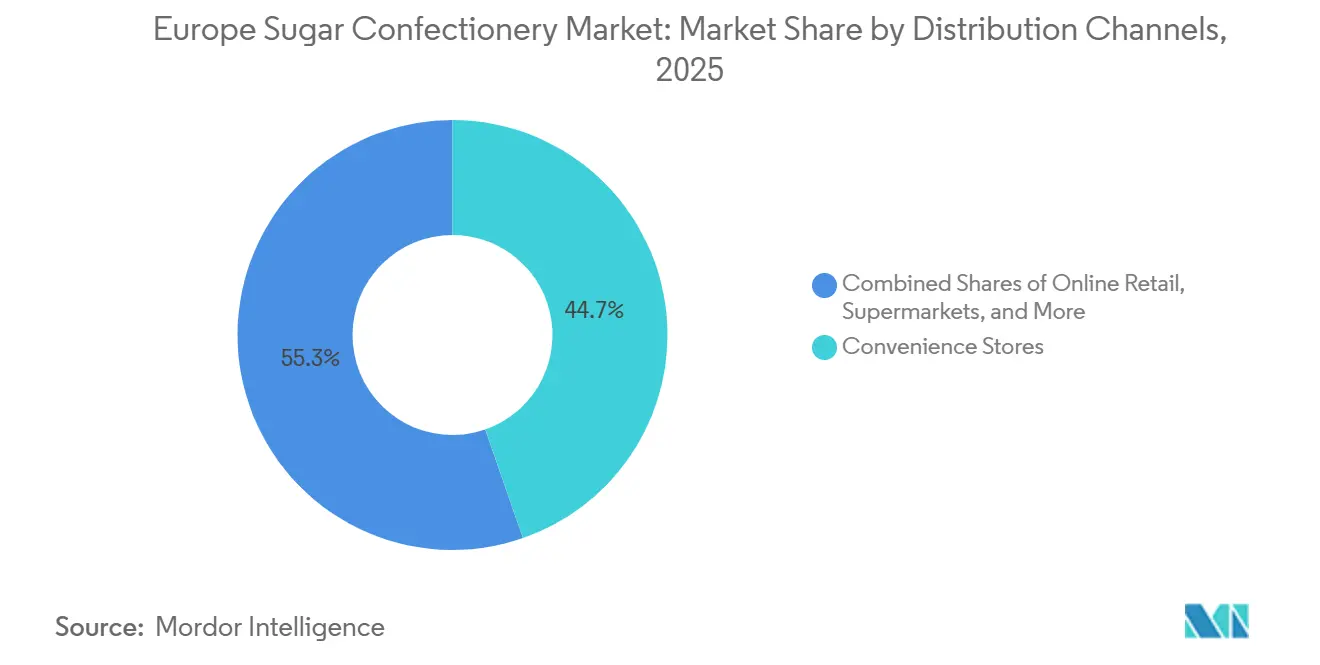

- By distribution channel, convenience stores commanded 44.68% of sales in 2025. Online retail is forecast to deliver a 6.85% CAGR up to 2031.

- By geography, Germany generated 22.88% of regional value in 2025, whereas Turkey is anticipated to expand at an 11.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Sugar Confectionery Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Incomes Enabling Higher Discretionary Spending | +0.9% | Central & Eastern Europe (Poland, Czech Republic, Hungary), Turkey | Medium term (2-4 years) |

| Continuous Product Innovation with New Flavors, Formats, and Healthier Sugar Alternatives | +1.2% | EU-wide, with early adoption in Germany, Netherlands, UK | Short term (≤ 2 years) |

| Increasing Consumer Demand for Premium and Artisanal Confectionery Products | +0.7% | Western Europe (Germany, France, UK, Belgium), urban centers | Long term (≥ 4 years) |

| Seasonal and Festive Occasions Promoting Traditional Confectionery Consumption | +0.6% | Northern & Central Europe (Germany, Netherlands, Belgium), Mediterranean during Easter | Short term (≤ 2 years) |

| Development of Sugar-Free, Vegan, and Natural Ingredient-Based Confectionery | +1.0% | EU-wide, strongest in Nordics, Germany, UK | Medium term (2-4 years) |

| Popularity of Convenient, On-the-Go Snack Formats and Portion Sizes | +0.8% | Urban EU markets, UK, France, Germany, Italy | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes Enabling Higher Discretionary Spending

Disposable income growth in Central and Eastern Europe is unlocking latent demand for branded and imported confectionery, particularly in Poland, the Czech Republic, and Hungary, where wage convergence with Western Europe accelerates. Turkey's per-capita chocolate consumption reached 3.1 kilograms in 2020, ranking fifth globally, and gifting culture around Ramadan drives boxed assortment purchases among middle- and high-income urban consumers. This income elasticity is bifurcating the market: value-conscious shoppers gravitate toward domestic brands and smaller pack sizes, while affluent segments trade up to premium imports and artisanal offerings. The European Commission's Health at a Glance 2024 report noted that diet-related spending patterns are shifting as household budgets accommodate both indulgence and health-oriented purchases, creating dual demand corridors[1]Source: European Commission, Directorate-General for Health and Food Safety. "Health at a Glance 2024." ec.europa.eu. Manufacturers are responding with tiered portfolios that span mass-market impulse packs and limited-edition luxury formats, enabling price segmentation across income cohorts. Seasonal promotions and multi-buy offers further amplify discretionary spending during festive periods, when confectionery penetration peaks.

Continuous Product Innovation with New Flavors, Formats, and Healthier Sugar Alternatives

Flavor proliferation and format experimentation are central to defending shelf space and driving trial. Emsland Group's January 2026 launch of plant-based starch for gelatin-free confectionery exemplifies ingredient innovation targeting vegan and clean-label consumers, enabling gummy manufacturers to reformulate without animal-derived gelatin. HARIBO's seasonal SKU launches, including Unicorn-i-licious and Awesome Axolotls, demonstrate how novelty shapes and limited-time offerings sustain consumer engagement and social-media visibility. Ferrero's May 2024 introduction of Tic Tac Chewy, a fruit-flavored sugar candy with a crunchy-chewy texture, signals diversification beyond chocolate as cocoa futures more than doubled year-to-date, pressuring margins. Alternative sweeteners, erythritol, stevia, and fruit concentrates are gaining regulatory traction; EFSA's 2017 opinion confirmed that sugar-free hard confectionery with at least 90% erythritol reduces dental plaque and caries risk, providing a health-claim pathway for manufacturers.

Increasing Consumer Demand for Premium and Artisanal Confectionery Products

Premiumization is offsetting volume declines in mature markets, with affluent consumers willing to pay higher price points for provenance, ethical sourcing, and experiential packaging. Financial Times reported in April 2025 that premium chocolatiers are achieving stronger margins and sales growth versus mass-market players, driven by single-origin cocoa, bean-to-bar production, and sustainability certifications. Rococo Chocolates exemplifies this trend, sourcing Domori couverture from the Ivory Coast and hand-finishing limited batches in its London Chocolate Kitchen, while offering global e-commerce with loyalty rewards (5 points per GBP 1 spent, 100 points = GBP 1 discount) to cultivate direct relationships. Gifting occasions, Valentine's Day, Easter, and Christmas, amplify premium positioning, with retailers expanding luxury food halls and specialty stores to capture higher-margin sales. Lakrids By Bülow, a Danish premium licorice brand, was acquired by IDG Capital in August 2025 to accelerate global expansion, signaling private-equity appetite for scalable artisan brands.

Seasonal and Festive Occasions Promoting Traditional Confectionery Consumption

Seasonal peaks remain structural demand drivers, with December confectionery trade volumes rising sharply across Northern and Central European member states to meet Christmas demand, as documented by Eurostat. Ramadan in Turkey generates pronounced spikes in boxed assortments and premium imports, with gifting culture elevating confectionery to a social currency during the holiday European Commission. Easter drives gummy and jelly sales in Mediterranean markets, while Valentine's Day sustains chocolate and filled confectionery demand in Western Europe. Retailers expand seasonal assortments and promotional activity in Q4, increasing production and inventory levels to capture holiday purchasing. Manufacturers leverage limited-edition packaging, themed shapes, and co-branding (e.g., Mondelez's March 2025 Cadbury-Lotus Biscoff chocolate bars) to differentiate seasonal offerings and command premium pricing. Supply-chain implications include higher Q4 logistics volumes and tighter lead times, requiring planning and flexible capacity to meet concentrated demand windows.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Government Regulations on Sugar Content, Labeling, and Food Safety | -0.6% | EU-wide, stricter in Nordics, UK, France | Medium term (2-4 years) |

| Increasing Raw Material Costs Including Sugar, Gelatin, and Natural Sweeteners | -0.8% | EU-wide, acute in countries reliant on imports (UK, Italy, Spain) | Short term (≤ 2 years) |

| Rising Health Concerns Linked to Sugar Consumption, Obesity, Diabetes, and Dental Issues | -0.7% | EU-wide, pronounced in Western Europe (Germany, UK, Netherlands) | Long term (≥ 4 years) |

| Competition from Alternative Snacks and Sugar-Free Product Segments | -0.5% | Urban EU markets, UK, Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Government Regulations on Sugar Content, Labeling, and Food Safety

EU Regulation 1169/2011 mandates nutrition declarations including sugars per 100 grams, forcing manufacturers to disclose sugar content prominently and enabling consumer comparisons that can deter high-sugar purchases. EFSA's February 2022 recommendation that added and free sugars should be "as low as possible" provides scientific justification for member-state reformulation targets, front-of-pack labeling schemes, and marketing restrictions to children. The European Commission's December 2015 Added Sugars Annex to the EU Framework for National Initiatives encourages voluntary national programs for sugar reduction, portion-size controls, and public awareness campaigns, creating a patchwork of compliance requirements across member states. Turkey's Turkish Food Codex Regulation on Food Labelling (2017) requires Turkish-language stickers, country-of-origin labeling, and specific warnings for sweeteners (phenylalanine, polyol laxative effects), raising market-entry costs for EU exporters. Advertising restrictions targeting children, such as Turkey's ban on promoting "red-list" foods (chocolate, sweets) during children's programming, limit marketing reach and brand-building opportunities. Compliance costs for testing, labeling updates, and reformulation strain smaller producers, favoring multinationals with scale and regulatory expertise.

Rising Health Concerns Linked to Sugar Consumption, Obesity, Diabetes, and Dental Issues

The WHO's European Childhood Obesity Surveillance Initiative (COSI) sixth-round report (October 2025) documented persistent childhood overweight and obesity prevalence across European countries, reinforcing public-health narratives linking confectionery to adverse health outcomes. EFSA's February 2022 infographic on sugar consumption and health problems emphasized that high intakes of free sugars increase dental caries risk and contribute to excess energy intake, leading to overweight and obesity. The Europe Sustainable Development Report 2025 tracks obesity prevalence (BMI ≥30) as a key SDG indicator, providing policymakers with evidence to justify sugar taxes, marketing restrictions, and reformulation mandates, according to the Sustainable Development Solutions Network. Health taxes targeting sugary products are proliferating, with the European Commission's May 2025 report detailing fiscal measures (excise, ad valorem, per-sugar levies) across member states that raise retail prices and reduce consumption, according to the Publications Office of the European Union[2]Source: Publications Office of the European Union, “Regulation (EU) No 1169/2011 on the Provision of Food Information to Consumers,” eur-lex.europa.eu. Public awareness campaigns and front-of-pack labeling (traffic lights, Nutri-Score) increase transparency, enabling health-conscious consumers to avoid high-sugar products. Dental associations advocate for reduced sugar intake to prevent caries, amplifying negative sentiment around traditional confectionery. Manufacturers are countering with sugar-free and fortified variants, smaller portions, and health-claim positioning (e.g., erythritol dental benefits), but category stigma persists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Gummies Lead, Lollipops Accelerate

Pastilles, gummies, and jellies commanded 41.56% of the European sugar confectionery market in 2025, sustained by texture innovation and flavor variety that appeal to children and adults alike. Lollipops are expanding at 6.45% CAGR through 2031, driven by nostalgia marketing, premium positioning, and gifting occasions. Hard candy, mints, toffees, nougats, and other formats collectively account for the remaining share, each serving distinct consumption occasions and demographic preferences. Emsland Group's January 2026 launch of plant-based starch for gelatin-free gummies addresses vegan demand while maintaining the chewy texture that defines the category, enabling manufacturers to reformulate without animal-derived ingredients. Power mints are gaining traction in convenience and pharmacy channels, positioning as functional breath-freshening solutions with stronger menthol or caffeine content versus standard mints. Toffees and nougats skew toward premium gifting and seasonal assortments, with higher cocoa and nut content commanding elevated price points.

Hard candy remains resilient in value segments and elderly demographics, though volume growth is constrained by health concerns and competition from sugar-free alternatives. EFSA's 2017 health-claim approval for sugar-free hard confectionery with at least 90% erythritol provides a regulatory pathway for dental-health positioning, enabling manufacturers to differentiate in pharmacy and health-food channels[3]Source: European Food Safety Authority, “Sugar-Free Hard Confectionery With at Least 90 % Erythritol and Reduction of Dental Plaque,” efsa.europa.eu. Lollipops benefit from limited-edition collaborations and social-media-driven discovery, with younger consumers willing to pay premium prices for novel shapes, flavors, and packaging. HARIBO's seasonal SKU launches, Unicorn-i-licious, Awesome Axolotls, demonstrate how novelty shapes sustain consumer engagement and trial FoodBev. Mints are bifurcating into power mints and standard mints, with power mints capturing share in on-the-go and workplace consumption occasions. Regulatory compliance under EU Regulation 1333/2008 governs permitted additives and maximum levels, requiring manufacturers to navigate complex authorization processes for novel ingredients .

By Functional Benefit: Novelty Dominates, Fortified Surges

Novelty lines controlled 42.60% of category revenue in 2025, underscoring Europe’s enduring appetite for pure indulgence. The Europe sugar confectionery market size tied to novelty is expected to climb steadily, even as consumer curiosity shifts toward better-for-you claims. Fortified products, forecast at a 7.01% CAGR, inject vitamins, minerals, or botanicals that legitimize treat consumption among wellness-minded shoppers. Digestive and botanical candies appeal to adults who wish to avoid medicinal lozenges yet still desire functional relief. Energy chews containing B-vitamins and caffeine are emerging, targeting gamers and office workers seeking discreet stimulants. Regulatory hurdles for on-pack claims are high, which limits fringe entrants and favors larger firms with scientific validation budgets.

Brand narratives that combine indulgence with tangible wellness succeed in commanding higher shelf prices and in accessing pharmacy aisles traditionally closed to sugar confectionery. Novelty developers exploit licensing tie-ups, pop-culture tie-ins, and augmented-reality packaging that turns unboxing into shareable entertainment. Fortified gummies face taste-masking challenges, yet advances in microencapsulation are improving flavor integrity. Digestive candies use chicory fiber and prebiotic inulin to deliver gut-health benefits without compromising sweetness. The dual focus on cheer and utility ultimately broadens category reach across demographic cohorts and dayparts.

By Distribution Channel: Convenience Stores Anchor, E-commerce Climbs

Convenience outlets generated 44.68% of retail value in 2025, cementing their status as the leading route to market for the Europe sugar confectionery market. High traffic, late hours, and strategic locations near transit hubs fuel spontaneous purchases of single-serve packs. Supermarkets and hypermarkets contribute large absolute volumes through family bags and seasonal multipacks, though they exert significant price pressure via private label. Online retail is on a 6.85% CAGR trajectory through 2031, aided by subscription boxes, direct-to-consumer storefronts, and rapid-delivery applications. Pure-play e-tailers leverage data-driven personalization to upsell novelty bundles and limited runs that are unavailable in brick-and-mortar stores.

Cross-channel behaviors are blurring; 53% of consumers already use three or more shopping avenues for snacks in a typical month. Petrol stations and vending continue to supply late-night cravings but are also experimenting with premium mini-ranges that raise margins. Specialty stores and luxury food halls remain vital for artisanal brands that rely on storytelling and tastings. As unified commerce advances, inventory transparency and last-mile delivery speed become differentiators, encouraging manufacturers to invest in digital twins of their supply chains.

Geography Analysis

Germany anchored 22.88% of the European sugar confectionery market in 2025, sustained by high per-capita consumption, robust retail infrastructure, and strong domestic brands (HARIBO, Katjes, Storck). Turkey is surging at 11.12% CAGR through 2031, underpinned by a gifting culture around Ramadan, rising middle-class purchasing power, and per-capita chocolate consumption of 3.1 kilograms. France, the United Kingdom, Italy, Spain, the Netherlands, Belgium, and Russia collectively represent significant shares, each exhibiting distinct consumption patterns shaped by cultural preferences, regulatory environments, and economic conditions. HARIBO's GBP 22 million (USD 28 million) investment in its Castleford, West Yorkshire facility underscores the UK's strategic importance as a manufacturing hub serving Northern European markets. The rest of Europe, comprising Poland, the Czech Republic, Hungary, the Nordics, and the Balkans, is experiencing income-driven demand growth, particularly in Central and Eastern Europe, where wage convergence with Western Europe unlocks discretionary spending on branded confectionery.

Turkey's chocolate confectionery market reached EUR 1.36 billion in 2020, with countlines (EUR 586 million) and tablets (EUR 558 million) leading, while sugar confectionery segments included gum (EUR 246 million), other sugar confectionery (EUR 194 million), and pastilles/jellies/chews (EUR 112 million). European Commission. Germany's confectionery sector benefits from advanced manufacturing, innovation ecosystems (ingredient suppliers, packaging specialists), and export-oriented production serving EU and global markets. France and Belgium leverage chocolate heritage and artisan positioning, commanding premium pricing in luxury segments. The UK faces post-Brexit trade frictions and currency volatility, yet remains a major consumer market with strong retail concentration (Tesco, Sainsbury's, Asda) and impulse-channel penetration. Italy and Spain exhibit Mediterranean consumption patterns, with seasonal peaks around Easter and Christmas, and a preference for nougat, torrone, and filled chocolates.

Russia's market dynamics are shaped by import substitution policies, local production expansion, and geopolitical sanctions affecting ingredient sourcing and trade flows. The Netherlands serves as a logistics hub for pan-European distribution, with Rotterdam port facilitating cocoa, sugar, and finished goods imports. Poland, the Czech Republic, and Hungary are experiencing rapid income growth, driving premiumization and branded penetration at the expense of bulk and unbranded confectionery. Nordics (Sweden, Denmark, Finland, Norway) exhibit high health consciousness, favoring sugar-free, organic, and sustainably sourced products, with licorice (Lakrids By Bülow) and premium chocolate (Fazer) commanding strong local loyalty. Balkans (Greece, Romania, Bulgaria) represent emerging opportunities with lower per-capita consumption and fragmented retail, requiring localized distribution partnerships and price-competitive offerings. Regulatory harmonization under EU food law (Regulations 1169/2011, 1333/2008, Directive 2000/36/EC) facilitates cross-border trade within the EU, yet member-state variations in health taxes, labeling requirements, and marketing restrictions create compliance complexity for pan-European strategies.

Competitive Landscape

Top Companies in Europe Sugar Confectionery Market

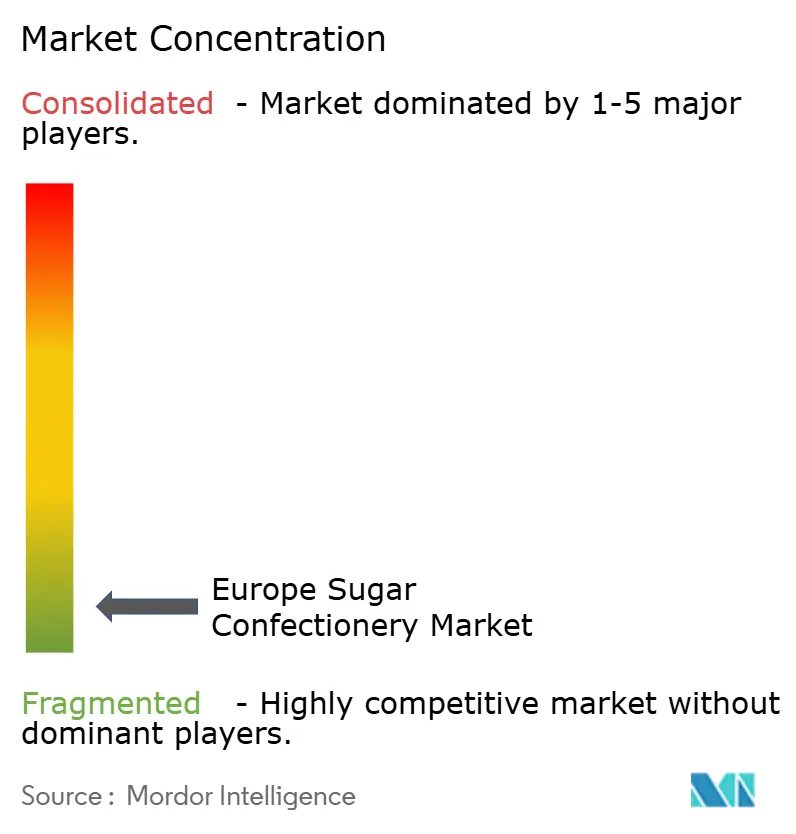

The European sugar confectionery market exhibits extreme fragmentation (concentration score 1 out of 10), with multinational incumbents (HARIBO, Mondelez, Ferrero, Mars, Perfetti Van Melle) competing alongside regional specialists (Cloetta, Katjes, Ricola, Storck) and artisan entrants (Lakrids By Bülow, Rococo Chocolates). Mars announced a EUR 1 billion investment in European capacity in September 2025, signaling a long-term commitment despite unresolved M&A dynamics with Kellanova Euronews. Mondelez faced a EUR 365.7 million EU fine in May 2024 for cross-border trade restrictions, underscoring regulatory enforcement shaping competitive conduct and distribution strategies.

Strategy patterns include portfolio diversification (Ferrero's Tic Tac Chewy sugar candy launch in May 2024 amid cocoa-cost pressure), brand licensing (Mondelez-Lotus Bakeries Cadbury-Biscoff collaboration in March 2025), and geographic expansion (Hershey's 2019 Fulfil Nutrition acquisition targeting European protein-snack growth). White-space opportunities include fortified confectionery (vitamins, botanicals), sugar-free premium tiers, and direct-to-consumer subscription models that bypass retail gatekeepers. Emerging disruptors, plant-based ingredient suppliers (Emsland Group), premium licorice brands (Lakrids By Bülow post-IDG Capital acquisition in August 2025), and functional-snack crossovers, are unsettling incumbents by targeting health-conscious and sustainability-driven consumers.

and Technology adoption, digital marketing, e-commerce platforms, supply-chain analytics, enable agile SKU launches and targeted promotions, with social media driving 55% of consumers to try new snacks (70% Gen Z, 71% millennials) per Mondelez's 2021 study. Compliance with EU Regulation 1333/2008 (food additives) and Directive 2000/36/EC (cocoa and chocolate products) governs ingredient use and labeling, creating barriers to entry for smaller players lacking regulatory expertise.

Europe Sugar Confectionery Industry Leaders

-

HARIBO Holding GmbH & Co. KG

-

Mondelēz International Inc.

-

Nestlé SA

-

Perfetti Van Melle BV

-

Ricola AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Roly's Fudge launched its seasonal Toffee Apple flavor ahead of Bonfire Night, capturing the nostalgic taste of caramelized apples with a crumbly, handmade texture using natural ingredients.

- July 2025: Premier Foods launched McDougalls No Added Sugar Vegan Jelly, targeting UK schools with HFSS-compliant, gluten-free, and allergen-free options in strawberry, raspberry, orange, and lime flavors.

- June 2025: World of Sweets and Bobby's launched Gumi Yum Surprise, a novelty gummy candy egg in the UK, featuring eight fruit-flavored layers (cherry, strawberry, orange, pineapple, lemon, green apple, blue raspberry, grape) encasing collectible toys from Zuru, like wildlife or transformer characters.

- May 2025: Ruly brand launched its caffeine-infused sweets in the United Kingdom, targeting busy professionals and fitness enthusiasts with a functional alternative to energy drinks. The lightning bolt-shaped candies come in Tropical Crush and Berry Delicious flavors; each 42g pack delivers 80mg caffeine from guarana plus B vitamins for jitter-free, micro-dosed energy boosts.

Europe Sugar Confectionery Market Report Scope

Hard Candy, Lollipops, Mints, Pastilles, Gummies, and Jellies, Toffees and Nougats, Others are covered as segments by Confectionery Variant. Convenience Store, Online Retail Store, Supermarket/Hypermarket, Others are covered as segments by Distribution Channel. Belgium, France, Germany, Italy, Netherlands, Russia, Spain, Switzerland, Turkey, United Kingdom are covered as segments by Country.| Hard Candy | |

| Mints | Power Mints |

| Standard Mints | |

| Pastilles, Gummies, and Jellies | |

| Toffees and Nougats | |

| Lollipops | |

| Others |

| Novelty |

| Fortified |

| Digestive / Botanicals |

| Others |

| Supermarket/Hypermarket |

| Online Retail Store |

| Convenience Store |

| Other Distribution Channels |

| Belgium |

| France |

| Germany |

| Italy |

| Netherlands |

| Russia |

| Spain |

| Turkey |

| United Kingdom |

| Rest of Europe |

| Type | Hard Candy | |

| Mints | Power Mints | |

| Standard Mints | ||

| Pastilles, Gummies, and Jellies | ||

| Toffees and Nougats | ||

| Lollipops | ||

| Others | ||

| Functional Benefit | Novelty | |

| Fortified | ||

| Digestive / Botanicals | ||

| Others | ||

| Distribution Channel | Supermarket/Hypermarket | |

| Online Retail Store | ||

| Convenience Store | ||

| Other Distribution Channels | ||

| Geography | Belgium | |

| France | ||

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| United Kingdom | ||

| Rest of Europe | ||

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms