Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

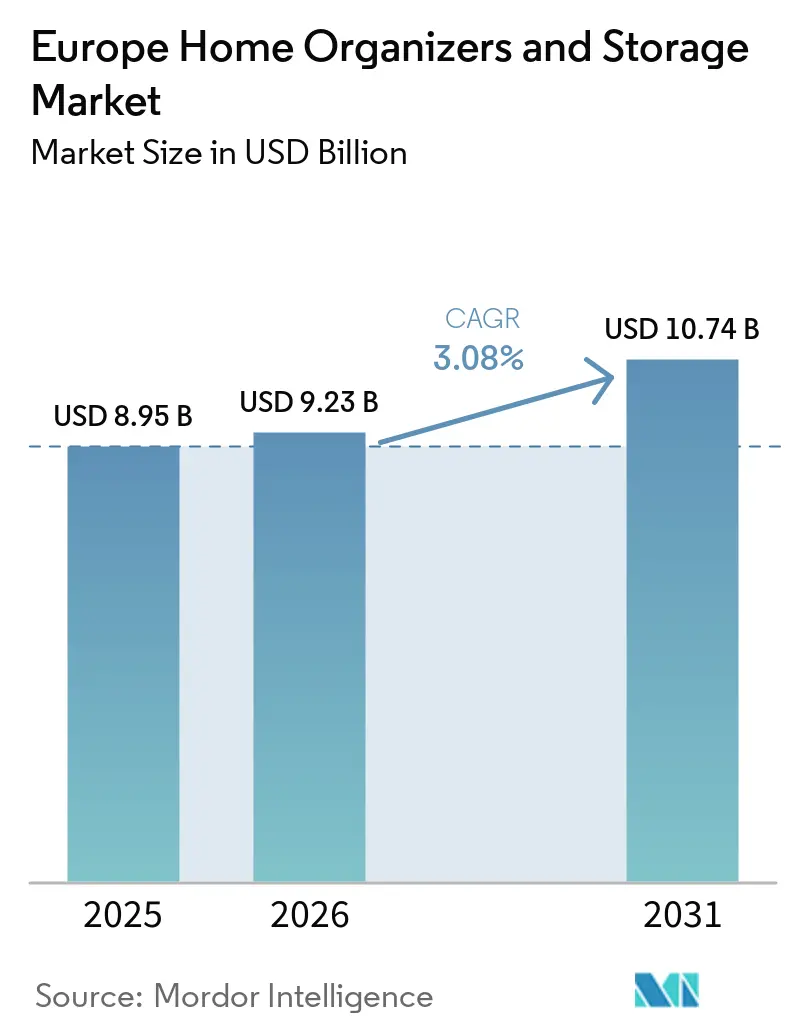

| Base Year Market Size (2025) | USD 8.95 Billion |

| Market Size (2026) | USD 9.23 Billion |

| Market Size (2031) | USD 10.74 Billion |

| Growth Rate (2026 - 2031) | 3.08% CAGR |

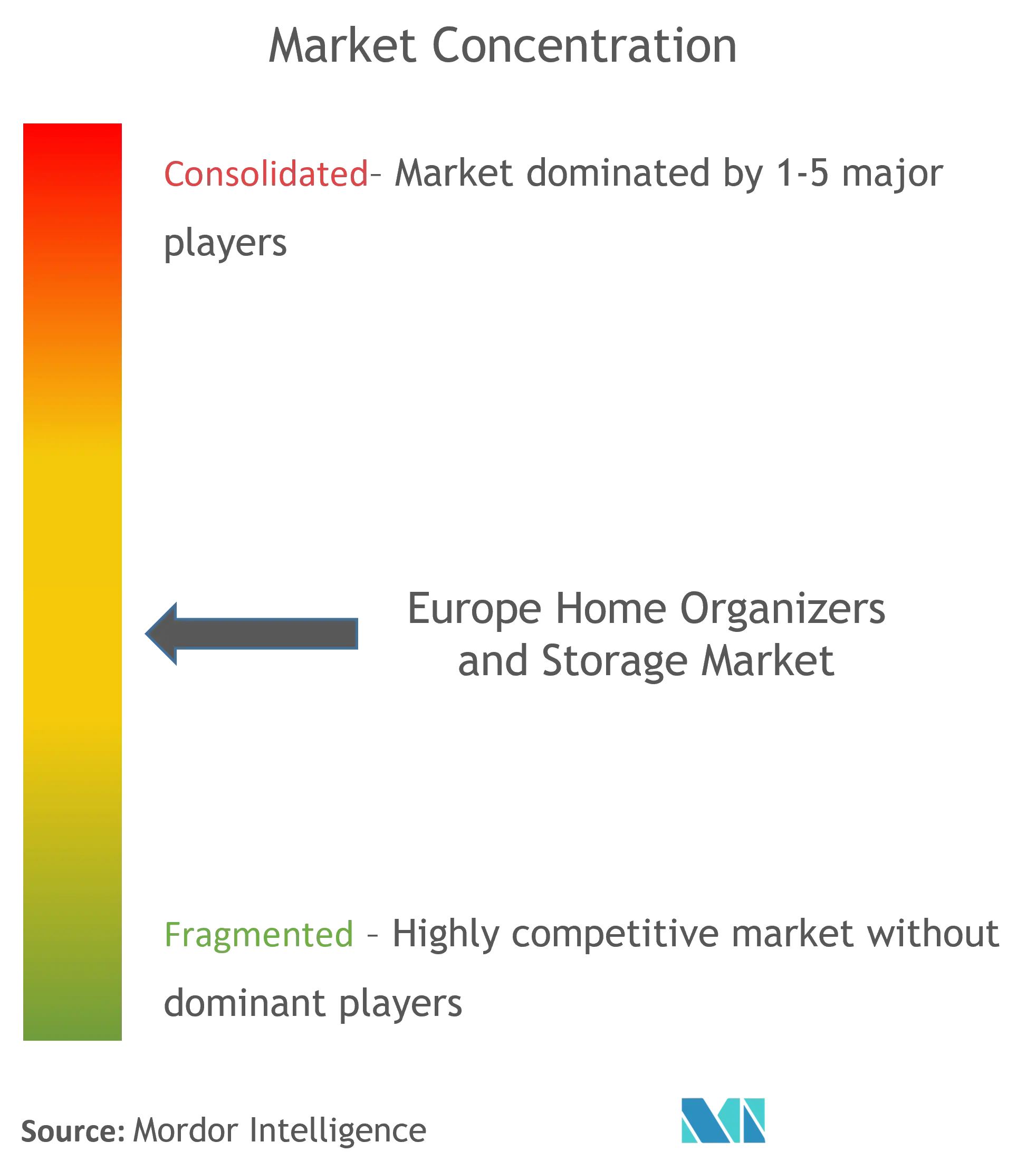

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Home Organizers and Storage Market Analysis by Mordor Intelligence

The home organizers and storage market size in Europe in 2026 is estimated at USD 9.23 billion, growing from 2025 value of USD 8.95 billion with 2031 projections showing USD 10.74 billion, growing at 3.08% CAGR over 2026-2031. Sustained growth stems from rising consumer focus on space optimization, widening adoption of modular storage, and policy support for circular‐design products. DIY engagement across the region encourages demand for ready-to-assemble organizers, while e-commerce infrastructure shortens discovery cycles for niche solutions. Premiumization lifts average selling prices as buyers seek materials and aesthetics matching interior upgrades. At the same time, companies face margin pressure from raw-material inflation and regulatory scrutiny on plastics, prompting a shift toward recyclable inputs and asset-light sourcing models. Competitive intensity remains moderate; scale players expand store networks and omnichannel services while newcomers penetrate online verticals, keeping the home organizers and storage market dynamic.

Key Report Takeaways

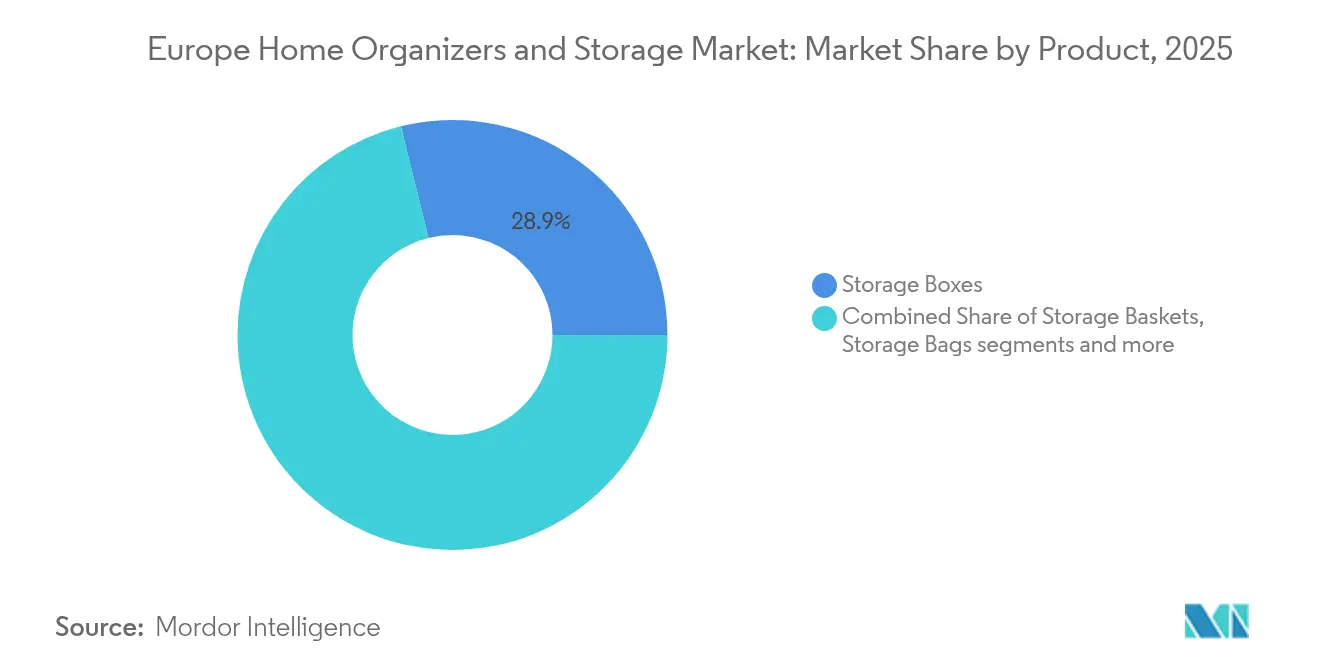

- By product category, Storage Boxes commanded 28.86% of the home organizers and storage market share in 2025. Modular Units are projected to expand at a 4.52% CAGR to 2031, the fastest rate among product segments.

- By application, Bedroom Closets led with 33.15% revenue share in 2025. Home Office storage is forecast to record the highest 4.89% CAGR through 2031.

- By distribution channel, Hypermarkets and Supermarkets held 46.78% of the home organizers and storage market size in 2025. Online channels are expected to advance at a 5.62% CAGR, the swiftest among channels.

- By geography, the United Kingdom accounted for a 12.98% share in 2025. BENELUX is anticipated to achieve the fastest 4.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Europe Home Organizers and Storage Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising DIY & Home-Improvement Culture | +0.8% | United Kingdom, Germany, NORDICS | Medium term (2-4 years) |

| Premiumization of Home Storage Products | +0.6% | United Kingdom, Germany, France, BENELUX | Long term (≥ 4 years) |

| Ageing Population Requiring Ergonomic Storage | +0.5% | NORDICS, Germany, Italy | Long term (≥ 4 years) |

| Circular-Economy Driven Modular Designs | +0.4% | EU-wide, led by Netherlands, Germany, France | Medium term (2-4 years) |

| Influencer-Led Micro-Organizing Trends | +0.3% | Urban centers across Europe | Short term (≤ 2 years) |

| Rise of Urban Micro-Apartments | +0.6% | London, Paris, Berlin, Amsterdam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising DIY & Home-Improvement Culture

European households channel discretionary budgets into self-directed renovations as inflation encourages cost-saving home upgrades. The regional DIY segment is forecast to gain USD 32.9 billion between 2025 and 2029 at a 3.2% CAGR, creating steady demand for flat-pack organizers[1]Insight DIY, “IKEA Launches Circular Campaign to Inspire Customers,” insightdiy.co.uk. How-to videos and retailer tutorials lower skill barriers, letting first-time buyers install modular closets without professional help. Retailers respond with QR-coded assembly guides and click-to-buy parts lists that simplify complex builds. IKEA’s “Keep good things going” program reused 32.5 million pre-owned products in 2025, showing how DIY culture supports circular goals. Weekend project enthusiasm also lifts ancillary sales of screws, liners, and labelling kits, making storage one of the fastest-turning categories in big-box home centers. As consumer confidence stabilizes, DIY momentum is expected to remain a reliable volume driver through 2030.

Premiumization of Home Storage Products

The multifunctional home pushes buyers to view organizers as décor elements rather than utility bins. Consumers increasingly pay for solid-wood drawers, powder-coated steel frames, and soft-close hinges that match furniture quality standards. Retailers like The Container Store expand Custom Spaces offerings that embed LED lighting and sustainable veneers, raising average ticket sizes. Premium finishes complement rising interest in interior design, a trend amplified by social media tours of “perfect pantries” and color-coordinated closets. Higher price points create margin headroom that offsets raw-material inflation while funding store-level design consultations. Durability also speaks to environmental priorities because longer product life reduces replacement frequency. Premiumization, therefore, serves economic, aesthetic, and sustainability objectives simultaneously, reinforcing its status as a structural growth lever.

Ageing Population Requiring Ergonomic Storage

Europe’s median age continues to rise, compelling manufacturers to prioritize accessibility in product design. Slide-out kitchen shelves, waist-height shoe racks, and push-to-open lids reduce bending and lifting for older adults. German and Italian households, where senior cohorts exceed one-fifth of residents, are early adopters of such features. Brands add large-print labels and soft-touch handles that also appeal to younger users seeking convenience. Universal design lowers the need for age-specific SKUs, letting suppliers achieve scale efficiencies while meeting inclusive design mandates. Health-focused insurers increasingly reimburse ergonomic home modifications, indirectly stimulating organizer purchases. By aligning health, comfort, and mainstream aesthetics, ergonomic storage is positioned for sustained demand across demographic segments.

Circular-Economy Driven Modular Designs

The EU Ecodesign for Sustainable Products Regulation introduces Digital Product Passports from 2025, requiring traceability of materials and end-of-life pathways[2]European Commission, “Ecodesign for Sustainable Products Regulation,” europa.eu. Manufacturers overhaul portfolios to favor mono-material panels, tool-free connections, and replaceable parts that simplify repair. IKEA pilots chemical foam recycling for mattresses, illustrating closed-loop principles that can migrate to plastic drawer components. Compliance elevates entry barriers for low-cost imports lacking documentation, steering buyers toward established European brands. Modular units inherently support longevity because damaged sections can be swapped without discarding entire systems. Retailers monetize the shift through buy-back credits and refurbishment services that extend customer lifetime value. As regulations tighten, circular design is expected to transition from a niche differentiator to a baseline market requirement.

Restraints Impact Analysis of Europe Home Organizers and Storage Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Cost Inflation | -0.4% | Eastern Europe manufacturing hubs | Short term (≤ 2 years) |

| Slowdown in New Housing Starts | -0.3% | United Kingdom, Germany, France | Medium term (2-4 years) |

| Sustainability Scrutiny on Plastics | -0.2% | NORDICS, Netherlands, EU-wide | Medium term (2-4 years) |

| Rental Furniture & Storage-as-a-Service Models | -0.2% | London, Paris, Berlin, Amsterdam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Cost Inflation

Surging freight rates and resin prices squeeze margins, especially for mass-market plastic bins where consumers resist price hikes. Griffon’s ClosetMaid division reported a 52% revenue drop in Europe between 2022 and 2023, citing weak demand and excess inventories built during logistics disruptions. To recover profitability, suppliers shorten bill-of-materials lists and localize component sourcing, but tooling changes raise upfront costs. Currency volatility further complicates cost planning for manufacturers reliant on Asian inputs. Retailers attempt to pass higher costs to consumers through “eco-upgrade” positioning, yet elastic segments experience volume declines when price thresholds are breached. Some brands hedge by shifting to lighter packaging that lowers dimensional weight charges, though material substitutions risk customer perception of reduced quality. Until freight indices normalize, cost inflation remains a prominent profitability headwind.

Slowdown in New Housing Starts

Building permits fell across the United Kingdom, Germany, and France in 2024, dampening demand for first-fit closet systems typically installed during construction[3]Eurostat, “Building Permits Annual Data,” eurostat.ec.europa.eu. Developers facing higher financing costs slow project pipelines, reducing bulk orders for built-in wardrobes. Suppliers pivot to renovation-friendly, freestanding pieces that appeal to homeowners improving existing spaces rather than moving. Average order values dip because retrofit projects seldom match the scale of furnishing an empty house. Retail partnerships with mortgage lenders and energy-retrofit programs aim to retrieve some lost volume by bundling storage with efficiency upgrades. However, the replacement cycle is lengthier than new-build cycles, lengthening revenue recovery timelines. Unless housing activity rebounds, the organizer market will rely on discretionary remodel spending to offset this structural restraint.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Europe Home Organizers and Storage Market Segment Analysis

By Product:

Modular Innovation Broadens ChoiceModular Units are projected to deliver the steepest 4.52% CAGR through 2031, reflecting rising preference for components that expand with household needs. Storage Boxes remain the largest contributor, holding 28.86% of the home organizers and storage market share in 2025. The home organizers and storage market size devoted to Boxes equaled USD 2.58 billion that year, underpinning category stability. Consumers favor clear polypropylene totes for seasonal clothing rotation and heavy-duty corrugate boxes for long-term attic storage. Manufacturers differentiate through stackability indexes and reinforced lids to support warehouse-style vertical storage.

Urban renters gravitate toward modular cubes that fit studio apartments as bookcases today and shoe racks tomorrow, underscoring the value of reconfiguration. Players such as STOCUBO promote tool-free connectors and 1 cm increment sizing that lets buyers build wall-to-wall libraries without custom carpentry. Travel luggage organizers and hanging fabric compartments post steady gains by targeting specific pain points like suitcase packing and door-mounted accessory storage. As circular design moves mainstream, brands highlight component replacement programs that extend unit life and cement customer loyalty within the home organizers and storage market.

By Application:

Home Office Momentum PersistsBedroom Closets dominate revenue at 33.15% because clothing management remains a universal need across household types. However, the surge in remote work sustains a 4.89% CAGR for Home Office organizers, the quickest among applications. The home organizers and storage market size captured by Home Office solutions was USD 1.03 billion in 2025 and is primed for continued expansion as hybrid schedules normalize. Built-in cable channels, lockable document drawers, and modular monitor stands differentiate these offerings from legacy stationery trays.

Kitchen Pantries hold mid-teens share as meal-prep culture fuels demand for bulk-ingredient canisters and tiered spice racks. Laundry Room products appeal to households seeking tidy segregation of detergents, ironing tools, and folded linens, though growth remains modest. Garage organizers cater to hobbyists and DIY enthusiasts wanting ceiling-mounted racks for bikes or wall grids for power tools. Suppliers bundling task-specific accessories into unified systems earn cross-selling advantages.

By Distribution Channel:

Digital Convenience AcceleratesTraditional Hypermarkets and Supermarkets retained a 46.78% share in 2025 through one-stop shopping convenience and immediate gratification. In contrast, Online channels will register a 5.62% CAGR, gaining the most ground among outlets. E-commerce penetration into furniture and homeware reached 39.9% in the United Kingdom in 2024, proving consumer comfort with sight-unseen purchases when accurate dimensions and load-bearing specs are provided. The home organizers and storage market benefits from augmented-reality apps that preview shelf layouts and capacity calculators that suggest bundle sizes.

Specialty Stores defend share by showcasing material samples and offering in-store design consultations. Omni-channel pioneers like JYSK deploy click-and-collect lockers inside grocery parking lots to merge digital ordering with quick pickup. Subscription and rental channels emerge in metropolitan cores where renters value mobility; providers supply rotating bins or wardrobe units on monthly contracts, a service aligned with circular economy objectives.

Geography Analysis

United Kingdom Home Organizers and Storage Market

The United Kingdom held 12.98% of regional revenue in 2025 thanks to mature e-commerce logistics, steady DIY participation, and elevated urban density that heightens the need for multi-purpose storage solutions. Online platforms such as Argos and Wayfair attract traffic by bundling price comparisons and delivery-date certainty. Regulatory commitments to net-zero homes stimulate demand for organizers made of certified timber and recycled plastics, steering producers toward sustainable sourcing.

Germany and France Home Organizers and Storage Market

Germany and France together form a sizeable core where manufacturing heritage and design sensibilities define consumer choice. German households reward engineering precision, favoring organizers with load certificates and TÜV markings, while French buyers lean toward visual harmony with interior palettes. Both markets track national programs that subsidize energy-efficient renovations, indirectly boosting storage upgrades tied to broader refurbishments.

BENELUX Home Organizers and Storage Market

BENELUX is projected to secure the fastest 4.66% CAGR through 2031, powered by Amsterdam’s micro-apartment boom and Brussels’s circular economy road map. Dutch consumers embrace premium modular solutions, allocating budget to design-forward systems that travel across rental moves. Europe self storage infrastructure provides flexible overflow capacity for the region's renters. Belgium leverages its logistics corridors to host regional distribution centers, shortening delivery lead times and reducing last-mile carbon footprints. Luxembourg’s high disposable income and expatriate population support sales of convertible organizers with global design cues.

Southern Europe and Nordics Home Organizers and Storage Market

Southern Europe shows recovering momentum. Italy’s older building stock creates demand for slimline wardrobes that bypass narrow staircases, while Spain’s coastal tourism rebound lifts sales of travel cubes and rental-friendly storage boxes. The NORDICS post above-average adoption of FSC-certified wood organizers, reflecting societal alignment with low-impact living. Overall, geographic diversification moderates cyclical swings, underpinning resilience in the broader home organizers and storage market.

Competitive Landscape

Market structure remains moderately fragmented; the five largest manufacturers and retailers together control roughly half of revenue, leaving room for regional specialists. JYSK demonstrated scale advantage by lifting 2024 turnover to DKK 41.4 billion, opening 137 new European stores, and integrating omnichannel fulfillment that shortens delivery windows to under two days in major capitals. IKEA sustains share through flat-pack efficiency and an expanding Buy-Back service that incentivizes product returns for refurbishment, aligning with upcoming digital passport mandates.

Digital native brands enter with direct-to-consumer subscription models, offering modular desks or wardrobe add-ons delivered at predefined intervals. Enky’s guaranteed buyback service appeals to corporate clients seeking flexible furniture packages that satisfy ESG goals. Traditional closet makers respond by embedding 3D design software on their websites, allowing customers to configure wall cavities and receive instant quotes. Automation adoption in warehouses—such as Kardex vertical lift modules—cuts picking times and enhances order accuracy for small-item bins and drawer inserts.

Strategic partnerships expand addressable audiences. Storebox merged with LOVESPACE to form Spectrum Storage Group, combining locker networks and self-storage rooms that double as last-mile hubs for e-commerce returns. Safestore’s entry into Italy via Easybox acquisition shows cross-border consolidation potential in under-penetrated self-storage markets. Looking ahead, compliance readiness for digital product passports and recyclable material mandates will separate leaders from laggards as European consumers scrutinize product provenance within the home organizers and storage market.

Europe Home Organizers and Storage Industry Leaders

IKEA Group

Elfa International AB

JYSK A/S

Brabantia Branding BV

Orthex Group

- *Disclaimer: Major Players sorted in no particular order

Europe Home Organizers and Storage Market Companies Covered in this Report

- IKEA Group

- Elfa International AB

- JYSK A/S

- Brabantia Branding BV

- Orthex Group

- Hettich Holding GmbH

- Hafele SE & Co KG

- Curver (Keter Group)

- Whitmor Inc.

- The Container Store Group Inc.

- Blum GmbH

- John Lewis PLC

- Leroy Merlin SA

- Muji Europe Holdings Ltd.

- Umbra LLC

- Tiger (Flying Tiger Copenhagen)

- Addis Housewares Ltd.

- Plast Team

- Wenko-Wenselaar GmbH

- Really Useful Products Ltd.

- H&M Home

Read Analysis of Europe Home Organizers and Storage Companies

Recent Industry Developments in Europe Home Organizers and Storage Market

- Jan 2025: Storage Giant announced plans for 11 new facilities across North Wales and North West England after posting its strongest revenue and customer gains to date. Three of the projects will open within 2025, reinforcing the brand’s strategy of serving secondary cities with affordable, drive-up units.

- Dec 2024: Safestore and Nuveen Real Estate set up a EUR 175 million joint venture to enter Italy by purchasing Easybox, the nation’s second-largest operator by site count. The move gives Safestore 55 locations in an under-penetrated market where self-storage density is one-tenth of the U.K. level.

- July 2024: Storebox merged with U.K. operator LOVESPACE to create Spectrum Storage Group, the largest omnichannel self-storage platform in the country. The new entity intends to add capacity through organic builds and targeted acquisitions, integrating lockers for e-commerce returns and traditional rooms under a single reservation system.

- June 2024: Self Storage Group paid NOK 320 million to acquire Eurobox Minilager AS and its four climate-controlled properties around Oslo. The deal expands the buyer’s lettable area by 10,800 square meters and consolidates its leadership in Norway’s capital region.

Europe Home Organizers and Storage Market Report Scope

The report provides the scope of the market along with primary growth factors and offers major market insights. The Europe Organizers and Storage Market report covers a brief overview of the segments and sub-segmentations including the product types, applications, companies and countries. This report describes the market size by analyzing historical data and future forecasts. The Europe Home Organizers and Storage Market is segmented by Product (Storage Baskets, Storage Boxes, Storage Bags, Hanging Stores, Multipurpose Organizers, Travel Luggage Organizers, and Others), by Application (Bedroom Closets, Laundry Rooms, Home Offices, Pantries and Kitchen, Garages, and Others), and by Geography (UK, Germany, France, Italy, Spain, Russia, and Rest of Europe).

Segmentation Overview

By Product

| Storage Baskets |

| Storage Boxes |

| Storage Bags |

| Hanging Storage |

| Multipurpose Organizers |

| Travel Luggage Organizers |

| Modular Units |

| Other Products |

By Application

| Bedroom Closets |

| Laundry Rooms |

| Home Offices |

| Pantries and Kitchen |

| Garages |

| Other Applications |

By Distribution Channel

| Hypermarkets and Supermarkets |

| Specialty Stores |

| Online |

| Other Distribution Channels |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Product | Storage Baskets |

| Storage Boxes | |

| Storage Bags | |

| Hanging Storage | |

| Multipurpose Organizers | |

| Travel Luggage Organizers | |

| Modular Units | |

| Other Products | |

| By Application | Bedroom Closets |

| Laundry Rooms | |

| Home Offices | |

| Pantries and Kitchen | |

| Garages | |

| Other Applications | |

| By Distribution Channel | Hypermarkets and Supermarkets |

| Specialty Stores | |

| Online | |

| Other Distribution Channels | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the European home organizers and storage market in 2026?

The market is valued at USD 9.23 billion in 2026 and is forecast to reach USD 10.74 billion by 2031.

Which product category holds the highest share?

Storage Boxes lead with 28.86% of revenue in 2025.

Which segment is growing fastest?

Modular Units are expected to post a 4.52% CAGR through 2031.

What is driving online sales of organizers?

Greater product variety, easy comparison, and high e-commerce penetration—39.9% in U.K. furniture and homeware—support online expansion at a 5.62% CAGR.

Which country is the leading market in Europe?

The United Kingdom accounts for 12.98% of regional revenue.

How will EU regulations impact suppliers?

The upcoming Digital Product Passport under the Ecodesign Regulation will require traceability of materials, favoring manufacturers that design for repairability and recycling.

Page last updated on: