Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 27 Billion |

| Market Size (2026) | USD 28.09 Billion |

| Market Size (2031) | USD 34.21 Billion |

| Growth Rate (2026 - 2031) | 4.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Self-storage Market Analysis by Mordor Intelligence

The Europe self-storage market size was valued at USD 27 billion in 2025 and estimated to grow from USD 28.09 billion in 2026 to reach USD 34.21 billion by 2031, at a CAGR of 4.02% during the forecast period (2026-2031). Expansion rests on steady urban population growth, rising residential mobility, and institutional capital inflows that treat storage assets as infrastructure rather than peripheral real-estate plays. Urban compression in London, Paris, Berlin, and similar Tier-1 cities, coupled with ageing populations downsizing, keeps occupancy and rental levels resilient across economic cycles. Small and medium e-commerce businesses increasingly adopt micro-warehousing strategies, while student and expatriate mobility supplies predictable seasonal demand. Climate-policy-driven retrofits, although costly, improve energy efficiency and create a premium segment that lifts yields for compliant facilities

Key Report Takeaways

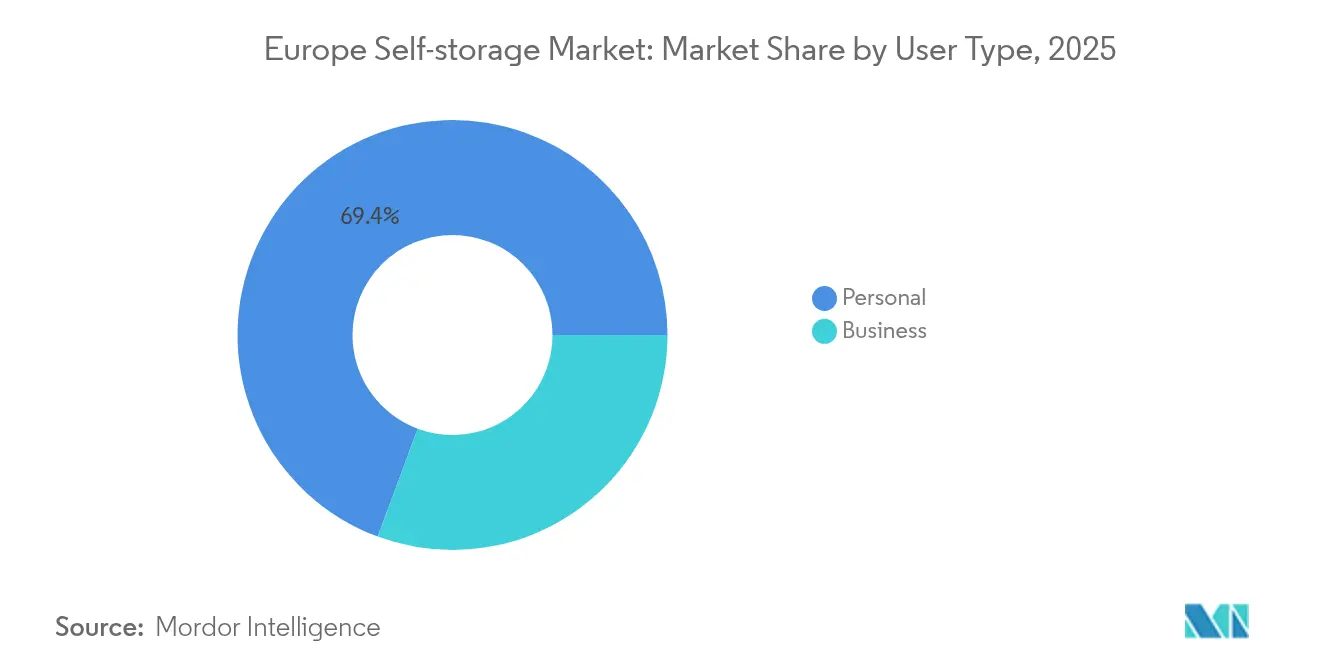

- By user type, personal users held 69.35% of the Europe self-storage market share in 2025; business users are rising at a 7.42% CAGR through 2031.

- By storage type, non-climate-controlled units captured 59.35% of revenue in 2025, while climate-controlled units are advancing at a 8.82% CAGR to 2031.

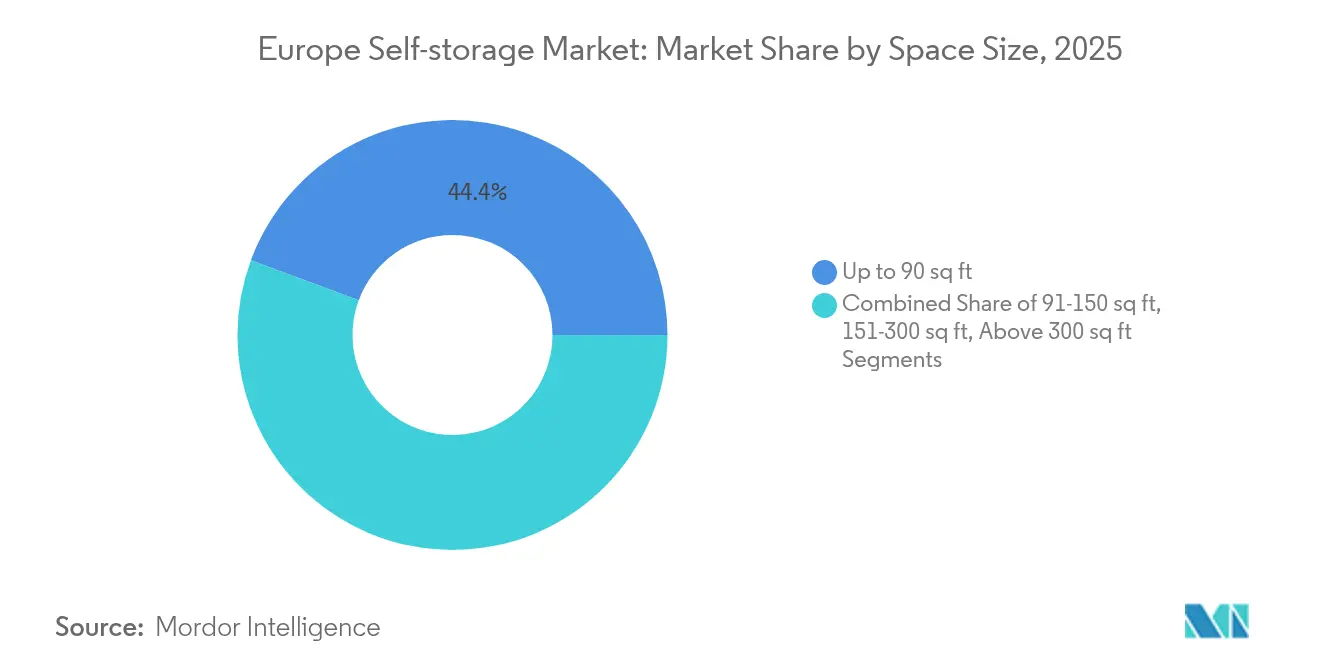

- By space size, units ≤90 sq ft accounted for 44.35% of the Europe self-storage market size in 2025; 151-300 sq ft units expand fastest at an 7.86% CAGR.

- By application, household goods dominated with 61.25% of the Europe self-storage market share in 2025; e-commerce micro-fulfilment should post a 10.05% CAGR to 2031.

- By country, the United Kingdom led with 33.60% of revenue in 2025, whereas Spain is set to grow at an 8.16% CAGR.

- Shurgard, Safestore, Big Yellow, and Access Self Storage jointly controlled ~28% of occupied floor area in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Self-storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban compression and micro-living | +0.8% | UK, France, Germany core cities | Medium term (2–4 years) |

| Ageing population downsizing | +0.6% | Germany, Italy, UK | Long term (≥ 4 years) |

| E-commerce SMB boom | +0.9% | UK, Netherlands | Short term (≤ 2 years) |

| Student & expat mobility | +0.4% | Schengen university hubs | Medium term (2–4 years) |

| Hybrid-work home-office clutter | +0.5% | Major metros | Short term (≤ 2 years) |

| Institutional investor appetite | +0.7% | UK, Germany, France, Netherlands | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Urban compression and micro-living

Intensifying land prices have shrunk average city dwellings, prompting residents to treat local storage facilities as an external “room.” Over 100 new complexes opened in the UK in three years, earning operators GBP 1 billion annually as renters off-load furniture and seasonal goods. Hybrid leases and 24/7 digital access further embed the service into day-to-day urban living.

Ageing population downsizing from larger homes

Older homeowners in Germany, Italy, and the UK are shifting to smaller dwellings, creating interim storage demand for heirlooms and bulky furniture. OECD projections show the 65+ cohort reaching 25% of G7 city dwellers by 2050, locking in a durable, needs-based customer base

E-commerce SMB boom driving flexible micro-warehousing

Quick-commerce revenues in Europe are projected to triple to EUR 72 billion by 2025, yet traditional warehouses remain oversized for SMBs. Facilities now integrate barcode inventory apps, last-mile courier bays, and flexible lease lengths, converting idle units into profitable micro-fulfilment nodes

Student & expat mobility

Cross-border education and work visas translate into term-time storage peaks. Operators near railway corridors and airports advertise semester packages and multilingual contracts, capturing this transient segment that renews predictably each academic year.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Nordic fire-safety codes | −0.3% | Norway, Sweden, Finland | Medium term (2–4 years) |

| Scarce zoned industrial stock in historic cores | −0.4% | Heritage European city centers | Long term (≥ 4 years) |

| Inflation-linked rental caps | −0.2% | France, Spain | Short term (≤ 2 years) |

| EU energy-efficiency retrofit mandates | −0.5% | EU-wide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Stringent fire-safety codes

Nordic rules require advanced suppression systems and verified risk assessments, adding up to 25% to conversion budgets and delaying market entry

Heightened energy-efficiency mandates

The Energy Performance of Buildings Directive obliges non-residential properties to reach class E by 2030, forcing HVAC and insulation retrofits that smaller owners struggle to fund

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By User Type: Personal demand anchors growth

Personal users accounted for 69.35% of Europe self-storage market revenue in 2025. Household moves, micro-living, and retirement downsizing secure long-tenure contracts that stabilise occupancy during macro shocks. The business cohort, while smaller, is expanding at 7.42% annually as SMEs embrace pay-as-you-go inventory space. Operators now tailor dual-branding strategies-lifestyle messaging for individuals and turnkey logistics features for corporations-to monetise both streams effectively.

The Europe self-storage market size attached to personal tenancy is forecast to maintain a dominant share through 2031, helped by digital reservation platforms that simplify short-cycle booking. Meanwhile, cross-selling services such as courier pick-up, racking, and insurance lift average revenue per business customer as e-commerce penetration deepens in peripheral cities.

By Storage Type: Climate control earns premium

Non-climate units delivered 59.35% of Europe self-storage market share in 2025 thanks to lower fit-out costs. Yet climate-controlled stock, growing at 8.82% CAGR, underpins margin expansion because sensors, HVAC, and stricter access controls command fees 25–40% above standard rooms.

Regulatory upgrades accelerate the pivot: facilities that already meet class E standards recoup retrofit spending via higher rents and lower churn. The Europe self-storage market size for climate-controlled units is on track to surpass USD 14.2 billion by 2031, supporting specialised insurance offerings for electronics, art, and archival documents.

By Space Size: Micro-Units Reflect Urban Space Constraints

Units up to 90 square feet capture 44.35% market share in 2025, reflecting Europe's urban density and the prevalence of smaller storage needs among personal users and micro-businesses. This dominance aligns with micro-living trends and the growing population of urban dwellers who require minimal storage for seasonal items, documents, and overflow belongings. Mid-size units (151–300 sq ft) are growing fastest at 7.86% CAGR through 2031, indicating customer migration toward larger storage solutions as businesses expand and personal storage needs evolve.

The space size distribution reveals market maturation as customers develop more sophisticated storage strategies beyond basic overflow needs. Smaller units provide entry-level pricing that attracts new customers, while mid-size units capture expanding businesses and customers with growing storage requirements. The 91–150 sq ft and above 300 sq ft segments serve specialized needs including business inventory storage and major life transitions. CBRE's 2024 industry report notes that European facilities average higher occupancy rates when offering diverse unit sizes, suggesting optimal facility design incorporates multiple size categories to maximize utilization. This segmentation pattern enables operators to capture customers across different lifecycle stages while optimizing revenue per square foot through strategic unit mix planning.

By Application: Household Goods Foundation Supports E-commerce Growth

Household goods storage commands 61.25% market share in 2025, representing the sector's core application serving personal users during relocations, downsizing, and seasonal storage needs. This dominance reflects the fundamental role of self-storage in supporting Europe's mobile population and space-constrained urban living arrangements. E-commerce micro-fulfillment is emerging as the fastest-growing application at 10.05% CAGR through 2031, driven by SME growth and the need for distributed inventory management in urban areas.

Document and archive storage serves professional and personal customers requiring secure, organized storage for important papers and records, while vehicle storage addresses urban parking constraints and seasonal vehicle needs. The application diversity provides operators with multiple revenue streams and reduces dependence on any single customer segment. E-commerce micro-fulfillment represents the most significant growth opportunity, with European quick commerce markets projected to reach €72 billion by 2025. This application requires specialized services including package handling, inventory management systems, and flexible access arrangements that enable operators to command premium pricing while serving high-growth customer segments.

Geography Analysis

The United Kingdom maintains 33.60% market share in 2025, benefiting from mature market awareness, dense urban populations, and established operator networks spanning major metropolitan areas. UK market leadership stems from early adoption of self-storage concepts, favorable zoning regulations, and high residential mobility rates that create sustained demand. Spain emerges as the fastest-growing market at 8.16% CAGR through 2031, driven by urbanization, tourism infrastructure development, and growing acceptance of storage solutions among Spanish consumers.

Germany, France, and Italy represent substantial markets with moderate growth rates, each offering distinct opportunities based on local demographic and economic conditions. Germany benefits from its aging population and high disposable incomes, while France faces regulatory constraints through rental price controls that limit pricing flexibility. The geographic distribution reflects varying market maturity levels, with the UK representing a developed market while Spain and other emerging markets offer higher growth potential. CBRE's 2024 report indicates that UK, France, Germany, and Spain together account for 68% of European facilities, highlighting market concentration in major economies. This geographic pattern suggests expansion opportunities in underserved markets while established markets focus on operational optimization and service enhancement.

The United Kingdom commands 33.60% market share in 2025, maintaining its position as Europe's most developed self-storage market through superior infrastructure density and customer awareness levels that support premium pricing strategies. UK market leadership reflects decades of market development, favorable regulatory environments, and high residential mobility rates that create sustained demand across economic cycles. The market benefits from institutional investment flows, with Access Self Storage's potential £1 billion sale attracting major investors including TPG and Aermont Capital, demonstrating the sector's evolution into a core real estate asset class. Recent developments include Big Yellow's £10 million Aberdeen acquisition, yielding 6% initially with projections reaching 9% as the facility integrates into their digital platform. The Guardian reports that over 100 new storage complexes opened in the UK within 3 years, generating £1 billion annually as the sector addresses housing crisis-driven demand for space solutions. However, the mature market faces supply constraints in prime urban locations and increasing competition that pressures rental rate growth.

Spain represents the fastest-growing European market at 8.16% CAGR through 2031, driven by urbanization trends, tourism infrastructure development, and evolving consumer acceptance of storage solutions in traditionally family-oriented living arrangements. Spanish growth benefits from relatively low market penetration compared to northern European markets, creating substantial expansion opportunities for both domestic and international operators. The market faces regulatory complexity through Catalunya's rent control legislation that limits rent increases in designated stressed zones, though these primarily affect residential rather than commercial storage applications. Tourism seasonality creates unique demand patterns for storage services, particularly in coastal regions where seasonal residents require temporary storage solutions. The Spanish market's growth trajectory reflects broader southern European trends toward storage adoption as urbanization and lifestyle changes drive demand for flexible space solutions.

Germany, France, and Italy collectively represent substantial markets with moderate growth rates, each offering distinct opportunities based on local demographic transitions and regulatory environments. Germany benefits from its aging population and high disposable incomes, creating sustained demand for downsizing-related storage services, while France faces pricing constraints through government-imposed 3.5% annual rent increase caps that limit operator flexibility info. Italy's market development lags northern European countries but shows potential as urbanization and changing family structures create storage demand. Shurgard's €9.3 million Paris region acquisition demonstrates continued investment in the French market despite regulatory challenges These markets benefit from EU energy efficiency mandates that drive facility modernization and operational improvements, though compliance costs create barriers for smaller operators. The geographic diversity provides operators with portfolio diversification opportunities while requiring localized strategies that address distinct regulatory and cultural environments.

Competitive Landscape

Shurgard tops the leaderboard with 339 stores covering 1.7 million m², pursuing a city-centric footprint where 93% of properties sit inside major metros. Safestore and Big Yellow follow, each integrating contactless access apps, dynamic pricing engines, and solar installations to boost NOI. Access Self Storage’s potential GBP 1 billion sale underscores intensifying institutional interest and likely triggers further consolidation rounds.[1]Inside Self Storage, “Major Investors Compete to Purchase Access Self Storage,” insideselfstorage.com

Technological platforms now underpin competitive advantage. Storable processed 82 million rent payments in 2024, freeing operators from manual billing and enabling algorithmic customer-retention campaigns. [2]Modern Storage Media, “Storable Reports on Its Self-Storage Impact in 2024,” modernstoragemedia.com Cross-border acquirers such as South Africa’s Stor-Age lever joint-ventures with private-equity funds to scale rapidly in the UK. Container-based mobile storage newcomers attract urban millennials seeking door-to-door convenience, but their capital intensity and lower density keep market penetration modest.

Europe Self-storage Industry Leaders

Shurgard Self Storage SA

Self Storage Group ASA

Safestore Holdings PLC

Big Yellow Group PLC

SureStore Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Access Self Storage attracts bidders TPG, Aermont Capital, and Shurgard in a mooted GBP 1 billion sale, with JPMorgan advising.

- July 2024: Big Yellow buys a 53,000 sq ft Aberdeen site for GBP 10 million, targeting a 9% yield post-integration.

- May 2024: Stor-Age acquires four English sites for GBP 59 million, taking total UK spend past GBP 100 million.

- April 2024: Shurgard purchases a second Paris-region facility for EUR 9.3 million, earmarking EUR 8.9 million for redevelopment.

Europe Self-storage Market Report Scope

Self-storage facilities allow people to rent and store any household or business possessions. Rental agreements for storage space, often known as storage units, are month-to-month agreements. Self-storage gives the user much greater control than full-service storage options, which restrict the customers' access to their possessions and dependence on the storage provider to maintain and manage them.

The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates during the forecast period. It also tracks the total lettable area across different European countries while providing market trends and key vendor profiles. Moreover, the study analyzes the impact of COVID-19 on the ecosystem.

The Europe Self-Storage Market is segmented by user type (personal and business) and country (Germany, United Kingdom, Italy, France, Netherlands, Spain, Norway, Denmark, Sweden, Rest of Europe).

The market sizes and forecasts are provided in terms of the (USD) for all the above segments.

By User Type

| Personal |

| Business |

By Storage Type

| Climate-Controlled |

| Non-Climate-Controlled |

By Space Size

| Up to 90 sq ft |

| 91-150 sq ft |

| 151-300 sq ft |

| Above 300 sq ft |

By Application

| Household Goods |

| E-commerce Micro-Fulfilment |

| Document & Archive Storage |

| Vehicle Storage |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By User Type | Personal |

| Business | |

| By Storage Type | Climate-Controlled |

| Non-Climate-Controlled | |

| By Space Size | Up to 90 sq ft |

| 91-150 sq ft | |

| 151-300 sq ft | |

| Above 300 sq ft | |

| By Application | Household Goods |

| E-commerce Micro-Fulfilment | |

| Document & Archive Storage | |

| Vehicle Storage | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size of the Europe self-storage market?

The market is valued at USD 28.09 billion in 2026 and is projected to hit USD 34.21 billion by 2031.

Which country leads the Europe self-storage market?

The United Kingdom holds the top position with 33.60% revenue share in 2025.

How fast is the climate-controlled segment growing?

Climate-controlled units are expanding at a 8.82% CAGR through 2031, outpacing traditional units.

What factors most influence demand?

Urban space constraints, downsizing seniors, e-commerce micro-warehousing, and rising student/expat mobility are the dominant drivers.

Page last updated on: