Content Disarm And Reconstruction Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

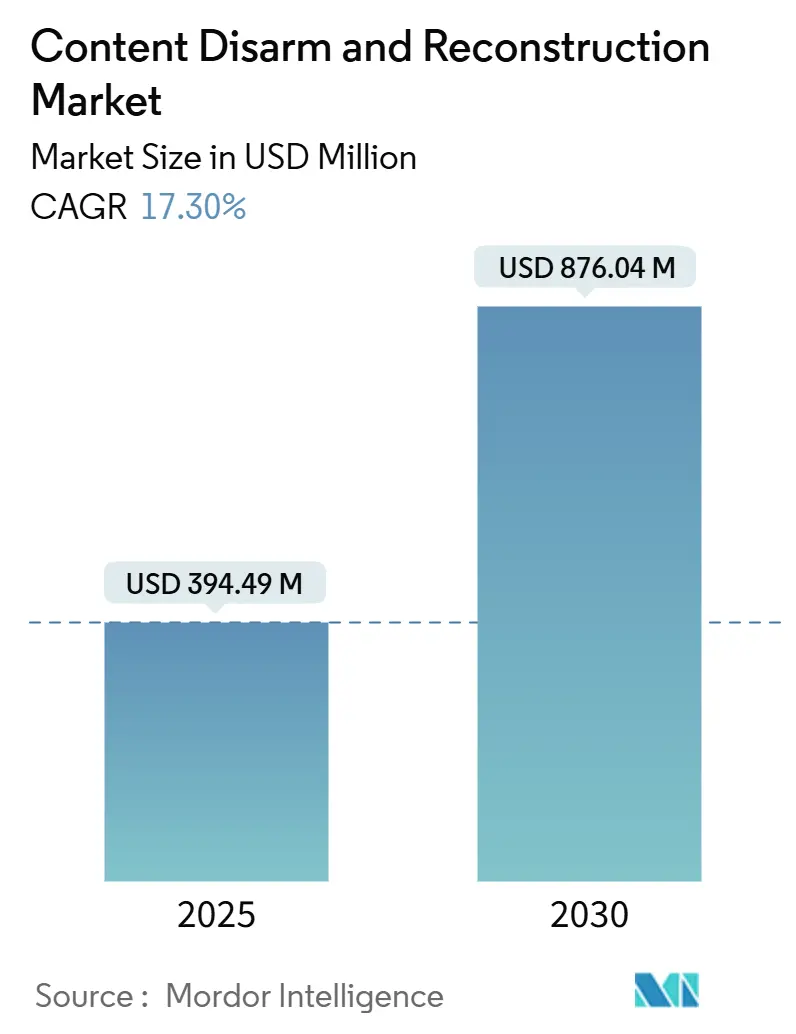

| Market Size (2025) | USD 394.49 Million |

| Market Size (2030) | USD 876.04 Million |

| Growth Rate (2025 - 2030) | 17.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Content Disarm And Reconstruction Market Analysis by Mordor Intelligence

The Content Disarm And Reconstruction Market size is estimated at USD 394.49 million in 2025, and is expected to reach USD 876.04 million by 2030, at a CAGR of 17.30% during the forecast period (2025-2030).

Demand is rising because file-based malware continues to evade signature-based tools, regulatory frameworks now mandate proactive controls, and enterprises are embedding CDR into broader zero-trust architectures. Cloud migration, the pivot to remote work, and browser-centric workflows are expanding threat surfaces faster than legacy security can keep pace. In parallel, advances in deterministic file sanitization are widening use cases from secure email gateways to SaaS collaboration platforms. Vendor competition focuses on integration depth, AI-driven policy tuning, and low-latency reconstruction that preserves user experience.

Key Report Takeaways

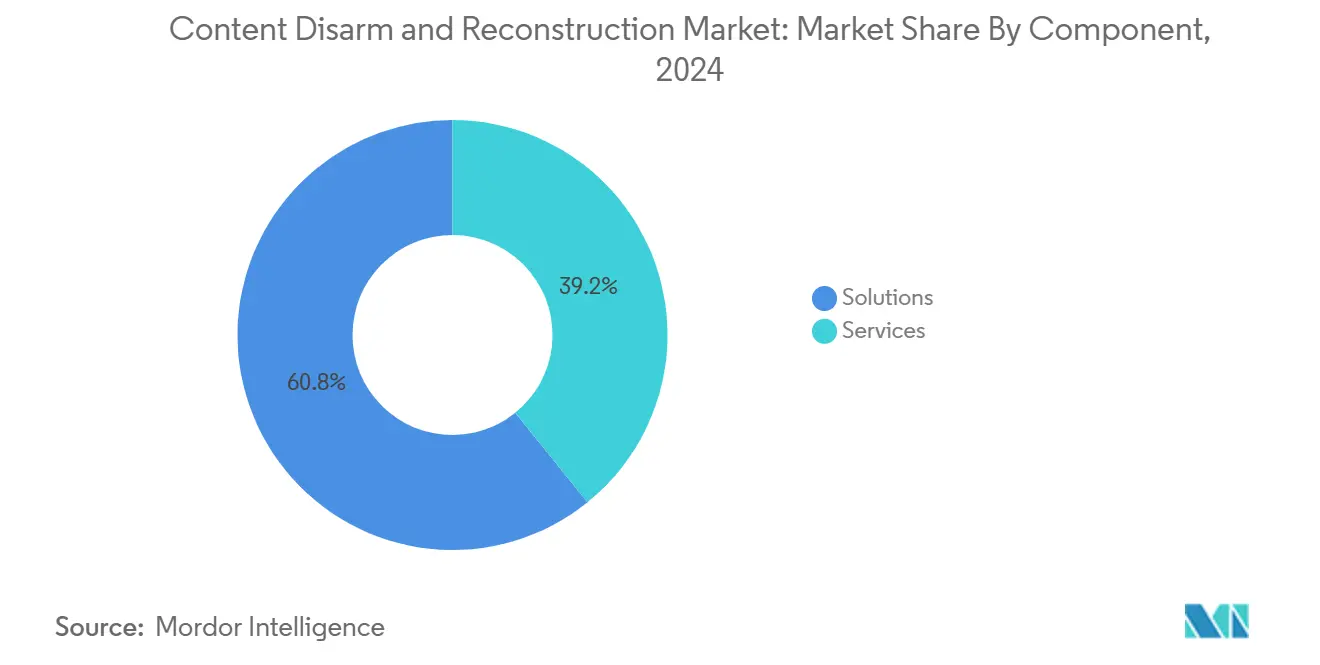

- By component, solutions held 60.8% of revenue in 2024; services are set to expand at a 21.8% CAGR through 2030.

- By deployment mode, on-premise implementations led with 54.6% of the content disarm and reconstruction market share in 2024, while cloud deployments are forecast to grow at a 23.5% CAGR to 2030.

- By application, email security captured 47.2% of the content disarm and reconstruction market size in 2024; browser isolation is projected to rise at a 22.6% CAGR between 2025-2030.

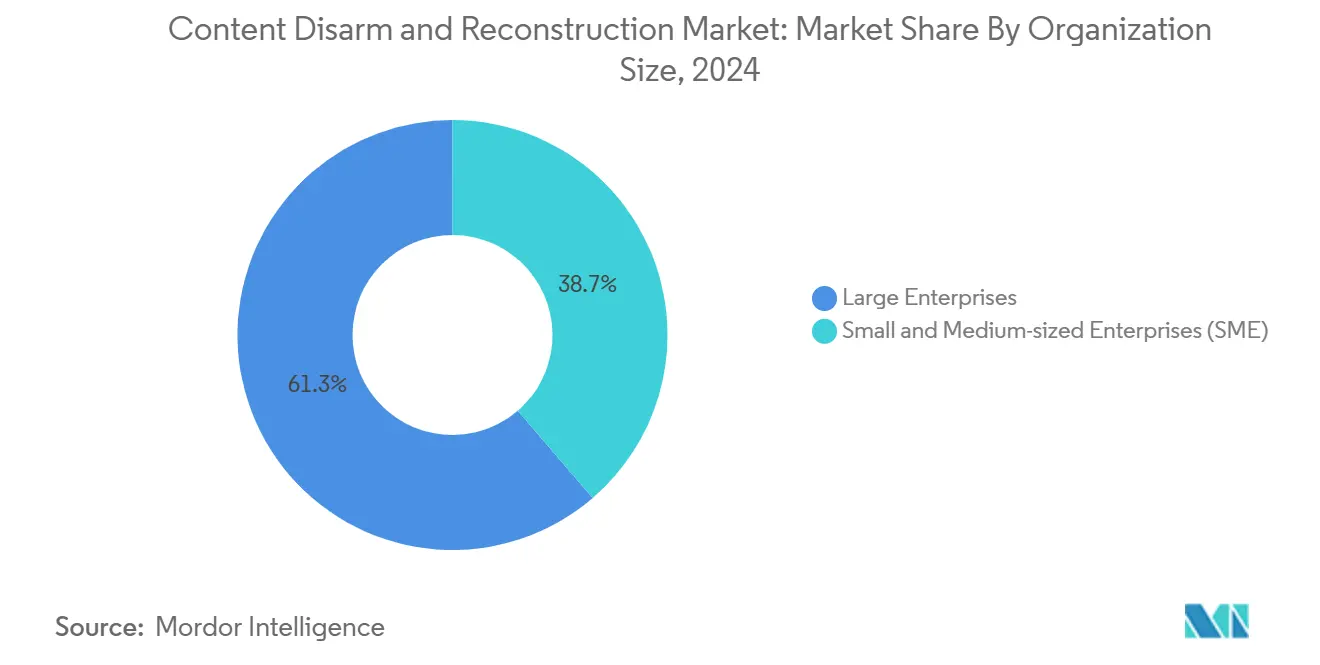

- By organization size, large enterprises commanded 61.3% share of the content disarm and reconstruction market size in 2024, yet SMEs represent the fastest CAGR at 21.2%.

- By end-user vertical, government and defense led with 23.7% revenue share in 2024; manufacturing is advancing at a 19.5% CAGR through 2030.

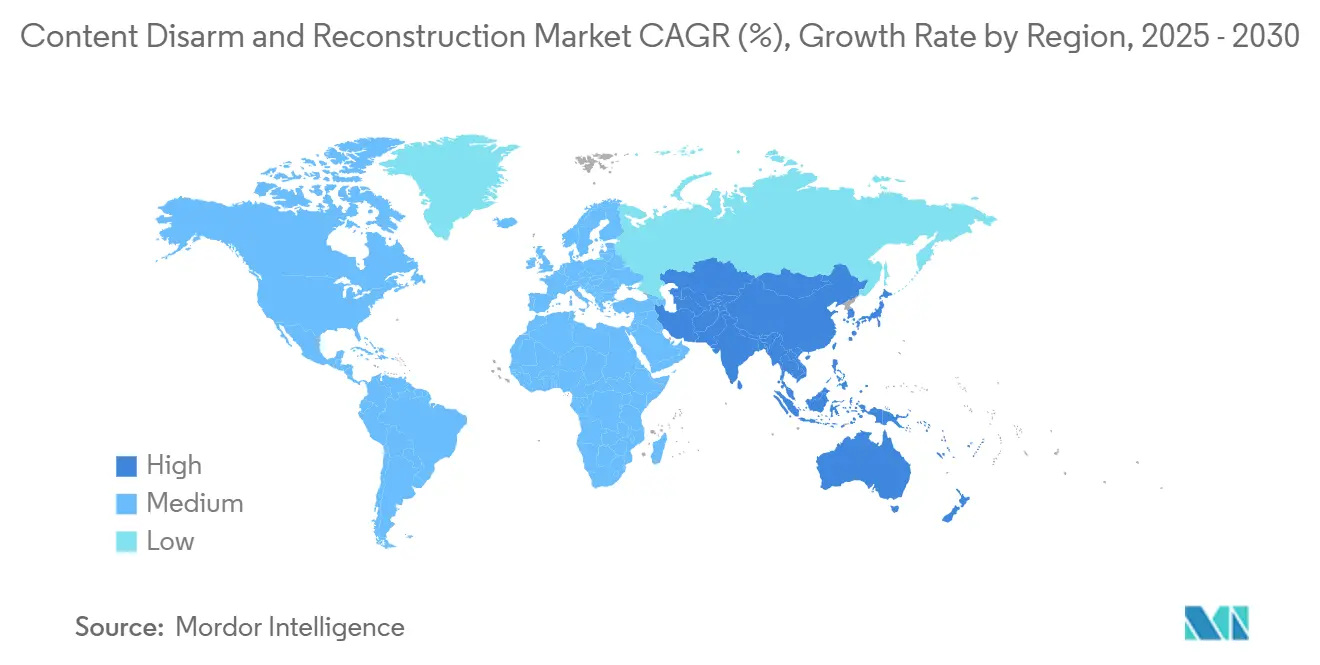

- By geography, North America accounted for 34.7% revenue in 2024, while Asia-Pacific shows the highest 20.6% CAGR to 2030.

Global Content Disarm And Reconstruction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising ransomware, APTs and zero-day exploits | +4.2% | North America, Europe | Short term (≤ 2 years) |

| Escalating regulatory compliance | +3.8% | North America, EU, APAC | Medium term (2-4 years) |

| Surge in file-based malware across cloud channels | +3.1% | APAC, North America | Short term (≤ 2 years) |

| Rapid email/browser isolation adoption embedding CDR | +2.7% | North America, Europe | Medium term (2-4 years) |

| Mandatory CDR in critical-infrastructure procurement policies | +2.4% | North America and Europe, selective APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising ransomware, APTs and zero-day exploits

Attackers increasingly weaponize files to deliver ransomware or establish persistence in OT networks. OPSWAT’s perfect score in SE Labs tests proved that deterministic reconstruction neutralizes novel payloads while maintaining file fidelity. [1]OPSWAT, “OPSWAT Sets New Standard in Cybersecurity with First-Ever 100 Rating in SE Labs CDR Test,” zawya.com Manufacturing saw 25.7% of cyber incidents aimed at industrial control systems in 2024, prompting plant owners to embed CDR at file-ingress points. Collaboration between threat actors and generative AI amplifies zero-day availability, making deterministic sanitization attractive because it does not rely on prior knowledge of malicious code. As a result, the content disarm and reconstruction market is becoming a baseline requirement in incident-prone sectors.

Escalating regulatory compliance (GDPR, HIPAA, CMMC 2.0)

CMMC 2.0 enforces file sanitization for defense contractors pursuing Level 2 and 3 certification, turning compliance projects into direct purchase triggers. Japan’s 2025 Active Cyber Defence law similarly drives adoption across critical infrastructure. Healthcare groups tighten HIPAA audits, so hospitals integrate CDR into secure email gateways to demonstrate due care for electronic protected health information. Financial institutions, exposed to GDPR fines, view deterministic sanitization as both a compliance control and an audit-ready safeguard against data leakage.

Surge in file-based malware attacks across cloud channels

Enterprises average 490 SaaS apps yet authorize fewer than half, expanding blind spots where malicious files circulate unchecked. Microsoft’s FileWall integration underscores vendor consensus that cloud-native threats need embedded, cloud-resident defenses. Banks moving loan-processing workflows to SaaS use CDR APIs to sanitize PDFs uploaded by customers, keeping processes friction-free while blocking polymorphic payloads.

Rapid email/browser isolation adoption embedding CDR

Browser isolation vendors now sanitize downloads within remote sessions, marrying zero-trust browsing with deterministic disarm. Votiro’s partnership with Zscaler delivers inline file reconstruction that users never notice. Palo Alto Networks added granular file-transfer policies to its isolation service, reducing data-loss risk by blocking unsanctioned uploads while allowing sanitized business content. [4]Palo Alto Networks, “Granular File Transfer Controls in Remote Browser Isolation,” paloaltonetworks.com Government agencies adopting isolation within zero-trust architectures find that embedded CDR ensures classified files remain safe even when accessed from unmanaged endpoints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budgetary constraints for SMEs | −2.8% | Global | Medium term (2-4 years) |

| False-positive fatigue and workflow friction | −1.9% | Global | Short term (≤ 2 years) |

| Proprietary file-format lock-in limiting interoperability | -1.5% | Global, particularly enterprise environments | Medium term (2-4 years) |

| Budgets shifting to AI-based deep-fake detection | -1.2% | North America and Europe, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budgetary constraints for SMEs

Nearly half of small firms operate with no dedicated cyber budget, and those that do spend only 7-12% of IT outlays on security. Up-front licensing, integration tasks, and skills gaps have slowed adoption, even though SMEs experience 43% of attacks. Subscription-based SaaS CDR and managed service bundles are easing this barrier by shifting capital costs to operating expenses and embedding expertise.

False-positive fatigue and workflow friction

Overly aggressive sanitization can strip macros from engineering drawings or remove embedded formulas from financial spreadsheets, halting critical workflows. When users perceive security tools as productivity blockers, they seek workarounds, undermining risk posture. Vendors counter by layering machine learning on deterministic policies, enabling selective reconstruction that preserves business logic while removing malicious content. Change-management programs and granular policy profiles are now essential elements of successful roll-outs, especially in high-volume design, media, and legal environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions remain the foundation of market demand

Solutions captured 60.8% revenue in 2024, reflecting enterprises’ preference for turnkey platforms that combine deep-file inspection, policy engines, and reconstruction pipelines. Many deployments start with an email gateway appliance before expanding to API-based microservices for SaaS workflows, illustrating the platform’s extensibility. Services, while smaller, are climbing at 21.8% CAGR as customers lean on integration specialists to weave CDR into SIEMs, SOARs, and SD-WANs. Incident response teams also use professional services to tune policies after observing live traffic, ensuring low latency and minimal false positives. Managed detection and response providers now bundle CDR with threat-hunting packages, giving mid-market clients access to enterprise-grade protection without capital purchases.

The consulting-intensive nature of complex OT and air-gapped networks further elevates services growth. Defense primes seeking CMMC 2.0 Level 3 certification rely on third-party auditors and implementers to validate that sanitized files retain evidentiary integrity. This dynamic signals that a sizable share of the content disarm and reconstruction market will continue shifting toward outcome-based service contracts rather than perpetual licenses.

By Deployment Mode: Cloud adoption accelerates despite on-premise holdouts

On-premise solutions held a 54.6% share in 2024 as regulated sectors retain data within sovereign boundaries. In contrast, cloud subscriptions are expanding at a 23.5% CAGR because they update threat intelligence continuously and scale elastically during traffic peaks. Global conglomerates use regionally hosted CDR nodes to enforce uniform policies across time zones while satisfying latency requirements. Hybrid models are popular among banks that keep core processing on-site yet offload SaaS and contractor traffic to cloud CDR, minimizing hardware refreshes.

Cost models also drive migration: cloud services convert capex into opex, include maintenance, and simplify version control. Vendors differentiate through zero-downtime upgrades and FedRAMP-aligned hosting. As regulators clarify that sanitized content satisfies data-residency laws, the content disarm and reconstruction market is likely to see its cloud cohort eclipse on-premise revenue before 2030.

By Application: Email security leadership meets rising browser isolation demand

Email retained a 47.2% share in 2024 as attackers exploited attachments in business email compromise schemes that cost USD 4.6 billion in 2023. Gateways embedding deterministic reconstruction now serve as the first control point for many zero-trust programs. Meanwhile, browser isolation’s 22.6% CAGR spotlights a shift toward web-delivered payloads disguised as office files or compressed archives. Organizations enforcing isolation for privileged users couple it with CDR so that sanitized downloads land safely on endpoints. FTP servers, content collaboration platforms, and removable media scans round out steady, compliance-led demand where air-gap integrity is paramount.

APIs extend CDR into DevOps pipelines, sanitizing third-party libraries and open-source components before integration. This move aligns with software supply-chain security mandates, stretching the content disarm and reconstruction market beyond human-initiated file transfers into automated workflows.

By Organization Size: SMEs narrow the protection gap

Large enterprises represented 61.3% of revenue in 2024, funding multi-vector roll-outs that span email, web, and DevSecOps pipelines. They also leverage licensing economies of scale and in-house SOC talent to refine policies quickly. Nevertheless, SMEs post the fastest 21.2% CAGR, driven by lightweight cloud CDR that slots into Microsoft 365 or Google Workspace. Bundles from MSSPs offload daily management, mitigating skills scarcity and making deterministic sanitization accessible at predictable monthly costs. Vendor pricing tiers aligned to mailbox counts or gigabyte throughput further reduce adoption friction.

Regional banks, for example, deploy managed CDR to protect loan documents without adding staff, meeting both security and audit requirements. This democratization suggests the content disarm and reconstruction industry could achieve broad mid-market penetration by the decade’s end.

By End-User Vertical: Manufacturing’s urgency boosts growth

Government and defense held 23.7% revenue in 2024, owing to strict classification rules and nation-state threat exposure. Manufacturing, however, is growing at 19.5% CAGR as Industry 4.0 connectivity links OT with corporate IT, exposing programmable logic controllers to file-borne malware. Automotive plants sanitize CAD drawings and firmware updates to safeguard intellectual property while keeping production lines running. BFSI institutes CDR for client statements and interbank transfers to satisfy regulators and customers alike.

Healthcare steadily adds deployments to guard ePHI flowing through electronic health-record systems, while energy operators adopt CDR for procedure manuals loaded onto portable media in remote sites. These verticals illustrate how deterministic sanitization now spans both information-rich office files and mission-critical operational data.

Geography Analysis

North America accounted for 34.7% of global revenue in 2024, propelled by CMMC 2.0 mandates and USD 1.7 billion in federal cybersecurity allocations for fiscal-year 2025. [2]Department of Homeland Security, “Cybersecurity and Infrastructure Security Agency Budget Overview FY 2025,” dhs.gov Mature SOC ecosystems and a high frequency of ransomware attacks sustain demand across government, healthcare, and finance. Canada prioritizes OT security within its National Cyber Security Strategy, prompting energy and telecom operators to embed deterministic sanitization for asset-transfer workflows. Mexico’s modernization of data-protection laws spurs cross-border enterprises to align with U.S. suppliers’ CDR standards.

Asia-Pacific is expanding at a 20.6% CAGR, driven by government funding and rapid digitization. Japan’s 2025 Active Cyber Defence statute compels critical-infrastructure firms to adopt proactive controls, accelerating procurement cycles for CDR. Singapore’s Smart Nation initiative funds secure citizen-service portals protected by deterministic file-sanitization layers. Australia’s Essential Eight framework recognizes CDR as a compensating control for patch lag, while India’s booming SaaS sector integrates CDR APIs to protect multitenant platforms.

Europe sustains growth with GDPR and the forthcoming Cyber Resilience Act reinforcing the need to neutralize malicious content before processing. Germany’s manufacturing base deploys CDR at plant DMZs to shield PLC firmware updates. The U.K. builds CDR into supply-chain security guidelines after high-profile ransomware incidents disrupted logistics. Smaller EU economies access CDR through regional MSSPs, funded partly by Digital Europe Programme grants. Collectively, strict privacy norms and industrial digitization guarantee steady regional adoption.

Competitive Landscape

The market remains moderately fragmented: a dozen vendors control a majority of revenue, yet no single provider exceeds one-quarter share. Established security suites from Broadcom and Fortinet integrate CDR to upsell existing customers, while specialists such as Votiro, Glasswall, and OPSWAT compete on reconstruction depth and policy agility. Performance metrics are becoming key differentiators; OPSWAT’s 100% SE Labs rating created measurable separation that marketing teams leverage in RFP cycles. Pure-play innovators adopt API-first designs, enabling quick insertion into CI/CD pipelines and SaaS back-ends.

Strategic partnerships dominate recent moves. Glasswall’s alliance with ReversingLabs injects 40 billion malware hashes into its decision engine, enhancing fidelity without inflating latency. [3]ReversingLabs, “Glasswall and RL: Enhancing CDR with Advanced Threat Intelligence,” reversinglabs.com Browser-isolation vendors integrate CDR for seamless web-file protection, broadening reach beyond email. Private-equity capital, illustrated by PSG Equity’s April 2025 investment in Glasswall, signals expectations of sustained double-digit growth and consolidation potential. Vendors also focus on certified deployments—FedRAMP Moderate or ISO 27001—to shorten procurement in regulated sectors. Altogether, competition now hinges on integration breadth, measurable efficacy, and the ability to deliver low-friction user experiences.

Content Disarm And Reconstruction Industry Leaders

Check Point Software Technologies Ltd.

Fortinet, Inc.

OPSWAT, Inc.

Broadcom Inc.

Glasswall Solutions Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Palo Alto Networks introduced granular file-transfer controls in Remote Browser Isolation.

- April 2025: PSG Equity completed a strategic growth investment in Glasswall to accelerate innovation and global expansion.

- April 2025: Sasa Software upgraded GateScanner Security Dome with enhanced file reconstruction for defense and finance users.

- February 2025: ReversingLabs and Glasswall partnered to combine threat-intelligence enrichment with deterministic file reconstruction.

- February 2025: Japan enacted Active Cyber Defence legislation authorizing proactive network defense measures, reinforcing demand for CDR in critical infrastructure.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the content disarm and reconstruction (CDR) market as all software and gateway appliances that automatically remove, rebuild, and deliver safe versions of inbound digital files, irrespective of file type, to prevent file-borne malware from entering enterprise or public-sector networks.

Scope Exclusions: solutions limited to passive detection or sandbox analysis without deterministic file rebuilding lie outside this study.

Segmentation Overview

- By Component

- Solutions

- Software-only CDR

- Integrated hardware gateways

- Services

- Professional/Integration

- Managed/MDR Services

- Solutions

- By Deployment Mode

- On-Premises

- Cloud

- By Application

- Web/Browser Isolation

- File Transfer Protocol (FTP/SFTP)

- Removable Media and Kiosk Imports

- APIs and Content Collaboration

- By Organization Size

- Small and Medium-sized Enterprises (SME)

- Large Enterprises

- By End-user Vertical

- BFSI

- IT and Telecom

- Government and Defense

- Manufacturing

- Healthcare and Life Sciences

- Critical Infrastructure (Energy and Utilities)

- Other End-user Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Singapore

- Malaysia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed CISOs at banks, defense agencies, and manufacturing majors across North America, Europe, and APAC, as well as product managers from leading secure-email gateway vendors. These conversations tested threat-incidence assumptions, average selling prices, deployment mixes, and upcoming regulation timelines, ensuring that desk findings translated into realistic adoption curves.

Desk Research

Our analysts first mapped the universe using freely available, reputable sources such as NIST's National Vulnerability Database, ENISA threat reports, United States Cybersecurity & Infrastructure Security Agency advisories, CERT-EU newsletters, and regional cyber-crime statistics from INTERPOL. Annual 10-Ks, investor decks, and procurement tenders added shipment and pricing color, while paid access to D&B Hoovers and Dow Jones Factiva supplied company-level revenues and recent deals that validate market momentum. Patent landscaping via Questel helped size emerging browser-isolation integrations. This list is illustrative; many additional sources informed data collection and verification.

Market-Sizing & Forecasting

A top-down reconstruction of endpoint counts, regulated-sector penetration rates, and file-transfer volumes generated the 2025 demand pool, which we then cross-checked through a selective bottom-up roll-up of supplier revenues. Key variables include average inbound file traffic per employee, share of zero-day malware flagged by national CERTs, CDR attach rates to email security renewals, cloud-migration ratios, and median subscription ASP trends. Multivariate regression, updated annually, links these drivers to historic growth; scenario analysis stress-tests the model for regulatory delays and price compression. Volume gaps detected in bottom-up samples are adjusted using weighted regional error factors before finalization.

Data Validation & Update Cycle

Outputs pass anomaly screening, peer review, and senior analyst sign-off. Reports refresh every twelve months, with interim updates triggered by material M&A, policy shifts, or >5% variance in quarterly run-rate indicators. Clients therefore receive an always-current baseline.

Why Mordor's Content Disarm and Reconstruction Baseline Commands Reliability

Published estimates often differ because firms pick dissimilar scopes, data vintages, and refresh cadences.

Key gap drivers stem from whether broader messaging-security revenues are blended with pure CDR, if legacy 2021 price points are extrapolated without new primary checks, or when regional breakouts are missing, forcing aggressive global assumptions. Our study uses a 2025 base year, keeps scope limited to deterministic rebuild technologies, applies fresh ASP interviews, and integrates both regulated-sector and SME demand, thereby balancing optimism with practical adoption realities.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 394.49 M (2025) | Mordor Intelligence | - |

| USD 305.2 M (2024) | Regional Consultancy A | Excludes browser-isolation CDR, limited primary validation |

| USD 200 M (2021) | Global Consultancy B | Older base year, assumes flat ASPs, no SME uptake modeling |

The comparison shows that once outdated prices, narrower scopes, and sparse interviews are adjusted, figures converge toward Mordor's balanced view, underscoring why decision-makers rely on our disciplined, transparent approach.

Key Questions Answered in the Report

What is driving the rapid growth of the content disarm and reconstruction market?

High-impact ransomware, stricter compliance mandates such as CMMC 2.0, and the migration of workflows to cloud and browser environments are pushing organizations to adopt deterministic file-sanitization technologies that neutralize unknown threats before execution.

How large is the content disarm and reconstruction market today and where is it heading?

The market is valued at USD 394.49 million in 2025 and is projected to reach USD 876.04 million by 2030, expanding at a 17.3% CAGR.

Which applications contribute most to current revenue?

Email security leads with 47.2% revenue share because attackers still favor attachments to deliver malware and launch business email compromise schemes that cost billions annually.

Why are SMEs now investing in CDR solutions?

Subscription-based cloud offerings and managed security service bundles lower upfront costs and provide expertise, helping SMEs counter the 43% of cyberattacks that target them.

Which region shows the fastest adoption?

Asia-Pacific is advancing at a 20.6% CAGR thanks to government cyber-defense policies, large-scale digitization projects, and rapid SaaS uptake across both developed and emerging economies.

How are vendors differentiating in an increasingly competitive landscape?

They emphasize measurable efficacy, AI-driven policy tuning to cut false positives, cloud-native architectures for scalability, and deep integrations with email gateways, browser isolation, and SaaS platforms.

Page last updated on: