Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

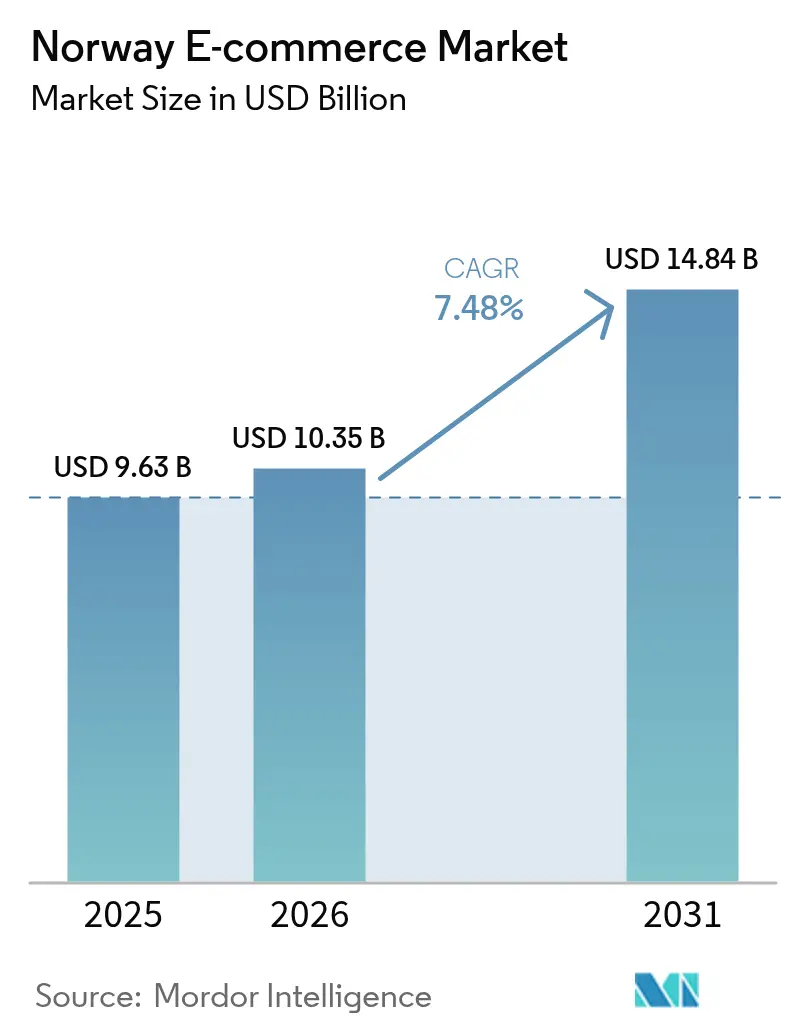

| Base Year Market Size (2025) | USD 9.63 Billion |

| Market Size (2026) | USD 10.35 Billion |

| Market Size (2031) | USD 14.84 Billion |

| Growth Rate (2026 - 2031) | 7.48% CAGR |

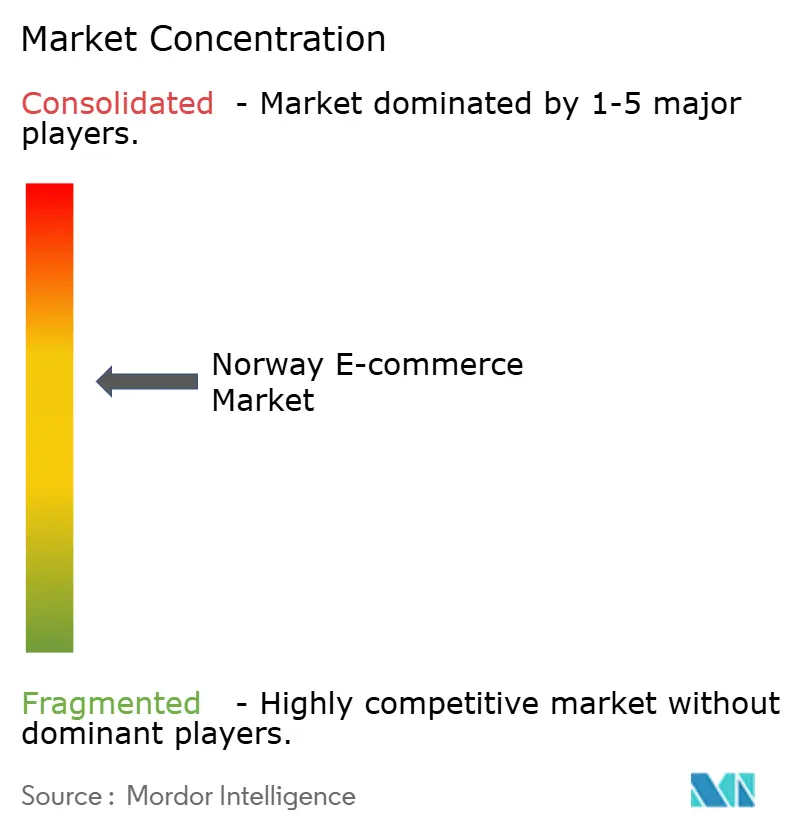

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Norway E-commerce Market Analysis by Mordor Intelligence

The Norway e-commerce market size was valued at USD 9.63 billion in 2025 and estimated to grow from USD 10.35 billion in 2026 to reach USD 14.84 billion by 2031, at a CAGR of 7.48% during the forecast period (2026-2031). Continuous public-sector investments in digital infrastructure, 98% internet penetration, and sustained consumer spending underpin this trajectory.[1]Ministry of Local Government and District Affairs, “Digitaliseringsstrategi 2024-2030,” regjeringen.no The government’s NOK 2.8 billion (USD 747 million) fiber program boosts remote connectivity, while 87% of domestic online sales already accrue to Norwegian stores, evidencing strong local capabilities. Mobile commerce, commanding two-thirds of sales, benefits from smartphone penetration exceeding 95% and a growing appetite for seamless “green delivery” options. Payment innovation is reshaping checkout experiences as Buy-Now-Pay-Later (BNPL) expands faster than any other method, driven by Klarna’s 18% domestic share. Currency volatility and high last-mile costs in sparsely populated areas temper full-market conversion but are mitigated by EU VAT One-Stop Shop (OSS) reforms that simplify cross-border compliance for small sellers.[2]“VAT OSS Guide,” taxation-customs.ec.europa.eu

Key Report Takeaways

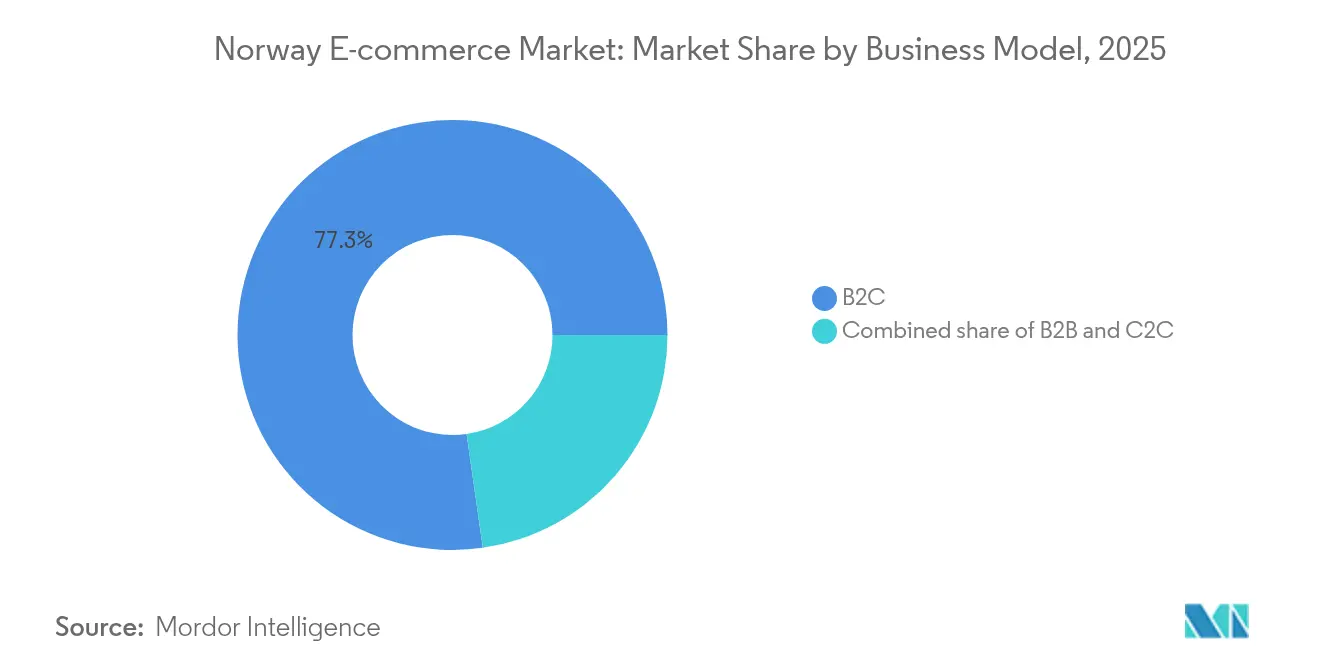

- By business model, B2C retained 77.25% of Norway e-commerce market share in 2025, while C2C is accelerating at a 12.05% CAGR through 2031.

- By device type, smartphones secured 65.40% revenue share in 2025; other connected devices are forecast to expand at a 10.05% CAGR to 2031.

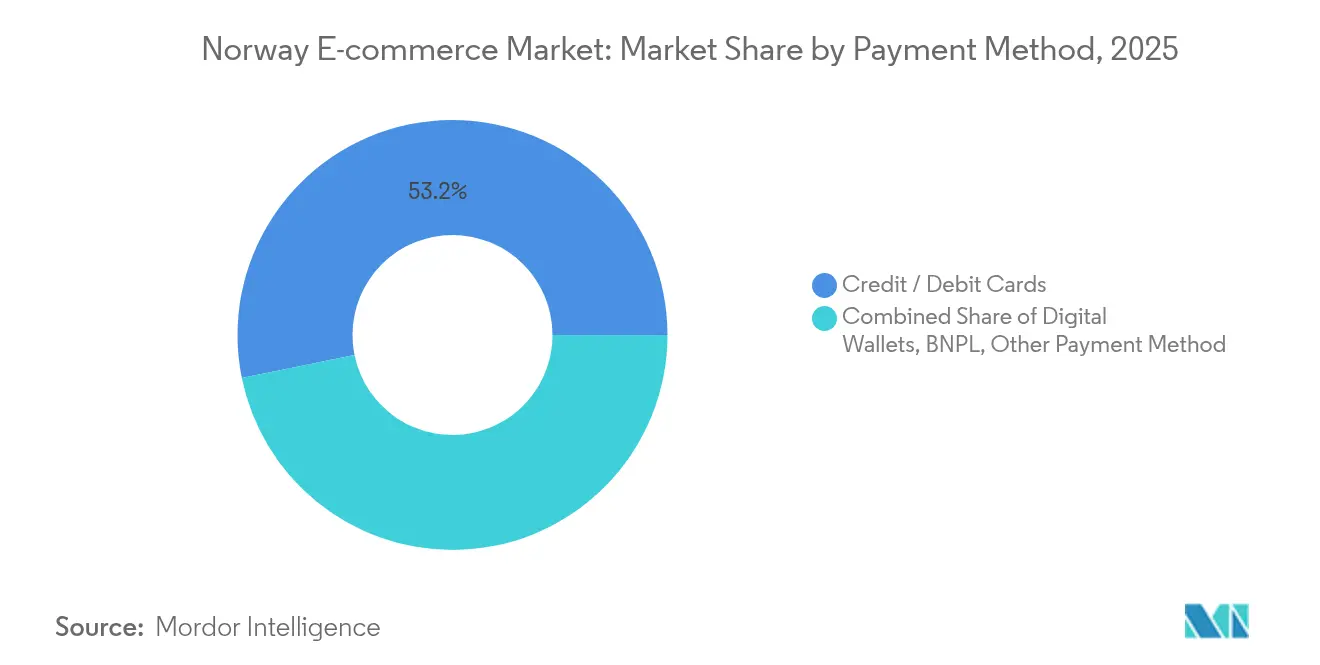

- By payment method, card payments held 53.20% share of the Norway e-commerce market size in 2025, but BNPL is scaling at a 13.15% CAGR through 2031.

- By B2C product category, fashion & apparel contributed 28.55% of the Norway e-commerce market size in 2025; food & beverages is advancing at a 14.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Norway E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed High-Speed Fibre Roll-out to Remote Regions | +1.2% | National, with early gains in northern regions | Medium term (2-4 years) |

| Growing Popularity of Buy-Now-Pay-Later among Gen-Z & Millennials | +0.9% | National, concentrated in urban areas | Short term (≤ 2 years) |

| EU Cross-border VAT One-Stop Shop (OSS) Simplifying Compliance for SMEs | +0.7% | National, with spillover to EU markets | Short term (≤ 2 years) |

| Surge in Domestic Warehousing Automation to Cut Delivery Lead-times | +0.8% | National, focused on Oslo and Bergen regions | Medium term (2-4 years) |

| Booming Adoption of Sustainable "Green Delivery" Preferences | +0.6% | National, strongest in urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-backed High-Speed Fibre Roll-out Drives the Market

Extending submarine cables to Svalbard and Jan Mayen broadens nationwide digital inclusion, transforming previously underserved households into viable e-shoppers. Space Norway’s oversight ensures strategic control and commercial participation, while the Ministry of Digitalisation’s 2024-2030 roadmap targets 100% gigabit coverage ahead of EU objectives. The fibre buildout complements hyperscale investments such as CoreWeave’s USD 2.2 billion AI campus, collectively raising cloud capacity and network resilience. As infrastructure bottlenecks ease, the Norway e-commerce market deepens outside metropolitan areas through reliable access, higher order frequency, and greater SKU diversity. Retailers that align expansion roadmaps with new coverage zones gain first-mover advantage in customer acquisition.

Growing Popularity of Buy-Now-Pay-Later among Gen-Z & Millennials

BNPL reshapes checkout economics by deferring cash outflow for consumers and lifting basket values for merchants. Klarna invoices feature on 39.2% of Norwegian online storefronts, reflecting deep trust and cultural proximity with Sweden. Two and Avarda’s 2025 white-label launch signals convergence of B2B and B2C BNPL rails, addressing a combined Nordic opportunity of USD 41.47 billion by 2025. Local payment methods are expected to command 59% of transactions by 2028, eroding credit card dominance to 30%. Merchants integrating BNPL early in the customer journey capture incremental sales without heightening fraud exposure, thus strengthening loyalty among digitally native cohorts who value transparency and instant approval flows. Consequently, the Norway e-commerce market benefits from higher conversion in discretionary categories such as fashion and electronics.

EU Cross-border VAT One-Stop Shop Simplifies SME Compliance

The OSS regime enables Norwegian sellers to file a single EU VAT return, eliminating the historical need for multiple country registrations. Since the 2024 VOEC upgrade, goods under NOK 350 (USD 93) are no longer duty-free, but VAT is settled at checkout, improving customer transparency while preserving fiscal neutrality. SMEs, which form the backbone of the Norway e-commerce market, report lower administrative costs and faster customs clearance. The alignment with Oslo’s goal of becoming the world’s most digitised capital boosts confidence for micro-exporters seeking Europe-wide reach. Cross-border sales already account for 37.5% of turnover, indicating sizeable headroom for further growth under simplified rules.

Surge in Domestic Warehousing Automation Cuts Lead-times

AutoStore maintains a 97% global share of cubic storage automation and anticipates USD 575–600 million in 2024 revenue, underscoring Norway’s technology leadership.[3]“Capital Markets Day 2024 Presentation,” autostoresystem.com Dense cube storage reduces picking times, frees floor space, and lowers energy use—critical advantages in the high-cost Norwegian labor market. Retailers deploying goods-to-person systems in Oslo and Bergen reduce same-day delivery cut-offs by nearly two hours, enhancing competitiveness with international platforms. StrongPoint’s focus on e-grocery order picking technology further shortens fulfilment cycles. These innovations align with consumer expectations for rapid, predictable delivery and minimize CO₂ emissions per parcel, reinforcing Norway’s sustainability ethos.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Last-mile Costs in Sparsely Populated Northern Regions | -0.8% | Northern Norway, rural areas | Long term (≥ 4 years) |

| Stringent Data-Privacy Norms Limiting Personalised Marketing | -0.5% | National, EU-aligned regulations | Medium term (2-4 years) |

| Persistent Returns-Logistics Burden in Fashion Category | -0.4% | National, concentrated in fashion segment | Medium term (2-4 years) |

| Dependence on Foreign Marketplaces Elevates Currency-Risk Exposure | -0.3% | National, affecting cross-border transactions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Last-mile Costs in Sparsely Populated Northern Regions

Delivering to remote settlements where population density falls below economic thresholds inflates logistics outlays by more than 20% of average order value. Light electric freight vehicles excel in Oslo but lose efficiency over Arctic distances. Although PostNord’s locker rollout eases urban congestion, scaling that model to the north requires capital that current parcel volume cannot justify. Many merchants institute delivery surcharges or higher free-shipping thresholds in these zones, slowing adoption and constraining the total Norway e-commerce market addressable base. Collaborative delivery hubs and state subsidies could ease the burden yet remain nascent.

Stringent Data-Privacy Norms Limiting Personalised Marketing

Norway enforces GDPR rigorously, and 5.3% of citizens avoid digital services due to privacy concerns. The digital strategy prioritizes “privacy-by-design,” compelling retailers to invest in consent-management platforms before deploying advanced personalisation engines. Email segmentation, product recommendations, and look-alike profiling face strict lawful-basis tests, resulting in higher acquisition costs and reduced remarketing ROI. Domestic firms lean toward first-party data accumulation and contextual targeting, which lengthen payback periods on marketing spend. In turn, adoption of AI-driven commerce tools lags peers in more permissive jurisdictions, slightly dampening Norway e-commerce market momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2C Stability Confronts C2C Acceleration

The B2C segment contributed 77.25% to the Norway e-commerce market in 2025, supported by omnichannel rollouts from legacy retailers and trusted local payment options. Heavyweights such as KID ASA expanded online revenue 17.6% year on year, illustrating how brick-and-mortar brands defend share by integrating click-and-collect, unified inventories, and free returns. The Norway e-commerce market size for B2C transactions is expected to rise in tandem with household spending growth and fiber reach into secondary cities. However, the C2C segment, propelled by sustainability and price sensitivity, is forecast to log a 12.05% CAGR through 2031, eroding B2C dominance. Schibsted Marketplaces monetises C2C traffic via listing fees and value-added logistics, capturing NOK 2,103 million (USD 561 million) in Q4 2024 revenue.

C2C uptake reflects a social shift toward circular consumption, with 34% of citizens purchasing second-hand goods online in the past year. Recommerce platforms generate network effects that traditional retailers struggle to replicate, pushing incumbents to launch take-back programs and own-brand marketplaces. B2B e-commerce, while currently niche, benefits from Two and Avarda’s BNPL rail for trade buyers, aligning invoicing simplicity with procurement workflows. As B2B digital maturity increases, the Norway e-commerce industry unlocks incremental volume from wholesale and industrial categories.

By Device Type: Mobile Supremacy Meets IoT Commerce

Smartphones accounted for 65.40% of turnover in 2025, and app purchases now represent 52% of mobile transactions, indicating preference for feature-rich native experiences. Retailers prioritise app personalisation, biometric login, and in-app BNPL modules to raise conversion. Nevertheless, the fastest-growing slice—other connected devices—will expand at 10.05% CAGR, catalysed by smart speakers, watches, and in-car infotainment commerce. Norway’s renewable-powered data-center cluster hosts the compute backbone for voice assistants, enabling merchants to trial hands-free re-order journeys.

Desktop usage remains relevant for complex, high-consideration purchases and B2B orders requiring detailed specifications. The Norway e-commerce market size for multi-device shoppers will continue to increase as IoT endpoints proliferate in households averaging 2.8 connected devices beyond phones. Early adopters already manage grocery re-plenishment through fridge sensors, while wearables nudge health-related product recommendations, foreshadowing broader omnichannel convergence.

By Payment Method: Cards Yield to BNPL and A2A Innovation

Card payments still led with 53.20% share in 2025, but growth has plateaued amid rising interchange scrutiny and card-not-present fraud prevention expenses. BNPL, expanding at 13.15% CAGR, capitalises on transparent fee structures and soft-credit checks attractive to millennials wary of revolving credit. Vipps anchors domestic wallets, facilitating low-cost peer-to-merchant transfers that now appear alongside BNPL at checkout. A2A payments will double to 16% share by 2028, supported by PSD2 APIs that route funds instantly and cheaply between bank accounts.

Merchants integrating multi-rails achieve higher acceptance rates and lower cost-of-payment. The first movers leverage real-time settlement data to optimise inventory and reduce chargeback risk. Consequently, the Norway e-commerce market enjoys enhanced liquidity cycles for SMEs and better user experience across checkout journeys.

By B2C Product Category: Fashion Leadership Faces F&B Momentum

Fashion & apparel dominated with 28.55% of Norway e-commerce market share in 2025, but return rates approach 45%, pressuring logistics budgets. Sustainability concerns elevate interest in rental and second-hand fashion, compelling brands to develop circular programs. Food & beverages is the fastest-growing vertical at 14.1% CAGR, as Oda scales dark-store operations and accelerates ambient-temperature SKUs. The Norway e-commerce market size for online groceries is positioned to climb as consumers embrace weekly subscription models for pantry staples.

Electronics remains resilient due to high disposable income and early adoption of new gadgets. Komplett and Elkjøp shield domestic share through express pick-up and extended warranty bundles. Beauty & personal care benefits from premiumisation, while furniture gains from augmented-reality visualisers that mitigate size-related cart abandonment. Category expansion underscores how breadth of assortment and last-mile reliability dictate competitive advantage.

Geography Analysis

Urban clusters around Oslo and Bergen form the core of the Norway e-commerce market, generating dense delivery routes and shorter fulfilment windows. Domestic firms optimise inventory staging within 50 kilometres of these hubs to achieve same-day cut-offs. By contrast, Northern Norway’s sparse population yields a cost-to-serve that reduces average order frequency even though fibre coverage is improving under public investment programs. Shipping surcharges erode price competitiveness against physical retail, prompting experimentation with micro-fulfilment and communal pick-up points.

Cross-border behaviour remains entrenched: 48% of consumers place international orders monthly, primarily from Sweden and China, leveraging currency arbitrage and broader assortments. EU OSS reforms enable Norwegian SMEs to counterbalance outbound flows by marketing niche products to Europe without complex tax filings. The European cross-border e-commerce market reached EUR 326 billion (USD 354 billion) in 2024, presenting ample upside for export-oriented Norwegian brands. A strong trade surplus and energy-backed NOK valuation can, however, dampen import attractiveness, shifting consumer focus toward domestic SKUs when the krone strengthens.

Infrastructure resilience also varies by region. The upcoming Svalbard cable redundancy and new DC campuses position Northern territories as viable data-intensive commerce hubs over the long term, narrowing the urban-rural digital divide. Collectively, these dynamics sustain a multi-speed Norway e-commerce market that rewards localisation strategies and cross-border dexterity in equal measure.

Competitive Landscape

Norway’s e-commerce arena exhibits moderate fragmentation where domestic proficiency in logistics and local taste offsets global scale. Schibsted Marketplaces posted NOK 8,326 million (USD 2.2 billion) in 2024 revenue, validating its focus on classifieds and recommerce at a national level. International apparel giants Zalando and H&M leverage advanced AI recommendation engines but must accommodate local payment rails and high free-return expectations. Electronics leaders Komplett, Elkjøp, and Power utilise regional warehouses integrated with AutoStore robotics to maintain 24-hour delivery promises statewide.

Technology capability acts as the prime differentiator. AutoStore’s global automation footprint attracts foreign retailers seeking modular fulfilment inside Norway, indirectly enriching the Norway e-commerce market ecosystem. Vipps’ expansion into bundled financial services fosters platform lock-in effects similar to Asian super-apps, giving domestic merchants a loyalty lever unattainable to global competitors operating without local banking partnerships. Emerging players like Tise.com exploit sustainability niches by aligning peer-to-peer commerce with green values, enabling agile entry against incumbents bound to inventory-heavy models.

M&A prospects concentrate on logistics tech, payment orchestration, and niche marketplaces, evidenced by increased FDI scrutiny as the government lowers filing thresholds from one-third to 10 % of ownership for sensitive sectors. Overall, the Norway e-commerce market rewards speed-to-doorstep, eco-credentials, and adaptability to evolving payment habits.

Norway E-commerce Industry Leaders

Prisjakt Sverige AB

Komplett AS

Elkjøp Norge AS

Finn.no

Power International AS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Schibsted Marketplaces announced plans to distribute NOK 500 million (USD 133 million) in special cash dividends from Adevinta asset proceeds in Q2 2025, reinforcing its commitment to capital allocation following its transformation to a pure-play marketplace model.

- February 2025: Two and Avarda launched their white-label payment solution partnership targeting the Nordic e-commerce market, projected to reach USD 41.47 billion by 2025. The integration combines Two’s B2B Buy Now, Pay Later technology with Avarda’s B2C expertise, initially launching in Sweden, Norway, Denmark, and Finland to transform payment handling across the region.

- January 2025: The Norwegian government submitted a comprehensive report to parliament proposing a complete overhaul of the FDI screening system, lowering the threshold for mandatory filings from one-third to 10 % of ownership. This change is expected to significantly increase the number of e-commerce deals requiring FDI screening, particularly affecting foreign investments in technology and telecommunications sectors.

- December 2024: Norway’s Ministry of Digitalisation launched the National Digitisation Forum (NDF) to support AI and digital transformation strategies, serving as an advisory hub for technology experts and government officials. The initiative aims to accelerate digitisation policies and prepare for technological changes affecting the e-commerce sector.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Norway's e-commerce market as the total gross merchandise value generated when residents buy physical goods and select digital downloads through internet-enabled storefronts, whether hosted on domestic or cross-border platforms, across business-to-consumer, business-to-business, and consumer-to-consumer models.

Scope Exclusions: pure payment gateway fees, in-app gaming micro-transactions, and motor-vehicle sales are outside this assessment.

Segmentation Overview

- By Business Model

- B2C

- B2B

- C2C

- By Device Type

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method

- Credit / Debit Cards

- Digital Wallets

- BNPL

- Other Payment Method

- By B2C Product Category

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then interview marketplace operators, large omnichannel retailers, logistics integrators, and payment service specialists across Oslo, Bergen, and Trondheim. Their insights confirm conversion funnels, average selling prices, and category-level momentum, closing gaps left by secondary data and letting us fine-tune assumptions before final modeling.

Desk Research

We begin with a wide desk scan. Public statistics from sources such as Statistics Norway on household broadband, Eurostat's retail volume index, the World Bank's logistics performance tables, and Posten Norge's parcel-flow releases help our team frame internet reach, spending power, delivery capacity, and cross-border trade patterns. Trade association briefings (ICT-Norway, Virke Retail), company filings, and reputable press archives gathered through Dow Jones Factiva provide timely competitive signals, while payment trend dashboards from Norges Bank clarify method mix shifts. These references supply the foundational metrics we need, yet many additional sources are also checked to validate figures and definitions.

Market-Sizing & Forecasting

We anchor the market by applying a top-down build that reconstructs Norway's online spend pool from retail sales, card clearing data, and parcel counts, which is subsequently cross-checked with sampled seller roll-ups and device-level traffic to guard against overstatement. Key variables, such as smartphone share of checkouts, cross-border order ratio, average basket value, VAT-inclusive pricing, disposable income growth, and delivery surcharge trends, feed a multivariate regression that projects value through the forecast period. Where merchant disclosures are incomplete, we impute volumes by blending web-traffic-to-conversion benchmarks validated during interviews.

Data Validation & Update Cycle

Every model pass is peer-reviewed, variance-tested against Statista, card-scheme dashboards, and customs data, and sent back to experts for a final sense check. Reports refresh yearly, with mid-cycle updates triggered by material regulatory or macro shocks, ensuring clients always receive an up-to-date baseline.

Why Our Norway E-commerce Baseline Stands Up to Scrutiny

Market estimates published elsewhere often diverge because researchers choose different scope cut-offs, exchange rates, and refresh cadences.

Key gap drivers include whether digital downloads are counted, how cross-border GMV is treated, the cadence of price-level adjustments, and the depth of primary validation. Mordor's disciplined scope selection and annual expert-verified refresh keep our numbers closely aligned with real transaction flows.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.63 B (2025) | Mordor Intelligence | - |

| USD 8.50 B (2024) | Regional Consultancy A | Narrow product basket and limited primary checks |

| USD 10.90 B (2024) | Data Provider B | Includes digital media downloads and uses fixed 2023 FX rate |

| USD 7.19 B (2024) | Industry Portal C | Excludes B2B spend and applies store-only revenues |

Taken together, the comparison shows that when definition drift and infrequent updates are stripped away, our balanced bottom-up and top-down approach delivers a dependable reference point for planners who need numbers they can trace back to clear, repeatable steps.

Key Questions Answered in the Report

What is the current size of the Norway e-commerce market?

The market is worth USD 10.35 billion in 2026 and is forecast to grow to USD 14.84 billion by 2031 at a 7.48% CAGR.

Which business model leads online retail in Norway?

B2C dominates with 77.25% share in 2025, although C2C is the fastest-growing at 12.05% CAGR through 2031.

How important is mobile commerce in Norway?

Smartphones generate 65.40% of online sales, and dedicated apps account for more than half of those purchases.

Why is BNPL growing so quickly in Norway?

BNPL appeals to Gen-Z and millennials for fee transparency and budgeting flexibility, driving a 13.15% CAGR to 2031 and eroding traditional credit card usage.

What challenges hinder e-commerce expansion in Northern Norway?

Low population density and harsh terrain inflate last-mile delivery costs by over 20% of order value, prompting surcharges and longer lead-times.

How does the EU OSS regime benefit Norwegian sellers?

It allows SMEs to file one consolidated VAT return for all EU sales, cutting administrative overhead and accelerating cross-border shipments.

Page last updated on: