Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

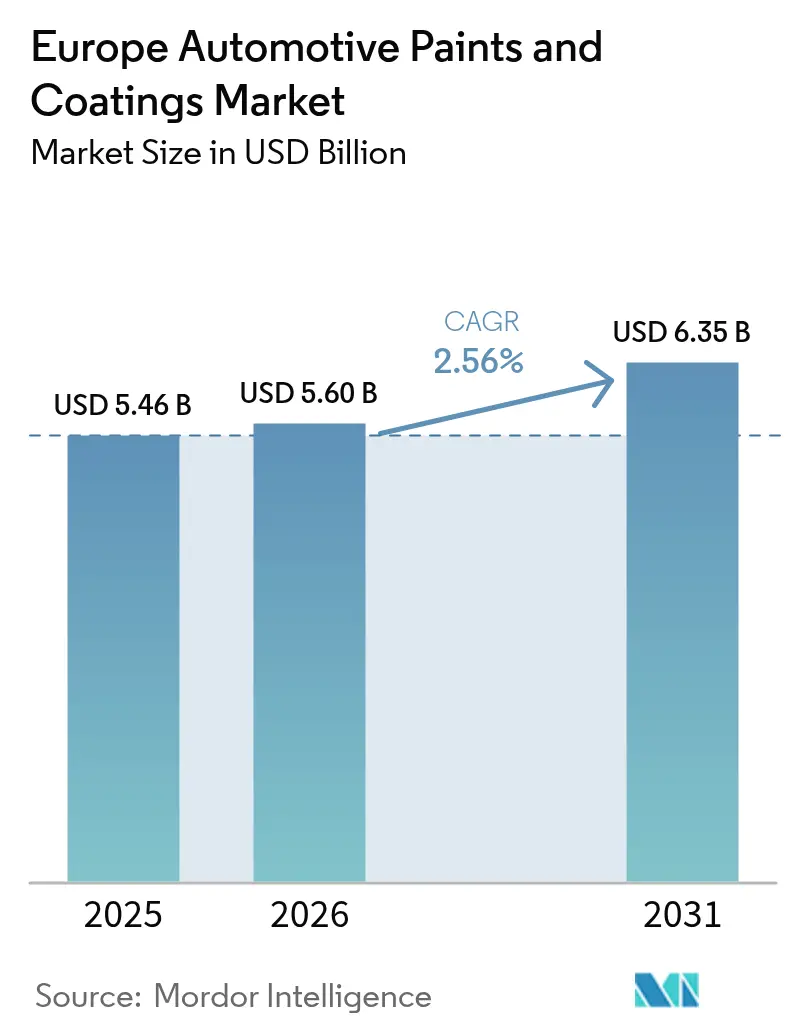

| Base Year Market Size (2025) | USD 5.46 Billion |

| Market Size (2026) | USD 5.60 Billion |

| Market Size (2031) | USD 6.35 Billion |

| Growth Rate (2026 - 2031) | 2.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automotive Paints And Coatings Market Analysis by Mordor Intelligence

The Europe Automotive Paints And Coatings Market size is expected to increase from USD 5.46 billion in 2025 to USD 5.60 billion in 2026 and reach USD 6.35 billion by 2031, growing at a CAGR of 2.56% over 2026-2031. The recovery in vehicle production, stricter EU decarbonization regulations, and the growing adoption of battery-electric platforms are influencing demand trends. Original Equipment Manufacturers (OEMs) are transitioning from solvent-borne to water-borne technologies to comply with the Industrial Emissions Directive’s 45 g/m² VOC limit for new paint shops. Early adopters, such as AkzoNobel, have reduced processing times by 50% using new water-borne basecoats. Electric vehicle designs also necessitate corrosion-resistant e-coat primers and low-bake clearcoats to protect heat-sensitive battery packs, driving increased demand for polyurethane resins. On the regulatory side, the Carbon Border Adjustment Mechanism (CBAM), which entered its definitive phase in 2026, is encouraging localized, low-carbon supply agreements and benefiting coating suppliers that demonstrate reductions in Scope 1 and 2 emissions. Competitive strategies are now focused on AI-driven color-on-demand systems, four-wet low-energy processes, and advancements in self-healing clearcoat technology, which enable luxury brands to offer lifetime paint warranties.

Key Report Takeaways

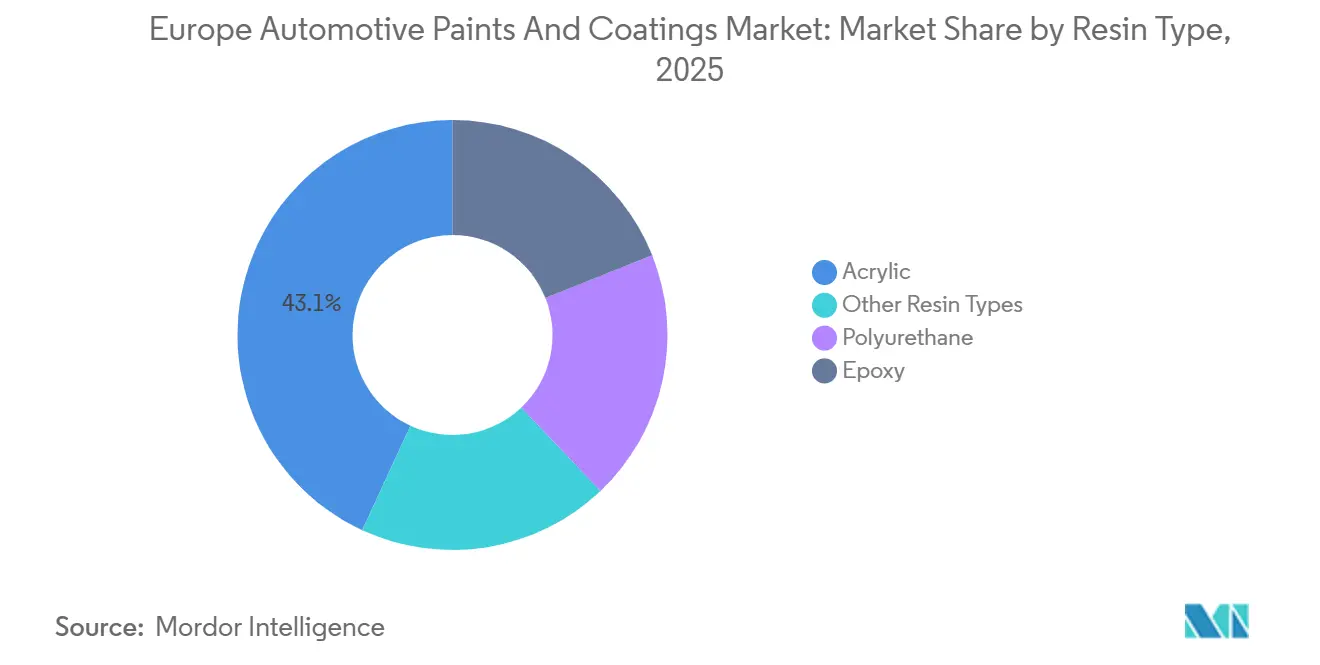

- By resin type, acrylic led with 43.11% of the Europe automotive paints and coatings market share in 2025, while polyurethane is projected to expand at a 2.81% CAGR through 2031.

- By technology, solvent-borne accounted for 49.26% of the Europe automotive paints and coatings market share in 2025; water-borne is advancing at a 2.96% CAGR through 2031.

- By layer, clearcoat accounted for 39.22% of the Europe automotive paints and coatings market share in 2025; e-coat is advancing at a 2.89% CAGR through 2031.

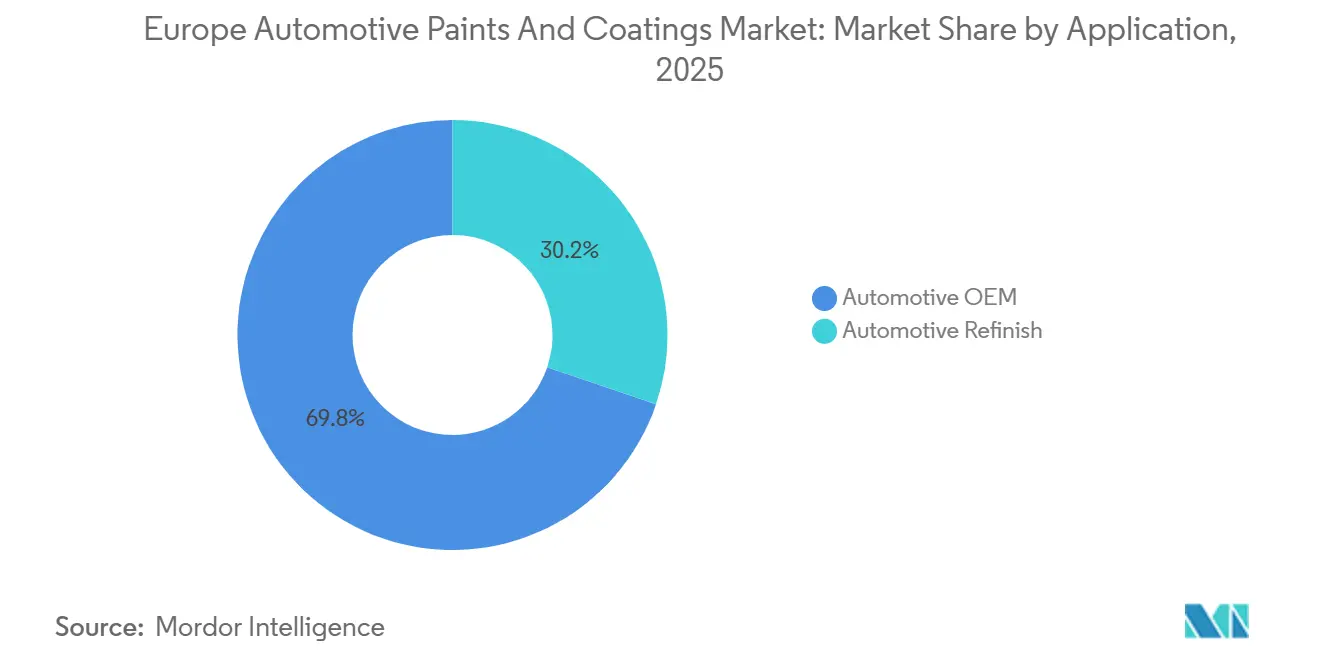

- By application, automotive OEM held 69.78% share of the Europe automotive paints and coatings market share in 2025 and is forecast to grow at a 3.12% CAGR through 2031.

- By geography, Rest of Europe captured 44.14% of the Europe automotive paints and coatings market share in 2025, whereas Germany is forecast to grow at a 2.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Automotive Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to low-VOC waterborne systems | +0.8% | Germany, France, Nordic Countries, Rest of Europe | Medium term (2-4 years) |

| Recovery of European vehicle output | +0.6% | Germany, Spain, Rest of Europe (Poland, Czech Republic) | Short term (≤ 2 years) |

| Carbon Border Adjustment Mechanism shaping supply contracts | +0.4% | Germany, France, Italy, Rest of Europe | Long term (≥ 4 years) |

| AI-guided color-on-demand mixing at OEM lines | +0.3% | Germany, UK, France | Medium term (2-4 years) |

| Nanostructured self-healing coatings enabling lifetime warranties | +0.2% | Germany, Nordic Countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift to Low-VOC Waterborne Systems

Waterborne formulations are expanding at a CAGR of 2.96% as OEM paint shops strive to maintain VOC levels below 45 g/m² for new production lines[1]European Environment Agency, “VOC Emissions in European Industry,” eea.europa.eu. AkzoNobel's 2025 basecoat, with a VOC content of 380 g/L, has achieved a 60% reduction in energy consumption and halved production cycles. BASF facilities operating with VOC levels under 250 g/L now serve as a benchmark for several German OEMs. According to ACEA, VOC emissions per car have dropped by 51.3% since 2005, but achieving the remaining 20% reduction will require significant investments in retrofitting paint booths. Since paint shop energy usage accounts for 65% of plant CO₂ emissions, adopting waterborne systems plays a critical role in meeting Scope 1 and Scope 2 emission targets.

Recovery of European Vehicle Output

Germany manufactured 4.15 million vehicles in 2025, with projections of 4.11 million for 2026, providing a stable base for OEM coating demand. Eastern European countries, such as Poland, the Czech Republic, and Slovakia, are becoming key assembly hubs, contributing to the Rest of Europe representing 44.14% of regional demand in 2026. Electric vehicle (EV) production in Germany reached 1.67 million units in 2025 and is expected to grow to 1.76 million in 2026, increasing the need for mixed-material corrosion primers. Stellantis' four-wet lines in Gliwice have reduced energy consumption to 245 kWh per vehicle, setting a benchmark for energy efficiency.

Carbon Border Adjustment Mechanism Shaping Supply Contracts

The Carbon Border Adjustment Mechanism (CBAM) integrates CO₂ costs into imported components, raising prices by 10-20% and encouraging OEMs to shift toward decarbonized local coatings. BASF's Münster e-coat research center has reduced solvent content to below 1% and lowered Scope 1 emissions by 30%, positioning its products to comply with CBAM requirements. PPG's Enviro-Prime Epic 300 cures at 140°C, cutting gas consumption by 12% and aligning with low-carbon procurement standards.

AI-Guided Color-on-Demand Mixing at OEM Lines

Axalta's Irus Scan spectrophotometer analyzes inverse-angle effect pigments, reducing rework by 15-20%. BASF's Refinity cloud platform captures five color points in 30 seconds and connects with VIN data for closed-loop traceability. Real-time mixing eliminates the need for pre-mixed inventories, reducing working capital requirements by 10-15%. Premium OEMs in the UK and Germany are leading the adoption of this technology, with just-in-time plants maintaining only two days' worth of coating stock.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening REACH and PFAS restrictions | -0.5% | Germany, France, Nordic Countries, Rest of Europe | Medium term (2-4 years) |

| Energy-price-driven curing-oven OPEX spikes | -0.3% | Germany, Italy, Spain, Rest of Europe | Short term (≤ 2 years) |

| Paintless film wraps cannibalizing aesthetic repaints | -0.2% | Germany, UK, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening REACH and PFAS Restrictions

The European Chemicals Agency’s (ECHA) draft for August 2025 includes over 10,000 PFAS chemicals in the candidate list, with transport paints specifically mentioned[2]European Chemicals Agency, “PFAS Restriction Proposal,” echa.europa.eu. The EU has already prohibited PFAS in firefighting foams and plans to implement restrictions on PFHxA starting in 2027. Leading suppliers estimate costs of EUR 50-100 million for portfolio adjustments to meet these regulations. Furthermore, Nordic regulators often enforce bans two years earlier than the EU, creating a staggered compliance schedule.

Energy-Price-Driven Curing-Oven OPEX Spikes

Natural gas prices are expected to stabilize at EUR 40-60 per MWh in 2025, which remains twice as high as 2019 levels. This is projected to increase curing energy costs by 30-40%. For instance, PPG’s 140 °C e-coat and four-wet lines at Stellantis Sochaux have reduced oven energy consumption by 30%, showcasing viable methods to address energy price fluctuations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyurethane Gains on Durability Premium

Polyurethane resins are anticipated to grow at a CAGR of 2.81% through 2031, driven by the need for greater flexibility and chemical resistance in EV clearcoats. Acrylic resins accounted for a 43.11% market share in 2025, primarily used in primers and basecoats due to their cost-effectiveness. Two-component polyurethane remains dominant in collision repair as repair shops aim for OEM-grade finishes. Hybrid acrylic-polyurethane resins are being evaluated for mid-range EVs to combine faster drying times with enhanced durability. PPG CeramiClear, which integrates ceramic nanoparticles into a polyurethane matrix, offers five times the scratch resistance, underscoring the value of innovation in premium products.

The Europe automotive paints and coatings market continues to be segmented by cost and performance. Acrylic resins are preferred for applications requiring UV stability and quick drying, while polyurethane resins cater to premium applications demanding long-lasting gloss. Epoxy resins remain critical for e-coat primers in multi-metal vehicle bodies. Suppliers focusing on water-borne polyurethane variants can capture market share by addressing both regulatory compliance and performance needs.

By Technology: Waterborne Ascendancy Reshapes Supply Chains

Water-borne technology is projected to grow at a CAGR of 2.96% through 2031, driven by strict VOC limits of 45 g/m² and Scope 1 CO₂ reduction goals. Solvent-borne technology held a 49.26% market share in 2025 due to the continued use of legacy spray booths. AkzoNobel’s 380 g/L VOC basecoat demonstrated a 60% reduction in cycle energy, illustrating how regulatory compliance can align with operational efficiency. Powder and UV-cure technologies remain niche, primarily used for wheels and small components due to their high bake temperature requirements.

OEM adoption of water-borne technologies is progressing faster than in the refinish segment, where body shops lag by 3-5 years due to the high cost of dehumidification kits, which exceed EUR 100,000 per bay. Axalta AquaEC targets chain operators capable of amortizing these upgrades. Stellantis Sochaux’s four-wet process integrates water-borne base and clear coats, eliminating one bake cycle and reducing energy consumption by 30%.

By Layer: E-Coat Surges on EV Corrosion Demands

E-coat is expected to grow at a CAGR of 2.89% through 2031, as mixed-material EV bodies increasingly rely on uniform cathodic primers. BASF CathoGuard 800 uses tin-free chemistry with less than 1% solvent content, reducing Scope 1 emissions by 30%. PPG’s low-bake e-coat enables the use of lighter-gauge parts that cannot withstand traditional 160 °C ovens.

Clearcoat remains the leading layer, with a 39.22% market share in 2025, as consumers prioritize scratch-resistant finishes. Self-healing and ceramic-reinforced clearcoats command a 10-20% price premium but offer lower lifetime costs. Primer surfacers are expected to grow in line with the overall market, while basecoats increasingly shift to water-borne dispersions to meet VOC regulations. Suppliers focusing on low-bake e-coat technologies are well-positioned to support the growing use of composite materials in EVs.

By Application: Automotive OEM Outpaces Refinish on Production Recovery

The automotive OEM segment is forecasted to grow at a CAGR of 3.12% through 2031, supported by a rebound in vehicle production. Real-time color systems, such as Axalta Irus Scan and BASF Refinity, reduce rework by 20% and improve inventory turnover. Energy savings from four-wet processes at Stellantis facilities further validate the benefits of integrated production changes.

The refinish segment faces slower growth as paint protection films (PPF) reduce demand for cosmetic repairs. Multi-site operators are investing in AI-based color matching and are likely to comply with VOC regulations faster than independent shops. Suppliers offering water-borne chemistries with solvent-borne performance characteristics can maintain market share, while bundling PPF kits with coatings provides a strategy to offset declining spray job volumes.

Geography Analysis

The rest of Europe held a 44.14% share in 2025, as Poland, the Czech Republic, and Slovakia supplied German and French OEMs. Facilities like Stellantis Gliwice achieved 245 kWh per vehicle, 24% below corporate targets, emphasizing cost-driven efficiency. Spain continues to support large Volkswagen and Renault production lines, while Italy's 35% decline in post-2019 production volumes has reduced coatings demand. Despite a 35% drop in assembly, the UK remains significant in the refinish segment due to a high collision frequency.

Germany is projected to grow at a CAGR of 2.58% through 2031, driven by an estimated 1.76 million EVs by 2026 and significant e-coat R&D investments at BASF Münster. France has introduced a carbon-neutral Sochaux facility, reducing energy consumption by 30% through water-borne four-wet systems. Nordic countries, led by Volvo Cars' carbon-neutral initiatives, are adopting bio-based binders and solvent loops, positioning themselves as test beds for circular innovations.

These regional differences indicate that the Europe automotive paints and coatings market relies on Eastern Europe's cost advantages, Germany's EV growth, and Nordic sustainability initiatives. Suppliers that establish facilities near Polish or Slovakian clusters and offer CBAM-compliant low-carbon product lines are well-positioned to secure long-term OEM contracts.

Competitive Landscape

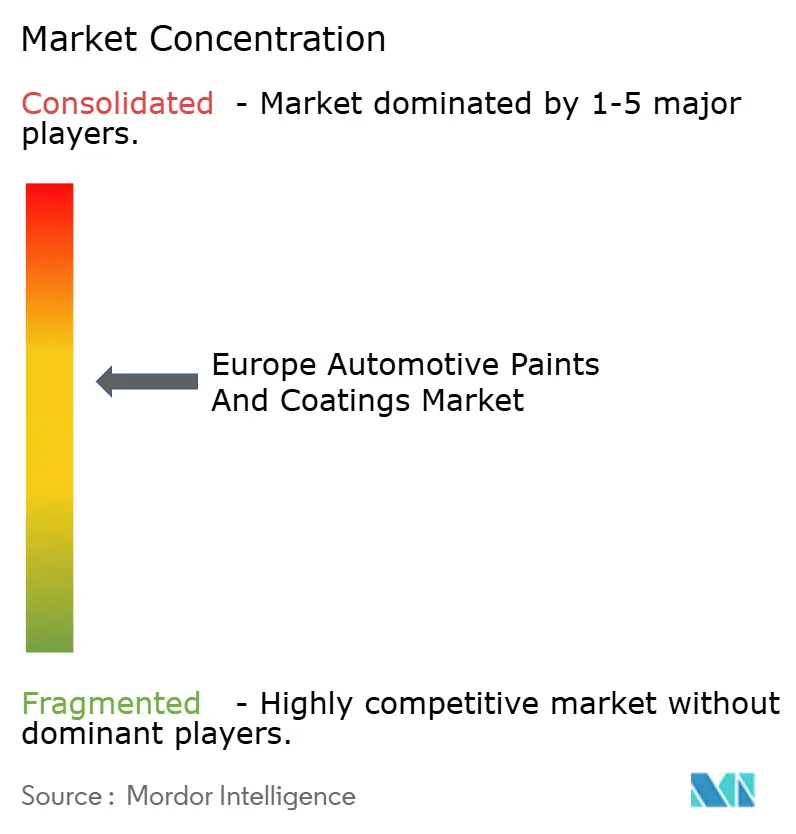

Global players such as Akzo Nobel, Axalta, BASF, PPG, and Sherwin-Williams controlled approximately 68% of the market share in 2025, resulting in a moderately concentrated Europe automotive paints and coatings market. Digitalization is a key competitive factor, with BASF Refinity and Axalta Irus Scan integrating cloud analytics and spectrophotometry into paint lines to reduce waste and enhance customer retention through proprietary platforms. Decarbonization is another critical focus, exemplified by PPG Enviro-Prime Epic 300 and Stellantis' four-wet plants, which set benchmarks for low-bake and low-energy processes. Regulatory compliance is also a priority, with suppliers accelerating the development of PFAS-free and tin-free chemistries.

Mid-tier competitors such as Beckers and Teknos are targeting niche segments like powder coatings for wheels and aluminum primers, leveraging faster formulation cycles for greater agility. However, entry barriers remain high, as qualifying a single OEM line requires an investment of EUR 5-10 million and adherence to IATF 16949 standards. Technologies that combine water-borne compliance with solvent-borne finishes are particularly valuable, especially when integrated with AI-driven color matching and carbon tracking systems.

Looking forward, CBAM regulations are expected to drive increased vertical integration, with OEMs entering multi-year contracts tied to verified carbon intensity metrics. Suppliers lacking renewable-powered facilities or solvent recovery systems risk being excluded from new platforms.

Europe Automotive Paints And Coatings Industry Leaders

Akzo Nobel N.V.

Axalta Coating Systems

The Sherwin-Williams Company

BASF

PPG Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: BASF, in partnership with Qatar Investment Authority (QIA), entered into a binding agreement concerning BASF’s automotive OEM coatings and automotive refinish coatings business. This marked an important step in realizing the value of BASF’s standalone businesses as the company advanced its Winning Ways strategy.

- March 2025: BASF and the Chinese electric vehicle manufacturer NIO entered into a strategic partnership. The collaboration focused on advancing innovative paint technologies to support sustainable and high-quality vehicle painting within the e-mobility market.

Europe Automotive Paints And Coatings Market Report Scope

Automotive paints and coatings consist of four key components: pigment, binder, solvent, and additives. These are designed to enhance aesthetic appeal, provide corrosion resistance, and protect against environmental factors. Most modern vehicles utilize acrylic polyurethane enamel within a basecoat/clearcoat system, known for its high gloss and durability.

The Europe Automotive Paints And Coatings Market is segmented by resin type, technology, layer, application and geography. By resin type, the market is segmented into acrylic, polyurethane, epoxy, and other resin types. By technology, the market is segmented into solvent-borne, water-borne, and other technologies. By layer, the market is segmented into clearcoat, e-coat, primer, and basecoat. By application, the market is segmented into automotive OEM and automotive refinish. The report also covers the market sizes and forecasts for automotive paints and coatings in 5 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Resin Type

| Acrylic |

| Polyurethane |

| Epoxy |

| Other Resin Types |

By Technology

| Solvent-borne |

| Water-borne |

| Other Technologies |

By Layer

| Clearcoat |

| E-coat |

| Primer |

| Basecoat |

By Application

| Automotive OEM |

| Automotive Refinish |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| NORDIC Countries |

| Rest of Europe |

| By Resin Type | Acrylic |

| Polyurethane | |

| Epoxy | |

| Other Resin Types | |

| By Technology | Solvent-borne |

| Water-borne | |

| Other Technologies | |

| By Layer | Clearcoat |

| E-coat | |

| Primer | |

| Basecoat | |

| By Application | Automotive OEM |

| Automotive Refinish | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe |

Key Questions Answered in the Report

What is the size of the Europe automotive paints and coatings market?

The Europe automotive paints and coatings market stands at USD 5.60 billion and is projected to reach USD 6.35 billion by 2031, reflecting a 2.56% CAGR from 2026.

Which resin type will grow fastest through 2031?

Polyurethane is expected to post the quickest growth at a 2.81% CAGR through 2031 thanks to demand for durable EV clearcoats.

Which technology will grow fastest through 2031?

Water-borne technology is rising at a 2.96% CAGR through 2031 as plants comply with 45 g/m² VOC caps.

Why does CBAM matter for coating suppliers?

CBAM adds 10-20% cost to high-carbon imports, so OEMs favor suppliers with verified low-emission production lines.

Page last updated on: