Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

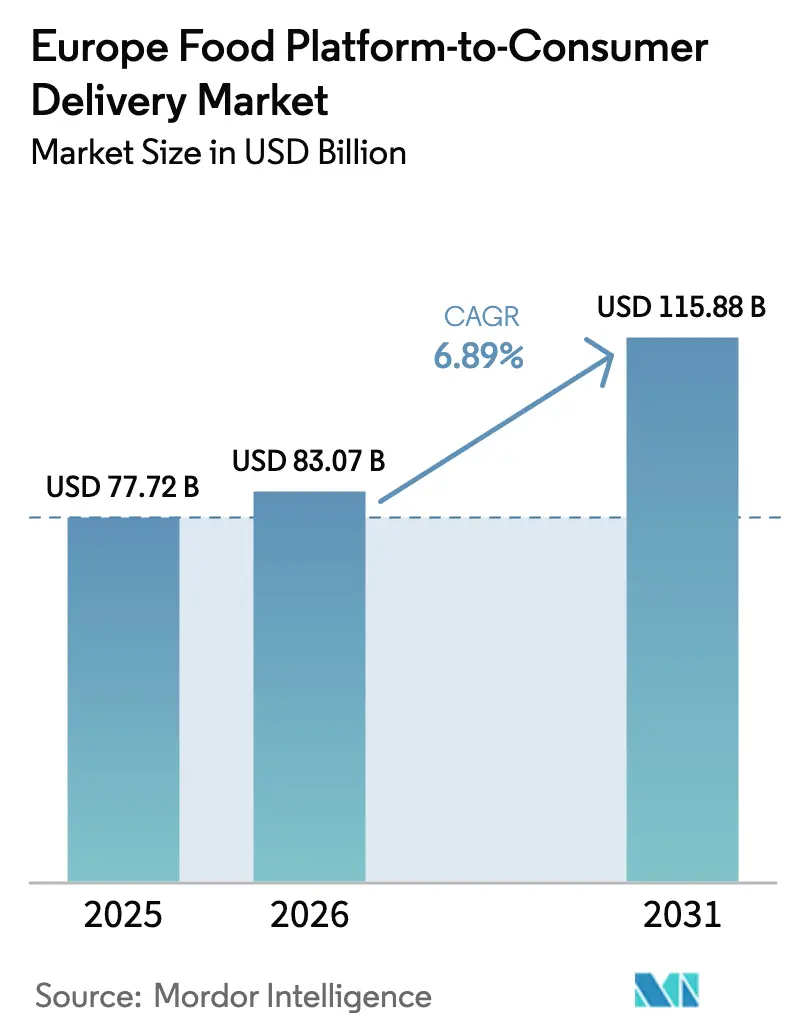

| Base Year Market Size (2025) | USD 77.72 Billion |

| Market Size (2026) | USD 83.07 Billion |

| Market Size (2031) | USD 115.88 Billion |

| Growth Rate (2026 - 2031) | 6.89% CAGR |

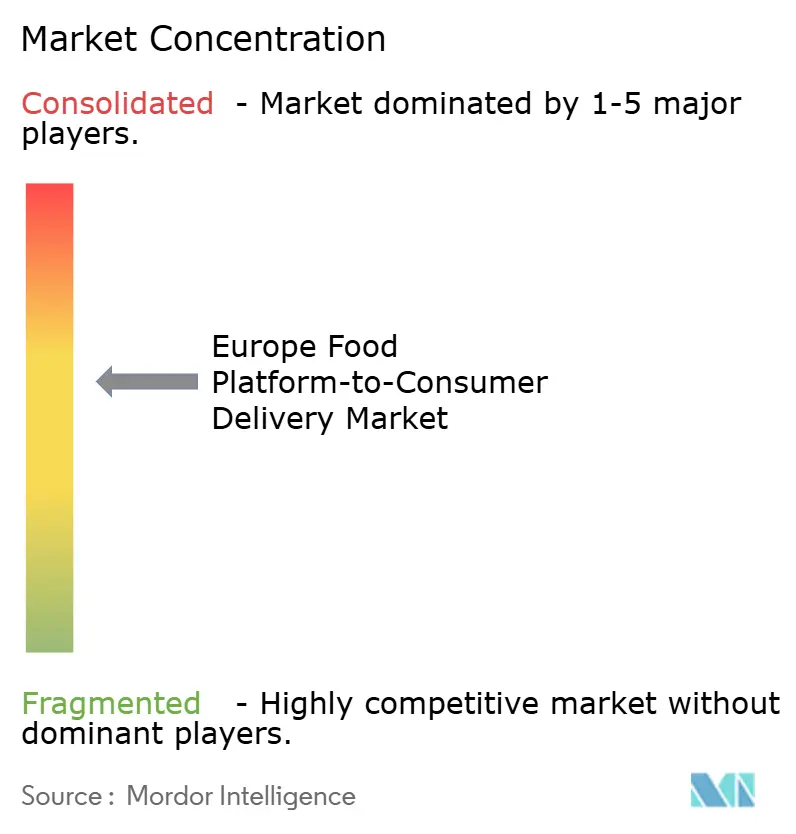

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Food Platform-to-Consumer Delivery Market Analysis by Mordor Intelligence

The Europe food platform-to-consumer delivery market size was valued at USD 77.72 billion in 2025 and estimated to grow from USD 83.07 billion in 2026 to reach USD 115.88 billion by 2031, at a CAGR of 6.89% during the forecast period (2026-2031). Demand is shifting from pure convenience toward a seamless digital food ecosystem in which platforms serve as the primary interface between consumers and restaurants, grocers and specialty stores. Mobile-first ordering already captures 90% of transactions, while AI-driven personalization and dynamic menu pricing lift conversion rates and average basket sizes during peak periods. Rapid subscription uptake, hyperlocal fulfilment hubs and growing grocery quick-commerce broaden revenue streams, whereas EU sustainability mandates accelerate electrification of last-mile fleets and encourage investment in micro-hubs that shorten delivery distances by up to 65%. Intensifying regulation of labour practices, however, continues to elevate courier acquisition costs, making route-density and automation critical to protecting operating margins

Key Report Takeaways

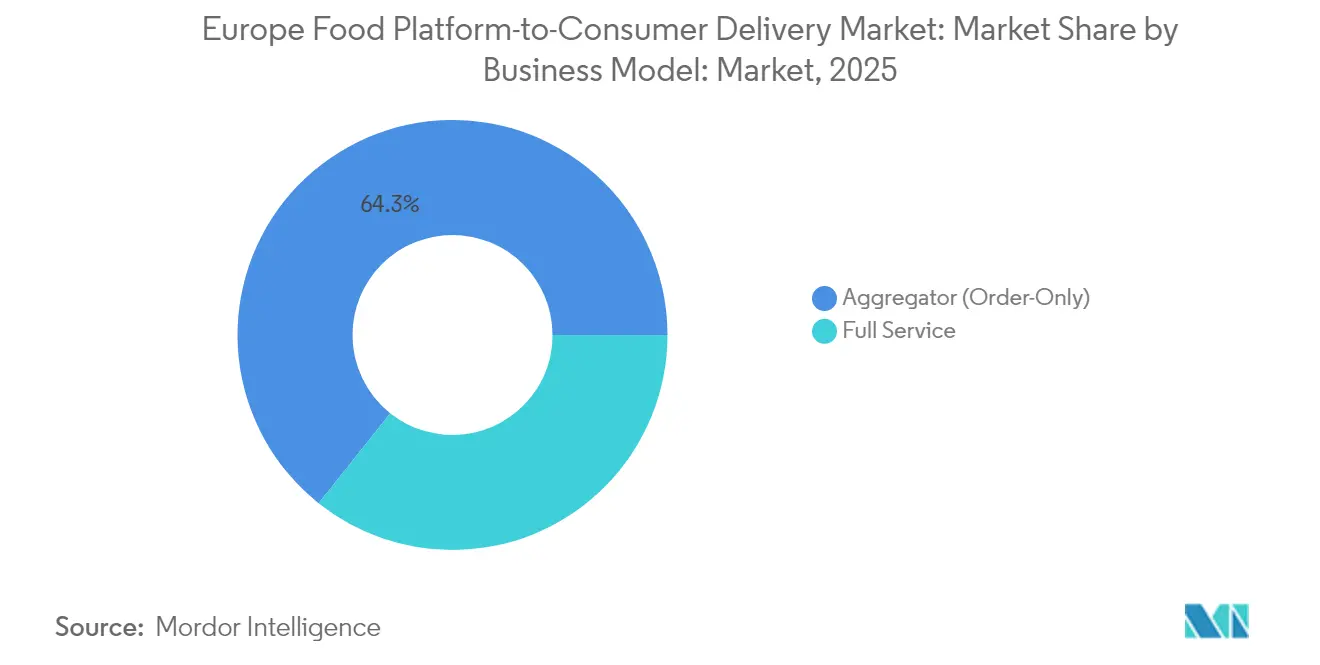

- By business model, Aggregators led with 64.30% of Europe food platform-to-consumer delivery market share in 2025, while Full-Service platforms are forecast to expand at a 8.55% CAGR to 2031.

- By device, mobile applications accounted for 89.20% share of the Europe food platform-to-consumer delivery market size in 2025 and are growing at an 7.9% CAGR through 2031.

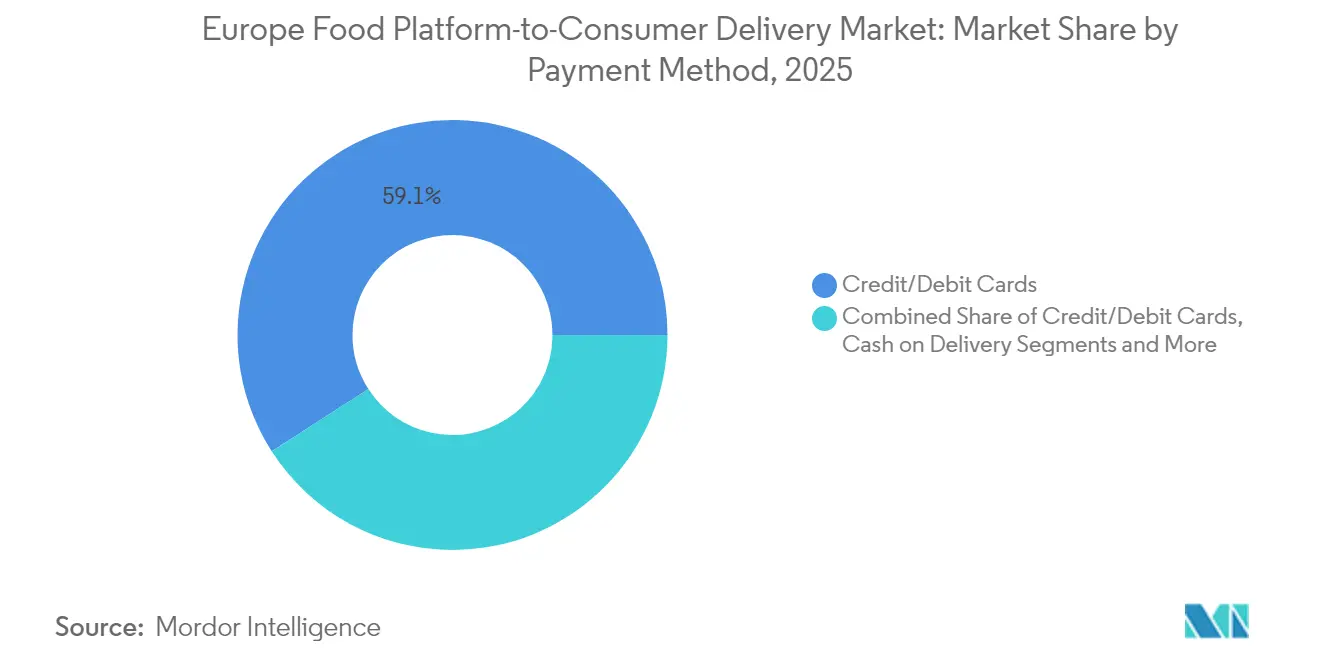

- By payment method, credit and debit cards held 59.10% revenue share in 2025; Digital Wallets and UPI record the fastest projected CAGR at 12.1% for 2026-2031.

- By type of delivery, Ready-to-Eat Meals commanded 44.30% share of the Europe food platform-to-consumer delivery market size in 2025, whereas the Groceries segment is advancing at a 14.6% CAGR.

- By geography, the United Kingdom generated 20.60% of market value in 2025; the Netherlands is poised for the fastest 9.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Food Platform-to-Consumer Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperlocal fulfillment centres accelerating delivery speed across Tier-1 European cities | +1.8% | UK, Germany, France, Netherlands | Medium term (2-4 years) |

| Rise of subscription-based "delivery club" models improving customer lifetime value | +1.2% | UK, France, Germany, Spain | Medium term (2-4 years) |

| Convergence of grocery quick-commerce with meal platforms in Western Europe | +2.1% | UK, Germany, France, Netherlands | Short term (≤ 2 years) |

| Regulatory support for low-emission urban logistics (e-bikes & e-scooters) | +0.7% | Netherlands, Germany, France, Spain | Long term (≥ 4 years) |

| Integration of real-time data & AI for dynamic menu pricing | +0.9% | UK, Germany, France | Medium term (2-4 years) |

| Millennial dual-income households' preference for convenience dining | +0.4% | Pan-European | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyperlocal Fulfilment Centres Accelerating Delivery Speed

Micro-hubs positioned within 2-3 km of dense neighbourhoods enable consistent sub-20-minute service, boosting repeat orders and lowering last-mile costs across the Europe food platform-to-consumer delivery market. Paris alone handles more than 300,000 daily deliveries, and these hubs now complete 78% of drops with electric bikes or cargo trikes, aligning with zero-emission goals. [1]Urbact Secretariat, “Making Every Step Count: Last-Mile Logistics For City Centres,” Urbact, November 04, 2024, urbact.eu. AI-powered demand forecasting improves inventory turn, trims waste and raises courier utilisation, reinforcing profitability.

Subscription-Based Delivery Models Enhancing Loyalty

Delivery-club subscriptions have reached penetration of 15-20% among active users in mature markets and drive 2.7-fold higher ordering frequency than non-subscribers. The predictable revenue stream shields platforms from volatility in average order value while granular usage data deepens personalisation. Millennial and Gen Z households exhibit the highest adoption, indicating further runway as these cohorts’ disposable income rises.

Grocery Quick-Commerce Convergence With Meal Platforms

Platforms extending into 30-minute grocery drops unlock 22% higher average baskets, offsetting lower commission rates. Dark stores dedicated to rapid picking underpin service-level reliability, while cross-selling of top-up baskets into evening meal windows smooths courier utilisation. Partnerships such as Uber Eats with Getir underscore the strategic value of integrated stock management as grocery orders trend toward surpassing meal orders in several Western European capitals by 2028.

Low-Emission Urban Logistics Regulatory Support

EU directives on clean mobility accelerate capital expenditure into electric vehicles and e-bikes that achieve 15-20% lower total cost of ownership over three years.[2]Polis Network, “Zero-Emission Zones For Freight: How-To Guide,” Polis Network, December 15, 2020, polisnetwork.eu. Cities including Rotterdam plan freight zero-emission zones by 2025, granting preferential access to compliant fleets; early movers therefore secure route-density advantages. Sustainable Urban Logistics Plans formalised under the European Commission framework push platforms to share data and invest in consolidated micro-depots, embedding environmental compliance as a competitive differentiator.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising courier acquisition costs amid tighter EU labour rules | -1.2% | Spain, France, Italy, Germany | Medium term (2-4 years) |

| Declining average order value as consumers trade down to discount grocers | -0.9% | Pan-European, especially UK, Germany | Short term (≤ 2 years) |

| Restaurant margin push-back reducing allowable platform commission rates | -0.7% | France, Italy, Spain | Medium term (2-4 years) |

| Stringent GDPR / Digital Markets Act limits on personalised upselling | -0.5% | Pan-European | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Courier Acquisition Costs Amid Tighter Regulations

The EU directive classifying gig workers as employees raises fixed labour costs, social security contributions and administrative overheads. Spain’s employee model increased operating expense by about 20% for major platforms, and Delivery Hero warned of a EUR 100 million (USD 109 million) EBITDA hit. Heightened cost pressures incentivise automation in dispatch, heavier shift scheduling and industry consolidation as smaller operators exit.

Declining Average Order Value Amid Economic Pressures

Inflation and wage stagnation spur consumers to trade down, evidenced by a 15-20% rise in single-meal receipts and heightened sensitivity to delivery fees. Price-comparison behaviours intensify discount wars, compressing commission margins and prompting platforms to pivot performance metrics toward frequency and subscriber growth over basket size. Diversification into advertising and data monetisation helps offset margin compression.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Aggregators Offset By Full-Service Momentum

The Europe food platform-to-consumer delivery market size attributed to Aggregators stood at 64.30% in 2025. However, the Full-Service model’s 8.55% CAGR is narrowing the gap as integrated logistics allow stricter control of customer experience. Urban density in Paris, Berlin and London favours Full-Service economics, while Aggregators retain advantage in suburban zones. Hybrid strategies that combine marketplace breadth with proprietary fleets are blurring traditional boundaries.

By Device: Mobile Applications Consolidate User Interface Power

Mobile apps captured 89.20% of orders in 2025 and will compound at an 7.9% CAGR. Geolocation, biometric authentication and push notifications create frictionless journeys, raising conversion and retention metrics. Desktop interfaces still serve corporate and group orders, yet incremental AI capabilities such as voice ordering favour mobile environments where average basket sizes rose 12-18%.

By Payment Method: Digital Wallets Lead Transaction Innovation

Credit and debit cards supplied 59.10% of spend in 2025; Digital Wallets and UPI, however, are outpacing at a 12.1% CAGR. Local solutions like iDEAL in the Netherlands and BLIK in Poland complement global wallets, supporting region-specific trust and regulation. Cash-on-delivery recedes but persists in parts of Southern and Eastern Europe, sustaining operational complexity.

By Type of Food Delivery: Groceries Surpass Prepared Meals Growth

Ready-to-Eat Meals retained a 44.30% share in 2025; groceries are expected to climb 14.6% annually, doubling the wider Europe food platform-to-consumer delivery market growth pace. Higher basket values and cross-meal order frequency position groceries as a strategic expansion vector, while adjacent categories optimise courier utilisation during off-peak periods.

Geography Analysis

The United Kingdom contributed 20.60% of 2025 revenue. DoorDash’s USD 3.86 billion purchase of Deliveroo in May 2025 consolidated share and scaled innovations such as drone pilots. Germany ranked second at 17.60% share, underpinned by the EU’s largest food-and-beverage sector worth USD 128.7 billion in 2023. Strong environmental regulations encourage electric-fleet deployment, and subscription adoption outperforms the European average. The Netherlands, projected to post a 9.15% CAGR to 2031, benefits from compact city layouts conducive to 20-minute drops and forthcoming zero-emission freight zones.

Competitive Landscape

Approximately 65% of sales accrue to the top five operators, signalling moderate concentration. DoorDash-Deliveroo and Prosus-Just Eat Takeaway combinations demonstrate the premium on scale, while Delivery Hero’s brand merger streamlines overlapping assets.[3]Delivery Hero, “Delivery Hero Merges Its Foodora, Yemeksepeti And Foodpanda Business Teams,” Delivery Hero, July 31, 2024, deliveryhero.com. Technology leadership—especially AI-driven dispatch and dynamic pricing—remains the decisive differentiator as platforms seek 15-20% efficiency gains.

Europe Food Platform-to-Consumer Delivery Industry Leaders

Just Eat

Foodhub Limited

Uber Technologies Inc. (Uber Eats)

Delivery Hero SE

Deliveroo plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: DoorDash closed the USD 3.86 billion acquisition of Deliveroo, expanding to nine additional European markets

- May 2025: Uber purchased an 85% stake in Trendyol GO for USD 700 million, deepening its presence in Turkey

- February 2025: Prosus acquired Just Eat Takeaway for EUR 4.1 billion (USD 4.43 billion), forming a cross-market conglomerate.

- November 2024: Wonder Group bought Grubhub for USD 650 million, signalling ambitions to export kitchen-only models.

Europe Food Platform-to-Consumer Delivery Market Report Scope

The scope of the Platform-to-Consumer Delivery market focuses on online delivery services that deliver orders from partner restaurants. The platform itself handles the delivery process from restaurants that do not necessarily have to offer food delivery themselves. The scope of the market doesn't include orders by telephone, unpacked food for immediate consumption as well as non-processed or non-prepared food. Europe Food Platform-to-Consumer Delivery Market is segmented by country.

By Business Model

| Aggregator |

| Full Service |

By Device

| Mobile Applications |

| Desktop / Web |

By Payment Method

| Digital Wallets and UPI |

| Credit/Debit Cards |

| Cash on Delivery (COD) |

By Type of Food Delivery

| Ready-to-Eat Meals |

| Cooked-to-Order Meals |

| Groceries |

| Other Type of Food Deliveries |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Rest of Europe |

| By Business Model | Aggregator |

| Full Service | |

| By Device | Mobile Applications |

| Desktop / Web | |

| By Payment Method | Digital Wallets and UPI |

| Credit/Debit Cards | |

| Cash on Delivery (COD) | |

| By Type of Food Delivery | Ready-to-Eat Meals |

| Cooked-to-Order Meals | |

| Groceries | |

| Other Type of Food Deliveries | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

What is the expected value of the Europe food platform-to-consumer delivery market by 2031?

The market is forecast to reach USD 115.88 billion in 2031, growing at a 6.89% CAGR from 2026.

Which segment is expanding fastest within the market?

Grocery quick-commerce leads with a 14.6% CAGR for 2026-2031, outpacing restaurant meal delivery.

How large is the UK’s share of the market?

The United Kingdom generated 20.60% of market revenue in 2025, making it the region’s largest national market.

Why are hyperlocal fulfilment centres important to market growth?

Micro-hubs reduce last-mile distances by up to 65% and enable consistent sub-20-minute delivery, improving customer satisfaction and repeat order rates.

What impact do EU labour regulations have on delivery platforms?

Reclassification of couriers as employees raises labour expenses by roughly 20% in affected markets, accelerating consolidation and investment in automation

Which payment methods are gaining popularity across the market?

Digital Wallets and UPI are the fastest-growing payment modes, projected to expand at a 12.1% CAGR, driven by tokenised security and one-click check-out experiences

Page last updated on: