Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.79 Billion |

| Market Size (2031) | USD 13.57 Billion |

| Growth Rate (2026 - 2031) | 11.76% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Dating Services Market Analysis by Mordor Intelligence

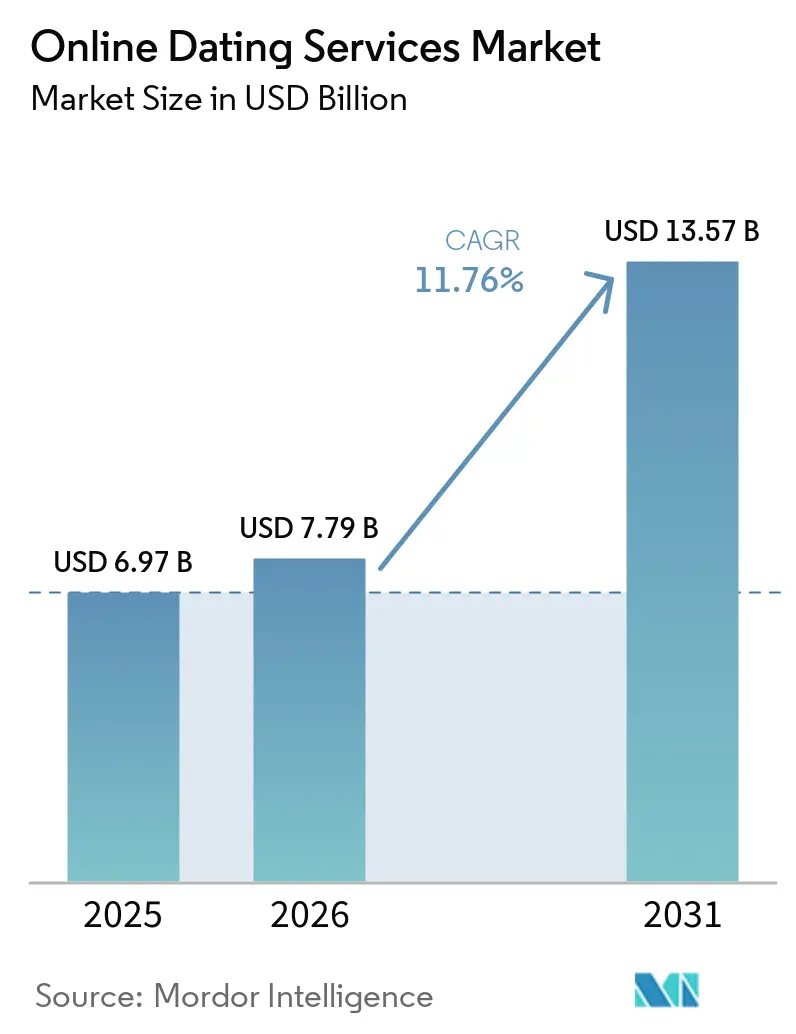

The online dating services market size is expected to grow from USD 6.97 billion in 2025 to USD 7.79 billion in 2026 and is forecast to reach USD 13.57 billion by 2031 at 11.76% CAGR over 2026-2031. Rapid smartphone adoption, normalized perceptions of finding partners online, and rising disposable incomes are converging to expand paid subscriber bases. Generational shifts matter: Millennials still dominate usage, yet Generation Z’s willingness to pay for micro-transactions fuels incremental revenue. Asia-Pacific leads in both scale and speed of adoption, driven by video-centric formats that blend social-commerce and livestreaming. Meanwhile, regulatory scrutiny heightens operating costs, pushing platforms toward stronger compliance infrastructures and data-privacy safeguards. Competitive intensity is moderate, with subscription revenue concentrated among a handful of global players, but faster growth lies with niche platforms catering to specific identities.

Key Report Takeaways

- By type, paying services held 69.45% of the online dating services market share in 2025 and are expanding at a 12.61% CAGR through 2031.

- By revenue model, subscription plans captured 54.35% share of the online dating services market size in 2025, while micro-transactions and virtual gifts are advancing at a 14.58% CAGR to 2031.

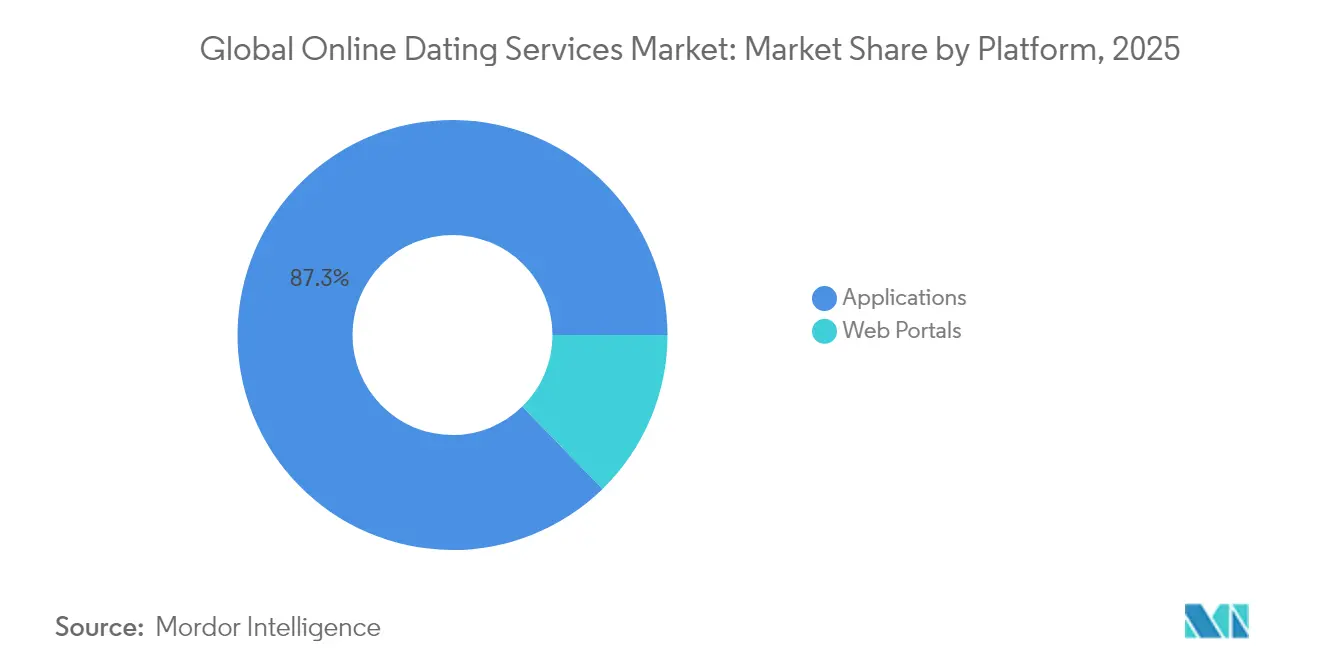

- By platform, mobile applications accounted for 87.30% of the online dating services market in 2025 and will grow at a 12.05% CAGR over the period.

- By age group, Millennials led with 34.20% revenue share in 2025; Generation Z is forecast to expand at a 13.07% CAGR through 2031.

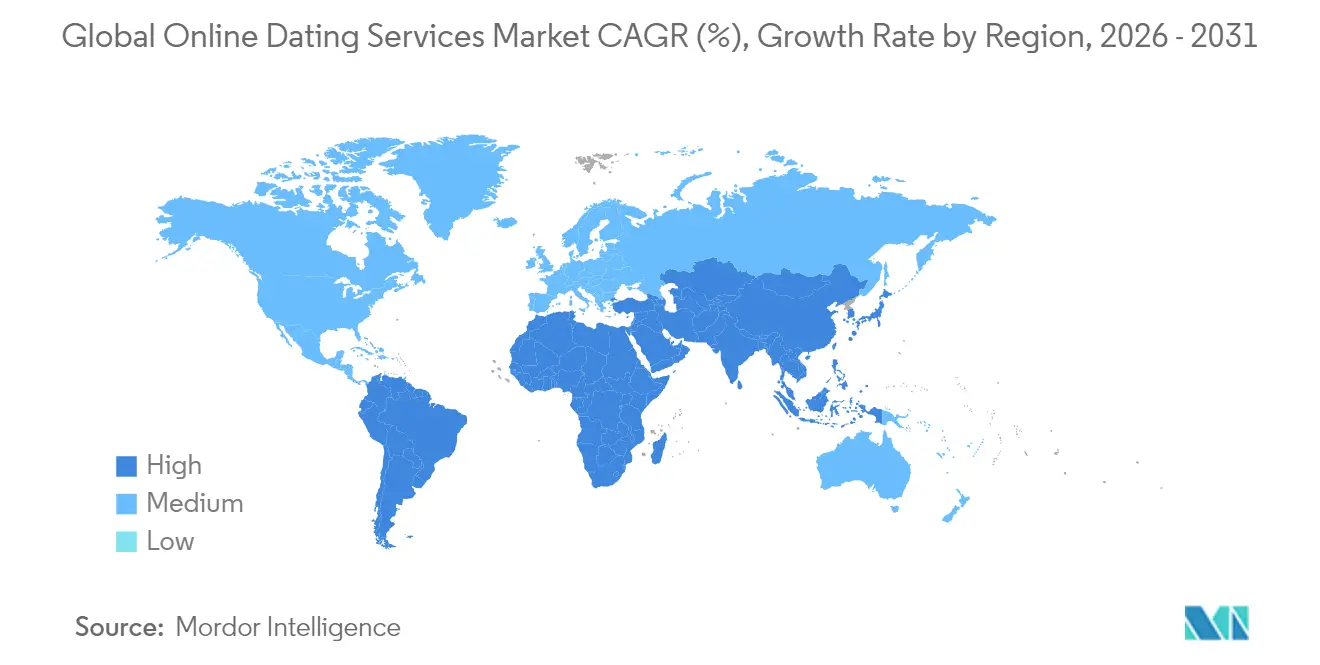

- By geography, Asia-Pacific commanded 34.85% of the market in 2025 and is forecast to grow at a 13.12% CAGR to 2031.

- Match Group, Grindr, and Bumble collectively generated more than USD 4 billion revenue in 2024, underscoring the revenue concentration among top-tier operators.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Dating Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Gen-Z and Millennial Willingness to Pay for Premium Matchmaking Features | +2.1% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Growing Acceptance of Niche & Identity-Based Platforms | +1.8% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| AI-Led Personalization Improving Match Success Rates in Asia | +2.3% | APAC core, spill-over to global markets | Short term (≤ 2 years) |

| Integrations with Social-Commerce & Live-Streaming in China and SEA | +1.9% | China & Southeast Asia, limited global impact | Medium term (2-4 years) |

| 5G-Enabled Video-First Dating Formats Driving User Time-Spent | +1.6% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Gen-Z and Millennial willingness to pay for premium matchmaking features

Premium adoption reflects a move from casual browsing toward intentional relationship building. Match Group reported a 17% rise in revenue per payer in 2024, with a 26% jump in the Americas, showing higher spending even as overall payers declined. Micro-transactions accelerate as users opt to pay for boosts or profile insights instead of fixed plans, creating tiered offers that meet different wallet sizes. Higher spending users also demonstrate longer retention, sustaining platform cash flows. This shift helps offset user-acquisition costs that continue to rise in saturated cities.

Growing acceptance of niche & identity-based platforms in North America & Europe

Niche applications attract users who value community alignment over large pools. Grindr’s 25% Q1 2025 revenue jump and 14.5 million MAUs validate the viability of focused segments. Faith-based or lifestyle-specific services monetize via higher ARPU, stemming from deeper engagement and lower churn. Success forces major apps to add community filters and tailored algorithms to retain users.

AI-led personalization improving match success rates in Asia

Platforms incorporate language-processing, image recognition, and cultural parameters to refine compatibility scores. Match Group plans an AI assistant launch in March 2025 to curate profiles and coach users. Japanese municipal programs back AI matching to address falling birth rates, reinforcing government acceptance of algorithmic pairings. Early data shows reduced swipe fatigue and higher first-date conversion, spurring global adoption.

Integrations with social-commerce & live-streaming in China and SEA

Chinese singles join matchmaking livestreams hosted by cyber matchmakers, buying virtual gifts and products featured during sessions. Monetization blends subscriptions, digital goods, and affiliate sales, broadening revenue sources. Southeast Asian operators replicate the model, bundling dating, entertainment, and shopping within one application, further lifting time-spent per user.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Privacy-Regulation Costs under GDPR & California CPRA | -1.4% | Europe & California, expanding globally | Short term (≤ 2 years) |

| Rising User Fatigue & App-Deletion Rates in Saturated Urban Clusters | -2.2% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Payment-Fraud & Charge-back Losses on Micro-Transactions | -0.8% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Cultural Push-back in MEA on Liberal Dating Norms | -0.6% | Middle East & Africa, limited to conservative regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating privacy-regulation costs under GDPR & California CPRA

Grindr incurred a EUR 5.7 million fine (USD 6.2 million) in Norway for data-sharing infractions. Italy’s data authority penalized Luka Inc. EUR 5 million (USD 5.4 million) for its AI companion service. Compliance now demands dedicated legal teams, data-mapping systems, and third-party audits, raising barriers for new entrants and squeezing margins for smaller players.

Rising user fatigue & app-deletion rates in saturated urban clusters

Ofcom data showed leading UK apps losing substantial users, with Tinder down by 600,000 between May 2023 and May 2024. Users cite ghosting, superficiality, and perceived profit-driven algorithms. Platforms counter with in-person events, but these require offline logistics and increase unit costs. Churn among high-value segments like women in their 30s threatens revenue stability if fatigue persists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Paying Services Capture Value from Serious Seekers

Paying services controlled 69.45% of the online dating services market in 2025 and will compound at 12.61% through 2031. The online dating services market size for paying tiers increases as users equate fees with safety and algorithm quality. Free tiers act as funnels; once initial matches spark confidence, users migrate to paid plans for read-receipt visibility, advanced filters, and verification badges. Platforms balance upsell tactics with user satisfaction to avoid backlash from aggressive paywalls.

Non-paying services retain relevance in emerging economies where disposable incomes lag, yet conversion potential rises alongside smartphone penetration. Advertiser support partially funds free offerings, but privacy curbs on ad targeting pressure ARPU. Consequently, dual-tier or freemium models remain dominant, with iterative feature gating calibrated to optimize lifetime value without stalling onboarding velocity.

By Revenue Model: Micro-Transactions Unlock Flexible Monetization

Subscriptions captured 54.35% share of the online dating services market size in 2025. However, micro-transactions growing at 14.58% CAGR signal a pivot toward à-la-carte spending. Virtual gifts, profile boosts, and timed visibility passes encourage spontaneous purchases during peak engagement moments. Users perceive fairness in paying only when they need an edge, mitigating subscription fatigue.

Asian platforms set precedents with detailed virtual economies. Grindr introduced weekly subscriptions to match budget-sensitive segments, illustrating granular price-point experimentation. Advertising remains a secondary pillar, but cookie deprecation and consent rules limit precision, giving direct-payment streams higher strategic value.

By Platform: Mobile Applications Dominate Everyday Interaction

Applications represent 87.30% of the online dating services market today in 2025 and advance at a 12.05% CAGR. Push notifications, GPS-based discovery, and camera-integrated profiles enrich engagement. Video calling and voice notes cater to authenticity demands. The online dating services market share of web portals, at 12.70%, serves older cohorts who prefer expansive profile narratives and desktop typing comfort.

Mobile-first design forces lightweight onboarding, emphasizing swipe mechanics and quick chats. Yet depth returns through embedded quizzes, voice prompts, and longer video bios that counter swipe fatigue. App stores remain critical funnels, making ASO spend and compliance with platform-fee structures ongoing strategic concerns.

By Age Group: Generation Z Sets the Future Pace

Millennials held 34.20% of revenue in 2025, but Generation Z’s 13.07% CAGR makes them the prime growth engine. Younger users gravitate to ephemeral video stories, AR filters, and community-centric rooms that mix friendship and networking with dating. They also show higher tolerance for micro-spending, aligning with gaming-style reward loops.

Adult cohorts aged 25-34 stay reliable contributors yet expect transparent safety tools after high-profile harassment incidents. Baby Boomers and Generation X continue steady adoption as stigma recedes and widowhood or divorce prompts renewed relationship searches. Platforms craft simplified UIs and scam-prevention guides to serve these groups effectively.

Geography Analysis

Asia-Pacific commanded 34.85% of the online dating services market in 2025 and is projected to grow at a 13.12% CAGR. China’s 240 million singles fuel video-first platforms where livestream dating merges with social-commerce, yielding diversified revenues beyond subscriptions. Tokyo’s investment of USD 1.28 million in an AI-driven government app underscores institutional support. India generated USD 398 million in 2024 revenue with expectations of USD 783 million by 2025, boosted by tier-2 city adoption. Localized features such as parental dashboards meet cultural norms, widening appeal.

North America retains high ARPU and established brands despite slower expansion. Match Group raised revenue per payer by 26% in the Americas, demonstrating pricing headroom. The California Consumer Privacy Rights Act adds compliance layers that increase fixed costs, incentivizing scale economies. User fatigue prompts firms to organize real-world mixers and mental-health partnerships to sustain engagement.

Europe experiences balanced growth amid stringent GDPR oversight. A EUR 5.7 million fine on Grindr set a precedent that prompts preemptive investment in consent management tools. Northern Europe posts the highest per-capita usage, while Southern markets catch up as dating app stigma eases. Brexit complicates cross-border data flows for operators serving the UK and EU, forcing data-residency solutions that raise infrastructure expenses. Identity-based and relationship-focused apps gain traction in culturally conservative pockets, broadening the competitive field.

Competitive Landscape

Global leadership remains with Match Group, which earned USD 3.48 billion revenue in 2024 even as Tinder’s payers fell 8%. [1]Simply Wall St, “Match Group Earnings 2024,” simplywall.st The firm is rolling out AI assistants across its portfolio to combat churn. Grindr, focused on LGBTQ+ users, recorded 33% revenue growth and announced a USD 500 million stock repurchase, signaling confidence in cash generation. Bumble diversifies into friendship and career networking to hedge dating cyclicality, supporting Generation Z’s holistic social-connection demand.

Strategic moves emphasize three levers. First, partnerships combine online matching with offline events, as seen in Pairs and Omikare’s June 2025 alliance linking 25 million users with 920,000 matchmaking club members.[2]PR TIMES, “Pairs-Omikare Partnership Announcement,” prtimes.jp Second, AI enrichment remains pivotal; Grindr’s 2025 roadmap outlines chat summaries and travel heatmaps, while Match Group schedules a March launch for automated profile coaching. Third, capital restructuring protects balance sheets: Spark Networks erased USD 45 million debt under the StaRUG framework to refocus on Christian Mingle and JDate.[3]Spark Networks, “Financial Restructuring Completion,” spark.net

Mid-tier firms exploit white space in faith-based, professional, and hybrid offerings. Regulatory barriers provide defensible moats for capital-rich incumbents, yet also slow feature deployment. Market entry costs climb as privacy and security standards tighten, allowing deep-pocketed players to acquire promising niche apps at favorable valuations. Overall, innovation cycles now hinge on video, AI, and community layers rather than pure swipe mechanics.

Online Dating Services Industry Leaders

Match Group, Inc.(Tinder)

Bumble Inc

The Meet Group(Cupid Media Pty Ltd.)

Happn SAS

TrulyMadly Matchmakers Pvt Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Pairs partnered with Omikare to merge online matching and offline meetups, creating blended ecosystems for authentic interactions.

- March 2025: Newborn Town issued a positive profit alert, with FY 2024 revenue surpassing RMB 5 billion (USD 690 million) due to MENA and Southeast Asian expansion of AI-powered social apps.

- March 2025: Hinge launched a USD 1 million fund to back Gen Z social events across London, New York, and Los Angeles, aligning digital matching with in-person experiences.

- February 2025: Spark Networks SE completed reorganization under German StaRUG, eliminating over USD 45 million debt and gaining new ownership by MGG Investment Group, improving liquidity for core brands.

Global Online Dating Services Market Report Scope

Online dating services is a digital service that allows people to find and introduce themselves to potential connections via the Internet. Online dating services focus on casual contact and easy flirting among their members. The users normally carry out the search on their own by applying search filters with regard to criteria such as age, location, and other attributes.

Global Online Dating Services Market is Segmented by Type (Non-Paying Online Dating, Paying Online Dating) and Geography.

By Type

| Paying Online Dating |

| Non-Paying Online Dating |

By Revenue Model

| Subscription |

| Advertising-Supported |

| Other Model |

By Platform

| Web Portals |

| Applications |

By Age Group

| Adult |

| Baby Boomer |

| Generation X |

| Generation Z |

| Millennials |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Nordics | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Type | Paying Online Dating | |

| Non-Paying Online Dating | ||

| By Revenue Model | Subscription | |

| Advertising-Supported | ||

| Other Model | ||

| By Platform | Web Portals | |

| Applications | ||

| By Age Group | Adult | |

| Baby Boomer | ||

| Generation X | ||

| Generation Z | ||

| Millennials | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the online dating services market?

The market stands at USD 7.79 billion in 2026 and is projected to reach USD 13.57 billion by 2031, reflecting an 11.76% CAGR over 2026-2031.

Which region contributes the largest revenue share?

Asia-Pacific holds 34.85% of global revenue in 2025 and is set to expand at a 13.12% CAGR through 2031.

How significant is the paying services segment?

Paying tiers captured 69.45% of total revenue in 2025 and are growing at a 12.61% CAGR as users invest in premium features through 2031.

Which monetization model is accelerating the fastest?

Micro-transactions and virtual gifts lead with a 14.58% CAGR, outpacing traditional monthly subscriptions to 2031.

What regulatory factors are affecting providers?

Compliance with GDPR and California CPRA has increased operating costs, highlighted by Grindr’s EUR 5.7 million (USD 6.2 million) fine for data-privacy breaches.

Which demographic cohort will drive future user growth?

Generation Z is forecast to expand at a 13.07% CAGR, outpacing Millennials and reshaping feature priorities toward video-centric and authentic interactions through 2031.

Page last updated on: