Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

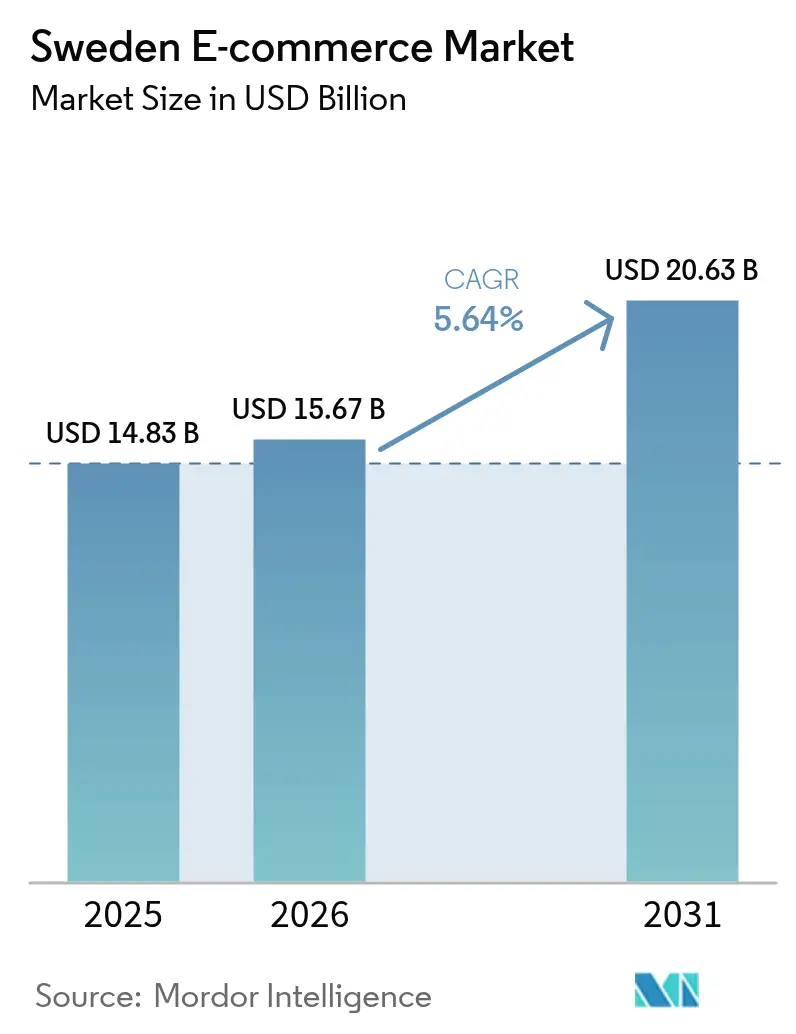

| Base Year Market Size (2025) | USD 14.83 Billion |

| Market Size (2026) | USD 15.67 Billion |

| Market Size (2031) | USD 20.63 Billion |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden E-commerce Market Analysis by Mordor Intelligence

The Sweden e-commerce market size was valued at USD 14.83 billion in 2025 and estimated to grow from USD 15.67 billion in 2026 to reach USD 20.63 billion by 2031, at a CAGR of 5.64% during the forecast period (2026-2031). This sustained growth reflects the country’s near-universal broadband connectivity, a sophisticated logistics network, and a population that routinely prioritizes digital-first shopping. Mobile devices dominate browsing and checkout, and card-less payments such as Swish now set the benchmark for friction-free transactions. Real-time cross-border settlement via the TARGET Instant Payment Settlement (TIPS) rail reinforces national platforms’ competitiveness across the wider Nordic region. Regulatory support for responsible Buy-Now-Pay-Later (BNPL) lending is broadening average order values, while retailer marketplace roll-outs are lifting customer lifetime value and lowering inventory risk. At the same time, rising penalties for GDPR breaches and last-mile congestion in heritage urban zones temper profit margins and spur investment in sustainable delivery innovations.

Key Report Takeaways

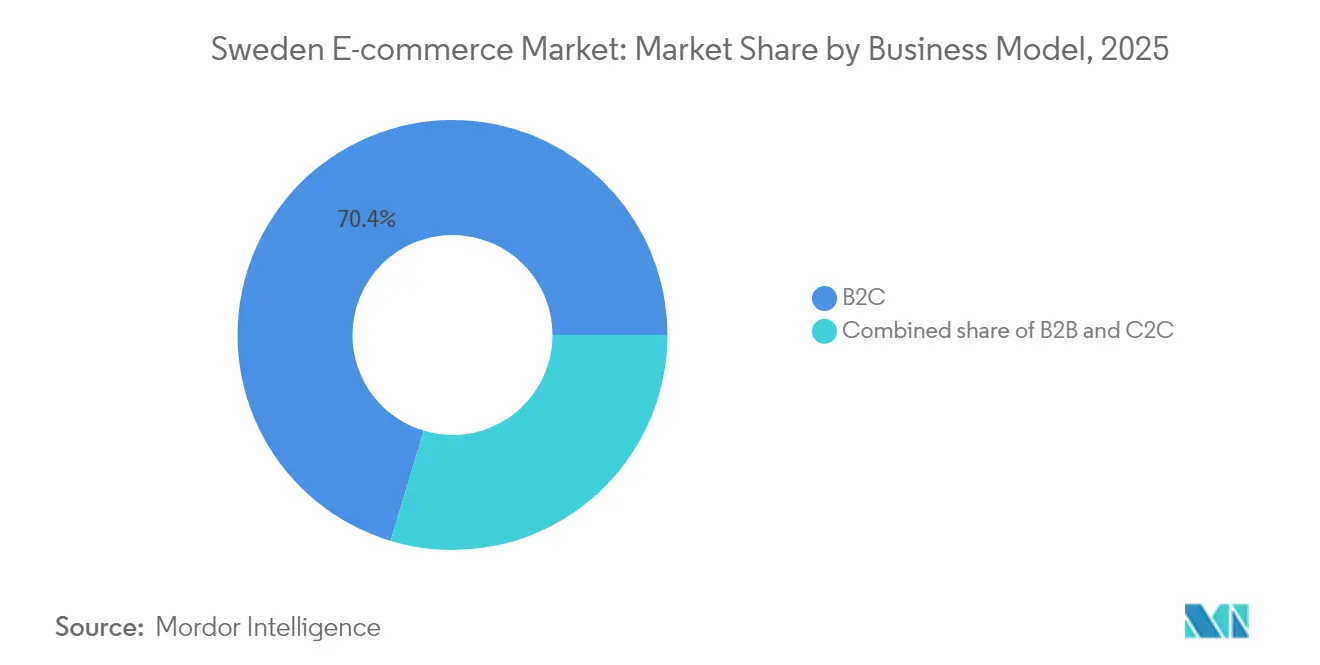

- By business model, B2C accounted for 70.35% of Sweden e-commerce market share in 2025, while C2C is projected to expand at a 8.89% CAGR through 2031.

- By device type, smartphones captured 58.40% Sweden e-commerce market share in 2025 and will record the fastest 7.95% CAGR to 2031.

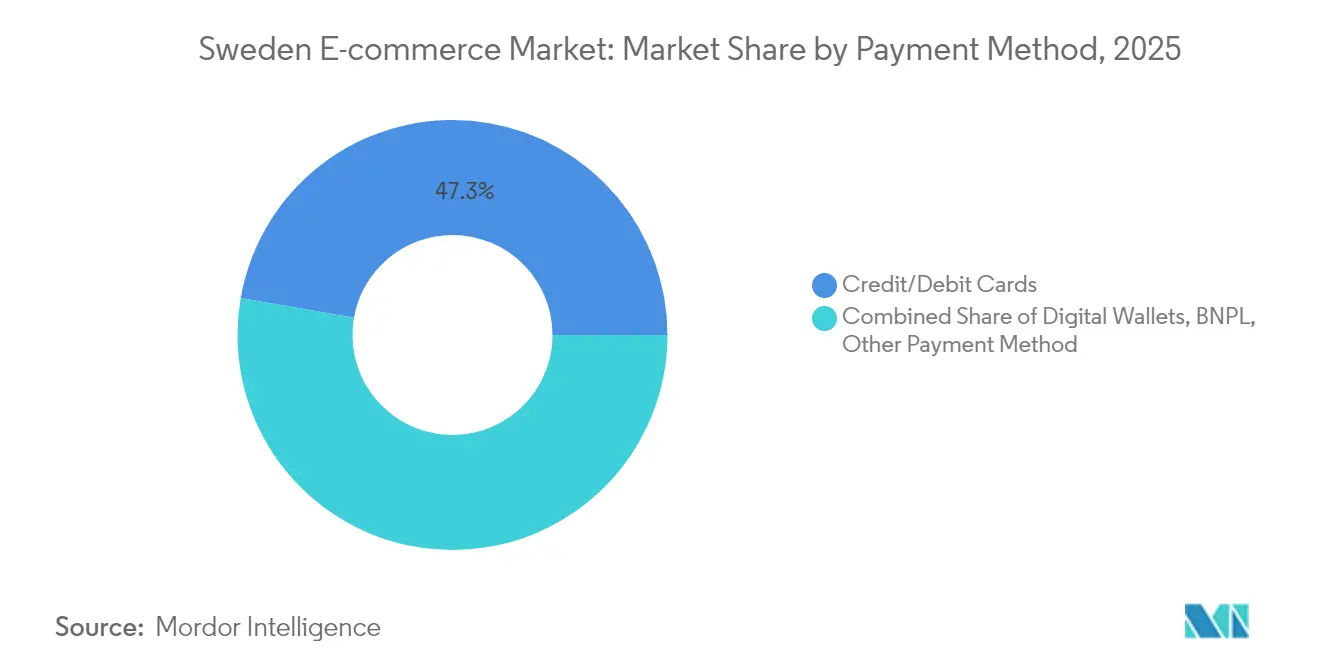

- By payment method, traditional cards held 47.25% share of Sweden e-commerce market size in 2025, whereas BNPL is advancing at a 6.81% CAGR.

- By B2C product category, consumer electronics led with 25.65% revenue share in 2025; food and beverages is forecast to grow at an 8.04% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sweden E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Card-less Mobile Payments (Swish) Surpassing Card Transactions in Urban Sweden | +1.2% | Stockholm, Gothenburg, Malmö urban centers | Short term (≤ 2 years) |

| Logistics-as-a-Service Networks Enabling Same-Evening Delivery in Greater Stockholm & Gothenburg | +0.8% | Stockholm metropolitan area, Gothenburg region | Medium term (2-4 years) |

| BNPL Regulation Driving Consumer Shift Toward Invoice-Based Check-outs | +0.6% | National, with higher adoption in urban areas | Medium term (2-4 years) |

| H&M, Ikea & Other Flagship Retailers' Rapid Marketplace Roll-outs Elevating Average Basket Size | +0.9% | National, with spillover to Nordic region | Long term (≥ 4 years) |

| EU Digital Product Passport Mandate Accelerating Re-commerce Platforms' Adoption | +0.4% | EU-wide, early implementation in Sweden | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Card-less Mobile Payments (Swish) Surpassing Card Transactions in Urban Sweden

Swish serves 7 million users, or close to 70% of residents, and now processes more urban e-commerce checkouts than cards.[1]Swish AB, “Annual Transaction Statistics 2024,” swish.nu Merchants integrating Swish report conversion gains of 15-20% because shoppers avoid manual card entry. Transaction fees are around 60% lower than card rails, allowing competitive pricing strategies that resonate with price-sensitive buyers. Since February 2024 Sweden’s access to the eurozone TIPS network delivers instant cross-border settlement in SEK, which lowers FX friction for Nordic shoppers and further raises merchant adoption.[2]Finextra, “Sweden Links Krona to TIPS Settlements,” finextra.com Local SMEs that previously balked at card fees can now participate online with minimal overhead, driving incremental digital sales.

Logistics-as-a-Service Networks Enabling Same-Evening Delivery

Velove’s cargo-bike hubs in Stockholm and Gothenburg fulfill more than 1 million orders with 95% on-time performance, eliminating roughly 40 diesel vans from city streets each day.[3]Velove, “Year in Review 2024,” velove.com The model reduces CO₂ emissions and avoids parking fines in restricted heritage zones, giving merchants a dual cost-and-sustainability dividend. Instabee, formed through the Budbee–Instabox merger, spans 40 million Nordic consumers and offers evening delivery on items ordered before 3 p.m., setting new benchmarks for speed. Same-evening fulfillment now acts as a strategic differentiator in fashion and electronics, elevating customer expectations across categories.

BNPL Regulation Driving Consumer Shift Toward Invoice-Based Check-outs

Sweden’s Financial Supervisory Authority imposes strict disclosure rules that cap late fees and mandate affordability checks. Klarna reported a profitable 2024 after absorbing USD 50 million in fines and re-engineering its credit scoring engine. Consumers retain flexible installment options for higher-value baskets, while default rates remain below many EU peers. The resurrection of digital invoices dovetails with Sweden’s historic comfort with post-delivery payments, keeping approval rates high. Retailers report order-value uplifts in furniture and electronics categories as risk-weighted credit limits expand responsibly.

H&M, IKEA & Other Flagship Retailers’ Rapid Marketplace Roll-outs

H&M generated USD 7 billion online, or 30% of total revenue, and now hosts third-party brands to extend assortment without inventory risk. Average basket size and frequency both climbed once complementary accessories appeared alongside core apparel lines. IKEA has earmarked USD 2.2 billion for omnichannel upgrades, including 900 pick-up points and circular-economy programs that align with national sustainability preferences. Marketplace functionality leverages existing trust in heritage retailers, speeds onboarding for niche labels, and raises Sweden e-commerce market visibility for cross-border shoppers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Pick-up-Point Congestion in Urban Hubs Raising Last-Mile Costs | -0.7% | Stockholm, Gothenburg city centers | Short term (≤ 2 years) |

| Stricter GDPR Fines Limiting Third-Party Data for Personalisation Engines | -0.5% | National, with EU-wide implications | Medium term (2-4 years) |

| Parcel Locker Licensing Bottlenecks in Heritage City Zones | -0.4% | National | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Escalating Pick-up-Point Congestion in Urban Hubs Raising Last-Mile Costs

PostNord plans to expand from 3,800 to 4,500 lockers, yet heritage zoning slows approvals, especially in Stockholm’s Gamla Stan where vehicle access has been cut by 50%. Couriers reroute to satellite micro-hubs and cargo bikes, but unit economics worsen as average parcel-drop density falls. Operators report 15-20% cost inflation on the final mile, prompting some merchants to raise delivery fees or enforce minimum-basket thresholds. Customer satisfaction risks erosion if fees climb faster than perceived service gains.

Stricter GDPR Fines Limiting Third-Party Data for Personalisation Engines

The Swedish Authority for Privacy Protection fined Klarna USD 733,000 for insufficient data disclosures and added a USD 50 million penalty later in 2024. Retailers now privilege first-party behavioural data, but smaller sellers lack the onsite traffic to achieve meaningful scale. Algorithmic recommendation accuracy suffers when external data feeds are pared back, nudging marketing spend toward broader contextual advertising. Larger platforms with deep loyalty programs widen their competitive moat under this compliance regime.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Platform Innovation Reinforces B2C Leadership

B2C routes generated 70.35% of Sweden e-commerce market revenue in 2025, supported by established omnichannel giants and born-digital specialists. The segment benefits from nationwide trust in regulated payment rails and robust consumer-protection frameworks that encourage repeat purchases. Marketplace extensions by H&M and IKEA illustrate how incumbents widen assortment while diluting inventory risk. These roll-outs push average order values higher, extend session duration, and enhance cross-sell efficacy across fashion, homeware, and lifestyle goods. C2C activity, expanding at 8.89% CAGR, capitalises on rising demand for sustainable consumption and transparent provenance. Platforms integrate Swish for instant settlement and leverage national ID verification, fostering secure peer-to-peer exchanges that in turn bolster overall Sweden e-commerce market liquidity.

The B2B corridor remains smaller but undergoes rapid digitisation as procurement managers prioritise efficiency. Enterprises migrate from fax-based ordering to cloud marketplaces that streamline approval workflows and automate invoice reconciliation. Standardised e-invoicing and compatibility with enterprise resource planning suites reduce error rates and accelerate payment cycles. Over time this modernisation diminishes channel fragmentation and incrementally raises Sweden e-commerce market size through corporate accounts.

By Device Type: Mobile-First Experiences Set the Standard

Smartphones captured 58.40% Sweden e-commerce market share in 2025 and will post the fastest 7.95% CAGR through 2031. Superior 5G coverage and large-screen adoption foster convenient browsing, while biometric authentication curtails checkout friction. Progressive web apps and mini-programs compress page-load times and reduce data consumption, a boon for commuters shopping during transit. Retailers deploy augmented-reality fitting and real-time stock look-ups that deepen engagement and raise conversion probabilities. Desktop retains relevance for configurable products and enterprise buyers that demand advanced filtering and data export. Tablet traffic sees modest growth as households use shared screens for group purchasing decisions, especially in furniture and travel.

Emergent interfaces such as smart speakers and connected car dashboards open fresh touchpoints. Voice ordering of grocery staples ties into predictive replenishment engines that learn consumption patterns. Early movers embed voice commerce capabilities to secure customer mindshare before competitors flood the space, further expanding Sweden e-commerce market penetration into daily routines.

By Payment Method: Transaction Diversity Fuels Conversion Gains

Cards still represent 47.25% share of Sweden e-commerce market size in 2025, anchored by mature interchange frameworks and widespread consumer familiarity. Yet Swish and other digital wallets entice younger cohorts with single-tap authentication, accelerating checkout by removing credential entry. BNPL advances at 6.81% CAGR as regulatory clarity safeguards borrower repayment capacity while preserving flexibility for high-ticket items. Integrations with digital ID systems trim onboarding friction, enabling near-instant credit lines that mirror card-based simplicity. Bank-direct transfers over the TIPS rail cut processing fees and provide guaranteed settlement, improving merchant cash flow compared with traditional card rails.

Cryptocurrency remains niche yet gains traction in specific tech-savvy communities that value decentralisation. Merchants accepting crypto often convert proceeds immediately to fiat, hedging volatility while courting new customer segments. Payment choice abundance reduces cart abandonment and lifts overall Sweden e-commerce market conversion rates.

By B2C Product Category: Electronics Maturity Meets Food Velocity

Consumer electronics maintained the leading 25.65% revenue share in 2025, reflecting Sweden’s early-adopter culture and frequent hardware upgrade cycles. Bundling of extended warranties and subscription software elevates lifetime value on each device sale. Intense price-comparison behaviour keeps margins tight, so retailers differentiate through rapid fulfilment and premium support. Food and beverages exhibit the fastest 8.04% CAGR as same-day fulfilment and temperature-controlled last-mile options dissipate prior freshness concerns. MatHem’s partnership with Clas Ohlson signals ecosystem convergence that marries grocery with home-improvement cross-promotions.

Apparel and beauty categories embrace virtual try-on features and generous return windows that closely replicate in-store evaluation. Circular-fashion momentum propels resale marketplaces, offering brands a stake in second-life monetisation. Subscription boxes proliferate in beauty and specialty foods, locking in predictable revenue and data-rich feedback loops that feed continuous assortment tuning within the Sweden e-commerce market.

Geography Analysis

Greater Stockholm and Gothenburg together account for about 60% of national online orders, a function of population density, high disposable income, and dense parcel-locker networks. Stockholm benefits from multiple urban consolidation centres that shorten stem-miles and enable cargo-bike penetration on narrow medieval streets, trimming emissions by 73% when paired with micro-terminals. Gothenburg leverages port infrastructure to support import-to-consumer flows that compress lead times on international goods and elevate cross-border turnover within the Sweden e-commerce market.

Malmö capitalises on Øresund Bridge proximity, encouraging Danish shoppers to exploit price variations and favourable SEK exchange dynamics. Rural municipalities experience accelerating adoption as 5G coverage blankets sparsely populated areas. Nevertheless, elevated delivery surcharges persist outside major conurbations, challenging profit margins on low-value baskets. Some merchants experiment with community locker clusters in village centres to consolidate drop density and lower cost per parcel.

Internationally, Sweden’s membership of the EU single market and participation in TIPS facilitate friction-less cross-border trade. Nordic logistics alliances coordinate line-haul routes and share micro-fulfilment infrastructure, mitigating duplicate capital expenditure. Swedish sellers increasingly list on pan-European marketplaces, extending customer reach while preserving domestic fulfilment control. This outward orientation further enlarges Sweden e-commerce market size as local inventory addresses regional demand.

Competitive Landscape

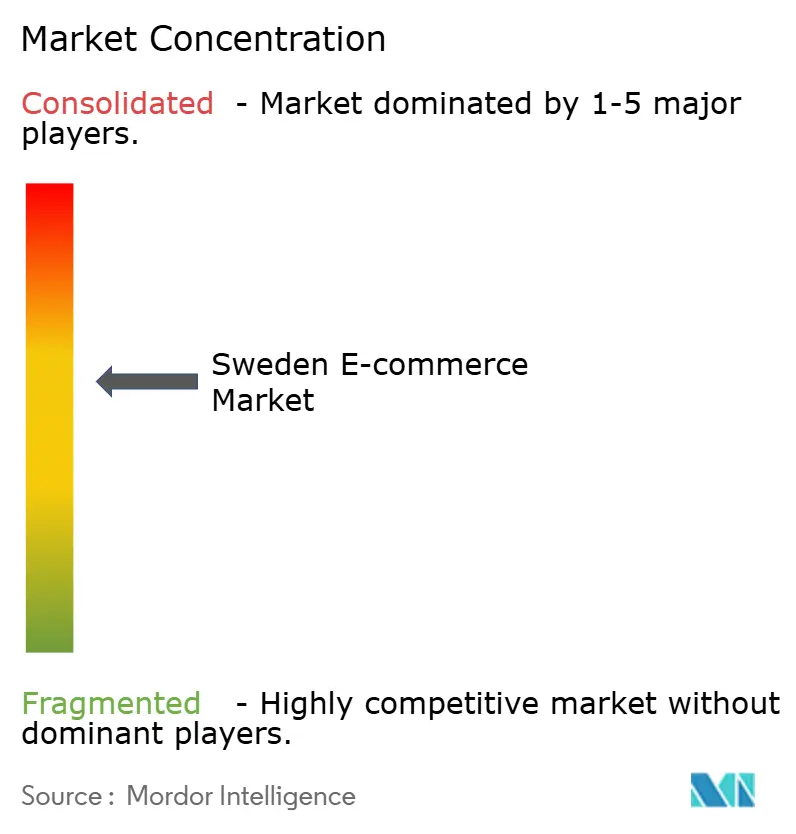

The market shows moderate concentration: the five largest platforms capture slightly under 60% of total Gross Merchandise Value, leaving room for agile specialists. H&M and IKEA exemplify omnichannel synergy by steering in-store traffic toward digital exclusives, thereby smoothing inventory turnover and deepening data capture. Amazon Sweden intensifies price transparency and accelerates two-day delivery benchmarks, pushing domestic players to enhance last-mile capabilities. Meanwhile, regional champions such as CDON pivot to third-party marketplace models that monetise site traffic without significant inventory risk.

Strategic M&A continues to reshape competitive lines. Axfood’s SEK 1.7 billion (USD 153 million) acquisition of City Gross expands fresh-food assortments and unlocks supply-chain synergies that lower per-parcel pick-rates. Clas Ohlson’s USD 26 million stake in MatHem brings home-improvement SKUs onto grocery delivery vans, creating one-stop convenience for household errands. Technology partnerships also flourish: Voyado’s SEK 3.5 billion (USD 0.37 billion) valuation round secures funds for AI-based loyalty modules that bolster repeat conversion metrics for fashion and lifestyle retailers.

Emerging disruptors differentiate on sustainability and hyper-local curation. Velove’s zero-emission deliveries attract eco-conscious brands seeking to align logistics with corporate responsibility targets. Nelly Group sustains niche apparel leadership through influencer collaboration pipelines that shorten trend cycles. Competitive intensity is therefore defined by agility in fulfilment, data-driven merchandising, and responsible consumer engagement frameworks across the Sweden e-commerce market.

Sweden E-commerce Industry Leaders

Elgiganten

Webhallen Sverige AB

Zalando SE

Apotea AB

NetOnNet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Voyado secured majority investment from Viking at a SEK 3.5 billion (USD 317 million) valuation, enabling accelerated roll-out of AI-driven loyalty engines that retailers deploy to deepen customer lifetime value while H&M retains a strategic share.

- April 2025: Storytel Group surpassed 2.5 million subscribers, underlining the scalability of content-based e-commerce models that cross-sell audiobooks into broader digital media bundles.

- March 2025: H&M unveiled a digital relaunch focused on seamless 360-degree customer journeys; marketplace expansion remains central, reinforcing multi-brand basket building.

- January 2025: Axfood completed the SEK 1.7 billion (USD 153 million) purchase of City Gross, consolidating grocery market share and streamlining e-commerce fulfilment.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Swedish e-commerce market as domestic or cross-border online purchases of physical goods by Swedish residents via websites or apps.

Scope exclusion: Pure digital content, gambling, and B2B procurement suites sit outside reported totals.

Segmentation Overview

- By Business Model

- B2C

- B2B

- C2C

- By Device Type

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method

- Credit / Debit Cards

- Digital Wallets

- BNPL

- Other Payment Method

- By B2C Product Category

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed marketplace heads, payment firms, carriers, and consumer-brand managers across major Swedish cities. Inputs on basket sizes, BNPL uptake, and reverse-logistics costs tuned model assumptions.

Desk Research

We pulled baseline numbers from Statistics Sweden, the Post & Telecom Authority, and the Riksbank that outline internet reach and card flows. Checkout values from Svensk Digital Handel and Ecommerce Europe, plus merchant filings seen on Dow Jones Factiva and D&B Hoovers, refine average prices and return ratios. The sources noted are illustrative; many other open and paid references supported validation.

Market-Sizing & Forecasting

We begin with a top-down build from card and Swish totals, then balance them against PostNord parcel counts. Targeted bottom-up checks, store revenue roll-ups, and sample ASP × volume for electronics, fashion, and grocery anchor the model. Smartphone use, parcels per capita, payment mix, VAT thresholds, and holiday uplift feed a multivariate regression, while scenario analysis layers regulatory shifts. This is where Mordor Intelligence differentiates, and outputs are cross-checked before release.

Data Validation & Update Cycle

Results clear two analyst reviews and variance screens versus household spend. Reports refresh annually, and interim updates trigger when transaction lines move five percent or policy shocks occur.

Why Mordor's Sweden E-commerce Baseline Earns Trust

Published estimates vary because some fold in services, leave returns gross, or freeze exchange rates.

Benchmark of current-year values

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.83 B (2025) | Mordor Intelligence | - |

| USD 15.11 B (2024) | Regional Consultancy A | Combines B2B and gross figures |

| USD 22.20 B (2021) | Government Portal B | Includes travel & services, outdated FX |

These contrasts show how our tight scope, live exchange rates, and dual validation give users a balanced, repeatable baseline.

Key Questions Answered in the Report

What is the current size of the Sweden e-commerce market?

The Sweden e-commerce market is worth USD 15.67 billion in 2026 and is on track to reach USD 20.63 billion by 2031.

Which segment holds the largest Sweden e-commerce market share?

B2C sales dominate with 70.35% of market revenue in 2025, reflecting strong consumer trust in direct-to-consumer platforms.

How fast is mobile shopping growing in Sweden?

Smartphones command 58.40% of transactions and are set to grow at 7.95% CAGR through 2031 as 5G coverage and biometric checkout become ubiquitous.

Why are BNPL services popular in Sweden?

BNPL combines flexible instalments with strict regulatory oversight that keeps default rates low, helping the payment option expand at a 6.81% CAGR in high-ticket categories.

How are logistics providers tackling last-mile congestion?

Operators deploy cargo-bike micro-hubs and expand locker networks, reducing emissions and sidestepping vehicle restrictions in historic city centres.

What impact will the EU Digital Product Passport have on Swedish e-commerce?

Mandatory product passports will boost resale confidence and data transparency, accelerating the growth of re-commerce platforms ahead of the 2027 enforcement deadline.

Page last updated on: