Europe Offshore Helicopter Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

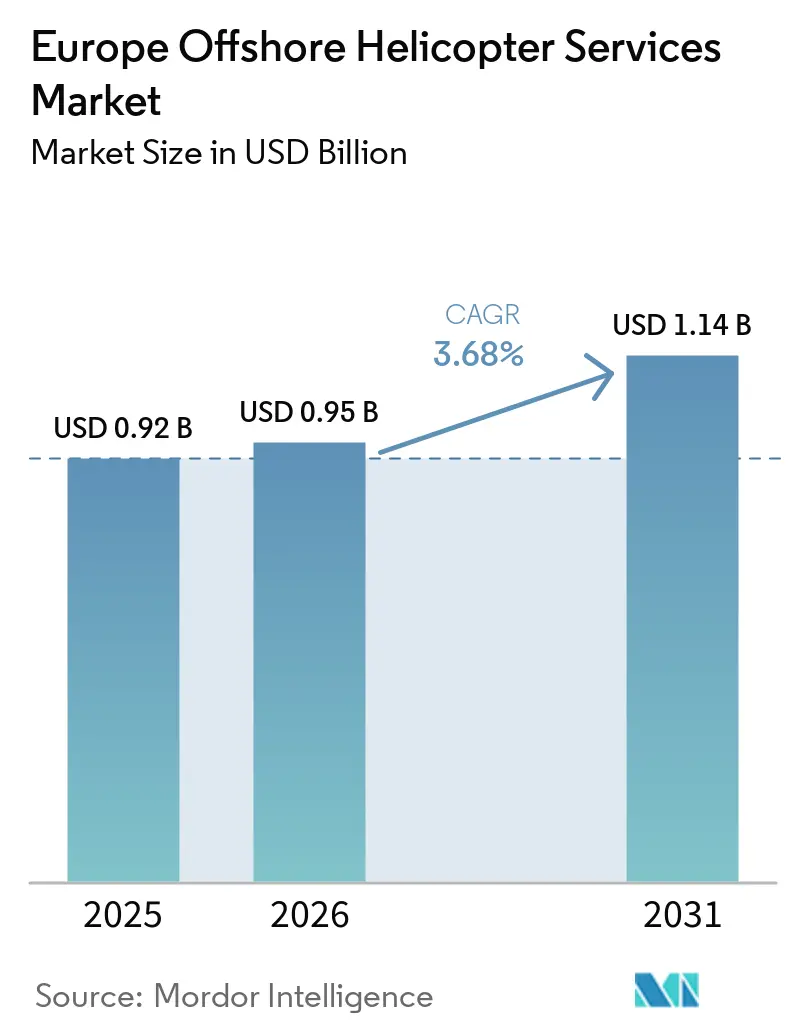

| Base Year Market Size (2025) | USD 0.92 Billion |

| Market Size (2026) | USD 0.95 Billion |

| Market Size (2031) | USD 1.14 Billion |

| Growth Rate (2026 - 2031) | 3.68% CAGR |

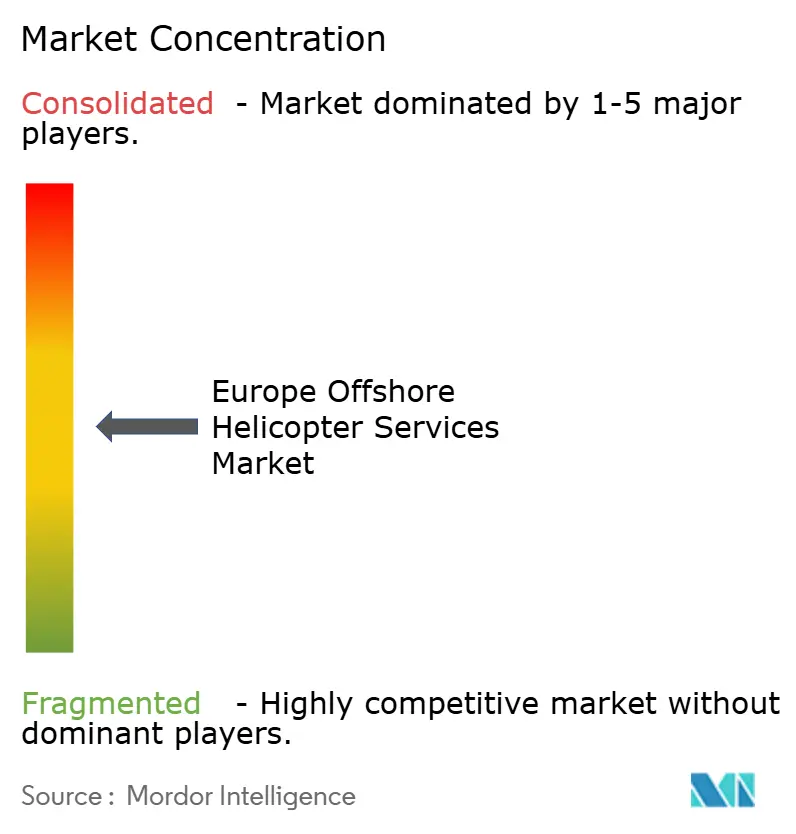

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Offshore Helicopter Services Market Analysis by Mordor Intelligence

The Europe Offshore Helicopter Services Market size is projected to expand from USD 0.92 billion in 2025 and USD 0.95 billion in 2026 to USD 1.14 billion by 2031, registering a CAGR of 3.68% between 2026 to 2031. Fleet renewal toward super-medium helicopters, the rapid build-out of wind farms situated more than 50 kilometers from shore and multi-year oil-and-gas contract awards underpin the market’s steady advance. Operators are diversifying away from the aging Sikorsky S-92, whose gearbox bottleneck constrains capacity, and embracing the Airbus H175 and Leonardo AW189 that lower per-seat costs on 100-kilometer legs. Meanwhile, crew-transfer vessels (CTVs) are seizing sub-30-kilometer routes, compelling helicopter carriers to redeploy aircraft toward longer missions. Finally, the EU’s sustainable-aviation-fuel blending rules and Phase IV emissions-trading costs are squeezing margins, pushing operators to negotiate pass-through clauses or adopt more fuel-efficient airframes.

Key Report Takeaways

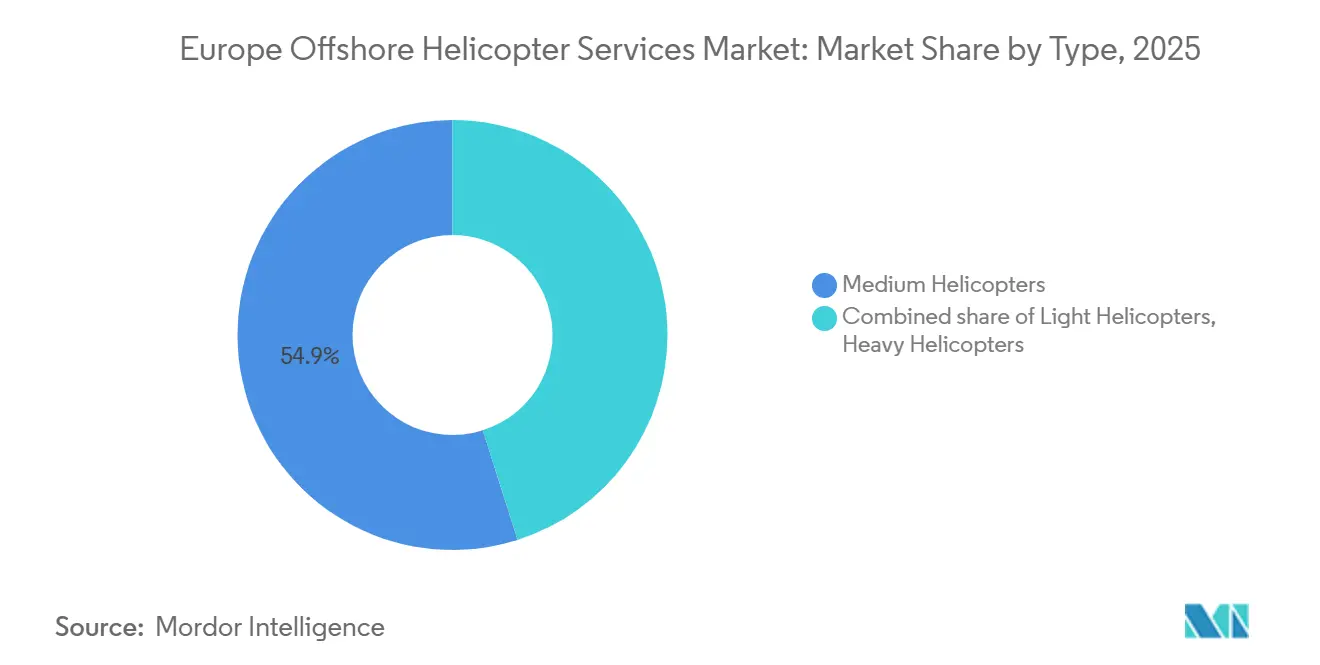

- By type, medium helicopters led with 54.9% of the Europe offshore helicopter services market share in 2025, while light helicopters are forecast to post the fastest 6.1% CAGR through 2031.

- By application, crew transport commanded 43.1% of the Europe offshore helicopter services market size in 2025 and inspection, monitoring and surveying is expected to expand at a 6.9% CAGR to 2031.

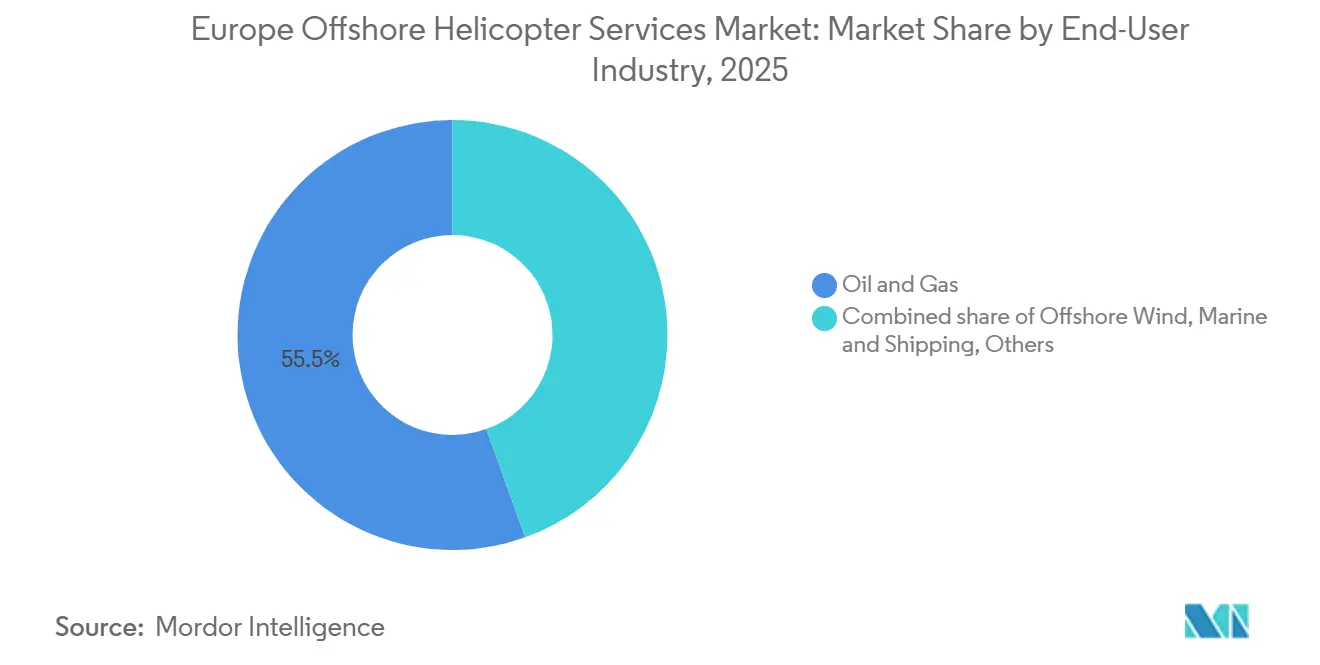

- By end-user industry, the oil and gas segment accounted for 55.5% of the Europe offshore helicopter services market size in 2025, whereas offshore wind is projected to register an 8.7% CAGR over the same period.

- By geography, the United Kingdom held 34.7% of regional revenue in 2025 and Denmark is projected to advance at a 7.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Offshore Helicopter Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Offshore wind build-out beyond 50 km from shore | +1.20% | UK, Germany, Denmark, Netherlands | Medium term (2-4 years) |

| Reshoring of deep-water rigs to Northern North Sea | +0.60% | Norway, UK | Short term (≤ 2 years) |

| Heavy-IFR super-medium fleet renewal cycle | +0.80% | UK, Norway, Netherlands | Medium term (2-4 years) |

| EU sustainable-aviation-fuel blending mandates | +0.30% | EU-wide | Long term (≥ 4 years) |

| OEM digital twins enabling predictive maintenance | +0.40% | UK, Norway, Germany | Medium term (2-4 years) |

| Green-corridor tax incentives for low-noise rotorcraft | +0.20% | Netherlands, Denmark, Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Offshore Wind Build-Out Beyond 50 km From Shore

Projects located farther offshore eliminate the economic viability of CTVs because sea-state limits prolong transits past two hours each way. Germany’s Nordlicht field, positioned 85 kilometers offshore, and the UK’s Outer Dowsing array at 54 kilometers both specify helicopter logistics for technician rotations and emergency response.[1]Offshore Wind, “Germany’s Nordlicht Offshore Wind Farm,” offshorewind.biz Belgium’s 5 GW Princess Elisabeth Island energy hub incorporates a helideck to coordinate wind-farm maintenance across multiple clusters.[2]Elia Group, “Princess Elisabeth Island Energy Hub,” eliagroup.eu Such infrastructure hard-wires long-term helicopter demand because OEM maintenance contracts stipulate aerial access to hit turbine-uptime guarantees. Upcoming projects like East Anglia TWO, with first power due 2028, further widen the addressable route portfolio.

Reshoring of Deep-Water Rigs to the Northern North Sea

Equinor’s Rosebank development and the redeployment of the Deepsea Bollsta to Norwegian waters in 2025 illustrate a reversal of the post-2014 rig exodus.[3]Offshore Energy, “Outer Dowsing Offshore Wind Farm,” offshore-energy.biz Rig activity triggers regular crew-change flights out of Sumburgh and Bergen, highlighted by Equinor’s NOK 4.3 billion Bergen contract split between CHC and Lufttransport in October 2025.[4]Offshore Energy, “Outer Dowsing Offshore Wind Farm,” offshore-energy.biz Decommissioning campaigns Shell’s Brent Delta and AF Gruppen’s 39,500-ton platform lift also need heavy-lift sorties, ensuring a baseline of missions even as production wanes.

Heavy-IFR Super-Medium Fleet Renewal Cycle

Sikorsky S-92 gearbox shortages lengthen downtimes to 18–24 months, so operators are pivoting toward the Leonardo AW189 and Airbus H175. Bristow ordered four AW189s in late 2025 for North Sea deployment. Lufttransport and PHI also expanded AW189 fleets under framework deals announced at Verticon 2025. The 16- to 19-seat super-medium class bridges the payload gap while delivering 15% better fuel burn than heavy types, lowering exposure to ETS costs.

EU Sustainable-Aviation-Fuel Blending Mandates

ReFuelEU requires 2% SAF in 2025, climbing to 6% by 2030 and 70% by 2050. HeliService International’s Baltic Eagle pilot confirmed technical feasibility but faced a 15-20% cost premium. Operators at Aberdeen, Stavanger and Den Helder are negotiating pass-through clauses, yet oil-and-gas clients resist surcharges, squeezing operating margins.

Restraints Impact Analysis*

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Two-year production bottleneck for S-92 gearboxes | -0.50% | UK, Norway | Short term (≤ 2 years) |

| North Sea crew-transfer-vessel substitution on short hops | -0.70% | Netherlands, UK, Denmark | Short term (≤ 2 years) |

| Limited helideck capacity on next-gen floating turbines | -0.30% | UK, Norway | Medium term (2-4 years) |

| EU ETS Phase IV cost pass-through on jet-A1 | -0.40% | EU-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Two-Year Production Bottleneck for S-92 Gearboxes

Sikorsky’s Phase IV gearbox has slashed groundings, yet machining complexity still leaves an 18–24-month lead time. Carriers dependent on the 19-seat S-92 must lease aircraft or defer discretionary flights, inflating residual values for serviceable airframes and prompting Bristow’s pivot to AW189s.

North Sea Crew-Transfer-Vessel Substitution on Short Hops

Electric CTVs such as Tidal Transit’s 24-seat fleet and Artemis’ 36-knot EF-12 match helicopter transit times on sub-30-kilometer legs at lower per-seat cost. As wind-farm O&M contracts prioritize cost, helicopter flight hours on Dutch and UK near-shore routes are falling, pressuring carriers to redeploy assets to longer missions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Super-Medium Renewal Drives Fleet Mix

Medium helicopters held 54.9% of Europe offshore helicopter services market share in 2025 thanks to entrenched AW139 and H175 fleets serving 150-kilometer oil-and-gas corridors. Light helicopters are set to post a 6.1% CAGR to 2031 as operators choose lower-cost H135 or AW109 platforms for turbine blade inspections and short-hop crew rotations. Heavy helicopters, chiefly the S-92, remain essential for decommissioning lifts and deep-water rigs but face slower growth because gearbox bottlenecks restrict capacity and high fuel burn magnifies ETS exposure. The Europe offshore helicopter services market size tied to heavy types therefore grows below the overall CAGR.

Momentum is shifting to 16- to 19-seat super-medium aircraft. NHV’s H175 fleet began dedicated wind-farm service in April 2025, demonstrating the type’s 15% fuel-efficiency edge over heavy rivals. Bristow’s four AW189 deliveries between 2025 and 2026 widen mission flexibility, while Leonardo’s digital-twin modules extend component lives and lift dispatch reliability. As a result, super-medium platforms are expected to erode medium-segment Europe offshore helicopter services market share beyond 2028.

By Application: Inspection Surges as Turbines Age

Crew-transport flights accounted for 43.1% of Europe offshore helicopter services market size in 2025, but their growth is modest as CTVs nibble at near-shore routes. Inspection, monitoring and surveying is projected to clock a 6.9% CAGR through 2031, reflecting OEM mandates for predictive maintenance. Helicopters equipped with high-resolution cameras and thermal sensors can hover near nacelles, reducing technician ladder climbs and lowering downtime penalties. The Europe offshore helicopter services market share linked to inspection will therefore expand steadily, encouraged by eight-year SAR and inspection framework extensions such as Offshore Helicopter Services UK’s 2024 award.

Cargo transport and relocation flights remain bundled with crew missions, providing incremental revenue but limited dedicated growth. Decommissioning spikes are episodic, tied to platform removals like Shell’s Brent Delta programme. Search-and-rescue contracts continue to supply baseline flight hours, yet their rate-regulated nature caps upside potential.

By End-User Industry: Wind Outpaces Oil and Gas

Oil and gas contributed 55.5% of Europe offshore helicopter services market size in 2025, upheld by multi-year Equinor and Shell contracts. However, offshore wind is forecast to outpace every segment at an 8.7% CAGR as wind-farm clusters expand deeper into the North and Baltic Seas. Technicians must reach Nordlicht, Horns Rev 3 and Thor arrays that lie beyond economical CTV range, cementing high-frequency helicopter demand. Marine and government users offer stable but low-growth utilization focused on SAR and border-patrol missions.

Developers now embed helicopter availability targets into turbine-uptime service-level agreements, shifting operational risk to carriers. Operators that combine high aircraft availability with SAF roadmaps and digital maintenance solutions are best placed to win long-term offshore wind tenders.

Geography Analysis

The United Kingdom retained 34.7% of 2025 revenue, anchored by Aberdeen’s hub, satellite bases at Sumburgh and Norwich and Great Yarmouth’s public-funded operations campus slated to support East Anglia TWO from 2028. Despite CTV encroachment on southern North Sea legs, sustained decommissioning projects and deep-water rig activity keep UK flight hours high.

Norway remains the second-largest market. Equinor’s NOK 4.3 billion Bergen award and its NOK 1.9 billion Barents Sea contract to Bristow in February 2026 guarantee predictable volumes. The country’s harsh-weather profile preserves the helicopter’s comparative advantage over CTVs, particularly for SAR and medical evacuations.

Denmark is the fastest-growing geography at 7.0% CAGR. Thor, Horns Rev 3 and Ørsted legacy arrays extend beyond 50 kilometers, requiring hoisting-capable flights staged from Esbjerg and Billund. Avincis’ 2025 acquisition of KN Helicopters Denmark exemplifies corporate moves to capitalize on the Baltic wind pipeline. Germany and the Netherlands round out the core, propelled by Hollandse Kust, IJmuiden Ver and EnBW’s He Dreiht projects. Rest of Europe including Belgium, Poland and France grows modestly on floating-wind pilots but lacks the scale to meaningfully alter the regional mix before 2031.

Competitive Landscape

Bristow, CHC and Babcock capture roughly 60% of regional flight hours, giving the Europe offshore helicopter services market a moderate concentration profile. These incumbents leverage decades-long client ties, extensive safety records and simulator training centers at Aberdeen, Stavanger and Den Helder to protect share. NHV, Lufttransport and HeliService International thrive in niches: NHV specializes in wind-farm hoisting with H175s, Lufttransport balances oil-and-gas with government SAR and HeliService runs SAF pilots that appeal to ESG-minded wind developers.

Strategic moves are oriented around fleet modernization and geographic reach. Bristow’s four AW189 orders, CHC’s Bergen contract and Bond Helicopters’ five-year Perenco return demonstrate active bidding for high-margin North Sea routes. Babcock posted EUR 215 million Aviation revenue in H1 FY26, a 26% rise tied to new French contracts, signaling that diversified government and medical portfolios cushion commodity cycles. OEM collaboration accelerates new-type introduction; PHI’s 2025 deployment of the Airbus H160 under a Shell charter highlights risk-sharing arrangements that include training and spares guarantees.

Regulatory tailwinds favor younger fleets. The European Commission’s February 2026 proposal to tighten Annex 16 noise and CO₂ standards from 2027 will penalize operators reliant on older aircraft lacking retrofit pathways. Smaller carriers may struggle to fund replacements, driving further consolidation.

Europe Offshore Helicopter Services Industry Leaders

Bristow Group Inc.

CHC Group Ltd.

PHI Group Inc.

NHV Group

Babcock International Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The European Commission proposed Annex 16 amendments covering helicopter noise and emissions standards effective 2027

- February 2026: Bristow Group won a NOK 1.9 billion contract from Equinor for Barents Sea helicopter services.

- December 2025: Heli-One secured a maintenance extension with Leonardo for Norway’s AW101 SAR Queen fleet through 2030.

- November 2025: Babcock reported EUR 215 million Aviation segment revenue in H1 FY26, up 26% year-on-year.

Europe Offshore Helicopter Services Market Report Scope

Offshore helicopter services provide specialized aerial transportation, facilitating the movement of personnel, equipment, and cargo between onshore bases and offshore locations such as oil rigs, production platforms, ships, and wind farms. These services play a vital role in energy sector logistics, supporting crew transfers and emergency operations in challenging and remote environments.

The Europe Offshore Helicopter Services Market is segmented into type, application, end-user industry, and geography. By type, the market is segmented into light helicopters, medium helicopters, and heavy helicopters. By application, the market is segmented into crew transport, cargo transport, inspection, monitoring, and surveying, relocation and decommissioning support, and other applications. By end-user industry, the market is segmented into oil and gas, offshore wind, marine and shipping, and government and defence. The report also covers the market size and forecasts for the offshore helicopter services market across key countries in Europe, including the United Kingdom, Norway, the Netherlands, Denmark, Germany, and the Rest of Europe. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Light Helicopters |

| Medium Helicopters |

| Heavy Helicopters |

| Crew Transport |

| Cargo Transport |

| Inspection, Monitoring, and Surveying |

| Relocation and Decommissioning Support |

| Other Applications |

| Oil and Gas |

| Offshore Wind |

| Marine and Shipping |

| Government and Defence |

| United Kingdom |

| Norway |

| Netherlands |

| Denmark |

| Germany |

| Rest of Europe |

| By Type | Light Helicopters |

| Medium Helicopters | |

| Heavy Helicopters | |

| By Application | Crew Transport |

| Cargo Transport | |

| Inspection, Monitoring, and Surveying | |

| Relocation and Decommissioning Support | |

| Other Applications | |

| By End-user Industry | Oil and Gas |

| Offshore Wind | |

| Marine and Shipping | |

| Government and Defence | |

| By Geography | United Kingdom |

| Norway | |

| Netherlands | |

| Denmark | |

| Germany | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe offshore helicopter services market in 2026?

The market is valued at USD 0.95 billion in 2026 and is on track to reach USD 1.14 billion by 2031.

Which helicopter segment is growing fastest?

Light helicopters are projected to expand at a 6.1% CAGR through 2031 as operators seek cost-efficient aircraft for short-range inspections.

Why is Denmark the fastest-growing geography?

Baltic Sea wind projects such as Thor and Horns Rev 3 sit more than 50 kilometers offshore, creating sustained demand for helicopter logistics and driving a 7.0% CAGR.

What is driving the shift toward super-medium helicopters?

Operators need aircraft that match heavy-helicopter range but burn less fuel, avoid S-92 gearbox delays and qualify for forthcoming noise and emissions rules.

How do EU emissions rules affect operators?

Phase IV of the EU ETS adds EUR 5-7 per flight hour in allowance costs, pressuring carriers to adopt fuel-efficient helicopters or negotiate cost pass-through clauses.

Page last updated on: