Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 19.39 Billion |

| Market Size (2026) | USD 20.29 Billion |

| Market Size (2031) | USD 25.49 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Modular Construction Market Analysis by Mordor Intelligence

Europe Modular Construction Market size in 2026 is estimated at USD 20.29 billion, growing from 2025 value of USD 19.39 billion with 2031 projections showing USD 25.49 billion, growing at 4.63% CAGR over 2026-2031. Modular construction in Europe is gaining momentum due to its ability to accelerate delivery schedules and support housing programs, with resilient order books despite a slowdown in broader construction output. Investors view the sector as a structural growth opportunity, driving investments in factory capacity and design innovation. Medium-sized manufacturers face pressure to scale quickly to compete with large incumbents and niche players. While steel dominates the current market, opportunities for concrete and hybrid systems indicate a future with diverse material solutions. Key markets like the UK, Germany, the Nordics, and Eastern European hubs benefit from policy incentives, sustainability goals, and skills shortages. The UK, holding a 22% market share in 2024, is poised for further growth with digital permitting tools and updated safety regulations. The shift toward permanent modular buildings in social housing and healthcare, coupled with revised risk models by insurers and lenders, is reducing financing costs and driving supply-chain investments toward vertically integrated models to meet multi-country demand.

Key Report Takeaways

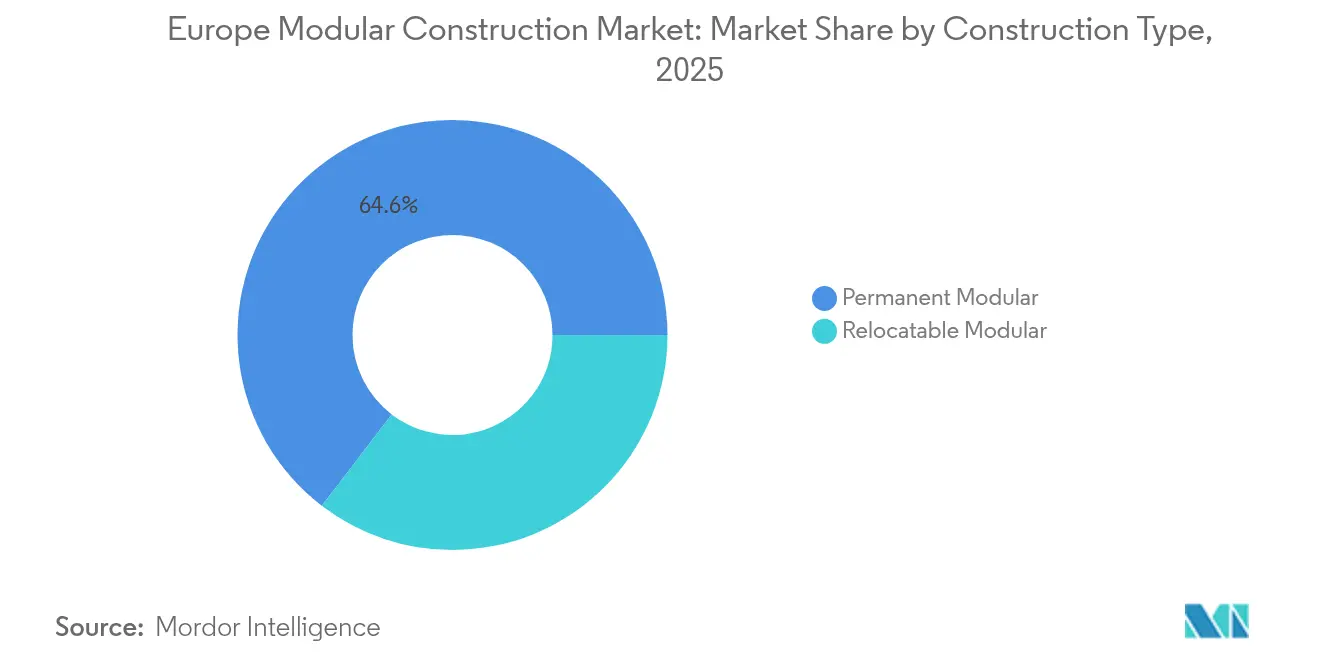

- By construction type, permanent modular led with 64.60% of the European modular construction market share in 2025, and is the fastest-growing type at a 5.17% CAGR through 2031.

- By material, steel held 47.70% of the European modular construction market share in 2025, and is projected to expand at a 5.54% CAGR to 2031.

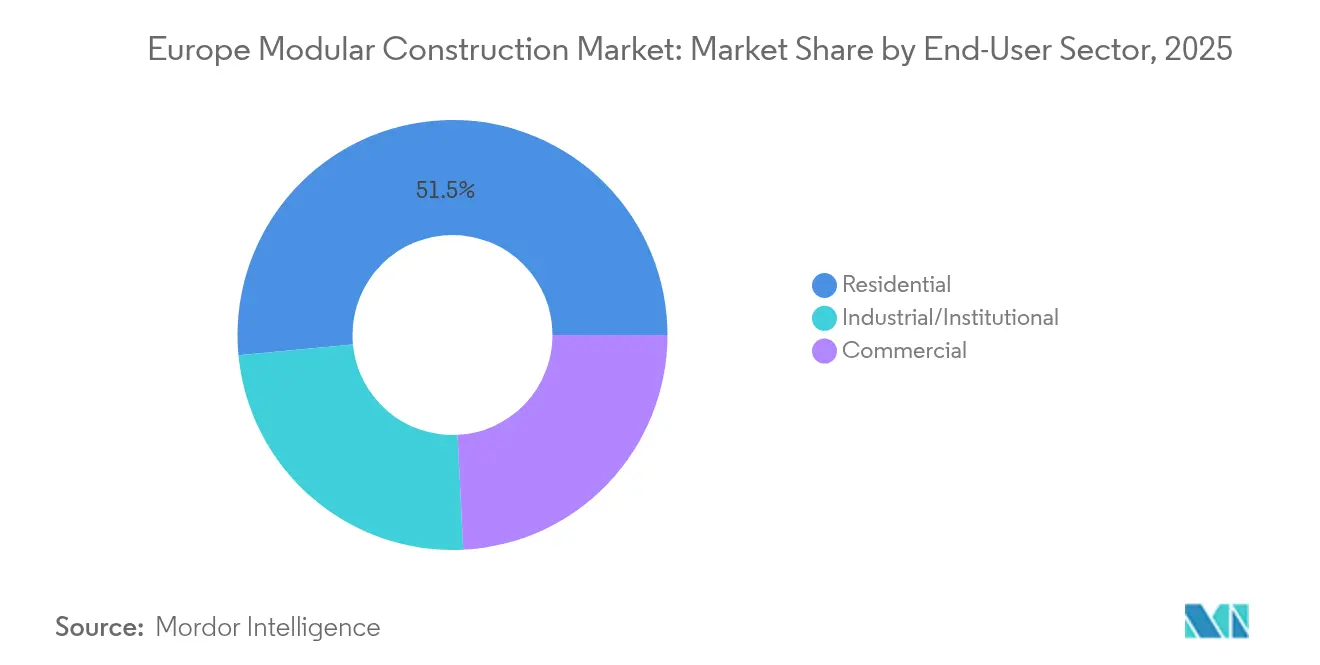

- By end-user sector, residential commanded 51.50% of the European modular construction market size in 2025; Industrial/Institutional are advancing at a 5.38% CAGR to 2031.

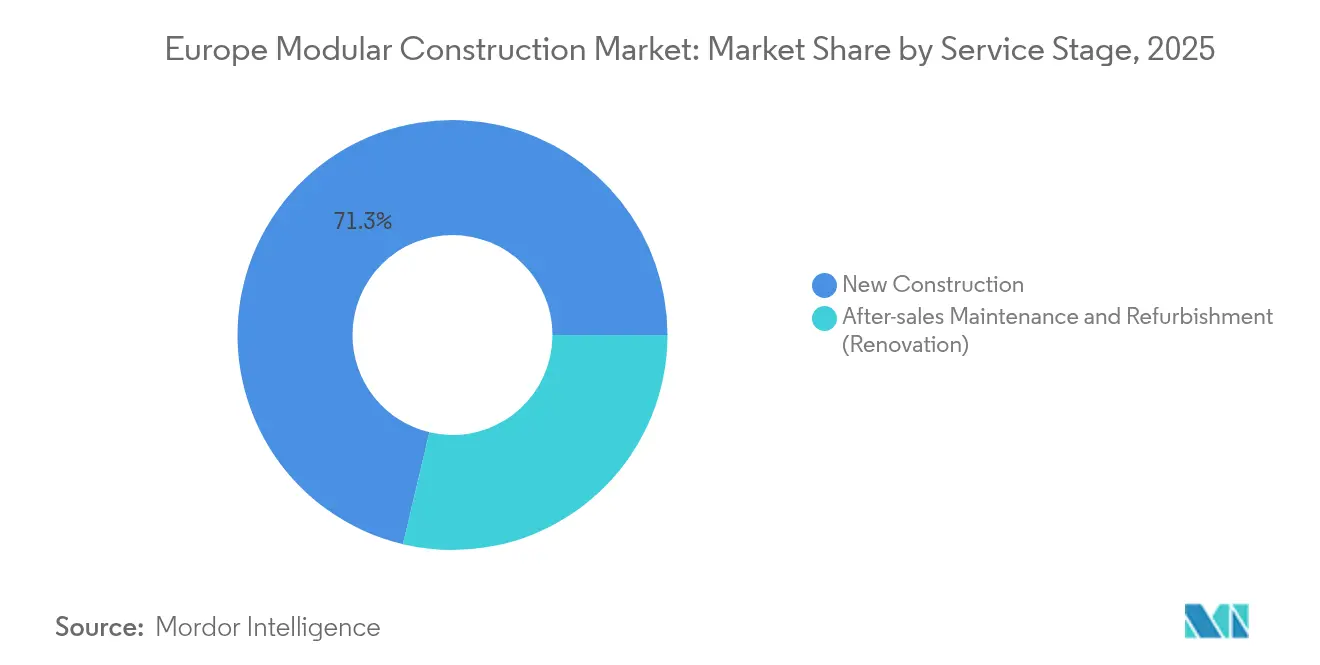

- By service stage, new construction led with 71.30% of the European modular construction market share in 2025; after-sales maintenance is projected to expand at a 5.27% CAGR through 2031.

- By region, United Kingdom captured 21.80% of the European modular construction market share in 2025 and is set to grow at the highest regional CAGR of 7.12% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Modular Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supportive Government Initiatives for Modular Construction | +1.20% | UK, Germany, France, Nordics | Medium term (2-4 years) |

| Rising Demand for Temporary/Portable Structures | +0.80% | Pan-European, strongest in UK | Short term (≤ 2 years) |

| Significantly Reduced Project Timelines | +1.00% | Pan-European | Short term (≤ 2 years) |

| Off-Site Labour Solutions Offsetting Ageing Workforce in Europe | +0.70% | Germany, UK, Nordics | Medium term (2-4 years) |

| Focus on Sustainability and Reduced Carbon Emissions | +1.10% | Pan-European, strongest in Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supportive Government Initiatives for Modular Construction

Policy support is steadily converting into real contracts across core markets. The UK Future Homes Standard consultation, completed in 2024, establishes energy-performance thresholds that modular systems meet with less cost, and that incentivize developers to specify off-site solutions. Germany’s KfW climate-friendly new-build program channels state-subsidized loans toward low-carbon units, indirectly favoring factory precision that reduces thermal bridging. A clear inference here is that governments are linking financial support to measurable environmental outcomes, thereby rewarding manufacturers able to document carbon savings.

Rising Demand for Temporary/Portable Structures

Businesses now view relocatable modules as strategic assets that solve space volatility without locking in long lease liabilities. Rental fleets for education, health care, and light industrial uses are being redeployed more frequently, signaling that the value proposition has shifted from cost saving to operational agility. Providers such as Algeco have widened product height limits to four storeys, which means a broader set of applications can be served without bespoke engineering. The takeaway is that higher utilization rates quietly improve capital returns in the European Modular Construction market.

Significantly Reduced Project Timelines

Factory fabrication can compress overall schedules by up to half, and developers are translating the time saved into earlier revenue recognition or reduced interim financing charges. Hospitals commissioned during the pandemic demonstrated that completed floor space could be handed over weeks earlier than brick-and-mortar builds, validating the modular approach for critical infrastructure. That experience has altered procurement checklists, with speed now weighted as heavily as price and aesthetics. An emergent inference is that accelerated timelines indirectly raise building volume capacity for overstretched contractors.

Focus on Sustainability and Reduced Carbon Emissions

Factory precision lowers waste to single-digit percentages, and material optimization reduces embodied carbon relative to conventional builds. Fossil-free steel trials, such as the SSAB-Parmaco concept building scheduled for 2025[1]SSAB AB, “SSAB and Parmaco team up to build the world’s first fossil-free steel concept building,” ssab.com , illustrate how modular construction can align with corporate net-zero commitments. Meanwhile, lifecycle data indicates that modular homes can cost markedly less to heat, amplifying their appeal in an energy-price-sensitive Europe. The implication is that sustainability credentials are becoming a decisive differentiator in winning public-sector tenders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Country-Level Certification (BBA, Avis Technique, ETA) Slowing Cross-Border Supply | -1.00% | Pan-European, most acute at borders | Medium term (2-4 years) |

| High Initial Investment | -0.90% | Pan-European | Short term (≤ 2 years) |

| Design Limitations | -0.60% | Pan-European, less in Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Country-Level Certification Slowing Cross-Border Supply

Different national approvals—BBA in the UK, Avis Technique in France, and ETA for non-standard products—force suppliers to navigate multiple testing regimes, adding time and cost. Dual CE and UKCA marking services offered by organizations such as Bureau Veritas[2]Bureau Veritas, “Bureau Veritas and the British Board of Agrément partner up to provide the construction products industry with dual marking,” group.bureauveritas.com mitigate the issue but still require duplicated paperwork. Smaller firms often restrict themselves to domestic markets, which unintentionally limits economies of scale across Europe. An immediate inference is that companies mastering regulatory complexity gain a competitive moat in export opportunities.

Design Limitations

Historic perceptions of “boxy” modular units persist, yet award-winning projects like the reconfigurable Study Pavilion in Braunschweig show how flexible grids can unlock architectural creativity. Advances in connection technology allow bigger spans and varied façade treatments, eroding the visual gap between modular and site-built options. Clients are beginning to understand that standardization lives mainly in hidden structural frames, not in external appearance. Therefore, design freedom is expanding in parallel with technical refinements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Construction Type: Permanent Solutions Gaining Momentum

Permanent modular buildings account for 64.60% of Europe Modular Construction market size in 2025 and are projected to expand at a 5.17% CAGR to 2031, outpacing the industry average. Demand stems from the growing conviction that factory-built homes, schools, and clinics deliver enduring performance equal to traditional structures. Developers recognise that bank valuations now increasingly accept permanent modules at full parity with masonry, which removes a historic financing barrier. The segment’s ascent implies factories will need to switch from short production runs to continuous flow manufacturing to meet volume expectations.

A related observation is that product innovation focuses on hybrid steel-and-timber frames that merge strength with lower embodied carbon, signaling more diverse material palettes ahead. As councils and housing associations chase energy-efficiency targets, permanent modular solutions become the default for achieving tight thermal envelopes within cost caps. The inference is that planners may soon reference volumetric typologies directly in zoning guidance, further mainstreaming the approach.

Material: Steel Leads Innovation and Growth

Steel modules hold 47.70% Europe Modular Construction market share in 2025 and demonstrate the fastest expansion at 5.54% CAGR through 2031. Superior strength-to-weight ratios permit larger column-free interiors, supporting open-plan offices and adaptable healthcare bays. Pioneering fossil-free steel referenced earlier suggests that emissions associated with steel frames could fall significantly, enhancing the material’s sustainability narrative. An immediate inference is that manufacturers able to secure low-carbon steel billets early will gain preferred-supplier status on green projects.

Concrete remains an essential contender for high-rise modular towers where mass aids acoustic and fire performance, while innovations in alkali-activated binder mixes point toward lower CO₂ pathways. Plastic-composite elements, though the smallest slice, carve out niche use cases in corrosion-prone environments like coastal data centers. Collectively, this material diversity reduces supply risk and allows architects to tailor specifications to site constraints, hinting at expanded design flexibility across the industry.

End-user Sector: Residential Dominance Meets Industrial Growth

Residential applications command 51.50% of the European Modular Construction market size in 2025, nourished by acute housing deficits and ambitious build-out targets in the UK and other states. Modular systems offer repeatable floor plans that satisfy affordable housing benchmarks while compressing delivery cycles, thereby freeing up capacity for additional schemes. A subtle inference is that volume housebuilders are forming alliances with module factories to ring-fence slots and guarantee pipeline flow, echoing automotive just-in-time logistics.

The industrial/institutional sub-sector, though smaller today, is projected to grow at 5.38% CAGR to 2031, driven by healthcare expansions and advanced manufacturing plants that value predictability. Biopharma clean-rooms and battery gigafactories are choosing modular sub-fab assemblies to meet aggressive commissioning dates, turning what was once a niche solution into a strategic default. In practice, this diversification reduces reliance on residential cycles and smooths revenue volatility for suppliers.

Service Stage: New Construction Dominates While Refurbishment Accelerates

New builds represent 71.30% of the 2025 Europe Modular Construction market share, yet refurbishment services are accelerating at a 5.27% CAGR that slightly tops new-build growth. Ageing public-sector real estate is ripe for modular over-cladding and volumetric extensions that minimize disruption to daily operations. Digital design twins allow accurate as-built surveys, letting installers prefabricate retrofit units that click onto facades with minimal tolerance gaps. Refurbishment projects provide counter-cyclical workload when new developments pause.

After-sales maintenance packages now bundle IoT-based energy dashboards, turning module suppliers into long-term service partners rather than one-off contractors. Examples such as the PHOENIX platform achieving double-digit percentage energy savings highlight the value of data-driven optimisation. As operating-expense reductions rise in importance for property owners, maintenance contracts could evolve into subscription revenue for modular firms, smoothing cash flow and enhancing investor appeal.

Geography Analysis

The United Kingdom accounts for 21.80% European Modular Construction market share in 2025 and is forecast to advance at 7.12% CAGR through 2031, well above the continental growth rate. Demand is powered by acute housing needs and a proactive regulatory environment that rewards energy-efficient prefabricated solutions. High-profile failures of some start-ups have sharpened investor focus on capitalization strength, meaning future capacity additions may come from joint ventures between established contractors and private equity funds. Consequently, the competitive set is consolidating even as demand climbs, signaling a maturing market phase.

Germany, supported by subsidies for climate-friendly housing, holds a significant share by channeling affordable financing toward compliant constructions. Industrial clients appreciate Germany’s precision-manufacturing culture, aligning naturally with off-site construction’s process discipline. Meanwhile, stricter energy regulations drive interest in airtight modular envelopes that can hit passive-house standards without extensive site rework. The inference is that German adoption will rise fastest in regions where factory clusters overlap with automotive and machinery supply chains, exploiting shared logistics networks.

France, the Nordics, Italy, Spain, and Eastern Europe compose the remainder, each exhibiting distinctive traits. Nordic countries benefit from long winter daylight shortages that make off-site fabrication under roof more appealing, while Polish plants leverage lower labor costs to export volumetric frames westward. Fragmented certification still complicates cross-border module flows, but voluntary ETA routes provide partial relief for non-standard products. Taken together, regional diversity cushions the overall European Modular Construction industry against localized downturns, spreading risk for multi-country operators.

Competitive Landscape

The industry remains fragmented, yet a shift toward scale is visible as larger groups integrate design, manufacturing, and installation functions. Traditional contractors such as Skanska and Bouygues have invested in dedicated factories or acquired specialists, enabling them to offer turnkey modular packages alongside conventional services. Smaller pure-play entrants counter by focusing on speed, customization, or niche segments like healthcare pods. One practical inference is that hybrid partnership models will persist, where general contractors outsource volumetric fabrication while retaining site management.

Financial robustness has emerged as a critical differentiator in the wake of insolvencies. Diversified players like Algeco, backed by Modulaire Group’s pan-European asset base, can pivot units between rental and sale depending on market conditions. Technology partnerships represent the next competitive frontier. Few manufacturers have fully embedded digital twins or IoT performance monitoring into standard offerings, creating a white-space opportunity. Early adopters of data analytics can capture service revenues post-handover, turning buildings into connected assets. Suppliers mastering this capability will gain repeat business as facility managers prioritize operational efficiency throughout the asset life cycle.

Europe Modular Construction Industry Leaders

Modulaire Group

Bouygues Construction

Laing O’Rourke

Portakabin Ltd

Skanska

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Skanska sold its BoKlok Byggsystem modular housing factory in Gullringen, Sweden, to Surewood Housing for SEK 100 million. The divestment allows Skanska to redeploy capital into low-carbon product development.

- July 2024: Laing O’Rourke's Bristol Port factory has started producing large steel reinforcement cages, which play a critical role in strengthening concrete. This advancement is anticipated to drive growth in the European modular construction market by enhancing the durability and reliability of prefabricated construction materials.

Europe Modular Construction Market Report Scope

Modular construction is a construction technique that involves the prefabrication of 2D panels or 3D volumetric structures in off-site factories and transportation to construction sites for assembly. This process has the potential to be superior to traditional construction in terms of both time and cost. The Europe modular construction market is segmented by type, material, end-user, and by geography. By type, the market is segmented into permanent and relocatable. By material, the market is segmented into steel, concrete, wood, and plastic. By end-user the market is segmented into commercial, industrial/institutional, and residential. The report covers market sizes and forecasts for four major countries across the region. For each segment, the market sizing and forecast have been done on the basis of revenue (in USD million).

By Construction Type

| Permanent Modular |

| Relocatable Modular |

By Material

| Steel |

| Concrete |

| Wood |

| Plastic |

By End-user Sector

| Residential |

| Commercial |

| Industrial/Institutional |

By Service Stage

| New Construction |

| After-sales Maintenance and Refurbishment (Renovation) |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Nordics |

| Spain |

| Rest of Europe |

| By Construction Type | Permanent Modular |

| Relocatable Modular | |

| By Material | Steel |

| Concrete | |

| Wood | |

| Plastic | |

| By End-user Sector | Residential |

| Commercial | |

| Industrial/Institutional | |

| By Service Stage | New Construction |

| After-sales Maintenance and Refurbishment (Renovation) | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Nordics | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current Europe Modular Construction market size?

The market is valued at USD 20.29 billion in 2026.

How fast is the Europe Modular Construction market forecast to grow?

It is projected to register a 4.63% CAGR between 2026 and 2031.

Which country holds the largest market share in Europe?

The United Kingdom leads with about a 21.80% share in 2025.

Why is steel the dominant material in European modular construction?

Steel offers high strength-to-weight ratios and now benefits from emerging fossil-free production pathways.

What is driving demand for refurbishment modules?

Building owners seek energy upgrades and minimal disruption, making factory-built over-cladding and extensions attractive.

Page last updated on: