Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

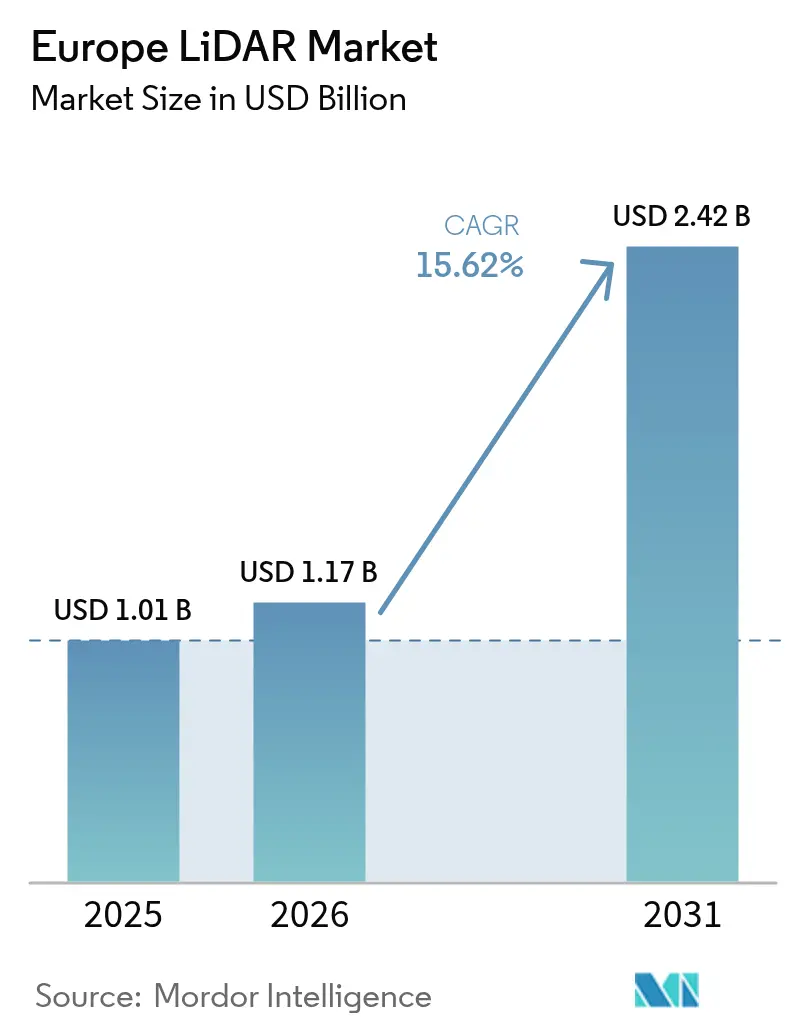

| Base Year Market Size (2025) | USD 1.01 Billion |

| Market Size (2026) | USD 1.17 Billion |

| Market Size (2031) | USD 2.42 Billion |

| Growth Rate (2026 - 2031) | 15.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe LiDAR Market Analysis by Mordor Intelligence

Europe LiDAR market size in 2026 is estimated at USD 1.17 billion, growing from 2025 value of USD 1.01 billion with 2031 projections showing USD 2.42 billion, growing at 15.62% CAGR over 2026-2031. Accelerated growth aligns with Euro-NCAP’s 2026 sensor-based safety mandates, EU-funded smart-city programs, and mandatory BIM Level 3 requirements that collectively reinforce LiDAR’s role in automotive, construction, and environmental monitoring. Market expansion also benefits from offshore wind-farm proliferation, where floating LiDAR systems now provide economically viable wind-resource assessments, and from rapid cost declines in solid-state sensors produced at automotive scale. Simultaneously, supply-chain diversification and the integration of advanced post-processing software shorten deployment cycles and widen applicability. Competitive intensity is rising as European incumbents face pricing pressure from Asian suppliers able to deliver automotive-qualified units in high volume, prompting strategic collaborations that bundle hardware, software, and lifecycle services for differentiation.

Key Report Takeaways

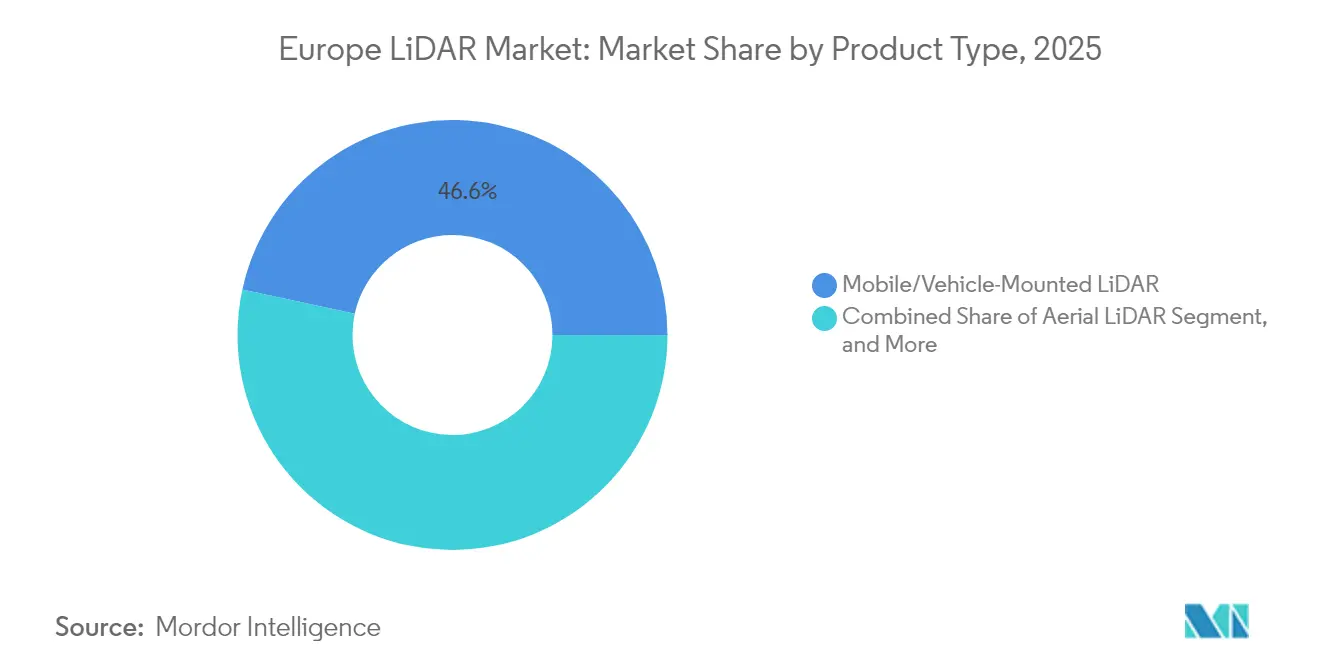

- By product type, Mobile/Vehicle-Mounted LiDAR led with 46.60% revenue share of the European LiDAR market share in 2025; Bathymetric/Marine solutions are projected to expand at a 16.6% CAGR to 2031.

- By technology, Mechanical Scanning held 51.20% of the European LiDAR market share in 2025, while FMCW/Hybrid systems record the highest projected CAGR at 16.7% through 2031.

- By platform, Ground Vehicles accounted for 39.10% of the European LiDAR market size in 2025, and Marine/Shipborne deployments are advancing at a 16.8% CAGR to 2031.

- By end-use, Automotive and Transportation captured 35.10% revenue share of the European LiDAR market in 2025; Aerospace and Defense applications are forecast to expand at a 17.0% CAGR through 2031.

- By country, Germany dominated with a 29.40% share of the European LiDAR market in 2025, whereas Spain is poised for the fastest growth at a 17.1% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe LiDAR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid ADAS uptake spurred by Euro-NCAP 2026 sensor-based safety ratings | +4.2% | Germany, France, United Kingdom, Nordics | Medium term (2-4 years) |

| UAV-LiDAR demand for corridor mapping and digital-twin projects | +2.8% | Germany, Netherlands, Spain, Nordics | Medium term (2-4 years) |

| Solid-state cost decline from automotive-scale production | +3.5% | Germany, France, Italy, Spain | Long term (≥ 4 years) |

| EU-funded smart-city LiDAR deployments | +2.1% | Netherlands, Germany, Spain, Belgium | Short term (≤ 2 years) |

| Offshore wind-farm site assessment via floating systems | +1.9% | United Kingdom, Germany, Netherlands, Denmark | Medium term (2-4 years) |

| Mandatory BIM Level 3 specs in EU public-works tenders | +1.5% | United Kingdom, Germany, Netherlands, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid ADAS uptake spurred by Euro-NCAP 2026 sensor-based safety ratings

Euro-NCAP’s revised 2026 protocol forces OEMs to deploy redundant perception suites that include LiDAR to achieve five-star scores. German premium brands have already commercialized Level 3 driving packages that bundle long-range LiDAR at price points exceeding EUR 5,000, validating consumer willingness to pay for the technology.[1]Reuters Staff, “Mercedes to develop smart cars for global markets with China's Hesai lidar,” Reuters, reuters.com Regulatory pressure compresses adoption timelines, encourages multi-sourcing strategies, and anchors high-volume demand forecasts through 2030. Infrastructure providers follow suit, upgrading test tracks and certification labs to handle multi-sensor validation, while tier-1s invest in solid-state roadmaps to meet cost-down targets. As a result, the European LiDAR market experiences cross-industry ripple effects, pushing suppliers to improve weather robustness and cybersecurity compliance simultaneously.

UAV-LiDAR demand for corridor mapping and digital-twin projects

Across rail, power, and fiber corridors, European engineering firms deploy drone-mounted LiDAR to obtain centimeter-level point clouds that feed asset-management platforms. Systems such as RIEGL’s miniVUX-2UAV deliver 200,000 measurements per second to capture true-color point clouds needed for vegetation encroachment and slope-stability analysis. Municipal agencies favor UAV workflows because flight permits can be issued rapidly under the EU’s risk-based drone rules, though strict BVLOS limitations still add planning complexity. Project owners note substantial cost savings versus helicopter surveys, and the ability to refresh datasets quarterly enables predictive maintenance regimes. As energy-transition projects proliferate, corridor-mapping volume feeds steady demand into the European LiDAR market, even as vendors lobby for uniform BVLOS standards to unlock scale.

Solid-state cost decline from automotive-scale production

OEM agreements, exemplified by Mercedes-Benz’s 2025 supply contract with Hesai, guarantee million-unit volumes that justify new 200 mm wafer fabs and automated back-end lines. Volume leverage reduces bill-of-materials by integrating VCSEL arrays and SPAD receivers on common substrates, slashing test times while lifting yield. European R&D houses such as Scantinel Photonics explore frequency-modulated continuous-wave (FMCW) architectures that integrate photonics and radar-style Doppler processing for simultaneous range and velocity detection. By 2030, average automotive solid-state unit prices are expected to fall by as much as 70%, enabling diffusion into construction machinery, port automation, and mobile robotics. This cost curve fundamentally reshapes the European LiDAR market, shifting revenue pools from low-volume, high-margin survey units toward mid-volume, mid-margin industrial installations.

EU-funded smart-city LiDAR deployments

The Horizon Europe program earmarked EUR 290 million for data and AI pilots, with LiDAR-enabled traffic analytics and air-quality mapping among the flagship demonstrators.[2]European Commission, “New Horizon Europe Funding Boosts European Research in Data, Computing, and AI Technologies,” digital-strategy.ec.europa.eu Dutch cities now install curb-mounted LiDAR pods that anonymously track multi-modal traffic, feeding adaptive signal controllers that lower congestion by double-digit percentages. LiDAR’s privacy-preserving point-cloud output allows authorities to comply with GDPR without facial-recognition concerns that plague camera networks. Vendors bundle edge compute modules to parse flow data on-device, easing bandwidth strain on municipal fiber backbones. Because EU funding stipulates open data sharing, integrators gain exposure to cross-border deployments, lifting addressable demand for interoperable solutions across the European LiDAR market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High unit cost of long-range, high-resolution sensors | -2.8% | Cost-sensitive segments continent-wide | Medium term (2-4 years) |

| Performance degradation in fog, rain, and snow | -1.9% | Northern Europe and Alpine regions | Long term (≥ 4 years) |

| Strict BVLOS drone-flight regulations | -1.4% | Europe-wide with national variations | Short term (≤ 2 years) |

| Supply-chain dependence on GaAs/SiGe laser diodes | -1.1% | All suppliers across Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High unit cost of long-range, high-resolution sensors

Premium automotive-grade LiDAR still commands list prices between EUR 3,000 and EUR 10,000 per unit, while full-waveform survey systems exceed EUR 100,000, curbing demand among cost-sensitive SMEs. European distributors confront margin compression as Chinese entrants drop prices 30-50%, forcing re-negotiations with OEMs and public agencies. To offset sticker shock, integrators now market subscription models that bundle hardware, analytics, and maintenance under multi-year SLAs. Government procurement frameworks begin to score total cost of ownership rather than capital expenditure alone, rewarding vendors that demonstrate lifecycle savings. The ability to localize manufacturing inside the EU will become a differentiator once proposed carbon-border adjustments take effect, tempering import-price advantages.

Performance degradation in fog, rain, and snow

LiDAR’s eye-safe wavelengths scatter strongly in water droplets, leading to range reductions exceeding 60% in dense fog and elevated false-positive rates during heavy snowfall. Nordic automotive test sites now include controlled mist chambers and ice tunnels to replicate these edge cases, raising validation cost for suppliers. Multi-wavelength and polarization-diverse emitters improve resilience but add BOM complexity. Software-level filtering mitigates ghost targets yet increases latency unacceptable for high-speed scenarios. Consequently, OEMs are adopting sensor-fusion stacks that down-weight LiDAR in adverse weather, limiting sole-source opportunities and tempering volume projections in the European LiDAR market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mobile Systems Drive Market Leadership

Mobile/Vehicle-Mounted units secured the largest slice of the European LiDAR market size, commanding 46.60% revenue share in 2025. Adoption accelerates as automotive OEMs integrate long-range sensors for Level 3 functionality and logistics operators equip yard tractors for autonomous marshalling. Mobile mapping vans also dominate municipal asset inventories, capturing curb condition, street furniture, and tree-canopy data in a single pass. Bathymetric/Marine LiDAR follows a steeper trajectory, advancing at a 16.6% CAGR to 2031 amid record offshore wind leasing and coastal resilience programs. Floating platforms, leveraging automotive-grade solid-state cores, cut setup costs by two-thirds and unlock measurements in previously inaccessible deep-water sites.

Continued cost convergence amplifies product-type rebalancing. As solid-state modules drop below USD 500, warehouse AGVs and construction machinery become mainstream targets, while terrestrial tripod systems transition from static documentation to periodic progress-tracking roles. Suppliers now bundle SLAM algorithms to turn backpack scanners into 3D mobile capture rigs for heritage preservation, opening a niche but recurring revenue. In aggregate, demand profiles show a clear preference for systems that can traverse complex environments, reinforcing mobile dominance in the European LiDAR market.

By Technology: Mechanical Dominance Faces Solid-State Challenge

Mechanical Scanning retained 51.20% of the European LiDAR market share in 2025, thanks to entrenched survey workflows and abundant spare parts inventories. Users appreciate known calibration routines and field-serviceable designs suited to rugged operations. However, FMCW/Hybrid and other solid-state approaches outpace at a 16.7% CAGR to 2031 as automotive validation completes and scalable packaging slashes per-unit cost. FMCW’s inherent Doppler capability delivers velocity data critical for collision-avoidance algorithms, and its interference immunity solves cross-talk issues in multi-sensor fleets.

European R&D, buoyed by the EUR 5 million CoRaLi-DAR project, seeks to leapfrog first-generation flash systems by integrating silicon photonics transmitters with MEMS beam-steerers. Parallel software innovation leverages edge AI to compress point-cloud streams, removing bandwidth bottlenecks. The tipping point is expected once automotive solid-state volumes exceed 10 million annually, triggering spill-over into construction and security domains. Consequently, the technology mix will rebalance toward solid-state architectures, although mechanical platforms will persist in ultra-long-range airborne mapping where the current solid-state range is insufficient.

By Platform: Ground Vehicles Lead Industrial Integration

Ground-vehicle installations generated 39.10% of 2025 deployments, underpinned by automotive OEM rollouts and surge demand for automated tugger trains in manufacturing. Automotive assembly plants showcase real-world use: BMW’s European factories now rely on LiDAR-guided marshalling robots that cut yard dwell time by 30%. Marine/Shipborne applications appear as the fastest riser, growing at 16.8% CAGR on the back of offshore energy and coastal-security investments. Floating LiDAR buoys, achieving 12-month autonomous endurance, enable wind developers to derisk site assessments and comply with environmental regulations.

UAV platforms maintain specialized yet growing appeal for linear-asset inspections, while handheld and backpack systems capitalize on urban-canyon mapping where GPS reception is poor. Fixed-infrastructure nodes, embedded in smart-city lamp posts, deliver continuous traffic analytics without privacy concerns. Platform diversification ensures layered demand, but ground vehicles remain the gravitational center of the European LiDAR market due to high unit volumes in both consumer and industrial fleets.

By End-use Industry: Automotive Leadership Drives Innovation

Automotive and Transportation captured 35.10% of 2025 revenue, anchoring the Europe LiDAR market share through regulatory pull and premium-segment differentiation strategies. OEM adoption cascades across tiers: suppliers qualify in-cabin driver-monitoring LiDAR and short-range flash units for automated parking. Aerospace and Defense, rising at 17.0% CAGR, benefits from UAV perimeter-security missions and terrain-following navigation packages. Military programs emphasize ITAR-free European sourcing, spurring local production incentives.

Engineering, Construction, and Surveying sustain steady purchases for progress-tracking and as-built validation, strengthened by BIM Level 3 mandates. Industrial and Logistics Automation explodes in warehouses where LiDAR-guided AMRs cut pick-cycle times and improve worker safety. Smart Cities tap curb-mounted pods for pedestrian heat-map analytics, while Environmental Monitoring deploys airborne systems for forest-inventory baselines. The resulting mosaic confirms automotive’s spill-over effect: technology validated on vehicles quickly migrates into adjacent verticals, compounding demand across the European LiDAR market.

Geography Analysis

Germany heads regional adoption with a 29.40% share in 2025, bolstered by OEM investment, precision-manufacturing expertise, and a dense ecosystem of tier-1 suppliers. Government R&D grants further subsidize perception-system trials on Autobahn testbeds, keeping the domestic procurement cycle brisk. Spain delivers the region’s fastest growth at a 17.1% CAGR to 2031, propelled by EUR 28 billion in renewable-energy and smart-mobility allocations that directly fund floating LiDAR and urban traffic-management projects. National digitalization strategies compel municipalities to adopt sensor suites that feed open data portals, accelerating public tenders for turnkey LiDAR solutions.

France and the United Kingdom maintain robust demand through aerospace and offshore wind, respectively. French spacecraft integrators collaborate with laser-source specialists to develop atmospheric LiDAR payloads for greenhouse-gas monitoring, elevating domestic content. The UK leverages Celtic-Sea leasing rounds to trial buoy-mounted sensors with ice-class survivability standards. Italy focuses on cultural-heritage scans and high-speed-rail BIM compliance, while the Netherlands pioneers curbside LiDAR deployments linked to MaaS (mobility-as-a-service) apps. Nordic nations serve as stress-laboratories for snow-resilient performance, informing firmware updates that feed back into continental fleets. Collectively, geographic diversification insulates the European LiDAR market against single-country slowdowns and fosters a continent-wide learning loop.

Regulatory Landscape

In Europe, LiDAR-enabled automotive functions operate within an increasingly harmonized EU type-approval framework anchored by the General Safety Regulation, Regulation (EU) 2019/2144. In March 2026, the European Commission adopted Commission Implementing Regulation (EU) 2026/481, amending the technical specifications for type-approval of automated driving systems in fully automated vehicles and supporting broader commercialization pathways for use cases such as automated valet parking through changes to the small-series approach.

Safety assurance is also moving beyond classical functional safety toward AI-aware processes. ISO/PAS 8800:2024 (published December 2024) provides a safety framework for AI-enabled road-vehicle systems, complementing ISO 26262 and ISO 21448, and is increasingly used as a practical compliance reference for LiDAR-centric perception stacks that depend on AI/ML. The EU approach also aligns with UN Regulations referenced in type-approval work (including UN R79 and UN 13/13-H for steering and braking in AVP contexts), which helps keep supplier validation aligned across European markets.

Value Chain Analysis

The Europe LiDAR value chain spans upstream optoelectronic components (laser sources, receivers, and semiconductor supply such as GaAs/SiGe-dependent elements), core sensor manufacturing (mechanical, solid-state, and hybrid architectures), firmware and perception software, and downstream integration into platforms such as vehicles, UAV payloads, mobile mapping rigs, and fixed infrastructure nodes. In automotive programs, Tier-1 and OEM qualification workflows also incorporate cybersecurity and safety evidence requirements, shaping design-for-compliance decisions and test spend. Public-space deployments for smart-city and infrastructure use cases add GDPR-driven data-handling constraints, which tends to favor privacy-preserving point-cloud analytics.

Distribution and system integration remain material in Europe, with authorized partners and regional distributors shortening lead times and providing application support for surveying, autonomy, and industrial automation deployments. Examples include European distribution moves tied to Hesai sensors, such as Visimind AB becoming an official distributor in April 2025 and France-based CADDEN formalizing authorized partner status in April 2025. Industry efforts to improve data interoperability, including the federated European Point Cloud Portal hosted by Delft University of Technology, also affect procurement and the attachment of recurring software and services through standards-adjacent work.

Competitive Landscape

European incumbents such as Leica Geosystems, Hexagon, and RIEGL lead in surveying and mapping niches through product breadth, services, and decades-long client relationships. Their portfolios now span single-photon airborne sensors capable of 14 million measurements per second, delivering country-wide coverage in record time. Meanwhile, Chinese entrants like Hesai secure major automotive contracts, leveraging cost leadership and rapid iteration cycles to penetrate OEM supply chains. Partnerships Mercedes-Benz with Hesai, Stellantis with Innoviz, illustrate buyer openness to global sourcing and amplify price pressure across the European LiDAR market.

Start-ups focus on solid-state innovation and perception software. Scantinel and Blickfeld chase FMCW commercialization, while Outsight bundles edge analytics for real-time object classification. Consolidation accelerates: Hexagon’s 2024 acquisition of a Canadian point-cloud AI firm underscores the shift toward end-to-end platforms. Vendors now differentiate on lifecycle value offering calibration-as-a-service, AI-driven mapping portals, and carbon-footprint dashboards. The twin forces of automotive volume and software-centric business models are set to reorder market-share rankings by 2030, although surveying incumbents retain defensive moats in regulatory certification and global support networks.

Europe LiDAR Industry Leaders

Leica Geosystems AG

Hexagon AB

RIEGL Laser Measurement Systems GmbH

Topcon Corporation

Trimble Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term commercial whitespace is forming around EU-wide type-approval clarity for higher automation features and the resulting demand for compliant perception stacks. Commission Implementing Regulation (EU) 2026/481 (adopted March 2026) tightens the linkage between automated driving approvals and demonstrable safety performance, reinforcing demand for LiDAR hardware paired with validated perception software, scenario libraries, and traceable verification artifacts. This supports opportunities for suppliers that package sensors with cloud-connected workflows and compliance-ready toolchains, rather than selling standalone units.

Another opportunity is scaling automotive-grade solid-state supply into adjacent verticals that already buy LiDAR but face budget and deployment-cycle constraints, including smart-city traffic analytics, infrastructure digital twins, and rail and corridor monitoring. Evidence of demand pull includes named OEM programs integrating LiDAR platforms (BMW Neue Klasse with InnovizTwo, Mercedes-Benz S-Class with Luminar Iris/Halo, and continued use of Valeo Scala) and the way component allocation pressure is spreading across sensing categories. As driver-monitoring and automated safety mandates phase in (including the July 2026 mandatory application of advanced driver distraction warning systems for new vehicle registrations under Delegated Regulation (EU) 2023/2590), Tier-1s and OEMs have incentives to secure multi-year component sourcing and to standardize software-defined perception architectures, creating room for European integrators and component suppliers that can meet automotive qualification and volume logistics.

Recent Industry Developments

- June 2026: Leica Geosystems launched the Leica RTC series terrestrial laser scanners (RTC300, RTC500, RTC700) with integrated real-time data streaming and connected workflows via Hexagon GeoCloud and Livelink. The release strengthens end-to-end delivery from capture to collaboration, supporting faster turnaround for construction, plant, and infrastructure scanning projects where clients increasingly require continuous data access rather than periodic file handoffs.

- May 2026: Vossloh made a firm offer to acquire UK-based LiDAR specialist Cordel Group for GBP 29 million to expand rail infrastructure monitoring capabilities using AI-enabled, train-mounted LiDAR. The move signals consolidation in rail inspection toolchains and accelerates the pairing of LiDAR capture with analytics for predictive maintenance in European rail networks.

- May 2025: Leica Geosystems introduced the Leica Pegasus TRK300 mobile mapping system, extending mobile LiDAR capture to a 300-meter range for asset mapping use cases. This broadened the addressable user base for vehicle-mounted mapping workflows in smart-city and transportation asset inventories, supporting higher-frequency corridor refresh cycles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Europe LiDAR market covers revenue generated from LiDAR hardware and related enabling software that is sold into European end users for sensing, mapping, and object detection across commercial and public applications.

Scope exclusions: We exclude non-LiDAR sensing alternatives (such as radar-only and camera-only systems) and general surveying services where LiDAR is not the primary value driver.

Segmentation Overview

- By Product Type

- Aerial LiDAR

- Mobile/Vehicle-Mounted LiDAR

- Terrestrial (Tripod) LiDAR

- Bathymetric/Marine LiDAR

- By Technology

- Mechanical Scanning

- Solid-State MEMS

- Solid-State Flash/OPA

- FMCW/Hybrid

- By Platform

- UAV/Drone

- Ground Vehicle

- Handheld/Backpack

- Fixed Infrastructure

- Marine/Shipborne

- By End-use Industry

- Automotive and Transportation

- Engineering, Construction and Surveying

- Industrial and Logistics Automation

- Aerospace and Defense

- Environmental Monitoring and Agriculture

- Smart Cities and Infrastructure

- Other End-use Industries

- By Country

- United Kingdom

- Germany

- France

- Spain

- Italy

- Netherlands

- Belgium

- Switzerland

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research supported the demand picture and helped keep the market boundary aligned to what buyers in Europe actually procure. We relied on public sources such as Eurostat datasets, national transport and road safety publications, aviation and geospatial authority portals, and peer-reviewed remote sensing journals to ground the discussion on deployments and use cases.

We also reviewed company annual reports, investor presentations, product brochures, and credible press coverage to track launch timelines and pricing direction, which then informed our assumptions. Where needed, we used paid subscriptions for company financials and intelligence, plus patent databases to verify technology direction and filing activity around solid-state designs and scanning approaches. The sources listed here are illustrative, and many other public references were used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work was used to stress-test inputs that are hard to observe from public data, especially adoption pace in automotive programs, construction and surveying budgets, and airborne and terrestrial project pipelines. We spoke with a mix of manufacturers, integrators, distributors, and end-user teams across key European countries so assumptions on volumes, average selling prices, and attach rates could be corrected before finalizing the totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | |

| Mid tier: 54% | Functional/Unit leaders: 40% | |

| Smaller Players: 15% | Managers: 46% |

Market-Sizing & Forecasting

The core market build uses a top-down and bottom-up approach. European demand is reconstructed from application-level adoption in automotive sensing, construction and surveying activity, and airborne mapping programs, then reconciled with supplier-side reality checks. To keep it reproducible, we start from measurable indicators and apply penetration and spend logic by use case, followed by country rollups to arrive at the regional total.

Key inputs tracked included vehicle safety and ADAS rollout timing (including rating and regulatory changes), the share of projects specifying LiDAR in surveying and corridor mapping, offshore wind measurement activity where floating LiDAR is used, typical unit pricing movement for solid-state versus mechanical designs, and the mix shift between airborne and terrestrial deployments. Forecasts use scenario analysis supported by a simple multivariate regression on leading indicators, with adoption and pricing paths adjusted based on primary feedback. When bottom-up coverage is incomplete for smaller deployments, we handle gaps through conservative channel checks and sampled ASP times volume ranges, then use those ranges to tune the final totals.

Data Validation & Update Cycle

Outputs are checked against independent signals, such as public procurement activity, technology adoption milestones, and shipment and pricing direction implied by company commentary, and any variance is investigated before sign-off. If a number looks out of line, we reopen the assumptions behind volumes, pricing, and country mix, then re-contact selected respondents to confirm whether the change is real or model-driven.

A multi-step internal review is followed so the final tables and narrative stay consistent. Reports are refreshed annually, with interim updates when major events occur that can shift demand, supply availability, or pricing. Before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Europe Lidar Market Size Versus Other Published Estimates

Published values for Europe LiDAR do not always match because each study selects its own base year and revenue boundary, then applies different adoption and pricing assumptions. Differences also show up when some models lean heavily on early automotive ramps or bundle in broader mapping and service revenue.

By tracking country rollups, checking platform-level adoption in automotive and mapping, and refreshing average selling price assumptions for solid-state and mechanical units, Mordor Intelligence keeps the market total tied to observable deployments and repeatable inputs rather than broad technology spending proxies. The biggest gap drivers tend to be whether service and integration revenue is included, how airborne mapping programs are annualized, and how currency timing is handled when values are converted into USD.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.17 B (2026) | |

| Industry Publisher A | USD 1.04 B (2025) | Uses a different base year and a longer forecast window, and its scope is structured around installation types and components, which can pull in more enabling systems around LiDAR deployments. |

| Research Publisher B | USD 0.73 B (2024) | Starts from a lower base year and segments heavily by LiDAR type and broad applications, which can undercount fast-ramping automotive programs if timing assumptions are conservative. |

Overall, the spread is mostly explained by base-year choice and what is counted inside the revenue definition, especially services, integration, and non-core enabling components. We keep the calculation steps transparent, so a reader can trace totals back to adoption indicators, pricing logic, and country-level additions.

Key Questions Answered in the Report

What is the current value of the Europe LiDAR market?

The market is valued at USD 1.17 billion in 2026 and is forecast to double by 2031.

Which product category leads sales in Europe?

Mobile/Vehicle-Mounted systems hold 46.60% of 2025 revenue due to widespread automotive and logistics use.

What CAGR is projected for marine LiDAR in Europe?

Bathymetric and marine deployments are expected to grow at a 16.6% CAGR through 2031.

Which country is the largest adopter of LiDAR in Europe?

Germany commands 29.40% share, anchored by its automotive OEM base and industrial automation focus.

How are solid-state sensors affecting prices?

Automotive-scale volumes are set to lower solid-state LiDAR prices by as much as 70% before 2030, broadening industrial uptake.

What regulatory change is accelerating automotive LiDAR demand?

Euro-NCAP’s 2026 sensor-based safety ratings effectively make LiDAR mandatory for five-star vehicle scores.

Page last updated on: