Europe Insulin Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

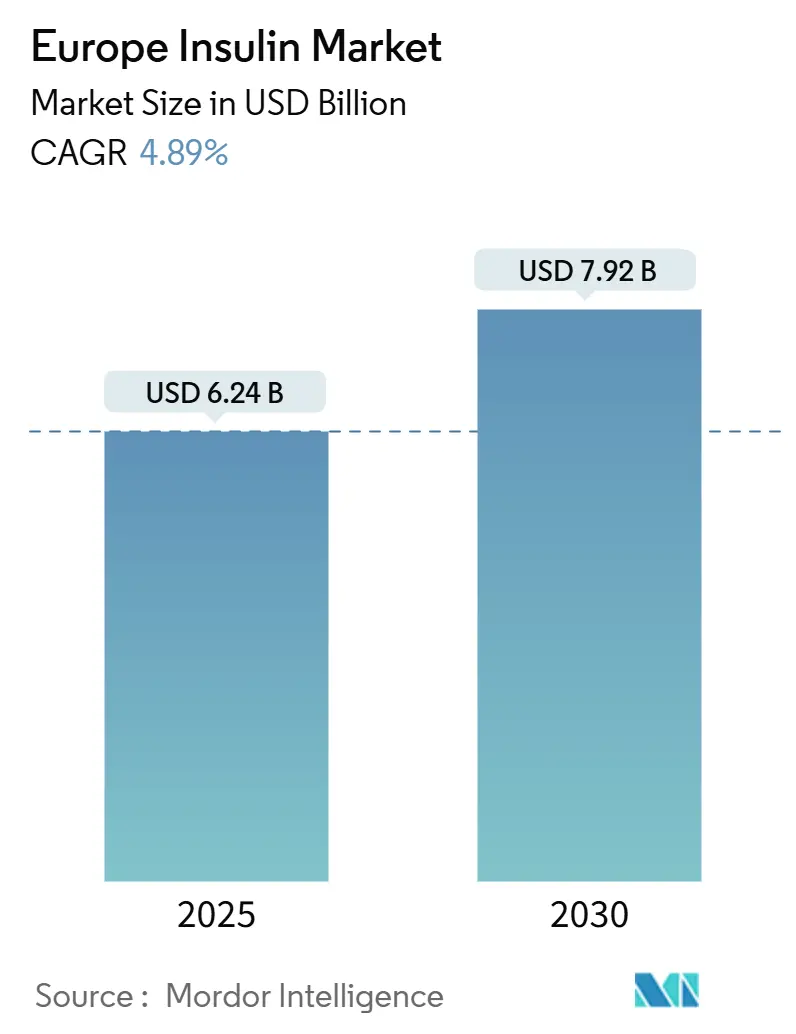

| Market Size (2025) | USD 6.24 Billion |

| Market Size (2030) | USD 7.92 Billion |

| Growth Rate (2025 - 2030) | 4.89% CAGR |

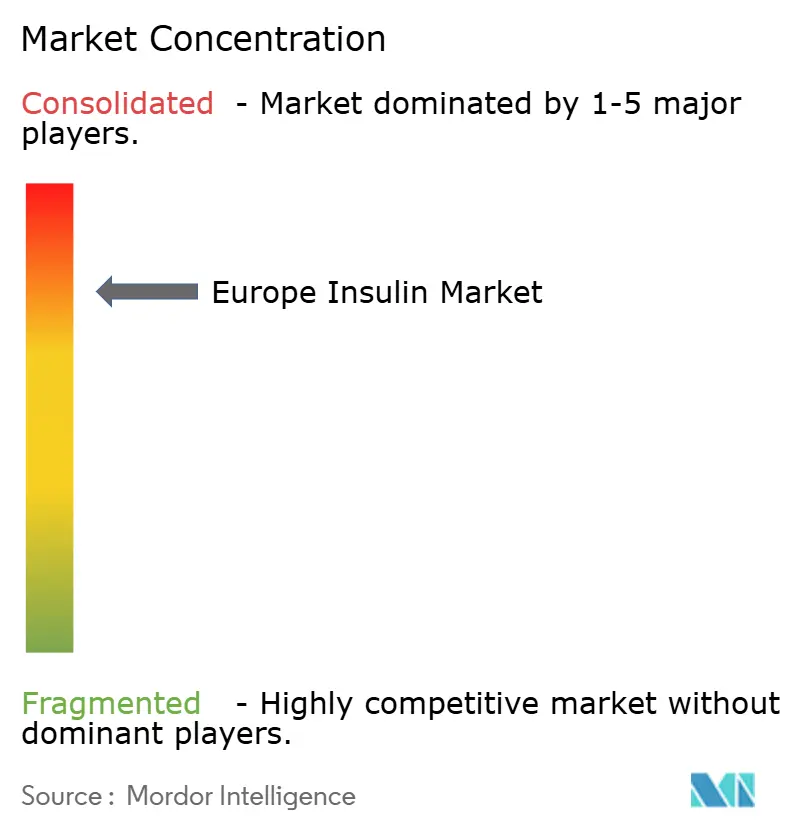

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Insulin Market Analysis by Mordor Intelligence

The Europe Insulin Market size is estimated at USD 6.24 billion in 2025, and is expected to reach USD 7.92 billion by 2030, at a CAGR of 4.89% during the forecast period (2025-2030).

Diabetes is a condition that is more commonly found among older individuals. In Europe countries, there are approximately 25 million people between the ages of 60 and 79 who have diabetes. While middle-aged men (between 40 and 59 years old) tend to have a higher prevalence of diabetes compared to women, the number of women with diabetes increases significantly after the age of 70. This can be attributed to the fact that women generally have a longer life expectancy.

In 2023, the average prevalence of diabetes among adults in EU countries was 7.5%, taking into account diagnosed cases and age-standardization. However, the rates varied across different countries. Cyprus, Portugal, and Germany had rates of 9% or higher, while Ireland and Lithuania had rates of less than 4%.

It is worth noting that the prevalence of diabetes seems to have reached a stable point in many European countries in recent years, particularly in Nordic countries. However, there has been a slight increase in diabetes rates in Southern European countries as well as Central and Eastern European countries. These upward trends can be attributed, at least in part, to the rise in obesity and physical inactivity, and how these factors interact with the aging population.

The European countries are suffering from the burden of high diabetes expenditure due to its rising prevalence. Approximately 10% of the total diabetes population is having type-1 diabetes and approximately out of this 10% of people only 80-90% use Insulin but the usage of insulin is rising from time to time, even type-2 diabetes patients are using the insulin drugs during COVID-19. Technological advancements have increased over the period in Insulin drugs.

Therefore, owing to the aforementioned factors the studied market is anticipated to witness growth over the analysis period.

Europe Insulin Market Trends and Insights

Increasing diabetes prevalence in Europe is Driving the Insulin Market

The European region has witnessed an alarming increase in the prevalence of diabetes in recent years. Patients with diabetes require many corrections throughout the day to maintain normal blood glucose levels, such as oral anti-diabetic medication or the ingestion of additional carbohydrates, by monitoring their blood glucose levels.

The rate of newly diagnosed type-1 and type-2 diabetes cases is seen to increase, mainly due to obesity, an unhealthy diet, and physical inactivity. The rapidly increasing incidence and prevalence of diabetic patients and healthcare expenditure are indications of the increasing usage of diabetic drugs.

According to the IDF, the overall diabetes expenditure in Europe among the population aged 20-79 years was USD 156 billion, and it is expected to increase to USD 174 billion by 2040. According to other statistics from the IDF, every year 21,600 children are added to the type-1 diabetic population pool. These figures indicate that approximately 9% of the total healthcare expenditure is spent on diabetes in Europe.

Germany is expected to register a healthy growth rate in the European Europe Insulin Market

Diabetes is a significant health problem and one of the astounding challenges facing healthcare systems all over Germany. The prevalence of known type-1 and type-2 diabetes in the German adult population is very high, along with a high number of patients who are not yet diagnosed with the disease. Due to an aging population and an unhealthy lifestyle, the prevalence of type-2 diabetes is expected to increase steadily over the next few years. High-quality care, including adequate monitoring, control of risk factors, and active self-management, are the key factors for preventing complications in German patients with type-2 diabetes.

The growing incidence, prevalence, and progressive nature of the disease have encouraged the development of new drugs to provide additional treatment options for diabetic patients. According to the German Diabetes Center (DDZ), at least 7.2% of the population in Germany currently lives with diabetes, which will increase significantly over the next two decades. German law requires public plans to cap out-of-pocket health care costs and to cover all medically necessary treatment, including insulin.

Germany is one of the most developed countries in terms of healthcare facilities. Moreover, the reimbursement policy and the pricing policy are highly regulated, which drives the market. The roll-out of many new products, increasing international research collaborations in technological advancement, and increasing awareness about diabetes among the public are some of the market opportunities for the players in the German insulin drug market.

Competitive Landscape

The European insulin drug market is highly consolidated in nature due to the presence of only a few major companies operating globally as well as regionally. Mergers and acquisitions between players in the recent past have helped companies strengthen their market presence. Eli Lilly and Boehringer Ingelheim have an alliance to develop and commercialize Abasaglar (Insulin Glargine).

Europe Insulin Industry Leaders

Novo Nordisk

Sanofi

Eli Lilly

AstraZeneca

Biocon

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: Medtronic has obtained European approval to integrate its most recent automated insulin pump with its latest glucose sensor for the first time. The CE mark includes the MiniMed 780G pump and the Simplera Sync system, which is characterized by the medtech company as a disposable, all-in-one blood sugar sensor that can be inserted under the skin in less than 10 seconds without the need for fingersticks.

- October 2022: Novo Nordisk announced headline results from the ONWARDS 5 phase 3a trial with once-weekly insulin icodec in people with type 2 diabetes. The ONWARDS 5 trial was a 52-week, open-label efficacy and safety treat-to-target trial investigating once-weekly insulin versus once-daily basal insulin (insulin degludec or insulin glargine U100/U300).

Europe Insulin Market Report Scope

Human insulin is used to control blood sugar in people with type-1 diabetes, a condition in which the body cannot produce insulin and cannot, therefore, control the amount of sugar in the blood, or type-2 diabetes, a condition in which the blood sugar is too high because the body cannot produce or use insulin normally and which cannot be controlled by oral medications alone. The European insulin Market is segmented into type and geography. The report offers the value (in USD) and volume (in units) for the above segments.

| Basal or Long-acting Insulins | Lantus (Insulin Glargine) |

| Levemir (Insulin Detemir) | |

| Toujeo (Insulin Glargine) | |

| Tresiba (Insulin Degludec) | |

| Abasaglar (Insulin Glargine) | |

| Bolus or Fast-acting Insulins | NovoRapid\Novolog (Insulin Aspart) |

| Humalog (Insulin Lispro) | |

| Apidra (Insulin Glulisine) | |

| FIASP (Insulin Aspart) | |

| Admelog (Insulin Lispro) | |

| Traditional Human Insulins | Novolin\Actrapid\Insulatard |

| Humilin | |

| Insuman | |

| Insulin Combinations | NovoMix (Biphasic Insulin Aspart) |

| Ryzodeg (Insulin Degludec and Insulin Aspart) | |

| Xultophy (Insulin Degludec and Liraglutide) | |

| Soliqua/Suliqua (Insulin Glargine and Lixisenatide) | |

| Biosimilar Insulins | Insulin Glargine Biosimilars |

| Human Insulin Biosimilars |

| United Kingdom |

| Germany |

| France |

| Russia |

| Spain |

| Italy |

| Rest of Europe |

| Insulin | Basal or Long-acting Insulins | Lantus (Insulin Glargine) |

| Levemir (Insulin Detemir) | ||

| Toujeo (Insulin Glargine) | ||

| Tresiba (Insulin Degludec) | ||

| Abasaglar (Insulin Glargine) | ||

| Bolus or Fast-acting Insulins | NovoRapid\Novolog (Insulin Aspart) | |

| Humalog (Insulin Lispro) | ||

| Apidra (Insulin Glulisine) | ||

| FIASP (Insulin Aspart) | ||

| Admelog (Insulin Lispro) | ||

| Traditional Human Insulins | Novolin\Actrapid\Insulatard | |

| Humilin | ||

| Insuman | ||

| Insulin Combinations | NovoMix (Biphasic Insulin Aspart) | |

| Ryzodeg (Insulin Degludec and Insulin Aspart) | ||

| Xultophy (Insulin Degludec and Liraglutide) | ||

| Soliqua/Suliqua (Insulin Glargine and Lixisenatide) | ||

| Biosimilar Insulins | Insulin Glargine Biosimilars | |

| Human Insulin Biosimilars | ||

| Geography | United Kingdom | |

| Germany | ||

| France | ||

| Russia | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How big is the Europe Insulin Market?

The Europe Insulin Market size is expected to reach USD 6.24 billion in 2025 and grow at a CAGR of 4.89% to reach USD 7.92 billion by 2030.

What is the current Europe Insulin Market size?

In 2025, the Europe Insulin Market size is expected to reach USD 6.24 billion.

Who are the key players in Europe Insulin Market?

Novo Nordisk, Sanofi, Eli Lilly, AstraZeneca and Biocon are the major companies operating in the Europe Insulin Market.

What years does this Europe Insulin Market cover, and what was the market size in 2024?

In 2024, the Europe Insulin Market size was estimated at USD 5.93 billion. The report covers the Europe Insulin Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe Insulin Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: