Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

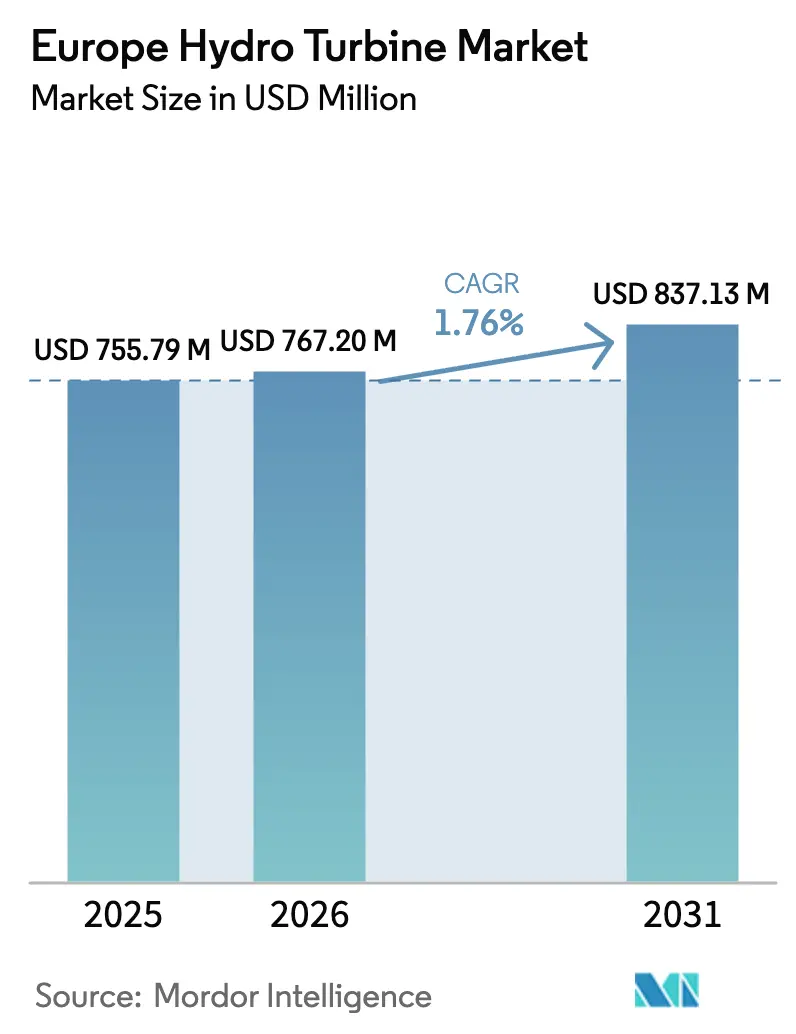

| Base Year Market Size (2025) | USD 755.79 Million |

| Market Size (2026) | USD 767.20 Million |

| Market Size (2031) | USD 837.13 Million |

| Growth Rate (2026 - 2031) | 1.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Hydro Turbine Market Analysis by Mordor Intelligence

The Europe Hydro Turbine Market size was valued at USD 755.79 million in 2025 and is estimated to grow from USD 767.20 million in 2026 to reach USD 837.13 million by 2031, at a CAGR of 1.76% during the forecast period (2026-2031).

A shift from greenfield dams to life-extension programs is underpinning this muted headline growth, as asset owners prioritize refurbishment that delivers faster returns and fewer licensing hurdles. Pumped-storage now represents roughly 90% of the continent’s installed energy-storage capacity, and its ability to provide multi-hour discharge is reinforcing demand for high-head reaction units.[1]European Commission, “REPowerEU: Affordable, Secure and Sustainable Energy for Europe,” energy.ec.europa.eu Record-high carbon prices under the EU Emissions Trading System, combined with thermal plant closures, are further tilting capital toward low-carbon, dispatchable hydro assets.[2]Bloomberg, “EU Carbon Prices Hit Record Highs in 2024,” bloomberg.com Meanwhile, modular small-hydro packages and fish-friendly runners are unlocking previously stranded run-of-river sites, diversifying the project pipeline even as greenfield reservoir construction wanes. Competitive intensity remains pronounced because predictive-maintenance platforms and variable-speed retrofits can lift plant availability by up to 30%, creating recurring service revenue that incumbents are eager to defend.[3]Andritz AG, “Annual Report 2024,” andritz.com

Key Report Takeaways

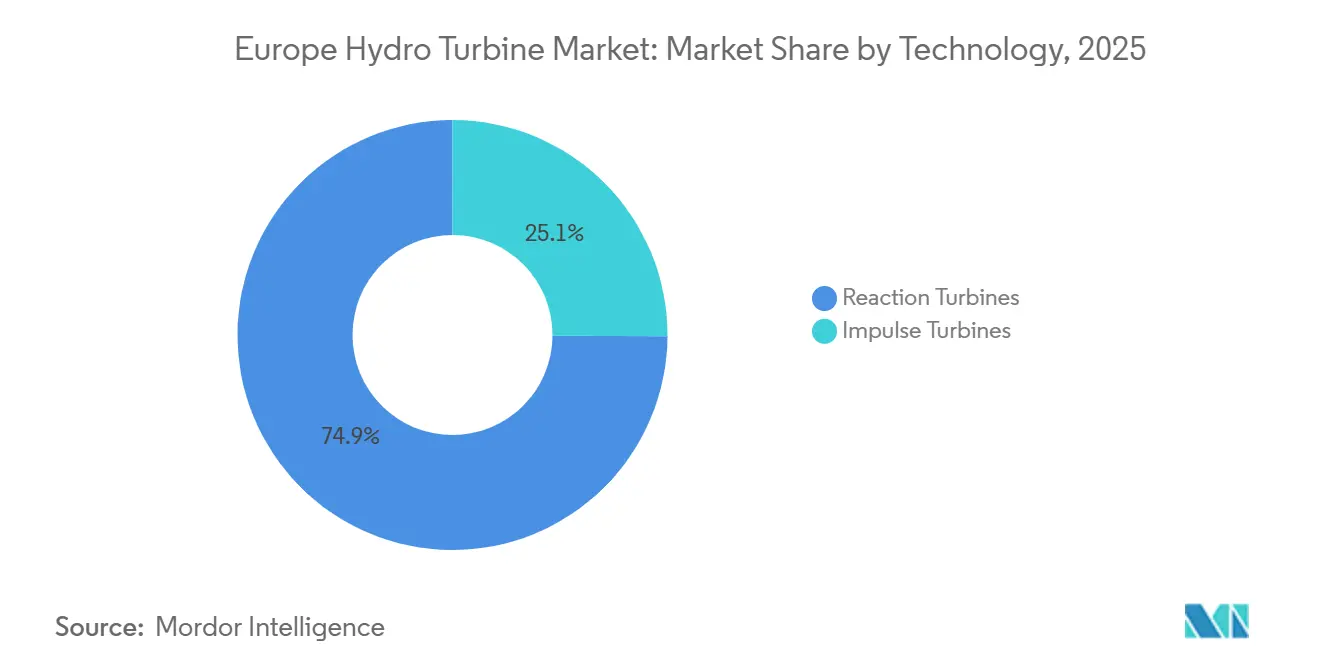

- By technology, reaction turbines commanded 74.9% of the European hydro turbine market share in 2025, while impulse units are the fastest-growing sub-segment at a 2.10% CAGR through 2031.

- By capacity, large installations above 100 MW delivered 50.1% of 2025 revenue, yet small and micro projects below 10 MW are forecast to expand at a 3.33% CAGR, the quickest pace in the segment.

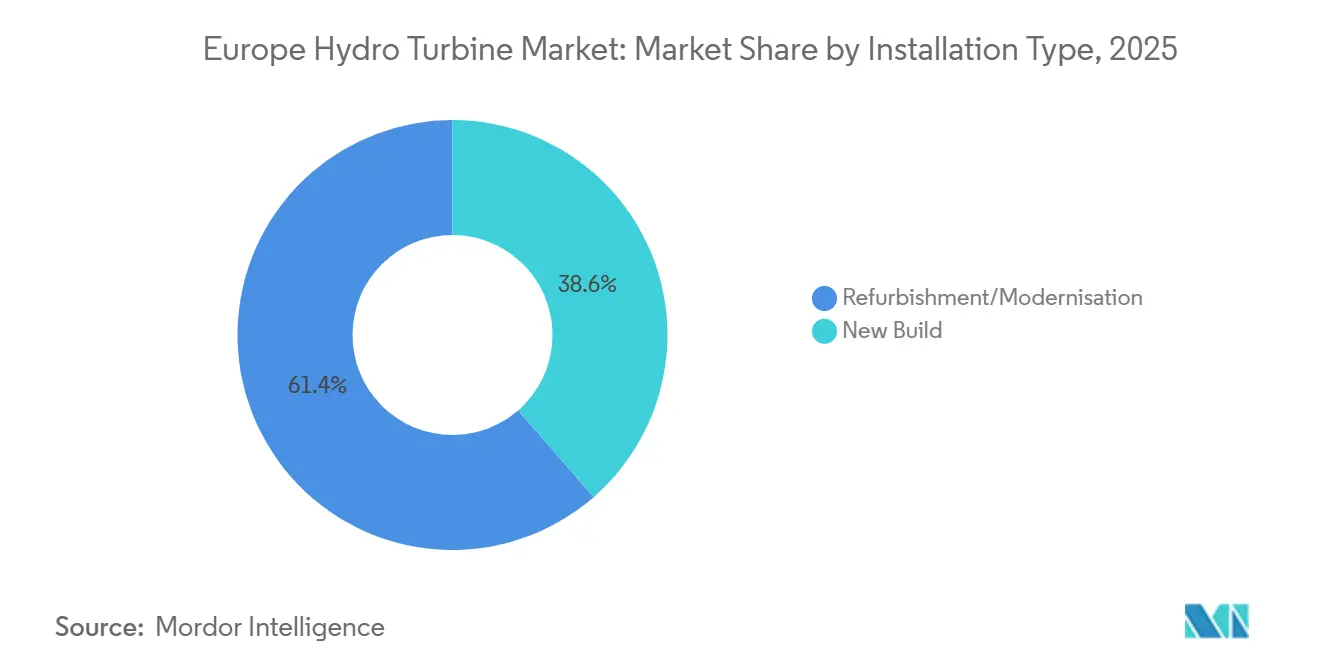

- By installation type, refurbishment captured 61.4% of market value in 2025 and is projected to grow at 2.15% annually, outstripping new-build activity.

- By component, generators led with a 35.5% share of the European hydro turbine market size in 2025 and remain the top growth category at a 2.06% CAGR thanks to widespread variable-speed upgrades.

- By geography, the United Kingdom is set to be the fastest-expanding national market at a 3.78% CAGR to 2031, propelled by Cap-and-Floor revenue guarantees for long-duration storage.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Hydro Turbine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Green Deal targets accelerating refurbishment & greenfield capacity | +0.4% | EU-27, UK, Norway, Switzerland | Medium term (2-4 years) |

| Retirement of thermal plants creating demand for pumped-storage stability | +0.3% | Germany, UK, Poland, Spain, Italy | Short term (≤ 2 years) |

| Carbon pricing & green finance improving hydro ROI | +0.3% | EU-27 (ETS coverage), UK (carbon price floor) | Long term (≥ 4 years) |

| Fish-friendly turbine designs easing biodiversity approvals | +0.2% | Alpine regions (Austria, Switzerland), Nordics (Sweden, Norway) | Medium term (2-4 years) |

| Digital-twin O&M lowering OPEX for small utilities | +0.2% | Germany, France, NORDIC countries, Rest of Europe | Medium term (2-4 years) |

| Corporate renewable PPAs from data-center operators | +0.1% | NORDIC countries (Norway, Sweden), UK, Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Green Deal Targets Accelerating Refurbishment & Greenfield Capacity

The REPowerEU plan, updated in 2024, mandates 42.5% renewable energy in final consumption by 2030 and explicitly highlights hydropower for flexibility services.[4]European Commission, “REPowerEU: Affordable, Secure and Sustainable Energy for Europe,” energy.ec.europa.eu Grid-infrastructure spending of EUR 584 billion through 2030 is channeling funds toward pumped-storage interconnections and turbine replacements that strengthen frequency response. Refurbishment enjoys preferential treatment under the EU Taxonomy, provided projects meet ecological-flow standards. Greece’s 680 MW Amfilochia scheme, approved in 2024, and Austria’s 150 MW Ebensee modernization showcase how recovery funds are fast-tracking lifecycle extensions. Variable-speed upgrades at Ebensee now deliver full-load-to-reserve transitions in under 90 seconds, a service currently priced at EUR 15 to EUR 20 per MWh in ancillary-service auctions. As these policy levers mature, the European hydro turbine market will see a sustained flow of refurbishment contracts across core EU economies.

Retirement of Thermal Plants Creating Demand for Pumped-Storage Stability

Coal and nuclear shutdowns removed 12 GW of synchronous capacity across Germany, the UK, Belgium, and Spain between 2024 and 2025. Pumped-storage hydropower, with 46 GW already installed, is the only proven technology capable of delivering multi-hour discharge without cycle-life degradation. The UK’s 600 MW Cruachan 2 and Spain’s 200 MW Salto de Chira schemes underscore renewed investor appetite. Portugal’s 1,158 MW Tâmega complex, commissioned in 2024, already provides 40% of national balancing reserves. As utilities chase grid-stability revenue, the European hydro turbine market gains a dependable growth avenue anchored in long-duration storage.

Carbon Pricing & Green Finance Improving Hydro ROI

EU ETS allowance prices averaged EUR 85 per tonne CO₂ in 2024, lifting the internal rate of return for zero-carbon dispatchable assets. The European Investment Bank now offers concessional loans at 100 basis points below market rates for hydro projects that meet enhanced fish-passage and sediment-continuity criteria. Slovakia’s EUR 120 million Čierny Váh retrofit, financed under this framework, doubles ancillary-service revenue by enabling bidirectional frequency regulation. Green bonds worth EUR 2.3 billion printed in 2024 were three times oversubscribed, signaling institutional confidence in the European hydro turbine market.

Fish-Friendly Turbine Designs Easing Biodiversity Approvals

The Alden turbine, Minimum Gap Runner blades, and Voith’s StreamDiver system are cutting fish mortality to below 5% at Alpine and Nordic sites. Horizon 2020’s FIThydro project published design guidelines in 2024 that are now written into permits across France and Sweden. Modular powerhouse designs eliminate extensive civil works, trimming construction schedules from 36 months to 18 months while meeting Water Framework Directive standards. These advances reduce litigation risk, accelerating project timelines and supporting steady expansion of the European hydro turbine market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy Environmental Impact Assessments (EIA) and permitting | -0.3% | Alpine regions (Austria, Switzerland, Italy), Nordics (Norway, Sweden) | Long term (≥ 4 years) |

| Price competitiveness of utility-scale solar + battery storage | -0.2% | Southern Europe (Spain, Italy, Greece), France | Short term (≤ 2 years) |

| Litigation against Alpine dam expansions | -0.2% | Alpine regions (Austria, Switzerland, Italy), France (Pyrenees) | Long term (≥ 4 years) |

| Specialty-steel supply shocks raising CAPEX volatility | -0.2% | EU-27, UK (affecting turbine manufacturing and project economics) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lengthy Environmental Impact Assessments and Permitting

Full EIAs for greenfield dams can stretch five to seven years, especially where projects intersect Natura 2000 zones or trigger Espoo Convention consultations. Austria’s proposed 900 MW Kühtai expansion has been in litigation since 2021, illustrating how biodiversity challenges stall investments. Switzerland’s revised Water Protection Act now demands net-positive biodiversity outcomes, steering funds toward refurbishments that qualify for expedited 18- to 24-month reviews. Although refurbishment enjoys shorter timelines, public consultations on downstream flow regimes can still delay schedules.

Price Competitiveness of Utility-Scale Solar + Battery Storage

Southern European auctions in 2024 awarded 3.3 GW of solar-plus-storage at EUR 0.047 per kWh, undercutting pumped-storage bids by up to 20%. Combined LCOE for solar with 4-hour lithium-ion batteries now stands at USD 0.07 to USD 0.11 per kWh, edging close to refurbished hydro's USD 0.08 average. Batteries remain less durable, losing up to 30% capacity after 5,000 cycles, and cannot deliver black-start capability, yet their lower upfront costs are attracting merchant investors. For short-duration peak shaving, this price arbitrage is eroding hydro's share of ancillary revenues in Spain, Italy, and Greece. While grid-operator studies in France still prescribe 5 GW of new pumped storage for 6-hour or longer discharge windows, near-term price pressure hinders the market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Reaction Units Maintain Leadership Amid Impulse Revival

Reaction designs accounted for 74.9% of the European hydro turbine market in 2025, supported by variable-speed generators that unlock higher ancillary revenue. This segment is projected to expand at a 1.99% CAGR, assuring a stable anchor for the European hydro turbine market size through 2031. Impulse turbines, led by Pelton wheels in high-head Alpine projects, are regaining momentum as melting-glacier inflows shift seasonal profiles. Suppliers report that 30% of 2024–2025 Francis orders already include full-converter drives, a sharp rise from 10% in 2020, underlining how digital upgrades are redefining performance baselines.

Variable-speed controls allow operators to fine-tune efficiency across fluctuating heads, double participation in frequency-response markets, and extend maintenance intervals. Kaplan variants now integrate fish-friendly blades that reduce blade-strike mortality below 5%, easing Natura 2000 compliance. Turgo turbines are penetrating sub-5 MW community projects where their compact footprint and sediment tolerance offer economic advantages. As grid operators valorize rapid ramping and inertia services, reaction technology remains the backbone of the European hydro turbine market, yet niche impulse units will outpace average growth from a smaller base.

By Capacity: Micro and Small Hydro Drive Incremental Growth

Installations above 100 MW retained 50.1% of 2025 revenue, but sub-10 MW assets are forecast to expand at a 3.33% CAGR, outpacing legacy giants by nearly two-to-one. Revised EU rules waive full EIAs for projects below 10 MW, slashing soft costs and accelerating build cycles. Community cooperatives in Germany, Austria, and Switzerland raised EUR 180 million between 2024 and 2025 to back run-of-river ventures that repay in under 12 years, a trend that anchors the grassroots tier of the European hydro turbine market.

Modular turbine–generator skids now ship factory-tested, reducing on-site works from 18 months to 6 months and de-risking loans. Medium facilities from 10 MW to 100 MW are thriving on refurbishment contracts that pair existing dams with lower-reservoir additions for hybrid storage. Large projects such as Scotland’s 1,500 MW Coire Glas remain rare but critical, adding 30 GWh of storage to smooth offshore-wind swings. In aggregate, scale diversity ensures the European hydro turbine market continues growing even as prime large-dam sites vanish.

By Installation Type: Refurbishment Commands Capital Allocation

Refurbishment captured 61.4% of the European hydro turbine market value in 2025 and is set to grow 2.15% annually, reflecting the fleet’s average age of more than 45 years. Typical modernization lifts turbine efficiency by 10% to 20%, translating to extra revenue of up to EUR 3 million per 50 MW plant at current wholesale prices. License renewals now bundle ecological-flow releases and fish-passage retrofits, effectively aligning regulatory compliance with performance upgrades.

New-build activity concentrates on pumped-storage, where contractual frameworks guarantee earnings; the UK’s Cap-and-Floor regime is a model. Refurbishments exploit existing grid links and avoid the EUR 50 million-plus connection fees common to greenfield sites. Digital twins from Andritz, Voith, and GE Vernova extend overhaul intervals to eight years and enhance availability to 95%, further weighting budgets toward modernization. This dynamic will keep refurbishment the dominant revenue pillar within the European hydro turbine market through 2031.

By Component: Generators Lead the Digital Pivot

Generators represented 35.5% of 2025 spend and are poised for 2.06% annual growth, propelled by full-converter variable-speed systems that decouple mechanical speed from grid frequency. Runner and blade assemblies are next in line, benefitting from additive manufacturing that cuts lead time by two-thirds and enables site-specific hydraulic profiles. Draft-tube optimization through computational fluid dynamics is extending component life by up to 30%, lowering lifetime ownership cost.

Control and digital systems, although smaller in value, exhibit the steepest growth curve, as utilities invest in AI-driven predictive maintenance that slashes unplanned outages by 30%. The “Others” basket, valves, seals, and auxiliaries see incremental material science gains that enhance corrosion resistance. Collectively, component innovation supports the long-term competitiveness of the European hydro turbine industry while enriching service revenue streams for OEMs.

Geography Analysis

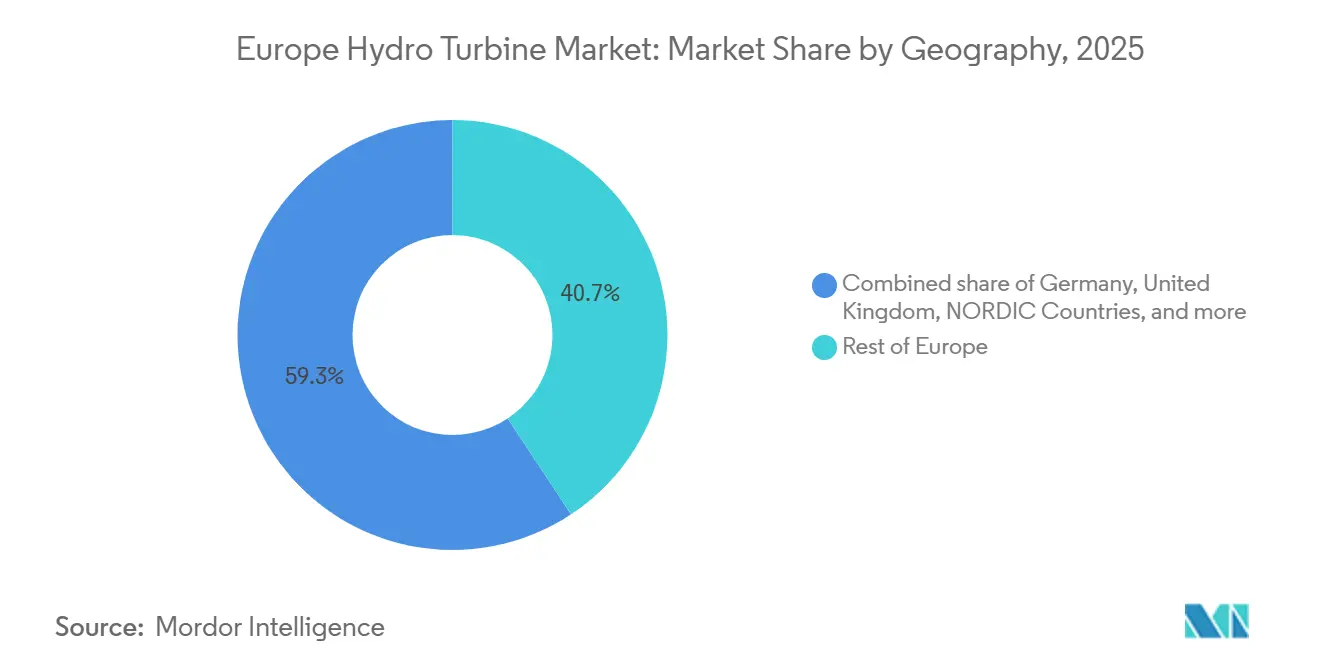

The Rest of Europe bloc, spanning Eastern Europe, the Balkans, and smaller Alpine states, held 40.7% of 2025 revenue, reflecting EU cohesion funds that prioritize hydro during coal phase-outs. Poland, Romania, and the Czech Republic secured EUR 300 million in concessional financing for turbine upgrades between 2024 and 2025, and Albania plus North Macedonia closed 120 MW of small-hydro deals backed by IFC guarantees. Switzerland’s mature fleet is adding pumped-storage capacity, such as the 900 MW Nant de Drance project, leveraging cross-border price spreads with Italy and France.

The United Kingdom is the fastest-growing national segment, expanding at 3.78% CAGR through 2031 as Cruachan 2 and Coire Glas move toward construction. Long-duration storage contracts under the Cap-and-Floor mechanism ensure bankability, while Scotland’s steep topography offers unrivaled high-head sites near offshore-wind hubs. Germany, France, and Italy together command roughly 25% of the European hydro turbine market; their focus remains squarely on digital upgrades that boost flexibility without new impoundments. Germany alone invested EUR 400 million in turbine and control-system retrofits in 2024–2025.

Spain and the Nordic countries reflect divergent fortunes. Spanish reservoirs fell to 40% capacity in 2024, pressuring output, yet the 200 MW Salto de Chira project on Gran Canaria highlights hydro’s role for island grids. Norway and Sweden, with 30 GW installed, are co-funding EUR 150 million in grid-integration upgrades to enhance cross-border balancing. Russia, outside the EU, maintains a substantial hydro fleet, but sanctions limit access to Western technology, opening space for Chinese suppliers. These regional nuances ensure that the European hydro turbine market continues to evolve along heterogeneous policy, hydrology, and financing lines.

Competitive Landscape

The European hydro turbine market is moderately consolidated: Andritz, Voith, GE Vernova, and Siemens Energy together hold 60%–70% of 2025 revenue, backed by decades-long installed bases and proprietary digital-twin suites. Their twin strategy blends high-margin aftermarket service, where operating margins exceed 30%, with differentiated hardware such as fish-friendly runners and variable-speed drives. Andritz’s Hydro-Matrix and Voith’s StreamDiver exemplify modular solutions that deconstruct conventional, civil-heavy builds into more agile packages suited for small-hydro opportunities.

Niche specialists such as Gilkes, Rainpower, and Litostroj focus on 5–50 MW refurbishments, offering bespoke engineering and rapid deployment that larger OEMs often overlook. Canadian Hydro Components and Norcan Hydraulic Turbine are expanding into Eastern Europe via joint ventures, capitalizing on refurbishment budgets that favor cost-effective alternatives. Patent filings for fish-passage designs and additive-manufactured runners jumped 20% between 2023 and 2025, with Andritz and Voith leading submissions. Upcoming IEC standard revisions for variable-speed testing will likely reinforce incumbent advantages by raising compliance costs for smaller entrants.

Digitalization is the new battleground. GE Vernova’s predictive-maintenance platform claims to reduce forced outages by 25% across its monitored fleet, providing sticky service contracts. Siemens Energy is rolling out cybersecure SCADA layers that integrate with national grid-code mandates. As utilities demand real-time performance analytics, suppliers able to bundle hardware, software, and long-term service agreements will cement their share. However, sub-10 MW packages remain fragmented, offering room for agile players to carve profitable niches inside the European hydro turbine industry.

Europe Hydro Turbine Industry Leaders

General Electric Company

Andritz AG

Litostroj Power Group

Siemens AG

Voith GmbH & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Voith’s Green Highland secured a contract to modernize and maintain the Kinlochleven hydropower plant in Scotland. The project focuses on optimizing the performance of its Francis turbines and generative equipment, ensuring the continued operation and renewable energy output of this century-old facility.

- September 2025: ABB inaugurated a hydroelectric generator refurbishment line at its Ring Motor factory in Bilbao, Spain, to support hydropower modernization across Europe. The facility produces upgraded generators and stators to enhance efficiency, safety, and performance in aging plants. Initial orders from Spain and Norway reflect utilities' focus on lifecycle upgrades.

- July 2025: Croatia’s Koncar – Generators and Motors signed a three-year agreement to refurbish generating units at Bosnia’s Mostar and Rama hydropower plants. The project includes turbine and generator upgrades aimed at improving power reliability and performance, aligning with broader hydropower maintenance efforts in Southeastern Europe.

- June 2025: European hydropower modernization is central to renewable energy expansion, with investments like Upper Austria’s Ebensee pumped storage upgrades enhancing turbine efficiency and grid stability. These refits extend plant lifespans, improve performance, and align with EU decarbonization objectives, underscoring the importance of hydro turbine and generator retrofits.

Europe Hydro Turbine Market Report Scope

Hydro turbines are devices used in hydroelectric generation plants that transfer energy from moving water to a rotating shaft to generate electricity. Hydropower plants utilize these turbines to generate electricity as a result of the introduction of water to their blades. Hydropower is the process of generating power by using water to produce energy.

The hydro turbine market is segmented by technology, capacity, installation type, component, and geography. By technology, the market is segmented into reaction and impulse. By capacity, the market is segmented into small (less than 10MW), medium (10MW - 100MW), and large (greater than 100MW). By installation type, the market is segmented into new build, refurbishment/modernisation. By component, the market is divided among runner and blades, draft tube and mechanical parts, generator, control & digital systems, and others. The report also covers the market size and forecasts for the hydro turbine market across major countries in the region. The market size and forecasts for each segment have been done regarding revenue (USD billion).

By Technology

| Reaction Turbines |

| Impulse Turbines |

By Capacity

| Large Hydro (Above 100 MW) |

| Medium Hydro (10 to 100 MW) |

| Small and Micro Hydro (Below 10 MW) |

By Installation Type

| New Build |

| Refurbishment/Modernisation |

By Component

| Runner and Blades |

| Draft Tube and Mechanical Parts |

| Generator |

| Control & Digital Systems |

| Others |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| NORDIC Countries |

| Russia |

| Rest of Europe |

| By Technology | Reaction Turbines |

| Impulse Turbines | |

| By Capacity | Large Hydro (Above 100 MW) |

| Medium Hydro (10 to 100 MW) | |

| Small and Micro Hydro (Below 10 MW) | |

| By Installation Type | New Build |

| Refurbishment/Modernisation | |

| By Component | Runner and Blades |

| Draft Tube and Mechanical Parts | |

| Generator | |

| Control & Digital Systems | |

| Others | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe hydro turbine market?

The market was valued at USD 767.20 million in 2026 and is on track to reach USD 837.13 million by 2031.

Which country is expected to grow the fastest in hydro turbine installations?

The United Kingdom leads with a projected 3.78% CAGR to 2031, driven by large pumped-storage schemes under the Cap-and-Floor regime.

Why are refurbishment projects dominating new investments?

Refurbishments avoid lengthy permitting, cost less than greenfield builds, and can boost plant efficiency by up to 20%, making them the preferred option for aging European fleets.

How does variable-speed technology benefit hydro plants?

Variable-speed generators decouple turbine speed from grid frequency, widening efficient operating ranges and doubling participation in frequency-response markets.

Can solar-plus-battery projects fully replace pumped-storage hydro?

Batteries excel for 2-4 hour discharge windows but lack multi-day storage and black-start capability, so grid operators still forecast a need for additional pumped-storage capacity.

Which component segment is growing the fastest?

Generator upgrades, especially full-converter variable-speed systems, are the fastest-expanding component category through 2031.

Page last updated on: