Europe Halal Food And Beverage Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

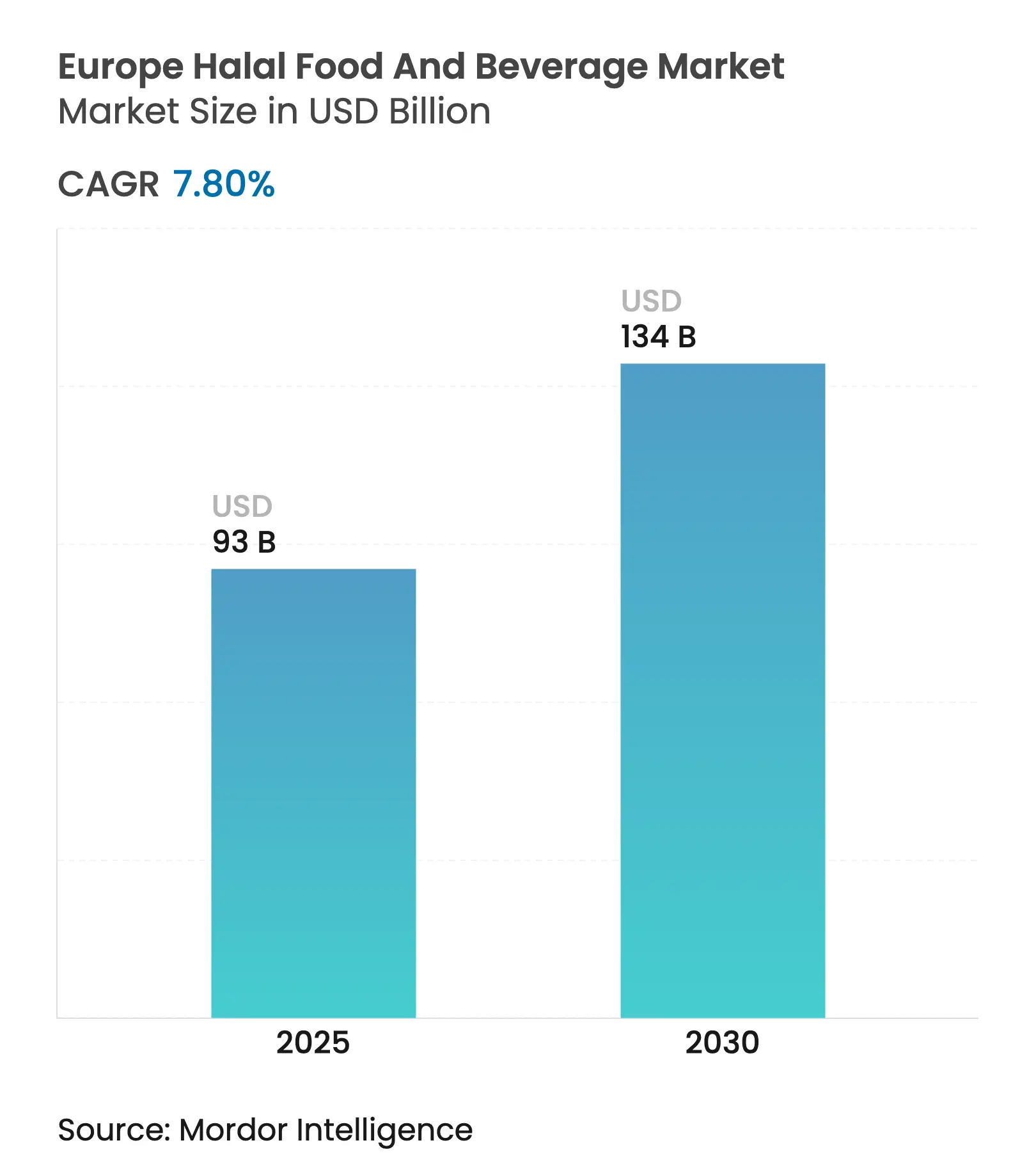

| Market Size (2025) | USD 93 Billion |

| Market Size (2030) | USD 134 Billion |

| Growth Rate (2025 - 2030) | 7.80 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Europe Halal Food And Beverage Market Analysis by Mordor Intelligence

The Europe halal foods and beverages market size stands at USD 93.0 billion in 2025 and is forecast to reach USD 134.96 billion by 2030, advancing at a 7.8% CAGR. Robust population growth among Europe’s 53.7 million Muslims, regulatory moves toward certification harmonization, and mainstream retailers’ private-label roll-outs collectively raise product visibility and normalize halal consumption across diverse demographic groups. Technology is tightening supply-chain controls through blockchain-enabled traceability, while e-commerce opens cross-border pathways for specialty meat and packaged goods that previously lacked scale in conventional distribution. Plant-based “halal-by-design” launches further diversify the Europe halal foods and beverages market, aligning ethical, health, and religious requirements within a single formulation. Despite the positive trajectory, activist pressure on ritual slaughter and the absence of a single EU-wide standard continue to elevate compliance costs and complicate intra-EU trade.

Key Report Takeaways

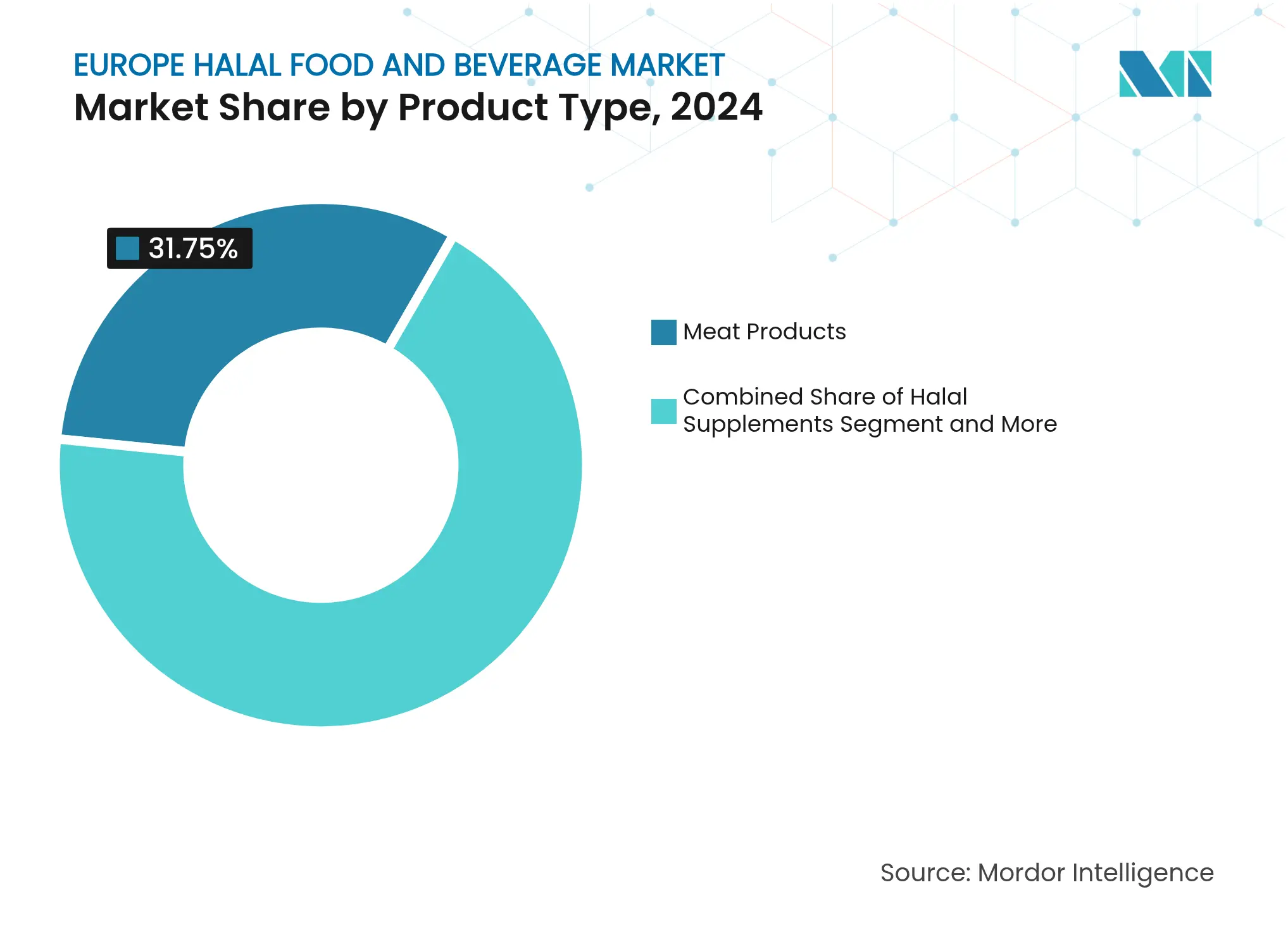

By product type, meat products held 31.75% of Europe halal foods and beverages market share in 2024; halal supplements are projected to expand at an 8.74% CAGR to 2030.

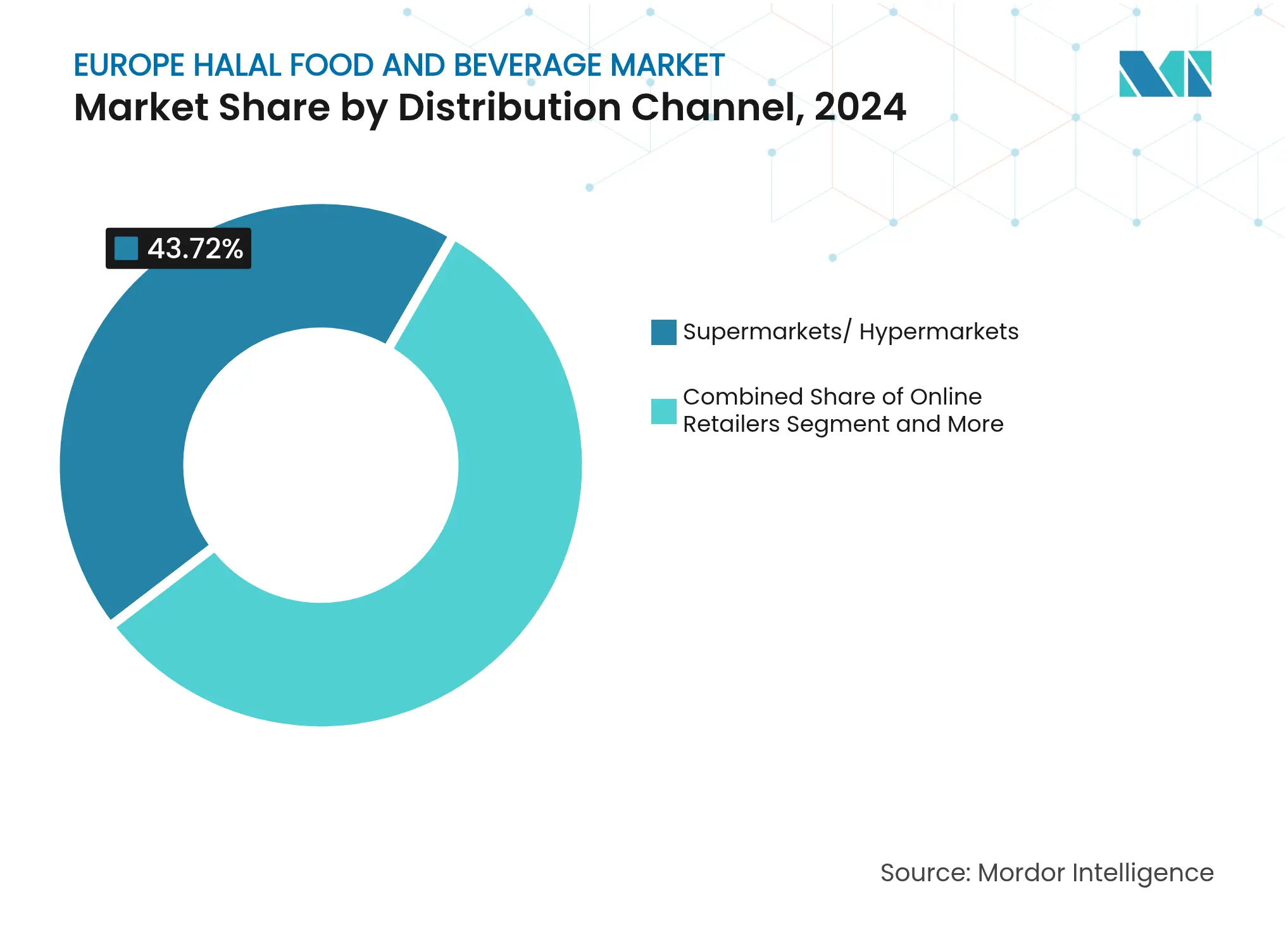

By distribution channel, supermarkets and hypermarkets captured 43.72% of Europe halal foods and beverages market size in 2024; online retailers record the highest projected CAGR at 9.27% through 2030.

By geography, France led with an 18.95% share of Europe halal foods and beverages market size in 2024; the Netherlands is advancing at an 8.18% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Halal Food And Beverage Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Muslim population & diaspora spend

Rising Muslim population & diaspora spend

| +1.8% | EU core markets, UK, Germany, France | Long term (≥ 4 years) |

( ) % Impact on CAGR Forecast

:

+1.8%

|

Geographic Relevance

:

EU core markets, UK, Germany, France

|

Impact Timeline

:

Long term (≥ 4 years)

|

Certification harmonization initiatives

Certification harmonization initiatives

| +1.2% | EU-wide, strongest in Netherlands, Belgium | Medium term (2-4 years) | |||

Retail private-label halal roll-outs

Retail private-label halal roll-outs

| +2.1% | Western Europe, France, Germany, UK | Short term (≤ 2 years) | |||

Cross-border e-commerce meat flows

Cross-border e-commerce meat flows

| +1.4% | Northern Europe, Germany, Netherlands | Medium term (2-4 years) | |||

Plant-based “halal-by-design” launches

Plant-based “halal-by-design” launches

| +0.9% | Spain, France, Germany, UK | Long term (≥ 4 years) | |||

Blockchain provenance solutions

Blockchain provenance solutions

| +0.6% | Netherlands, Germany | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Muslim Population & Diaspora Spend

Europe hosts 53.7 million Muslims whose annual spending continually outpaces population growth, creating dependable volume demand in the Europe halal foods and beverages market. Higher disposable incomes among second- and third-generation Muslims tilt purchases toward convenience formats, premium cuts, and fortified foods. Urban concentration in Paris, London, Berlin, and Amsterdam places these consumers within reach of large grocery networks that actively target them with season-long Ramadan promotions and loyalty campaigns. Supermarket participation reduces channel fragmentation by shifting demand away from niche ethnic shops to mass retail outlets with superior logistics. Diaspora influence extends beyond Muslims, as halal labels resonate with non-Muslims who equate the certification with cleaner slaughter practices and quality assurances.

Government-Backed Halal Certification Harmonization

The European Commission’s cross-border food-safety framework indirectly accelerates halal standard alignment, lowering the Europe halal foods and beverages industry entry barriers for small and mid-sized processors. Belgium and the Netherlands now accept joint audit protocols that cut repeat inspection costs by up to 30%, encouraging regional manufacturers to pursue wider geographic coverage. Early adopters are better positioned to win private-label supply contracts from retailers seeking a single EU-level certificate. Over the medium term, uniformity is expected to trim certification lead times from six months to fewer than three, freeing capital for product development.

Mainstream Retailers’ Private-Label Halal Roll-Outs

Carrefour’s 36% jump in private-label food sales includes a multi-country halal portfolio that doubles SKU count versus 2023. Tesco, Sainsbury’s, and Edeka mirror the approach, dedicating gondola ends to permanent halal ranges rather than seasonal Ramadan slots. Price premiums have fallen by nearly 12 percentage points, demonstrating that economies of scale generated in the Europe halal foods and beverages market now benefit final consumers. In-store visibility through bilingual packaging and QR codes linking to slaughter videos boosts trust and persuades flexitarian shoppers to trial halal items. Retailers also use data analytics to tailor planograms by neighborhood, ensuring optimum product-mix turnover.

E-Commerce-Led Cross-Border Specialty Meat Flows

Nosor Baladna’s revenue leap from EUR 300,000 to EUR 7 million in its first German year underscores how digital storefronts circumvent distribution-grid limitations. Online marketplaces integrate cold-chain logistics partners that guarantee 48-hour delivery across Benelux and DACH regions, expanding the Europe halal foods and beverages market beyond metropolitan clusters. Subscription models for “halal meat boxes” secure recurring revenue while lowering customer acquisition costs. Influencer partnerships on Instagram and TikTok strengthen brand storytelling and provide visual proof of slaughter compliance, combatting the trust deficit that plagues cross-border meat transactions.

Restraints Impact Analysis

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Lack of single EU-wide halal standard

Lack of single EU-wide halal standard

| -1.1% | EU-wide, particularly cross-border trade | Medium term (2-4 years) |

( ) % Impact on CAGR Forecast

:

-1.1%

|

Geographic Relevance

:

EU-wide, particularly cross-border trade

|

Impact Timeline

:

Medium term (2-4 years)

|

Mis-labeling scandals eroding trust

Mis-labeling scandals eroding trust

| -0.8% | UK, Germany, France | Short term (≤ 2 years) | |||

Higher unit cost versus conventional foods

Higher unit cost versus conventional foods

| -0.7% | Price-sensitive Eastern Europe | Long term (≥ 4 years) | |||

Activist push-back on ritual slaughter

Activist push-back on ritual slaughter

| -1.3% | Belgium, Germany, potential EU-wide | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Lack of Single EU-Wide Halal Standard

More than 50 certification bodies coexist, each interpreting jurisprudence differently, forcing processors to pursue multiple seals for multi-country distribution and inflating Europe halal foods and beverages industry operating costs. Fragmentation complicates supermarket sourcing schedules because SKU onboarding stalls until every inbound batch matches store-level compliance rules. Smaller manufacturers struggle to shoulder the redundant audit fees, leading to market exits or narrowed geographic coverage. The inefficiency directly tempers volume growth by limiting product availability on mainstream shelves.

Frequent Mis-Labeling Scandals Eroding Trust

The 2025 Welsh fraud case and Cardiff’s Universal Food fake-halal allegations rekindle consumer skepticism, prompting immediate dips in regional sales of uncertified fresh meat. Media amplification fuels scrutiny of local butchers and cash-and-carry outlets, driving cautious shoppers toward brands with tamper-evident packaging or digital traceability stamps. Retailers respond by widening audit scopes, adding indirect costs that trickle down the entire Europe halal foods and beverages market. The reputational damage also emboldens activist groups lobbying for stricter labeling laws, which could translate into higher compliance burdens.

Segment Analysis

By Product Type: Meat Products Remain Core While Supplements Accelerate

Meat products accounted for 31.75% of Europe halal foods and beverages market share in 2024, cementing their role as the non-negotiable centerpiece of Muslim diets. Demand for premium cuts and charcuterie continues to rise, encouraged by innovations such as nitrite-free halal sausages. The Europe halal foods and beverages market size tied to fresh and processed meat is forecast to enlarge in lockstep with urban population clusters that rely on supermarket butchery counters rather than neighborhood specialists. Halal supplements, although starting from a smaller base, post an 8.74% CAGR, reflecting a convergence of wellness and religious adherence.

Formulators of vitamins, protein, and omega-3 capsules substitute porcine gelatin with fish or plant-based alternatives, broadening penetration among athletes and aging consumers. Online subscription channels allow supplement brands to target diaspora students and professionals spread across university towns without large Muslim enclaves. The marketing narrative often centers on purity and clean-label attributes, appealing to secular consumers as well and thereby enlarging addressable volume. Over the forecast period, meat will remain indispensable, yet supplements are set to chip away at share gains as functional nutrition intersects with halal compliance.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Supermarkets Dominate, Digital Platforms Surge

Supermarkets and hypermarkets captured 43.72% of Europe halal foods and beverages market size in 2024 as chain operators integrated dedicated halal aisles within mainstream store formats. Vertical negotiation power allows retailers to lock in supply contracts that guarantee year-round availability, a key driver of shopper loyalty. Loyalty-card analytics reveal that non-Muslims account for nearly 22% of halal basket spend during Ramadan promotional weeks, underscoring crossover appeal.

E-commerce platforms record a 9.27% CAGR, propelled by immigrant communities accessing specialty items unavailable locally. The Europe halal foods and beverages market share attributed to digital sales remains single-digit yet is expanding rapidly as cold-chain innovations permit fresh-meat delivery in insulated recyclable packaging. Marketplace algorithms surface halal products when users search by ethical tags such as “animal-welfare” or “sustainable,” further broadening reach. Bricks-and-clicks hybrids, notably Carrefour Drive and Rewe’s home-delivery service, blur channel lines, ensuring the online curve continues to steepen.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

By early 2025, France leads the European halal foods and beverages market with an 18.95% share and five consecutive months of volume growth. Legacy brand Isla Délice expands its health-focused offerings, including nitrite-free chorizo and alcohol-free bread, while urban centers like Paris and Lyon integrate halal sections with QR-verified supply-chain data to address labeling concerns. Although government discussions on non-stun restrictions continue, domestic slaughter capacity remains unaffected, preserving local sourcing advantages. Germany, supported by a 6.6 million Muslim population, anticipates market growth from USD 12.44 billion in 2022 to USD 18.97 billion by 2032. Isla Délice’s acquisition of Gürkan strengthens its premium product portfolio, while Aldi explores limited-edition halal lines. However, judicial restrictions on ritual slaughter increase reliance on imports from Poland and Ireland, and certification challenges persist despite blockchain pilots in Bavaria aimed at improving transparency.

The Netherlands accelerates with advanced logistics and regulatory support for harmonized certification, leveraging Rotterdam’s food-port infrastructure to deliver chilled halal meats to Scandinavian markets within 24 hours. Digital audit acceptance by Dutch regulators reduces procedural delays, while the UK maintains steady growth with a compound annual rate above 5%, driven by retailer commitments to permanent halal ranges and GBP 1.7 billion in annual spending. Eastern Europe, though still emerging, is set for growth as migration inflows expand local Muslim populations and e-commerce bridges gaps in store density.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

Europe's halal foods and beverages market shows moderate fragmentation, with a concentration score of 4. Global players like Nestlé, Mars, and Ferrero are certifying mainstream products such as KitKat, Pringles, and Nutella through established supply chains, blending halal and conventional offerings. Processors like Isla Délice and Danish Crown’s halal division build trust through single-source slaughter oversight and religious authority endorsements. The dual-track structure enables niche players to scale quickly by outsourcing functions like cold-chain logistics and digital marketing. Strategic consolidations are accelerating, as seen in Mars’ USD 35.9 billion acquisition of Kellanova in 2024, which could drive halal snack innovation, and Isla Délice’s January 2025 acquisition of Gürkan, expanding its SKUs to over 250 and strengthening its presence in Germany’s premium butchery market.

Technology is becoming a critical differentiator. Carrefour uses blockchain supplier portals for instant authenticity checks, marketed to consumers via on-pack QR codes, while OneAgrix attracts processors with tiered subscription models similar to software-as-a-service. Fraud incidents, such as Cardiff’s fake-halal scandal, are pushing retailers and caterers to adopt transparency measures, rewarding early movers with preferred-vendor status. Companies failing to invest in transparency risk delisting from chain supermarkets, weakening their competitive position.

Europe Halal Food And Beverage Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Isla Délice Group has acquired Gürkan, a premium halal meat business based in Germany, thereby gaining entry into the German halal market. With this acquisition, Isla Délice can now provide more than 250 halal products, featuring exclusive items that were not accessible in Germany's halal retail outlets before.

- January 2025: French halal foods company Isla Délice has acquired German halal meat producer Gürkan, marking a significant expansion into the German market.

- December 2024: Kansas-based Deli Halal, known for its halal-certified meat and cheese products, has rolled out a new line of halal-certified sliced deli meats. These products are now available in major supermarket chains, including Giant Food Stores and Stop & Shop Supermarkets, spanning New England and much of the East Coast.

Table of Contents for Europe Halal Food And Beverage Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Muslim population & diaspora spend

- 4.2.2Government?backed halal certification harmonization

- 4.2.3Mainstream retailers- private-label halal roll-outs

- 4.2.4E-commerce-led cross-border specialty meat flows

- 4.2.5Novel plant-based 'halal-by-design' launches

- 4.2.6Blockchain-enabled end-to-end provenance tools

- 4.3Market Restraints

- 4.3.1Lack of single EU-wide halal standard

- 4.3.2Frequent mis-labeling scandals eroding trust

- 4.3.3Higher unit cost versus conventional foods

- 4.3.4Activist push-back on ritual slaughter

- 4.4Value Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

- 4.8Consumer Behaviour Analysis

5. Market Size and Growth Forecasts (Value, Volume)

- 5.1By Product Type

- 5.1.1Halal Food

- 5.1.1.1Meat Products

- 5.1.1.2Bakery Products

- 5.1.1.3Dairy Products

- 5.1.1.4Confectionery

- 5.1.1.5Ready Meals & Sauces

- 5.1.1.6Other Halal Foods

- 5.1.2Halal Beverages

- 5.1.3Halal Supplements

- 5.2By Distribution Channel

- 5.2.1Supermarkets / Hypermarkets

- 5.2.2Convenience Stores

- 5.2.3Specialty Halal Stores & Butchers

- 5.2.4Online Retail & Marketplaces

- 5.2.5Food-service (HoReCa)

- 5.3By Country

- 5.3.1Germany

- 5.3.2United Kingdom

- 5.3.3France

- 5.3.4Spain

- 5.3.5Italy

- 5.3.6Russia

- 5.3.7Netherlands

- 5.3.8Belgium

- 5.3.9Rest of Europe

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1Nestle SA

- 6.4.2Ferrero International SA

- 6.4.3Mars Inc.

- 6.4.4Coca-Cola Co.

- 6.4.5JAB Holding (Jacobs Douwe Egberts)

- 6.4.6Tahira Foods

- 6.4.7KQF Foods

- 6.4.8Isla Dolice

- 6.4.9Janan Meat Ltd

- 6.4.10Bilal Group

- 6.4.11Danish Crown (DANISH CROWN HALAL)

- 6.4.12BRF S.A. (Sadia / Perdix EU)

- 6.4.13Midamar Corporation

- 6.4.14Al Islami Foods

- 6.4.15Carrefour SA (Halal private-label)

- 6.4.16Tesco PLC (Authentic Halal)

- 6.4.17The Biltong Factory

- 6.4.18Mission Foods

- 6.4.19Heura Foods

- 6.4.20Cherkizovo Group

7. Market Opportunities & Future Outlook

Europe Halal Food And Beverage Market Report Scope

Halal refers to the term lawful and permissible that follows the Islamic guidelines for producing and manufacturing food and beverage products. The European market for halal food and beverage is segmented by product type into halal food, halal beverages, and halal supplements. Based on the distribution channel, the market is segmented into hypermarkets/supermarkets, specialty stores, convenience stores, and other distribution channels. This study also analyses regions such as the United Kingdom, Germany, France, Italy, Spain, Russia, and the Rest of Europe. The report offers market size and forecast value (USD million) for all the above segments.