Europe Guar Market Analysis by Mordor Intelligence

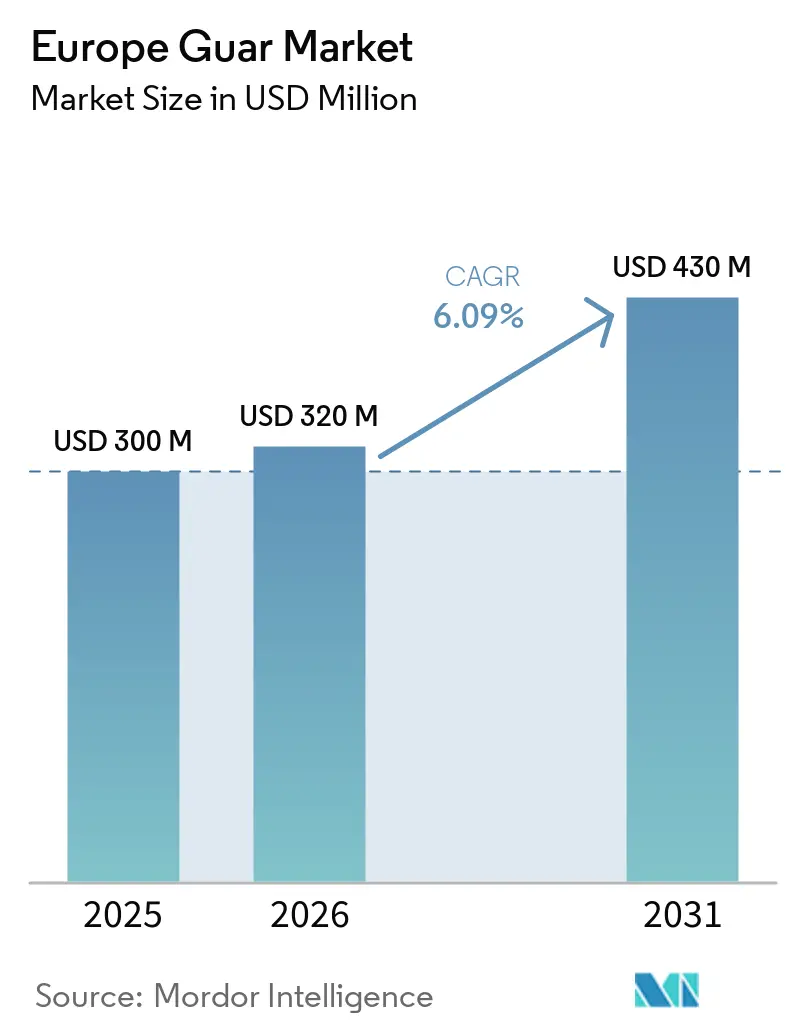

The Europe guar market size is projected to grow from USD 300.00 million in 2025 and USD 320.00 million in 2026 to USD 430.00 million by 2031, with a CAGR of 6.09% during 2026-2031. Factors such as improving compliance with clean-label standards, stricter ethylene oxide residue limits, and a shift toward cost-effective natural thickeners are influencing procurement decisions among more than 27,000 food processors in Europe. Additionally, demand is increasing in the pharmaceutical and cosmetics industries, where guar’s plant-based origin enables the replacement of synthetic binders while aligning with safety preferences for patients and consumers. In the compound feed sector, structural protein deficits in Europe, combined with guar meal’s 15–30% cost advantage over soybean meal, create a third value pool that supports overall demand stability. Meanwhile, upstream consolidation among alternative hydrocolloid suppliers, such as Tate & Lyle’s integration of CP Kelco, increases switching costs for buyers seeking comprehensive texture solutions.

Key Report Takeaways

- By geography, Germany led with the largest 23.5% of the Europe gaur market share in 2025, while Spain's market size is projected to expand at the fastest 9.7% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Guar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding food and beverage demand | +1.8% | Germany, France, United Kingdom, Netherlands, and Spain | Medium term (2–4 years) |

| Growth in animal feed applications | +1.5% | Germany, France, Netherlands, and Spain | Long term (≥ 4 years) |

| Increasing use in pharma and cosmetics | +1.2% | Germany, United Kingdom, and France | Medium term (2–4 years) |

| Rising need for natural thickeners | +1.4% | Pan-European with focus in Spain and Germany | Short term (≤ 2 years) |

| European Union projects on Mediterranean guar cultivation | +0.6% | Spain, Italy, and Greece | Long term (≥ 4 years) |

| Bio-based fracturing fluids for geothermal energy | +0.5% | Italy and Iceland, emerging in France and Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Food and Beverage Demand

The demand for guar in Europe is driven by its functional role in processed food applications, including bakery, dairy, and sauces, where it enhances texture and stability. In 2024, the European Food Safety Authority (EFSA) confirmed that guar gum (E412) remains authorized and widely used across various food categories, emphasizing its safety and regulatory acceptance in the food industry [1]Source: European Food Safety Authority (EFSA), Re-evaluation of Guar Gum (E412), efsa.europa.eu. This regulatory approval underpins its extensive application as a natural thickener and stabilizer. Additionally, food manufacturers are increasingly reformulating products to meet clean-label trends, further supporting the use of guar gum in a broad range of processed food applications.

Growth in Animal Feed Applications

Guar meal is gaining traction as a protein-rich ingredient in animal feed formulations across Europe. It is an effective alternative to traditional protein sources like soybean meal, contributing to feed diversification and cost efficiency. Its beneficial amino acid profile and functional properties improve feed efficiency and animal performance. Furthermore, the growing emphasis on sustainable, cost-effective feed ingredients is driving their adoption in the livestock and poultry industries. Reliable availability through global supply chains further reinforces its role in feed formulations, supporting its growing utilization in the European animal nutrition market.

Increasing Use in Pharma and Cosmetics

Guar gum is increasingly utilized in pharmaceutical and cosmetic formulations due to its natural origin and versatile properties. Its functions as a binder, thickener, and stabilizing agent make it applicable in tablet formulations, controlled-release systems, and various personal care products. The rising demand for plant-based and clean-label ingredients in Europe is driving manufacturers to replace synthetic additives with natural alternatives such as guar gum. Furthermore, favorable regulatory frameworks and advancements in formulation technologies are broadening its applications, solidifying its importance in the pharmaceutical and cosmetic industries.

Rising Need for Natural Thickeners

Consumer preference for natural ingredients is driving a shift away from synthetic thickeners toward plant-based alternatives such as guar gum. According to the Center for the Promotion of Imports from Developing Countries, the European natural food additives market was valued at approximately EUR 8.6 billion (USD 9.3 billion) in 2025, indicating a significant market for naturally derived ingredients in food applications [2]Source: Centre for the Promotion of Imports from Developing Countries (CBI), What is the demand for natural food additives in Europe?, cbi.eu. Guar gum is favored for its botanical origin and alignment with clean-label requirements. Food manufacturers are increasingly reformulating products to eliminate chemically modified additives, boosting demand for guar gum in sauces, dairy products, and bakery applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of guar seed | -1.2% | Pan-European with acute in Germany and United Kingdom | Short term (≤ 2 years) |

| Competition from substitute hydrocolloids | -1.0% | Germany, France, and United Kingdom | Medium term (2–4 years) |

| European Union ethylene-oxide residue regulations | -0.8% | Pan-European with strict in Germany and Netherlands | Short term (≤ 2 years) |

| Clean-label reformulation pressures | -0.5% | Spain, Italy, and France | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Guar Seed

The European guar market is notably affected by guar seed price volatility, primarily due to its reliance on Indian production and the crop's sensitivity to weather conditions. Fluctuations in monsoon rainfall and sowing patterns in India directly affect guar seed availability and pricing, leading to procurement challenges for European buyers. Data from the National Commodity & Derivatives Exchange Limited (NCDEX) in October 2025 indicates that guar seed prices fell by 7.45% within a month, reaching INR 4,808 per quintal (USD 579 per metric ton) [3]Source: NCDEX, “Monthly Commodity Digest – October 2025,” ncdex.com.. This significant short-term price fluctuation complicates long-term sourcing agreements, heightens raw material cost uncertainties for food and industrial manufacturers, and prompts end users to consider alternative hydrocolloids to mitigate supply and pricing risks.

Competition from Substitute Hydrocolloids

Guar gum is encountering growing competition from alternative hydrocolloids, including xanthan gum, pectin, and carrageenan, which provide comparable functional properties in food, pharmaceutical, and personal care applications. These alternatives often have the advantage of diversified sourcing and, in certain cases, controlled production processes that ensure consistent quality and supply. In Europe, manufacturers are increasingly turning to these substitutes to decrease reliance on guar-based inputs and address supply chain risks. This trend is particularly prominent among large-scale producers aiming for formulation stability, cost consistency, and greater flexibility in ingredient sourcing across various applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Germany led with the largest 23.5% of the Europe gaur market share in 2025, driven by its extensive food-processing and pharmaceutical industries. Demand is bolstered by the bakery, dairy-alternative, and personal care sectors, which utilize guar gum for its texturizing and binding properties. Industrial clusters in southern Germany contribute to consistent consumption, particularly in pharmaceutical excipients and cosmetic formulations. Regulatory compliance requirements, such as contaminant testing and traceability, influence sourcing strategies. Buyers increasingly focus on certified suppliers to ensure consistent quality and mitigate supply chain disruptions, shaping procurement practices across both food and non-food applications.

Spain is projected to expand at the fastest 9.7% CAGR from 2026 to 2031. Manufacturers are adopting guar gum as a cost-effective stabilizer to replace fats and starches in processed foods, enhancing profit margins while maintaining product quality. Additionally, growth in poultry and livestock production drives demand for guar meal in animal feed formulations. Consumer preferences for clean-label and non-genetically modified products further encourage the adoption of guar gum across various food categories. Early-stage domestic cultivation initiatives suggest potential for localized supply, though commercial-scale production remains limited in the short term.

Europe represents a substantial market for guar gum, driven by strong demand across the food processing, pharmaceutical, and personal care industries. According to the International Trade Centre (Trade Map), Europe imported 3.34 lakh metric tons of mucilage and thickeners derived from guar in 2025 against 3.11 lakh metric tons in 2024, marking a steady increase compared to previous years [4]Source: International Trade Centre (ITC Trade Map), Imports of Guar Gum (HS Code 130232) – Europe Aggregation, trademap.org. This reflects consistent regional demand, particularly in bakery, dairy alternatives, and cosmetics applications. Strict regulatory standards and quality requirements significantly influence sourcing strategies, with buyers prioritizing certified suppliers to ensure product consistency and compliance across diverse end-use industries.

Competitive Landscape

The competitive landscape includes a combination of global ingredient suppliers and specialized guar processors competing across food, feed, and industrial applications. Large multinational companies utilize integrated supply chains and diversified hydrocolloid portfolios to deliver customized texture solutions. This approach intensifies competition for guar gum in key applications such as dairy, sauces, and bakery products. Suppliers prioritize consistent quality and adherence to stringent regulatory standards to secure long-term contracts with food manufacturers and pharmaceutical companies in Europe.

Ingredient companies are broadening their portfolios through strategic investments and product innovation. Firms offering multiple hydrocolloids, such as xanthan, pectin, and carrageenan, provide tailored solutions that reduce reliance on single ingredients. This diversification enhances their market position and increases substitution pressure on guar gum suppliers. However, guar gum remains relevant due to its natural origin and functional efficiency. Smaller companies compete by emphasizing organic certification, traceability, and niche applications, particularly in pharmaceutical and personal care segments where formulation specificity is essential.

Competition is escalating as hydrocolloid suppliers expand integrated portfolios and deliver customized texture solutions across food and pharmaceutical applications. Companies with diversified ingredient systems gain a competitive edge by addressing multiple functional requirements within a single formulation. Guar gum suppliers counter this by focusing on consistent rheology, technical support, and supply chain transparency to retain customers. Growing emphasis on sustainability, traceability, and compliance with European regulatory frameworks significantly influences procurement decisions.

Recent Industry Developments

- February 2026: The European Commission has updated food additive regulations under Regulation (EU) 2026/196, establishing stricter purity specifications, residue limits, and usage guidelines for additives, such as guar gum, particularly in food products intended for vulnerable groups, including infants and young children.

- November 2024: Tate & Lyle finalized the acquisition of CP Kelco to enhance its portfolio of specialty food ingredients, including guar-based hydrocolloids and plant-derived texture solutions. This acquisition bolstered the company's expertise in clean-label and natural ingredient applications, addressing the increasing demand for guar and other plant-based stabilizers in the global food and beverage market.

- September 2024: Denmark’s Ministry of Justice has issued a draft proposal to amend the usage conditions and specifications for various food additives, including guar gum, specifically in infant food categories. The proposal aligns with Regulation (EC) No 1333/2008 and Regulation (EU) No 231/2012, emphasizing updated purity standards, allowable usage levels, and safety requirements for additives in infant nutrition products.

Europe Guar Market Report Scope

Guar is a plant whose seeds are processed to produce guar gum, a natural polysaccharide. Guar gum is commonly utilized as a thickening, stabilizing, and binding agent across food, pharmaceutical, cosmetic, and industrial applications. The Europe Guar market report includes production analysis (area harvested, yield and volume), consumption analysis (value and volume), import analysis (value and volume), export analysis (value and volume), wholesale price trend analysis and forecast, regulatory framework, list of key players, logistics and infrastructure, and seasonality analysis. The market is segmented by country (Germany, United Kingdom, France, Russia, Netherlands and the rest of Europe). The market forecasts are provided in terms of value (USD) and volume (metric tons).

By Geography

| Europe | Germany | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| United Kingdom | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| France | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Russia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| By Geography | Europe | Germany | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| United Kingdom | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| France | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Russia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

How large will the Europe gaur market be by 2031?

The Europe market is forecast to reach USD 430 million by 2031.

Which country currently leads demand?

Germany held the largest 23.5% of market share in 2025 due to high guar-gum imports and dense food-processing capacity.

What is driving Spain’s rapid growth?

A USD 181 billion food-processing economy and widespread value-seeking behavior are pushing Spain toward the fastest 9.7% CAGR from 2026 to 2031.

How do ethylene-oxide limits affect suppliers?

Regulation 2024/1038 requires non-fumigation sterilization, adding 5–10% to landed costs and causing shipment rejections at European Union borders.

Page last updated on: