Tunisia Agriculture Market Analysis by Mordor Intelligence

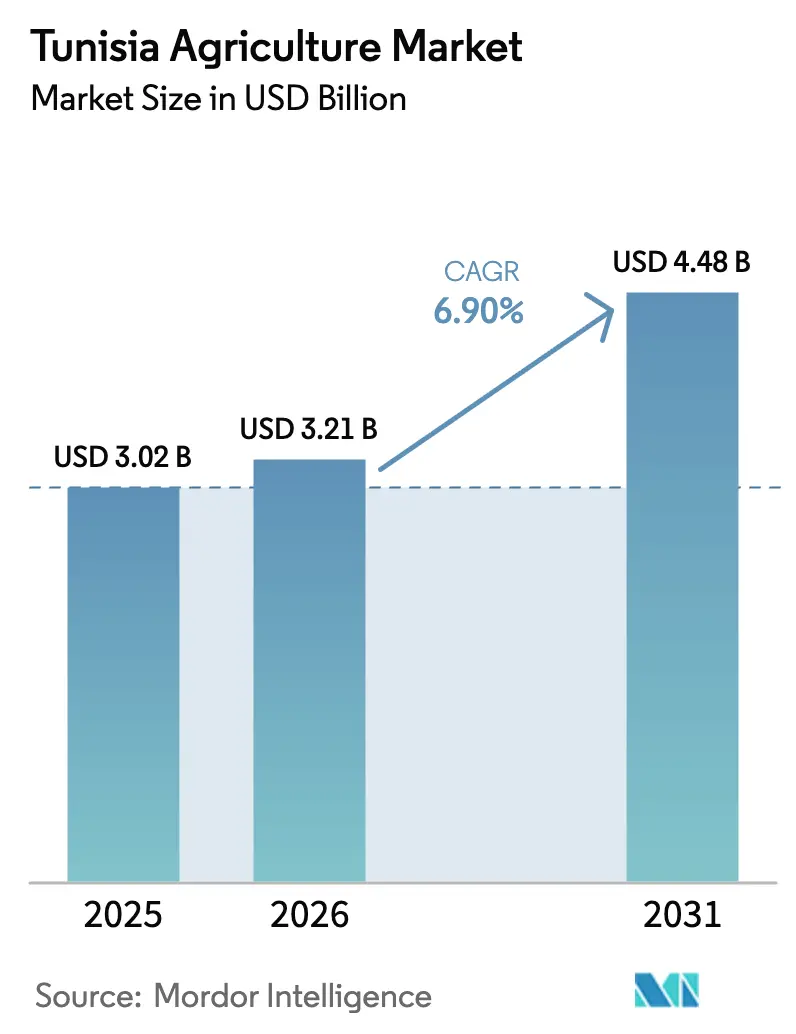

The Tunisia Agriculture Market size is anticipated to increase from USD 3.02 billion in 2025 to USD 3.21 billion in 2026 and reach USD 4.48 billion by 2031, growing at a CAGR of 6.90% over 2026-2031. The Tunisia agriculture market is expanding as greenhouse horticulture and premium olive oil exports offset structural water deficits. Public-sector capital, including the World Bank’s USD 520 million package, is being utilized to rehabilitate irrigation and post-harvest infrastructure[1]Source: United States Department of Agriculture, “Tunisia Grain and Feed Annual Report,” ipad.fas.usda.gov. Meanwhile, a EUR 59 million (USD 62 million) green-finance facility reduces borrowing costs for drip irrigation. Record olive oil output in the 2024-2025 marketing year, along with the introduction of new salt-tolerant cereal cultivars and the near-shoring advantages created by the European Union's Green Deal, are lifting profitability across export corridors. At the same time, fragmented landholdings and chronic water scarcity hinder cereal yields, thereby maintaining high import demand.

Key Report Takeaways

- By commodity type, cereals and grains accounted for the largest share, comprising 45% of the Tunisian agricultural market size in 2025. Fruits and vegetables emerge as the fastest-growing segment, expanding at a 6.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Tunisia Agriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government support and subsidy programs | +0.8% | National priority zones Kairouan, Kasserine, Sidi Bouzid | Medium term (2-4 years) |

| Growing domestic demand for cereals | +0.6% | Coastal cities Tunis, Sfax, Sousse | Long term (≥ 4 years) |

| Rising import demand for Tunisian olive oil | +1.0% | Sfax, Mahdia, Monastir | Short term (≤ 2 years) |

| Expansion of greenhouse horticulture footprint | +0.7% | Sahel, Sfax, Kebili, Tozeur | Medium term (2-4 years) |

| Near-shoring effect of the European Union Green Deal | +0.5% | Cap Bon, Sahel tomato and citrus corridors | Medium term (2-4 years) |

| Adoption of salt-tolerant cereal cultivars and solar-powered desalination | +0.4% | Kairouan, Mahdia, Sfax | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Support and Subsidy Programs

The World Bank's USD 300 million financing, approved in March 2024, modernizes 15,000 hectares of irrigation in the Medjerda Valley and funds 50 cold-chain aggregation centers, reducing spoilage losses in tomatoes and peppers from 25% to below 10%. Cabinet approval in June 2025 for fertilizer imports places subsidized urea and diammonium phosphate at prices 40% below global benchmarks, stabilizing cereal input costs. The EUR 59 million (USD 62 million) Green Economy Financing Facility halves the interest rates for micro and small-scale growers shifting to drip irrigation, reducing payback periods to under four years [2]Source: European Bank for Reconstruction and Development, “EBRD, EU, and TCX Launch EUR 59 Million Green Economy Financing Facility in Tunisia,” ebrd.com. These overlapping interventions compress production risk and raise net margins, especially for smallholders. Improved rural credit access further accelerates the uptake of technology and land consolidation.

Growing Domestic Demand for Cereals

Urban population growth of 1.1% per year in Tunis and Sfax underpins rising bread consumption, which keeps annual soft-wheat demand near 2.1 million metric tons, while domestic output reached only 1.25 million metric tons in the marketing year 2024-2025. Office des Céréales therefore imported 1.8 million metric tons of soft wheat and 400,000 metric tons of durum, spending USD 600 million in the marketing year 2024-2025. Subsidized bread prices at USD 0.06 per baguette (TND 0.19) sustain affordability but strain public finances. Genetic gains from new heat-tolerant durum varieties are indicated to increase yields to 2.2 metric tons per hectare by 2028, narrowing the gap between output and consumption.

Rising Import Demand for Tunisian Olive Oil

A record 340,000 metric tons olive oil crop in 2024-2025 lifted Tunisia to the world’s second-largest exporter. Firms diversified buyers in October 2025, shipping organic and Protected Designation of Origin certified oils to Asia and South America at 20% to 30% premiums over commodity grades. Gulf Capital took an equity position in CHO Company in May 2025, financing the bottling lines that capture value-added products in Tunisia. Investments in traceability made to comply with European pesticide thresholds of below 0.01 parts per million now underpin marketing claims in new regions. Higher export earnings feed back into grove renewal and mechanized harvesting.

Adoption of Salt-Tolerant Cereal Cultivars and Solar-Powered Desalination

Soil salinity touches 1.5 million hectares nationwide. The “Salim” durum wheat line tolerates eight deciSiemens per meter and yields 1.8 metric tons per hectare on degraded soils, which is double the yield of traditional varieties. Distribution reached 12,000 hectares in 2025 and aims at 50,000 hectares by 2028. Solar-powered reverse-osmosis units in Gabes and Mahdia treat groundwater to below one deciSiemens per meter, costing USD 8,000 per hectare to install yet eliminating USD 1,200 per hectare in diesel pumping each year. Lower operating costs and rising vegetable prices shorten payback to seven years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic water scarcity and inefficient irrigation networks | −1.2% | Kairouan, Kasserine, Sidi Bouzid, southern governorates | Long term (≥ 4 years) |

| Soil salinity and land degradation in coastal regions | −0.6% | Sahel, Sfax, Mahdia, Gabes | Long term (≥ 4 years) |

| Fragmented landholding limiting mechanization | −0.5% | Nationwide average farm 5 hectares | Medium term (2-4 years) |

| Stricter phytosanitary rules and pest incursions | −0.3% | Cap Bon, Sahel, Sfax export zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Water Scarcity and Inefficient Irrigation Networks

Renewable water supply averages 450 cubic meters per capita, far below the 1,000 cubic meter scarcity threshold[3]Source: Food and Agriculture Organization, “FAO Aquastat: Tunisia Water Resources,” fao.org/aquastat. Open canals lose up to 50% of flow. A USD 220 million corridor project replaces them with pressurized pipelines on 25,000 hectares, yet the full benefits will not arrive until 2028. Aquifer levels in the Sahel decline by 0.5 meters per year, and desalinated water at USD 1.50 per cubic meter remains uneconomical for broadacre crops, reinforcing reliance on rainfall patterns.

Fragmented Landholding Limiting Mechanization

The average plot size of five hectares sits below economic thresholds for combine harvesters. Custom hire costs USD 80 per hectare, eroding margins for cereal growers. Attempts to replicate dairy-sector cooperatives that aggregated 200 producers have stalled in field crops due to legal uncertainties around shared assets. Land consolidation proposals face political resistance, slowing the adoption of precision planting and harvest technologies that could lift productivity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Commodity Type: Cereals and Grains Face a Structural Water Ceiling

Cereals and grains accounted for 45% of Tunisia's agricultural market in 2025. The segment's CAGR lags behind the broader Tunisia agriculture market growth, as average wheat yields remain at 1.5 metric tons per hectare. New irrigation rehabilitation in the Medjerda Valley and the saline-tolerant “Salim” line aim to elevate productivity. However, imports will cover a 900,000-metric-ton soft-wheat gap through 2031. Domestic barley output of 600,000 metric tons meets only half of the feed demand. The adoption of conservation agriculture practices, including minimum tillage and stubble retention, improves soil moisture but requires machinery that is often beyond the reach of most smallholders.

The fruit and vegetable sector in Tunisia is projected to be the fastest-growing segment between 2026 and 2031, with a CAGR of 6.8%, despite cereals and grains holding the largest market share in 2025. This growth is attributed to factors such as Tunisia's strategic advantage as a leading organic exporter recognized by the EU and Switzerland, the adoption of modern technologies like greenhouse horticulture, shifting consumer preferences towards fresh produce, and targeted government support for high-value agro-food products.

Geography Analysis

The Medjerda Valley in the northwest anchors Tunisia’s grain and forage production, supported by relatively reliable surface water and a dense network of feeder canals. Ongoing rehabilitation of these canals improves delivery efficiency and limits seasonal rationing, giving growers a productivity edge over rain-fed zones. Access to paved roads and nearby milling hubs further shortens the time from harvest to processor, lowering spoilage and transportation costs. As irrigation upgrades continue, the valley is anticipated to preserve its role as the country’s principal food-grain corridor.

The Sahel coastal strip, stretching from Sousse to Mahdia, is a major hub for olive oil processing and horticulture exports. Proximity to deep-water ports and a cluster of modern mills enables producers to respond quickly to shifts in overseas demand and phytosanitary audits. Private equity funding supports integrated supply chains that capture higher margins through bottling and branding, enabling companies to achieve greater profitability. Despite concerns over climatic volatility, growers are increasingly adopting drip irrigation and certified organic practices to mitigate risks.

Southern governorates such as Kebili, Tozeur, and Gabes leverage geothermal resources and high solar irradiance to power greenhouses and date-palm packhouses. Solar photovoltaics and low-carbon heating align with European importers’ sustainability criteria, strengthening market access for off-season tomatoes and premium Deglet Nour dates. Despite chronically low groundwater reserves, investment in precision irrigation keeps expansion on track. Interior regions, such as Kairouan and Sidi Bouzid, lag in technology uptake, but targeted credit lines are beginning to narrow the gap.

Regulatory Landscape

Tunisia's agricultural sector is overseen by the Ministry of Agriculture, Water Resources and Fisheries (MARHP), which sets sector strategy and the policy framework for irrigation, water infrastructure, and production and trade. A key structural feature is the Office des Céréales, which maintains a state monopoly on the import, purchase, and sale of wheat and wheat products for the domestic market, while barley imports are liberalized for private importers. Private wheat imports can also occur under temporary admission when the finished product is exported.

Food and feed controls are in transition as the Food and Feed Safety Law moves toward full implementation through its pending implementing texts, with existing rules remaining in force in the interim. Investment conditions continue to be shaped by the 2016 Investment Law, including incentives of up to 50% for acquisition of agricultural equipment and high-tech project categories. Foreign entities can obtain long-term land leases but cannot own agricultural land, which affects how foreign participation develops in primary production.

Value Chain Analysis

Tunisia's crop value chain is shaped by fragmented smallholder production upstream, with farms commonly operating on a few hectares, which makes mechanization and standardized agronomy harder to scale. Input availability and affordability are persistent friction points. The government has relied on subsidized fertilizer stock-building and streamlined financing for the 2025-2026 season, but farmer organizations reported continued shortages of key products such as ammonium nitrate and diammonium phosphate, contributing to delayed planting decisions and pressure on early-season fruit and vegetable supply.

Water is the binding constraint across stages, since agriculture consumes most national water resources and losses from aging irrigation and conveyance systems reduce effective availability at farm level. Downstream, collection, grading, storage, and logistics determine export viability for higher-value chains (olive oil, dates, and greenhouse vegetables), while cereals remain shaped by institutional buying and import rules. Bottlenecks persist in storage capacity, cold-chain access outside major corridors, and transparency in grain collection and weighing, which amplifies price and quality disputes. Programs such as ARDII-Tounes (2026-2030) focus on climate-resilient seed systems, wastewater and water engineering, and policy dialogue mechanisms, aligning modernization investments with supply-chain performance improvements rather than only expanding planted area.

Competitive Landscape

Tunisia’s fresh-produce chain starts with more than 200,000 smallholder growers who grow tomatoes, peppers, citrus, melons, and dates on plots of 3 to 5 hectares. Consolidation appears farther downstream, where vertically integrated firms control branding, certification, and cold storage. Groupe Sotovit and Atlas Fruits operate packing houses equipped with optical sorters, which reduce rejection rates in European markets from 12% to below 5%. Their GlobalGAP and organic seals translate into price premiums of 15% to 20% in European Union retail aisles. Société Nouvelle Agricole utilizes contract farming in Cap Bon and Nabeul to supply seedlings, provide advice, and offer guaranteed pickup to 300 growers, thereby creating full traceability for phytosanitary checks.

Value addition centers on life-extension rather than processing. Greenhouse clusters in Kebili and Tozeur tap geothermal heat to ship winter tomatoes at USD 2.63 per kilogram (EUR 2.50 per kilogram), roughly double summer prices. Modified-atmosphere films now stretch shelf life to 14 days, making sea freight to northern Europe practical. Société Ellouhou Dates hand-sorts Deglet Nour and Allig varieties and secures 20% to 30% premiums in North American and Gulf stores. Solar photovoltaic projects guaranteed by the Multilateral Investment Guarantee Agency reduce electricity costs for regional cold rooms by 40%, allowing warehouses to operate profitably at smaller scales.

Competition hinges on fast port access and compliance with carbon audits mandated by the European Union Green Deal. Two-day sailings from Tunis to Marseille emit 0.15 kilograms of carbon dioxide per kilogram of produce, versus 0.45 kilograms for Turkish routes, giving Tunisian shippers a measurable edge. Only 8% of vegetable growers hold third-party organic certificates, leaving ample room for certification-driven differentiation. Leading exporters already utilize blockchain traceability and Internet of Things temperature sensors in refrigerated containers, while many small aggregators rely on paper logs, creating a fragmented supply chain that rewards verified operators and leaves uncertified producers vulnerable to volatile spot demand.

Market Opportunities and Future Outlook

Policy and funding flows are concentrating on water security, mechanization, and higher-efficiency production systems, which creates room for irrigation technologies, on-farm energy solutions, and digitized agronomy services. In April 2026, the World Bank provided financing of about EUR 305 million for water security and irrigation, targeting infrastructure in Jendouba, Beja, Bizerte, and Siliana. This reinforces demand for modern conveyance, pressurization, and monitoring solutions tied to irrigation rehabilitation. The government's 2026-2030 agriculture strategy, launched through a restricted ministerial council in April 2026, places food and water sovereignty, climate resilience, and modernization of cereal and dairy systems at the center of reforms, while also prioritizing digital channel modernization and measures aimed at limiting speculation.

On-farm and near-farm investment is supported through incentives under the national investment law (up to 50% for high-tech agricultural projects), supporting adoption of smart irrigation, renewable energy, and precision tools, especially where groundwater scarcity and input volatility increase production risk. The January 2026 inauguration of a EUR 6.5 million Italian-funded modernization project at the Echaal agricultural complex in Sfax, including tractors and machinery, highlights an active pipeline for mechanization upgrades and service models such as custom hire, contract farming, and cooperative equipment pools. Overall, these initiatives support a shift toward crops and systems with higher economic water productivity, notably greenhouse horticulture and export-oriented quality chains, while still requiring storage and import-handling capacity for structurally deficit staples such as wheat.

Recent Industry Developments

- June 2026: RoboCare raised a six-figure funding round from 216 Capital to expand its precision agriculture offering across Africa and the Middle East. The financing supports scaling of field-deployable monitoring and decision tools that align with Tunisia's push toward more data-driven irrigation and input use under water constraints.

- May 2026: Wafra Agricole, an Italian-Tunisian joint venture in Beja governorate, inaugurated production on about 200 hectares using computerized, solar-based irrigation and sustainable farming techniques. This adds a reference site for technology-forward field operations and reinforces investment models that combine local land access with modern irrigation and farm management practices.

- May 2024: The Multilateral Investment Guarantee Agency backed two 50 MW solar photovoltaic plants in Sidi Bouzid and Tozeur linked to new produce warehousing, lowering electricity costs and enabling cold storage at smaller break-even volumes. This support improved the economics of post-harvest infrastructure in interior and southern production zones, where power costs can constrain cold-chain expansion.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the agriculture market in Tunisia is treated as the annual value created from crops and livestock produced within the country, measured at first-sale prices and converted into USD for comparability.

Scope exclusions: Fisheries, aquaculture, and downstream food manufacturing are not counted in this market value.

Segmentation Overview

- By Commodity Type

- Grains and Cereals

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Pulses and Oilseed

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Fruits and Vegetables

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Cash Crop

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Grains and Cereals

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean fact base on Tunisia agriculture outputs and trade signals, so the later model inputs are anchored to observable series rather than assumptions. Public references used include sources such as FAOSTAT, the World Bank (agriculture value added), UN Comtrade for import and export flows, USDA FAS production and trade notes, and official statistics and releases from Tunisia agriculture bodies.

Alongside these, we review company filings and investor presentations where relevant, plus association websites and reputable press coverage to understand price movements, crop calendars, and policy changes that affect farm-gate economics. A paid subscription for company financials and intelligence is also used selectively to cross-check participant mix and to avoid missing major operators in the country. These examples are not exhaustive, and many other sources were also reviewed to collect data, validate it, and clarify open questions.

Primary Interviews and Surveys

Primary work is used to pressure-test desk assumptions on what is actually sold at first-sale prices, and how trade flows and water constraints show up in realized yields and prices. We speak with a mix of producers, exporters, input distributors, processors close to the farm gate, and sector specialists across Tunisia, and then we reconcile differences in their views before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | APAC: 42% |

| Mid tier: 53% | Functional/Unit leaders: 36% | EMEA: 31% |

| Smaller Players: 16% | Managers: 50% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach that reconstructs Tunisia agriculture value from national output indicators and price series, and then aligns it with trade and consumption signals where they materially shift local pricing. Once the first model total is produced, we corroborate it with selective bottom-up approximations, such as sampled crop value equals volume times an average first-sale price, and spot checks against supplier and channel feedback, so totals can be corrected when a category is overstated or understated.

Key inputs typically include harvested area and yield patterns for major crops, livestock headcount and production cycles, farm-gate price movements, import dependence for staples such as grains, and export realizations for products like olive oil and dates. When the data is patchy for smaller categories, gaps are handled by using stable ratios to better-reported aggregates and then validating those ratios through interviews. Forecasts are generated using scenario analysis, where weather sensitivity, irrigation adoption, and policy and trade conditions are adjusted with what market participants see as most likely, and then a final outlook is chosen after cross-checks with observed constraints.

Data Validation & Update Cycle

Validation is done by checking the output against independent signals, including agriculture value added trends, trade values, and price direction consistency, so the result does not drift away from what the country-level data implies. Outliers are flagged, investigated, and either corrected or explained, and then a second analyst review is completed before sign-off.

Reports are refreshed annually, and interim updates are triggered when material events occur, such as major policy shifts, a sharp currency move affecting USD conversion, or a large production shock. Before delivery, we perform a final review pass to make sure the latest public releases and interview learnings are reflected in the numbers.

Mordor Intelligence's Tunisia Agriculture Market Size Compared With Other Published Estimates

It is normal to see different market values published for Tunisia agriculture because groups do not always count the same activities, and they may also use different price points and year conversions. Differences can also come from whether the estimate is tied to production value at the first sale, or whether it blends in additional value chain activities.

The main spread here comes from whether the market is treated as crops plus livestock at farm gate prices, with constant-dollar handling, or whether distribution channels and downstream processing are mixed into the value, and it also depends on how often price and trade assumptions are refreshed in-country, which is where our approach stays closer to first-sale value accounting and constant 2024 USD conversion, a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.02 B (2025) | |

| Regional Consultancy A | USD 1.00 B (2025) | Appears to use a narrower commercial-market lens and may exclude subsistence and informal first-sale volumes, which can understate crop and livestock value when compared with a production-value construct. |

| Trade Journal B | USD 3.20 B (2025) | Uses a rounded country total with limited detail on pricing basis, currency timing, and whether values are constant or current USD, which can shift the figure when inflation and FX moves are significant. |

Across the three figures, the direction of the gap points back to scope and pricing mechanics rather than a single data point. By keeping the model tied to observable production volumes, first-sale price logic, and consistent USD normalization, the final estimate stays traceable and easier to reproduce when assumptions need to be revisited.

Key Questions Answered in the Report

What is the current size of the Tunisia agriculture market?

The Tunisia agriculture market reached USD 3.21 billion in 2026 and is projected to rise to USD 4.48 billion by 2031.

Which commodity group grows the fastest and at what rate?

Fruits and vegetables lead growth, advancing at a 6.80% CAGR through 2031 on the back of greenhouse expansion and off-season demand in Europe.

Which commodity holds the largest share and what is its growth outlook?

Cereals and grains account for 45% of market value in 2025 and expand at a 3.00% CAGR through 2031.

Where are geothermal greenhouses concentrated?

Kebili, Tozeur, and Gabes use underground heat and solar power to grow winter tomatoes and peppers.

Page last updated on: