Glucose Market Size and Share

Market Overview

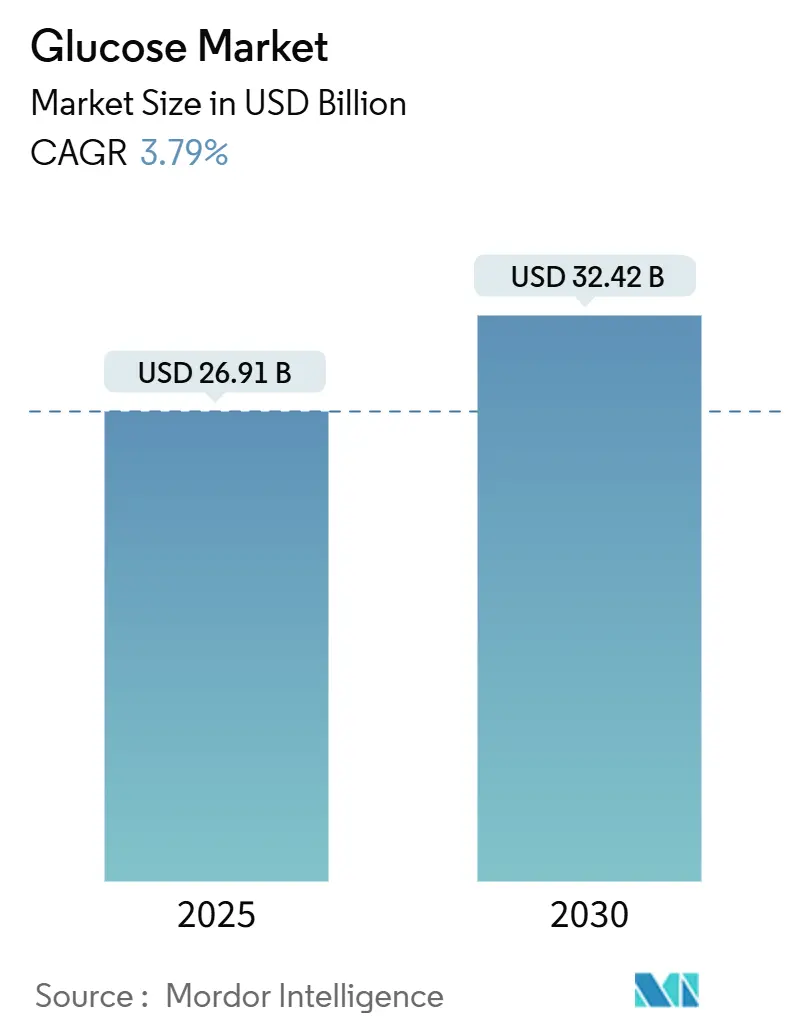

| Study Period | 2020 - 2030 |

| Market Size (2025) | USD 26.91 Billion |

| Market Size (2030) | USD 32.42 Billion |

| Growth Rate (2025 - 2030) | 3.79% CAGR |

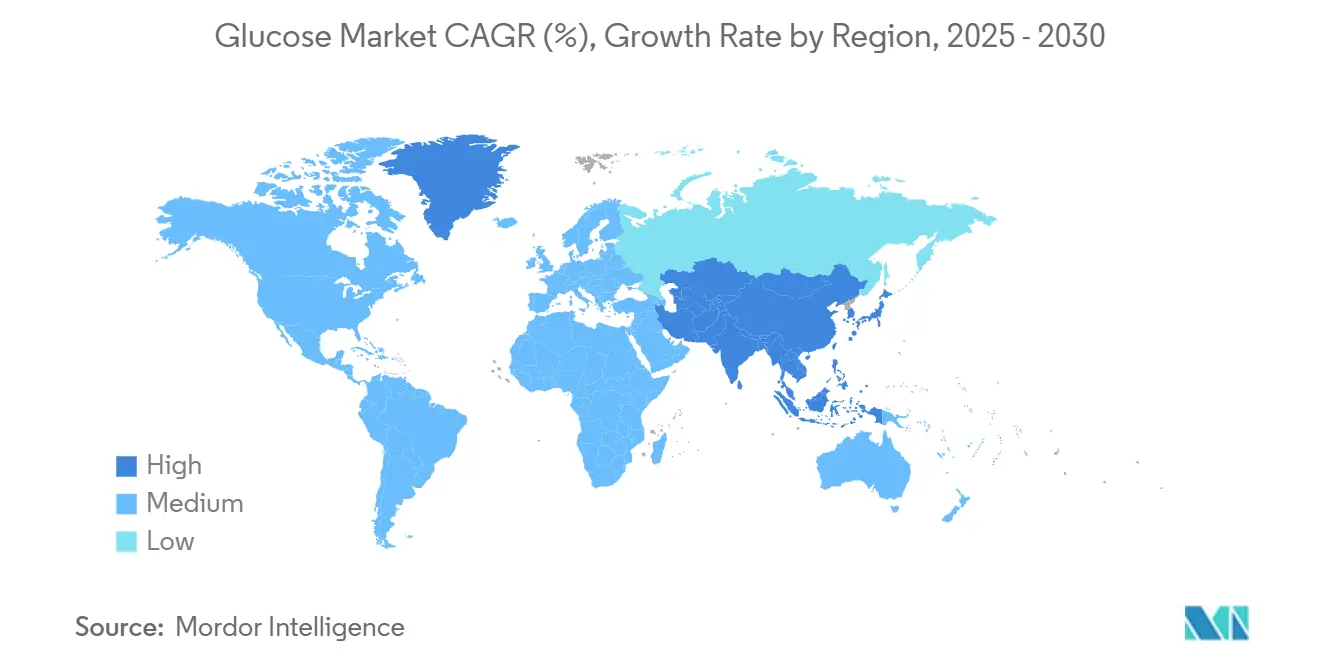

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Glucose Market Analysis by Mordor Intelligence

The glucose market value is estimated at USD 26.91 billion in 2025, with projections indicating growth to USD 32.42 billion by 2030, registering a CAGR of 3.79%. Glucose, a pivotal component of the glucose market, is widely used as a sweetener in various products, including baked goods, dairy items, and confections, offering 60-70% of sucrose's sweetness. In confectionery applications, glucose enhances fruity flavors, provides a cooling sensation, and balances sweetness. Additionally, glucose is utilized in beverages, ice creams, culinary dishes, meat curing processes, and pharmaceuticals. In milk-based beverages, such as chocolate and flavored drinks, glucose helps regulate sweetness when combined with other sugars. The food and beverage segment's glucose usage is increasing due to changing food habits and growing preference for snacks and desserts. Market growth is driven by rising demand for convenience foods and versatile sweeteners that offer health benefits across confectionery, bakery, and dairy sectors. However, the market faces challenges from fluctuating corn prices, supply chain disruptions, and economic changes. Global glucose producers are exploring wheat and cooked starch as sustainable alternatives for producing glucose syrups used in baked goods, beverages, and ice creams. The industry is experiencing increased demand for clean-label solutions, creating opportunities for glucose manufacturers, while companies are enhancing their portfolios through technology-supported product innovation.

Key Report Takeaways

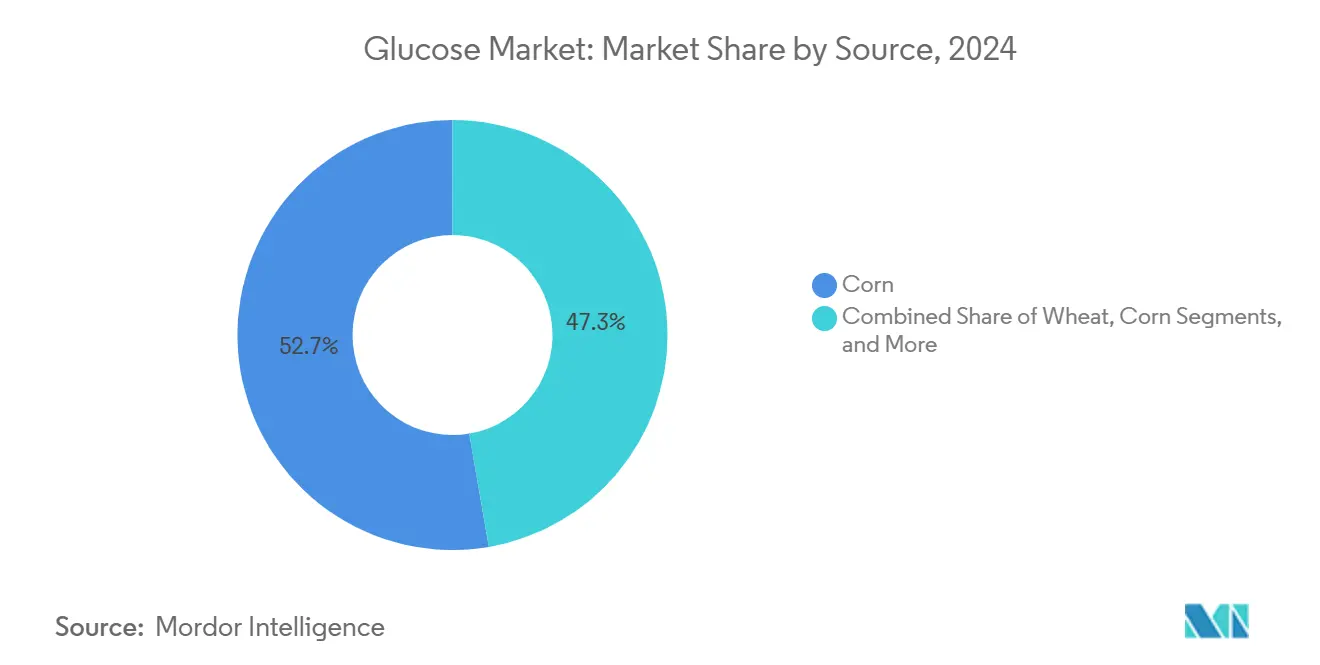

- By source, corn led with 52.7% of glucose market share in 2024 and is forecast to post a 3.2% CAGR through 2030, whereas wheat is set to grow fastest at a 5.15% CAGR.

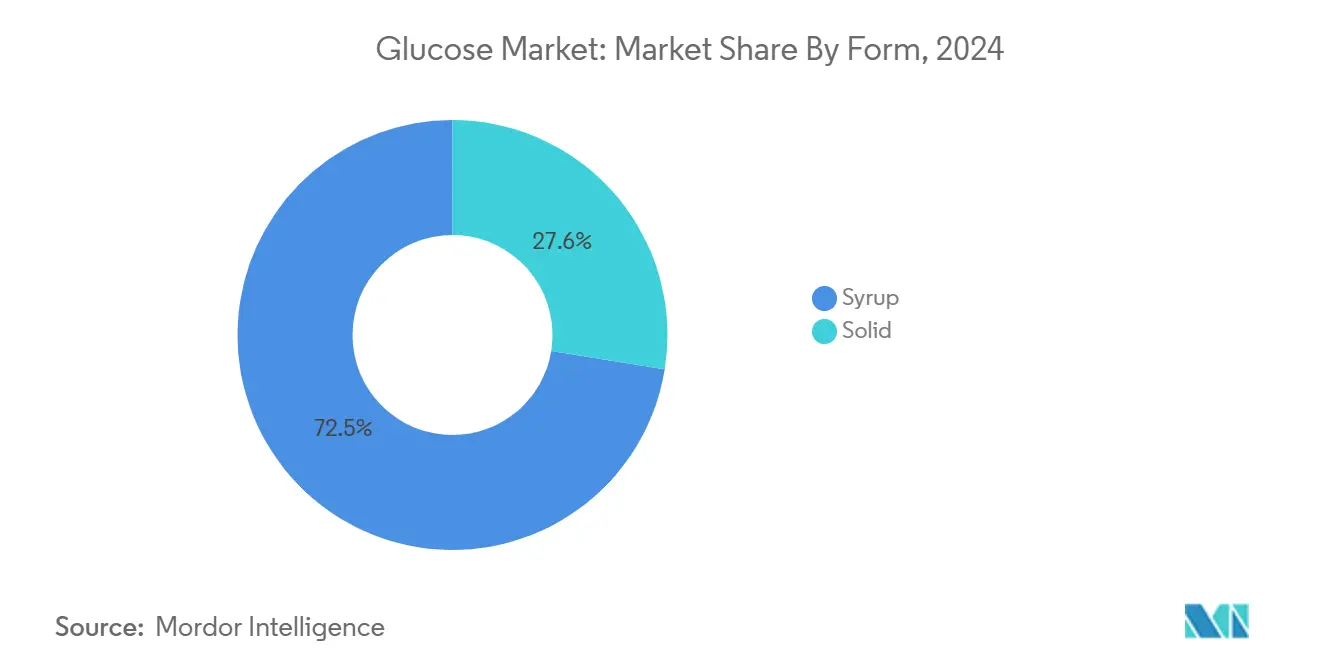

- By form, syrup held 72.45% of revenue in 2024; solid glucose is projected to expand at a 4.98% CAGR to 2030.

- By grade, food-grade commanded 61.15% of revenue in 2024; pharmaceutical-grade is anticipated to rise at a 5.69% CAGR.

- By application, food and beverage retained 56.15% share in 2024, yet personal care and cosmetics are expected to log a 5.45% CAGR.

- By region, North America accounted for 38.15% of 2024 revenue; Asia-Pacific is on track for the fastest 5.15% CAGR to 2030.

Global Glucose Market Trends and Insights

Driver Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for natural food sweeteners | +0.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Surging demand for convenience and processed foods | +0.9% | Asia-Pacific core, spill-over to Latin America | Short term (≤ 2 years) |

| Increasing adoption of glucose-based medical solutions | +1.2% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expanding use of glucose in fermentative bioplastic production | +0.4% | Global, with early adoption in Europe & North America | Long term (≥ 4 years) |

| Growth in sports and energy nutrition products | +0.3% | North America & Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Rising incorporation of glucose in infant and pediatric formulas | +0.5% | Global, with regulatory focus in developed markets | Medium term (2-4 years) |

Source: Mordor Intelligence

Growing Demand for Natural Food Sweeteners

The glucose market is experiencing significant expansion as food processors increasingly replace synthetic additives with glucose that complies with FDA GRAS (Generally Recognized as Safe) status [1]U.S. Food and Drug Administration, “Generally Recognized as Safe (GRAS),” fda.gov. According to the International Food Information Council (IFIC) Food & Health Survey published in 2024, approximately 43% of American consumers prefer natural sources of sweetness. [2]IFIC Food & Health Survey, “The International Food Information Council’s annual survey of American consumers,” foodinsight.org, indicating robust market growth and strong consumer preferences for natural alternatives. Green Plains' Clean Sugar Technology enables low-carbon production methods, demonstrating the compatibility between sustainability and functionality in modern glucose manufacturing processes. Suppliers who can verify renewable energy usage in production gain substantial competitive advantages as retailers implement stricter environmental certification requirements across their supply chains. The premium segment has evolved beyond traditional quality metrics, now emphasizing both superior product quality and verified environmental performance, reflecting a broader industry transformation toward sustainable practices.

Surging Demand for Convenience and Processed Foods

The shift toward urban lifestyles in the Asia-Pacific region maintains high production capacity in bakery, beverage, and ready-meal manufacturing facilities, where liquid glucose is essential for moisture retention and browning control. The rapid urbanization across major economies like China, India, and Southeast Asian countries has transformed traditional food consumption patterns, driving increased demand for processed and convenience foods. Chinese food processors import significant quantities of corn-based ingredients from the United States due to consistent supply quality and established trade relationships. Food manufacturers prefer glucose as it provides multiple functions - sweetness, fermentation support, and texture enhancement - through a single ingredient, reducing procurement complexity and operational costs. The growth of e-commerce platforms increases packaged food production, with major online retailers expanding their food delivery services and digital grocery segments. This digital transformation ensures steady demand growth even during periods of reduced consumer spending, as consumers increasingly rely on packaged food products for convenience and longer shelf life.

Increasing Adoption of Glucose-Based Medical Solutions

The pharmaceutical-grade glucose market has experienced higher demand compared to other segments, driven by the expansion of GLP-1 drug manufacturing capacity. Eli Lilly's USD 3 billion investment in peptide therapeutic production in December 2024 established a new premium baseline for glucose suppliers in the pharmaceutical industry. The global prevalence of diabetes, affecting 10% of adults worldwide, provides manufacturers with long-term volume visibility. This market stability encourages processors to invest in GMP-compliant production lines, which offer higher margins than food-grade glucose production. The pharmaceutical glucose market is evolving as manufacturers upgrade their facilities to meet strict quality requirements and increased demand from pharmaceutical companies.

Expanding Use of Glucose in Fermentative Bioplastic Production

Biotechnology advances enable sustainable plastic production from glucose, addressing environmental concerns while creating new opportunities for glucose producers. Research demonstrates glucose's applications in producing biobased polyethylene terephthalate (PET) and other bioplastics, though production costs currently affect economic viability. In November 2024, Solugen and ADM partnered to establish a biomanufacturing facility that uses ADM-sourced dextrose to produce low-carbon organic acids, with a capacity of 120 kilotonnes per year. Their fermentation process reduces carbon emissions compared to traditional chemical manufacturing, aligning with corporate sustainability initiatives and increasing environmental regulations. Integrated biorefineries using both first and second-generation feedstocks can enhance profitability and optimize glucose utilization across multiple product streams. This development represents glucose's evolution from a food ingredient to an essential chemical in sustainable material manufacturing.

Raw Material Price Volatility

Corn and wheat prices significantly influence the majority of glucose production costs. The Russia-Ukraine conflict severely disrupted grain exports, leading to substantial constraints in spot market supplies. The World Bank anticipates a decrease in overall crop prices in 2025 but indicates persistent price volatility in agricultural commodities [3]World Bank, “Commodity Markets Outlook,” worldbank.org. ADM's financial reports demonstrate considerable margin pressures in its Carbohydrate Solutions segment, primarily attributed to fluctuating raw material costs in the global markets. In response to these challenges, processors are implementing strategic measures, including the extension of forward-purchase agreements and incorporation of alternative feedstocks such as wheat and cassava. While these adaptations help manage market uncertainties, they only partially mitigate the ongoing price risks faced by industry participants.

Availability of Alternative Sweeteners

Natural sweeteners such as allulose, tagatose, and stevia are capturing increased market share due to their low-calorie properties and minimal impact on blood sugar levels. Consumer demand for healthier alternatives has established these sweeteners as essential ingredients in food and beverage manufacturing. South Korean manufacturers are expanding their allulose production capabilities, supported by government incentives and favorable regulations. Roquette and Bonumose are deploying new technologies in July 2024 to enhance tagatose production efficiency, enabling price competition with glucose in premium confectionery segments. The increasing demand for reduced-sugar products has reshaped the sweetener market. Glucose manufacturers have adapted by highlighting their products' natural origin, sustainable sourcing, and diverse applications across food categories, moving beyond price-based competition.

Segment Analysis

By Source: Corn Dominance Faces Wheat Innovation

Corn-based glucose represented a 52.7% market share in 2024 and projected a 3.2% CAGR to 2030. Integrated U.S. wet-milling complexes give processors structural cost benefits, including rail access and ethanol coproduct credits. ADM alone grinds millions of bushels annually, reinforcing supply reliability that beverage and confectionery majors value. Yet climate-driven yield variability and biofuel policy swings inject volatility, motivating contingency strategies.

Wheat-derived glucose grows at 5.15% CAGR as European and Asian processors hedge against corn price risk and leverage regional grain surpluses. EU starch plants re-tool lines for dual-feed capability, ensuring continuity if Black Sea logistics tighten again. Potato and cassava occupy niche but profitable corners where allergen-free labeling or tropical agronomy offer localized advantage. Clean Sugar Technology highlights how feedstock choice can dovetail with carbon-reduction branding, positioning glucose producers for scope-3 audits demanded by global CPG buyers.

Note: Segment shares of all individual segments available upon report purchase

By Form: Syrup Leadership Challenged by Solid Growth

The Syrup segment accounted 72.45% revenue share in 2024 owing to industrial pipelines built for liquid handling in beverage, bakery, and canning facilities. The glucose market benefits from syrup’s immediate miscibility, color-control attributes, and lower capital outlay versus crystallization. Automated dosage pumps and closed tanks also reduce microbial risks in continuous lines, a key in high-throughput snack plants.

Solid formats are estimated to register a 4.98% CAGR, attracting pharmaceutical, sports nutrition, and premium bakery users who prize precise gram dosing and extended shelf life. Pharmaceutical cleanrooms rely on crystalline glucose for injectable diluents, demanding microbial counts near zero. Energy-gel and supplement brands prefer agglomerated powders that dissolve rapidly yet resist caking in humid climates. Finer-mesh grades also enable 3D-printed food substrates, widening application innovation and pulling incremental volumes away from liquids.

Note: Segment shares of all individual segments available upon report purchase

By Grade: Food-Grade Stability Meets Pharmaceutical Premium

Food-grade streams delivered 61.15% of 2024 sales, underpinned by global GMP and Codex compliance that secures multi-country label acceptance. Mass-market drinks, canned fruit, and frozen desserts all continue to draw high-five-figure-tonne contracts underpinning baseline glucose market demand.

In contrast, pharmaceutical-grade volumes are smaller but fetch prices up to 60% higher. The glucose market size for injectable-class material is projected to climb from USD 2.3 billion in 2025 to USD 3.1 billion by 2030 on a 5.69% CAGR. Certification under ICH-Q7 and USP protocols raises production costs, yet investments such as Novo Nordisk’s North Carolina plant lock in multi-year off-take agreements. Technical-grade outputs aimed at fermentation nutrients or concrete admixtures round out portfolios, allowing plants to shift streams depending on margin signals.

By Application: Food Dominance Faces Personal Care Disruption

Food and beverage kept 56.15% share in 2024, equivalent to USD 15.1 billion of the glucose market size, with a modest 3% forecast CAGR. Liquid syrups continue to anchor confectionery, breweries, and dairy mixers because sucrose substitution lowers crystallization risk. However, lower-sugar positioning among premium brands caps volume upside, nudging processors to court adjacent categories.

Personal care rises at a 5.45% CAGR as formulators leverage glucose as a humectant and fermentation substrate for skin microbiome products. Japanese and Korean beauty routines spotlight naturally sourced moisturizers, translating into double-digit growth for glucose esters in serums. Pharmaceutical use, already analyzed, accelerates further as injectables and oral rehydration solutions expand across emerging markets. Animal nutrition and bioplastic feedstock segments round out demand, each buffered from dietary sugar substitution cycles.

Geography Analysis

North America held 38.15% market share in 2024 on the strength of an integrated corn belt, deep chemical processing expertise, and a robust pharmaceutical value chain. ADM, Cargill, and Ingredion concentrate starch-milling assets near Midwestern grain origination then ship syrups by rail to coastal bottlers. The region also hosts the largest cluster of GLP-1 drug facilities, guaranteeing steady draw for USP-grade glucose even when snack-food reformulation slows. Regulatory familiarity with FDA and USP codes lowers compliance friction, sustaining export competitiveness into Latin America.

Asia-Pacific records the fastest 5.15% CAGR to 2030 as China, India, and Southeast Asia urbanize. Expanded cold-chain and modern retail spur packaged-food penetration, while domestic starch processors scale to replace imports. Chinese mills integrate corn, wheat, and cassava to smooth feedstock costs, and local governments subsidize downstream candy exports that hinge on glucose inputs. Rising chronic disease incidence likewise fuels pharmaceutical-grade penetration, with multinationals building fill-finish sites inside the region to shorten supply lines.

Europe’s glucose market matures yet remains opportunity-rich in premium niches. Consumer aversion to artificial sweeteners channels demand toward grain-sourced syrups, while decarbonization policy amplifies interest in glucose-to-bioplastic ventures. Central European plants process both corn and wheat, mitigating Black Sea supply risks and keeping duty-free access within the Single Market. South America and Middle East & Africa stay emergent, but bakery and beverage investments in Brazil, Egypt, and Nigeria signal rising baseline demand once macro headwinds stabilize.

Competitive Landscape

The glucose market features moderate fragmentation, with multinational corporations competing against regional processors and emerging technology companies focused on sustainable production methods. Market concentration varies by geography and application. North America and Europe exhibit higher consolidation, dominated by major players like ADM, Cargill, and Ingredion. In contrast, the Asia-Pacific region remains more fragmented, with numerous local and regional processors serving domestic food industries. Pharmaceutical applications drive competitive intensity by creating premium pricing opportunities, attracting new entrants, and prompting capacity expansions from existing players.

The market demonstrates key strategic trends focused on vertical integration, sustainability initiatives, and application diversification as companies seek competitive advantages beyond cost leadership. Tate & Lyle's USD 1.8 billion acquisition of CP Kelco in November 2024 exemplifies this trend through consolidation that combines glucose production capabilities with specialty ingredients for comprehensive sweetening solutions. Companies such as Green Plains emphasize technological advancement, implementing Clean Sugar Technology to enhance production efficiency and achieve low-carbon glucose production.

White-space opportunities are emerging in pharmaceutical applications, bioplastics production, and personal care formulations, where glucose's natural origin and functional properties offer differentiation potential. Biotechnology companies are disrupting the market with fermentation-based production methods, while specialty processors are targeting niche applications with premium pricing structures. These developments underscore the evolving competitive landscape and the growing emphasis on innovation and sustainability within the glucose market.

Glucose Industry Leaders

-

Cargill, Incorporated.

-

Tereos S.A.

-

Wilmar International Limited

-

Louis Dreyfus Holding B.V.

-

Archer Daniels Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Tate & Lyle completed USD 1.8 billion acquisition of CP Kelco to create leading global specialty food and beverage solutions business, enhancing capabilities in sweetening, mouthfeel, and fortification applications.

- July 2024: Roquette partnered with Bonumose to enhance scalability of tagatose production, a low-glycemic sugar alternative that competes with traditional glucose applications in health-conscious consumer segments.

- April 2024: Solugen broke ground on biomanufacturing facility in Marshall, Minnesota, partnering with ADM to utilize dextrose for sustainable organic acid production with capacity reaching 120 kilotonnes per annum and creating over 50 high-skill jobs.

Global Glucose Market Report Scope

Glucose (dextrose) is a kind of sugar derived from natural sources like wheat, corn, and other sources.

The glucose (dextrose) market is segmented by source, application, and geography. Based on source, the market is segmented by wheat, corn, and other sources. By application, the market is segmented into food and beverage, pharmaceutical, and other applications. The food and beverage segment of the market is further segmented into bakery and confectionery, snacks and cereals, beverages, and dairy products. The study also covers the global level analysis of the major regions such as North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value in (USD million).

| By Source | Corn | ||

| Wheat | |||

| Potato | |||

| Cassava | |||

| Others | |||

| By Form | Syrup | ||

| Solid | |||

| By Grade | Food-Grade | ||

| Pharmaceutical-Grade | |||

| Others | |||

| By Application | Food and Beverage | Bakery and Confectionery | |

| Snacks and Cereals | |||

| Beverages | |||

| Dairy and Frozen Desserts | |||

| Others Food and Beverages | |||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Animal Feed | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Rest of Middle East and Africa | |||

| Corn |

| Wheat |

| Potato |

| Cassava |

| Others |

| Syrup |

| Solid |

| Food-Grade |

| Pharmaceutical-Grade |

| Others |

| Food and Beverage | Bakery and Confectionery |

| Snacks and Cereals | |

| Beverages | |

| Dairy and Frozen Desserts | |

| Others Food and Beverages | |

| Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Animal Feed | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current value of the glucose market?

The glucose market is valued at USD 26.91 billion in 2025 and is projected to reach USD 32.42 billion by 2030.

Which glucose source accounts for the largest revenue share?

Corn-based glucose leads with 52.7% of 2024 revenue, supported by mature processing infrastructure in North America.

Which source is growing fastest?

Wheat-derived glucose is forecast to expand at a 5.15% CAGR between 2025 and 2030 due to diversification and regional crop availability.

How dominant is syrup compared with solid glucose?

Syrup captured 72.45% of 2024 sales, while solid formats are expected to grow at a 4.98% CAGR as pharmaceutical and sports nutrition demand rises.

Page last updated on: June 30, 2025