Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

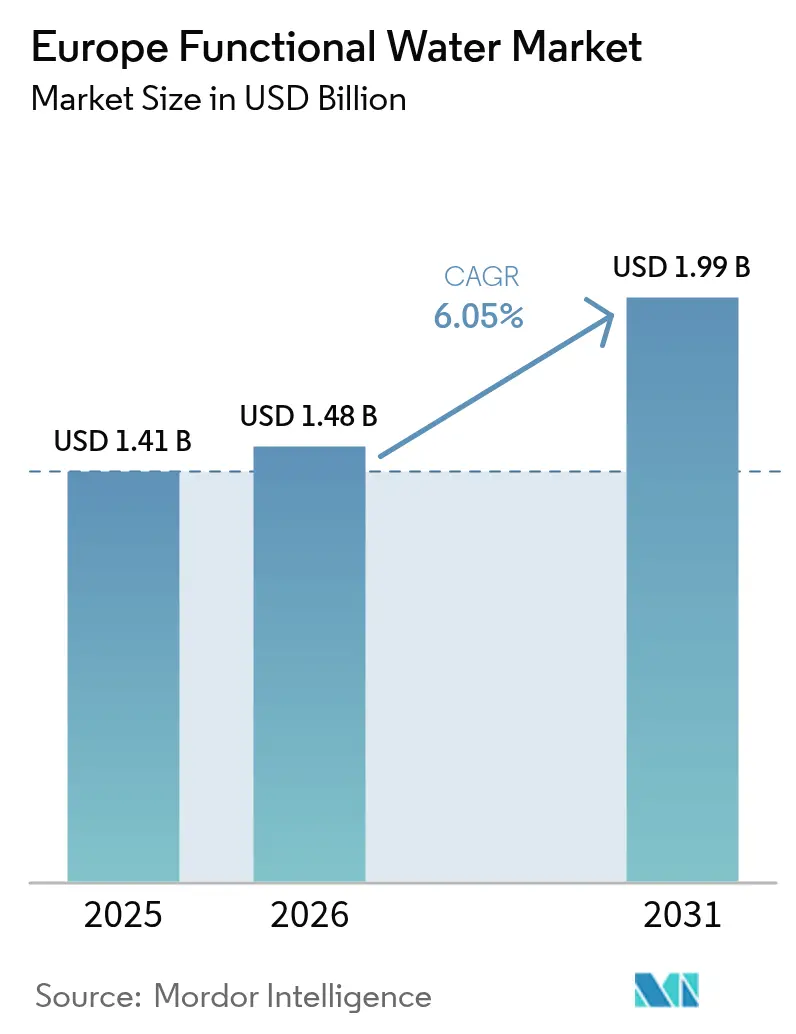

| Base Year Market Size (2025) | USD 1.41 Billion |

| Market Size (2026) | USD 1.48 Billion |

| Market Size (2031) | USD 1.99 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

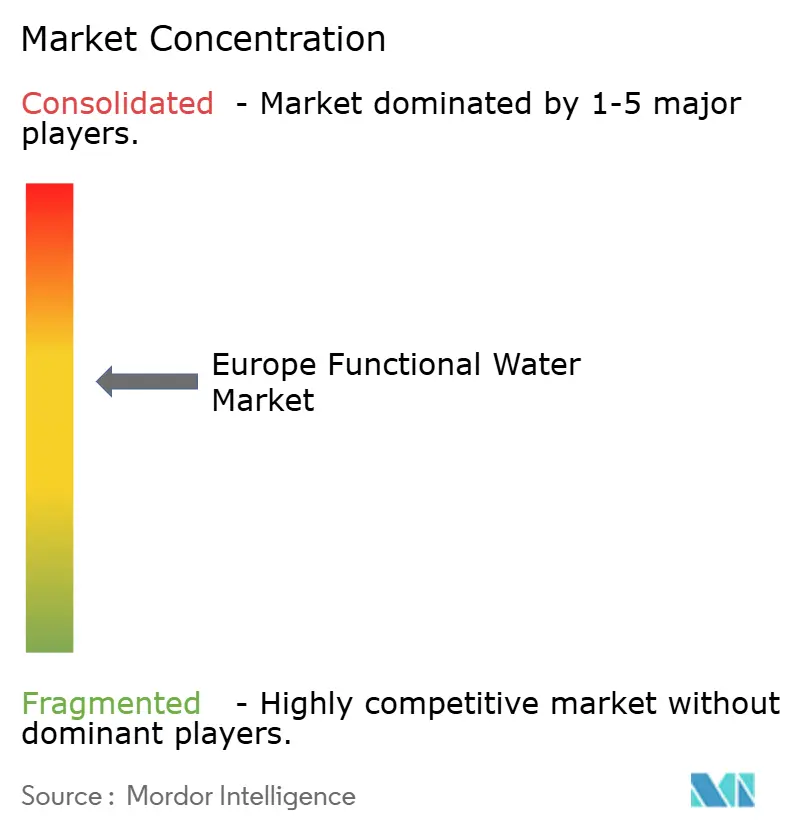

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Functional Water Market Analysis by Mordor Intelligence

The Europe Functional Water Market size is projected to expand from USD 1.41 billion in 2025 and USD 1.48 billion in 2026 to USD 1.99 billion by 2031, registering a CAGR of 6.05% between 2026 to 2031. The demand for functional water in Europe is increasing as consumers increasingly view hydration as a way to support daily wellness, enhanced with vitamins, electrolytes, or plant-based ingredients. Factors such as higher disposable incomes, the convenience of online shopping, and sustainability requirements are driving a preference for premium, clean-label products. Retailers are dedicating more shelf space to functional stock-keeping units, while private equity interest in the category is encouraging brand consolidation. Additionally, packaging trends are evolving, with aluminum cans gaining popularity due to their recyclability, and the growth of online grocery platforms is providing direct-to-consumer brands with cost-effective access to health-conscious consumers.

Key Report Takeaways

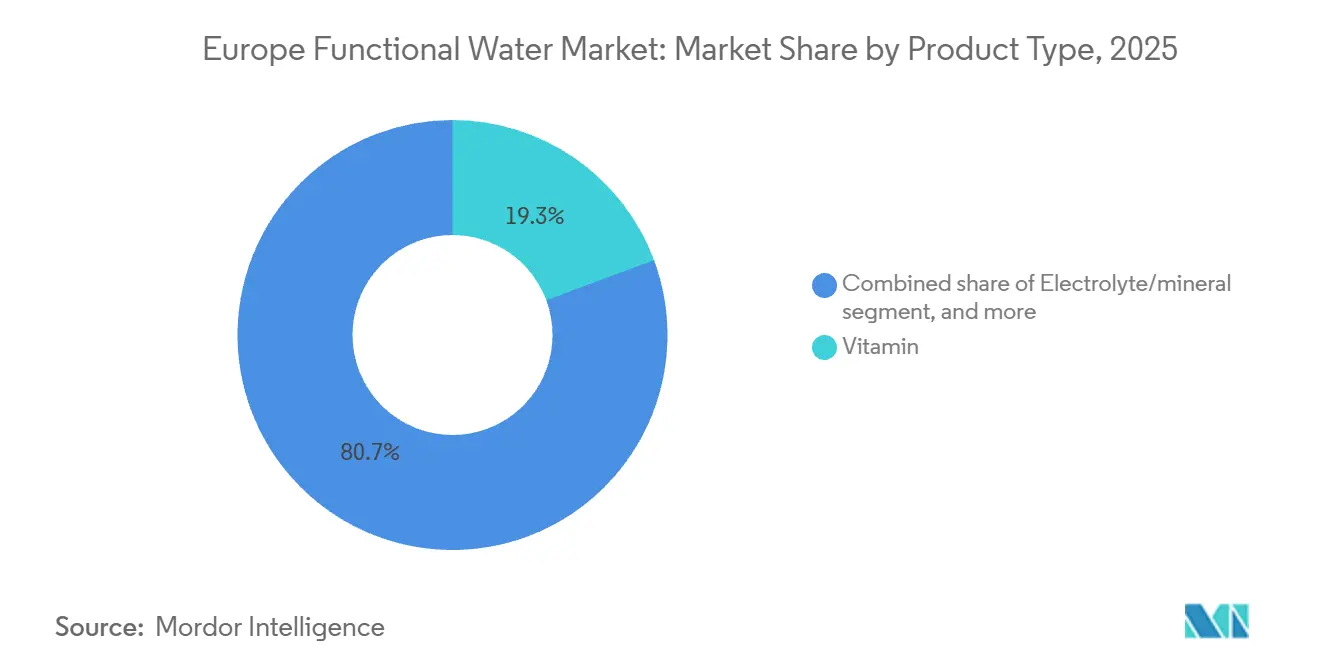

- By product type, vitamin-fortified water held 19.34% of Europe functional water market share in 2025, while electrolyte and mineral variants are forecast to expand at an 8.58% CAGR through 2031.

- By packaging type, PET bottles accounted for 86.39% of the Europe functional water market size in 2025; cans record the fastest projected growth at 9.42% CAGR to 2031.

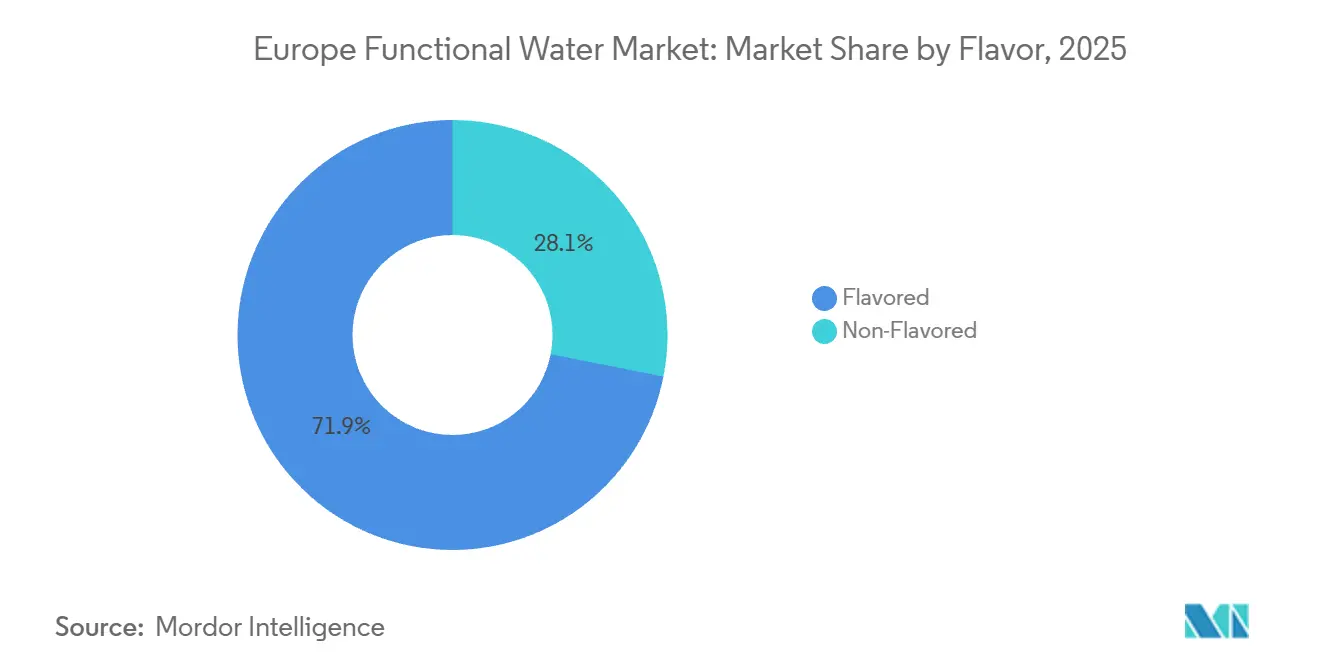

- By flavor, flavored formulations captured 71.91% revenue in 2025, whereas non-flavored options are set to rise at a 7.39% CAGR during 2026-2031.

- By distribution channel, supermarkets and hypermarkets led with 42.32% share of the Europe functional water market size in 2025; online retail is advancing at an 8.08% CAGR through 2031.

- By geography, the United Kingdom contributed 22.62% revenue in 2025; Germany is the fastest-growing market with a 7.71% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Functional Water Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer focus on proactive health and wellness maintenance | +1.2% | Global, with strongest uptake in United Kingdom, Germany, Nordics | Medium term (2-4 years) |

| Increasing demand for clean-label beverages with natural ingredients | +1.0% | Western Europe (United Kingdom, France, Germany, Netherlands), spreading to Southern Europe | Medium term (2-4 years) |

| Shift towards plant-based and organic functional beverages | +0.8% | Nordics, Germany, United Kingdom, Netherlands; emerging in France, Spain | Long term (≥ 4 years) |

| Aging population driving demand for preventive wellness beverages | +0.9% | Germany, Italy, France, Spain; moderate in United Kingdom | Long term (≥ 4 years) |

| Premiumization trend favoring high-quality natural ingredients | +1.1% | United Kingdom, Germany, France, Benelux; selective uptake in Southern Europe | Medium term (2-4 years) |

| Continuous innovation in new flavors, formats, and functional ingredients | +1.0% | Global, led by United Kingdom, Germany, France product launches | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising consumer focus on proactive health and wellness maintenance

European consumers are increasingly viewing hydration as a preventive health measure rather than merely a response to thirst. Many shoppers actively read ingredient labels and are willing to pay premiums for natural formulations. This shift is particularly evident among younger consumers, with a growing number expressing intent to purchase healthier products. Additionally, many consumers are prepared to pay higher prices for products offering functional benefits. The NU-AGE study, a multi-center European trial, has shown that tailored nutrition interventions can reduce inflammaging in older adults, providing clinical support for fortified beverages aimed at improving bone health, immune function, and cognitive performance [1]Source: World Health Organization, “Ageing and Health,” who.int. Brands are leveraging this evidence by promoting electrolyte and vitamin waters as part of daily wellness routines rather than as solutions for emergency rehydration. For example, Highland Spring's April launch of sugar-free, high fat, sugar, and salt (HFSS)-compliant flavored waters in Tesco highlights this approach, positioning the flavored still water category as complementary to plain water rather than as a substitute. This trend underscores the transition of functional water from niche sports nutrition to a mainstream grocery staple, becoming a regular wellness purchase for consumers.

Increasing demand for clean-label beverages with natural ingredients

Clean-label mandates are influencing formulation priorities across Europe, driven by consumer skepticism toward synthetic additives and increased regulatory scrutiny of health claims. The European Food Safety Authority's Regulation 1924/2006 mandates that all nutrition and health claims be scientifically validated and included in the Community Register, creating a compliance framework that emphasizes ingredient transparency [2]Source: European Food Safety Authority, “Nutrition,” efsa.europa.eu. Stevia, approved as E960, and erythritol, approved as E968, have emerged as common natural sweeteners; however, both present sensory challenges. Stevia's bitter aftertaste at higher concentrations requires flavor masking, while erythritol's laxative threshold limits its use in single-serve products. Vital Drinks, which secured funding to launch a zero-calorie, zero-sugar spring water range containing all vitamin groups, highlights the complexities of clean-label formulation. The brand uses British spring water and avoids artificial sweeteners, instead relying on natural fruit essences to enhance flavor. This approach results in a retail price that is significantly higher than the cost of standard bottled water, reflecting the premium consumers place on ingredient transparency. For mid-tier brands, the challenge lies in achieving taste parity with synthetic formulations while managing raw material costs that are higher. This cost pressure is driving increased consolidation and vertical integration within the market.

Shift towards plant-based and organic functional beverages

Plant-based fortification is becoming a key differentiator, particularly in regions with significant vegan and flexitarian populations, such as Germany, the Nordics, and the Netherlands. A peer-reviewed study on plant-protein microencapsulation for vitamin D delivery highlighted that pea and rice protein matrices can stabilize lipophilic vitamins in aqueous solutions, enabling fortification without the need for synthetic emulsifiers or preservatives. This development addresses a long-standing formulation challenge that has limited plant-based functional waters to water-soluble vitamins like B-complex and C. Arla Foods' advancements in whey protein solutions for functional beverages have set industry standards for protein water clarity and mouthfeel. However, dairy-free alternatives are gaining momentum as consumers increasingly prioritize wellness claims aligned with sustainability values. QNT Life Protein Water, introduced with protein per can, utilizes hydrolyzed collagen instead of plant protein, indicating that taste and solubility remain significant challenges for fully plant-based formulations in the protein water category. Organic certification adds further complexity and cost, requiring full traceability from source water to packaging. However, it provides access to premium retail channels and health-food distributors. The organic bottled water segment in Europe is expected to grow at a faster rate than conventional formats, although absolute volumes remain limited due to the scarcity of certified spring sources and higher audit expenses.

Aging population driving demand for preventive wellness beverages

Europe's aging population is driving consistent demand for functional waters addressing age-related health concerns. According to the World Health Organization's 2024 report on aging and health in Europe, by 2030, one in four Europeans will be aged 60 or older, with chronic conditions such as osteoporosis, sarcopenia, and cognitive decline becoming increasingly common. Calcium and magnesium fortification supports bone density maintenance, while B-vitamins aid energy metabolism and neurological function. In March 2024, Gerolsteiner launched Gerolsteiner Ursprung, a highly mineralized water containing 590 milligrams per liter of calcium and 167 milligrams per liter of magnesium. This composition meets 74% of daily calcium and 59% of daily magnesium requirements as per EU Regulation 1169/2011, positioning the product as a functional food rather than a standard beverage. With a total mineralization of 4,441 milligrams per liter and a unique volcanic carbonation narrative, the product differentiates itself from tap water and conventional bottled options, supporting its premium pricing in 1-liter returnable glass bottles. Aging consumers prioritize efficacy and product provenance over flavor variety, creating opportunities for mineral-rich, lightly flavored formats that emphasize functional benefits over sensory appeal. This contrasts with younger demographics, who prefer bold flavors and convenient formats, highlighting the need for age-segmented SKU strategies to build successful product portfolios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory requirements for health claim labeling | -0.7% | EU-wide, particularly stringent in Germany, France, Netherlands | Medium term (2-4 years) |

| Formulation difficulties with natural flavor enhancers and sweeteners | -0.5% | Global, acute in markets with high clean-label expectations (United Kingdom, Germany, Nordics) | Short term (≤ 2 years) |

| Elevated production costs for innovative and natural ingredients | -0.6% | Western Europe (high labor, energy costs); moderate in Southern/Eastern Europe | Medium term (2-4 years) |

| Complex regulatory landscape for ingredient approvals and labeling | -0.4% | EU-wide, fragmented enforcement across member states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent regulatory requirements for health claim labeling

The European Food Safety Authority's (EFSA) health-claims framework under Regulation 1924/2006 places a significant substantiation burden on smaller brands, giving multinational corporations with dedicated regulatory teams and clinical trial budgets a compliance advantage. Approved claims for vitamins and minerals are outlined in Regulation 432/2012, addressing functions such as energy metabolism, immune support, and bone health. However, any new claim requires the submission of a dossier, a scientific opinion, and authorization from the European Commission, a process that can take several years and involve substantial costs. Öko-Test's evaluation of electrolyte products sold in Germany revealed that none fully adhered to the Deutsche Gesellschaft für Ernährung's recommendations for optimal sports drinks. Many products exceeded recommended electrolyte concentrations or included unnecessary vitamins, leading to downgrades under Bundesinstitut für Risikobewertung's maximum intake guidelines. Products containing high sodium or magnesium levels received negative evaluations, highlighting the risks of over-fortification. Similarly, Verbraucherzentrale Nordrhein-Westfalen's market review of effervescent dietary supplements in Germany found that less than half of the products disclosed sodium content. Some supplements delivered significant amounts of salt per daily dose, equating to approximately 24% of the Deutsche Gesellschaft für Ernährung's maximum recommended intake and 30% of the World Health Organization's recommendation.

Formulation difficulties with natural flavor enhancers and sweeteners

Natural sweeteners approved under European Union regulations, such as stevia (E960) and erythritol (E968), present sensory and dosage challenges that complicate product development. Stevia's steviol glycosides offer sweetness hundreds of times more intense than sucrose but introduce a licorice-like bitterness at higher concentrations, requiring flavor masking with citrus or berry notes. Erythritol, a sugar alcohol, delivers 70% of sucrose's sweetness with minimal glycemic impact but produces a cooling mouthfeel and laxative effects at higher doses, limiting single-serve formats for an average adult. Öko-Test's 2025 review highlighted concerns regarding artificial sweeteners, including sucralose, acesulfame potassium, and aspartame, in electrolyte products due to potential long-term metabolic risks and environmental persistence. However, natural alternatives have yet to achieve comparable taste profiles. Vital Drinks' zero-sugar, zero-calorie formulation avoids sweeteners entirely, relying on natural fruit essences. While this approach eliminates artificial additives, it limits sweetness intensity, potentially reducing appeal among consumers accustomed to sweeter products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Electrolyte Variants Outpace Vitamin Waters

Vitamin-fortified water accounted for 19.34% of the Europe Functional Water Market in 2025, reflecting strong consumer recognition of B-complex and Vitamin C for energy and immune support. However, electrolyte and mineral formulations are projected to grow at a compound annual growth rate (CAGR) of 8.58% through 2031, marking the fastest growth rate among product types. This trend is driven by the mainstream adoption of sports nutrition and the repositioning of electrolytes as tools for daily wellness rather than solely for rehydration. For instance, Powerade Power Water, launched in October 2025, combines electrolytes with zero sugar, targeting gym-goers and active commuters who prefer low-calorie alternatives to traditional isotonic drinks. Similarly, Gerolsteiner Ursprung, introduced in March 2024, provides calcium and magnesium, meeting significant portions of daily requirements, and positioning itself as a functional food rather than a standard beverage.

Protein water, while a smaller segment, is experiencing rapid growth. The October 2025 United Kingdom launch of iPRO Protein Water features collagen protein per serving, aligning with hydration and beauty-from-within trends. Additionally, QNT Life Protein Water, introduced in September 2025, offers protein in cans, utilizing hydrolyzed collagen and natural sweeteners to address the chalkiness often associated with earlier protein water products.

By Packaging Type: Aluminum Cans Gain on Sustainability and Portability

PET bottles accounted for 86.39% of the Europe Functional Water Market packaging volume in 2025, supported by cost efficiency, transparency, and established supply chains. However, cans are expected to grow at a CAGR of 9.42% through 2031, driven by sustainability considerations and on-the-go convenience. Coca-Cola's April 2024 launch of smartwater in a canned format highlights this trend, leveraging aluminum's infinite recyclability and lower carbon footprint compared to virgin PET. Cans also offer premium positioning through tactile differentiation and enhanced shelf visibility, with brands like iPRO and QNT adopting 330-milliliter slim cans to convey modernity and functionality.

The European Union Packaging and Packaging Waste Regulation's mandate for 25% recycled content has increased recycled polyethylene terephthalate (rPET) prices to EUR 1,800 per tonne, compared to EUR 900 for virgin resin. This has narrowed the cost gap with aluminum, encouraging brands to adopt cans to avoid surcharges on virgin plastic. Danone's shift to 100% rPET for evian and Volvic from early 2025 reduced virgin plastic usage by 7,000 tonnes and carbon dioxide emissions by over 10,000 tonnes. However, the capital investment and supply chain complexities associated with rPET favor larger players, prompting smaller brands to consider cans as a more accessible sustainable alternative.

By Flavor: Non-Flavored Waters Gain as Clean-Label Purists Seek Simplicity

Flavored functional waters accounted for 71.91% of the Europe Functional Water Market in 2025, driven by consumer preference for taste variety and palatability. However, non-flavored options are projected to grow at a compound annual growth rate of 7.39% through 2031, reflecting a shift towards clean-label products and a backlash against natural and artificial flavorings. Highland Spring's April 2024 launch of Strawberry, Apple and Blackcurrant, and Lemon and Lime flavored waters in Tesco expanded the flavored still water category by 2.4% in volume and 10.7% in value during the 26 weeks ending February 2024, highlighting strong demand for familiar flavors. Similarly, Vitamin Well's United Kingdom debut in April 2023 introduced four flavored functional drinks, such as Elevate with pineapple and wild strawberry, and Reload with lemon and lime, each fortified with vitamins and minerals targeting immunity, skin health, and fatigue reduction. These launches emphasize the dominance of flavored variants in impulse purchases and trial occasions, where taste remains the primary purchase driver.

Non-flavored functional waters cater to a distinct consumer segment focused on ingredient minimalism and zero-additive formulations. This trend is particularly prominent in Germany, the Nordic countries, and the Netherlands, where clean-label expectations are highest. Gerolsteiner Ursprung exemplifies this approach with its natural volcanic carbonation and high mineral content, offering functional benefits without added flavoring. The brand leverages provenance storytelling and mineral density to support its premium pricing strategy.

By Distribution Channel: E-Commerce Disrupts Traditional Grocery Dominance

Supermarkets and hypermarkets are projected to account for 42.32% of the Europe Functional Water Market distribution in 2025, benefiting from extensive shelf space, promotional efforts, and opportunities to drive basket-building. However, online retail channels are expected to grow at a compound annual growth rate (CAGR) of 8.08% through 2031, marking the fastest growth among distribution channels. E-commerce penetration in United Kingdom food sales reached 13.1%, with online grocery channels growing at a rate above the European average. This growth is driven by subscription models, direct-to-consumer brands, and the acceleration of digital adoption during the pandemic [3]Source: EuroCommerce, “Retail Europe,” eurocommerce.eu. Vitamin Well's United Kingdom launch in April 2023 through WH Smith and Amazon highlights a dual-channel strategy that combines physical impulse purchase locations with online discovery and replenishment.

Similarly, Vital Drinks' February 2024 launch focused on direct-to-consumer and Amazon channels, enabling the company to retain margins and capture customer data to inform product development and marketing strategies. Convenience stores and other channels, including foodservice, gyms, and pharmacies, play niche roles in the market. These channels typically achieve higher per-unit margins but contribute lower absolute volumes. In the United Kingdom, the on-premise bottled water segment grew in 2024. This growth reflects the trend of premiumization in restaurants, cafes, and hotels.

Geography Analysis

In 2025, the United Kingdom accounted for 22.62% of the European Functional Water Market, driven by a health-conscious population, a strong e-commerce infrastructure, and a retail environment that fosters innovation. Highland Spring, supported by the popularity of sports-cap bottles and flavored options like Apple and Blackcurrant (which sold over 7 million liters), became the United Kingdom's leading bottled water brand in 2025, generating GBP 43.3 million from 37.8 million liters sold. The United Kingdom's High Fat, Salt, and Sugar (HFSS) regulations, which restrict the promotion of high-fat and high-sugar products, have accelerated the introduction of sugar-free and zero-calorie functional waters. Brands such as Highland Spring and Vital Drinks have successfully adapted to these regulations by using natural sweeteners or avoiding sweeteners altogether. With 45% of Generation Z expressing an intent to purchase healthier products (a 7% increase from the previous year) and one in three willing to pay a premium, the United Kingdom has positioned itself as a leader in functional water innovation. However, private labels captured 39.1% of United Kingdom grocery sales in 2024, challenging branded functional waters to justify price differences through clear benefits and sustained marketing efforts.

Germany is projected to be the fastest-growing market in Europe, with a Compound Annual Growth Rate (CAGR) of 7.71% through 2031, driven by premiumization, a strong mineral water heritage, and increasing health awareness. In 2024, Germany's mineral and healing water market expanded by 1.9% to reach 9.9 billion liters. Low-carbonation water led the market with a 39.5% share, while still (non-carbonated) water grew by 7.0%, capturing 25% of the market. Per-capita consumption reached 125.6 liters annually, emphasizing water's integral role in German diets. The premium bottled water segment, valued at USD 2,982.16 million in 2024, is expected to grow at a 7.84% CAGR to USD 5,882.98 million by 2033, with functional and mineral-enhanced waters driving this growth. Gerolsteiner's March 2024 launch of 'Ursprung', a water with a total mineralization of 4,441 milligrams per liter, highlights Germany's preference for functional density and provenance-focused products.

Other European countries, including Italy, France, Spain, the Netherlands, Poland, Belgium, Sweden, and others, contribute to the remaining market share. Italy stands out for its strong export performance, while France is notable for its retail scale. Italian mineral water exports increased by 28.5% to EUR 1.408 billion in 2024. The United States was the largest importer, accounting for EUR 476.7 million, followed by France at EUR 158.7 million, Germany at EUR 90.4 million (a 36.5% increase), and the United Kingdom at EUR 84 million (a remarkable 165.8% increase). This growth reflects a strong international demand for premium and functional Italian water brands.

Competitive Landscape

The Europe functional water market represents a competitive landscape where multinational corporations coexist with regional specialists and emerging players. In Italy, the top eight groups control a significant portion of the domestic market. However, fragmentation remains prevalent in Northern and Western Europe, where local spring sources and heritage branding enable smaller players to maintain market share. Multinational companies are increasingly focusing on portfolio optimization and functional premiumization strategies.

In early 2026, Nestlé initiated a multibillion-euro divestment of its bottled water division, inviting first-round bids for brands such as Perrier and San Pellegrino. Private equity firms are preparing substantial leveraged financing at multiple times estimated earnings before interest, taxes, depreciation, and amortization, reflecting a shift in market perception. While plain still water is seen as less profitable, functional and premium water formats are commanding higher valuations. Danone's water division generated significant revenue in 2023, accounting for a notable % of the company's total sales. Following strong cash generation in 2024, Danone is expected to pursue acquisitions of functional water brands to complement the sustainability positioning of its evian and Volvic brands. Meanwhile, Coca-Cola and PepsiCo are expanding their hydration platforms into functional waters. Notable innovations include smartwater's canned launch in early 2024 and Powerade Power Water's electrolyte-enhanced entry in late 2025, showcasing advancements in both format and functionality.

White-space opportunities in the market are concentrated around protein waters, plant-based fortification, and direct-to-consumer subscription models. For instance, iPRO launched a collagen protein water in late 2025, while QNT introduced a protein water in cans in the same year. These products address the intersection of hydration, sports nutrition, and beauty-from-within trends. However, both rely on animal-derived collagen, leaving plant-based protein waters as an underserved niche due to challenges with solubility and taste. Smaller brands are also leveraging digital channels to bypass traditional retail barriers. Vital Drinks, for example, raised significant funding in early 2024 to launch a zero-sugar, all-vitamin spring water through direct-to-consumer platforms and Amazon. This approach allows smaller players to capture higher margins and engage directly with consumers.

Europe Functional Water Industry Leaders

The Coca-Cola Company

PepsiCo Inc.

Danone SA

Nestlé SA

Acqua Minerale San Benedetto SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Activit Vitamin Water introduced updated packaging and expanded its flavor range to include Lemon and Lime, Blackcurrant and Raspberry, and Mango and Passion Fruit. Aimed at health-conscious consumers, the brand launched a 330ml can format, supported by digital advertising, influencer campaigns, and in-store promotions.

- May 2025: Coca-Cola's Vitaminwater brand introduced a refreshed packaging design, making a clear distinction between zero-sugar and full-sugar options. The brand also launched functional flavors such as “Elevate” (blue raspberry limeade with multivitamins) and “Re-Hydrate Zero Sugar” (pineapple passionfruit, enriched with electrolytes). Additionally, the “Power-C Zero Sugar” (dragonfruit) variant highlights vitamin C and zinc for immune support

- May 2024: Evian Sparkling was introduced in recyclable aluminum cans and 100% rPET bottles, aiming to achieve full packaging circularity by 2025. Emphasizing premium hydration, the product features fine bubbles and a subtle taste, supported by a marketing approach highlighting innovation and commitment to addressing environmental challenges.

Europe Functional Water Market Report Scope

Functional water is a type of non-alcoholic beverage that is enhanced with ingredients such as acids, herbs, raw fruits, or vegetables, providing a range of health benefits. The European functional water market is segmented by product type, including vitamin, protein, electrolyte or mineral, and others; by packaging type, such as Polyethylene Terephthalate (PET) bottles, cans, and others; by flavor, categorized as flavored and non-flavored; by distribution channel, including supermarkets and hypermarkets, convenience stores, online retail stores, and other channels; and by geography, covering Germany, United Kingdom, Italy, France, Spain, Netherlands, Poland, Belgium, Sweden, and the rest of Europe. The market sizing has been done in value terms in USD and volume in liters for all the abovementioned segments.

By Product Type

| Vitamin |

| Protein |

| Electrolyte/Mineral |

| Others |

By Packaging Type

| PET Bottles |

| Cans |

| Others |

By Flavor

| Flavored |

| Non-Flavored |

By Distribution Channel

| Supermarkets and Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Channels |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Vitamin |

| Protein | |

| Electrolyte/Mineral | |

| Others | |

| By Packaging Type | PET Bottles |

| Cans | |

| Others | |

| By Flavor | Flavored |

| Non-Flavored | |

| By Distribution Channel | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Channels | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

What is the forecast value of Europe functional water by 2031?

The category is projected to reach USD 1.99 billion by 2031.

How fast will functional water sales grow in Germany?

Germany’s revenue is expected to increase at a 7.71% CAGR between 2026 and 2031.

Which product type is expanding quickest?

Electrolyte and mineral waters, forecast at an 8.58% CAGR through 2031.

Why are aluminum cans gaining share in European hydration?

Rising rPET costs and aluminum’s recyclability are driving a 9.42% CAGR for cans to 2031.

What share did flavored functional waters hold in 2025?

Flavored variants captured 71.91% of European revenue that year.

Page last updated on: