Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 32.90 Billion |

| Market Size (2026) | USD 34.24 Billion |

| Market Size (2031) | USD 41.83 Billion |

| Growth Rate (2026 - 2031) | 4.08% CAGR |

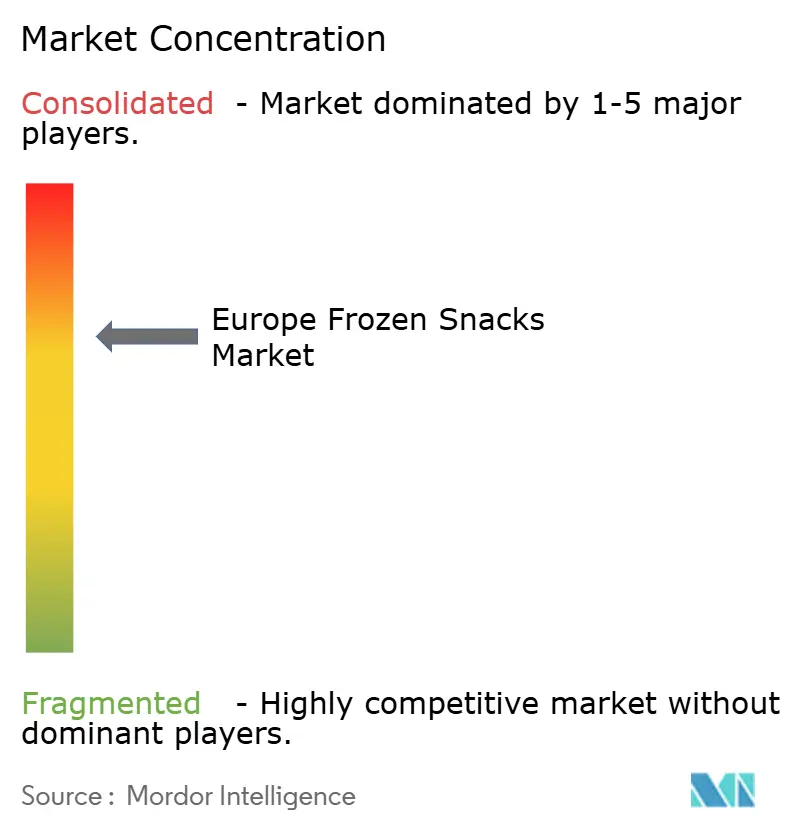

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Frozen Snacks Market Analysis by Mordor Intelligence

Europe frozen snacks market size in 2026 is estimated at USD 34.24 billion, growing from 2025 value of USD 32.90 billion with 2031 projections showing USD 41.83 billion, growing at 4.08% CAGR over 2026-2031. Sustained demand for convenient meal substitutes, a widening base of single-person households, and manufacturing upgrades that safeguard texture and flavor stability underpin near-term growth. Millennial and Gen Z consumers, who routinely favor prepared foods for at-home occasions, anchor volume momentum, while premiumization through organic certification and clean-label ingredient lists supports value expansion. At the same time, investments in advanced cryogenic and mechanical freezers have cut energy use and shrinkage, enabling manufacturers to scale at lower marginal cost and improve carbon profiles. Retail consolidation, tighter temperature-controlled logistics, and EU-wide labeling directives ensure wide product accessibility and consistent quality, keeping the Europe frozen snacks market on a predictable upward trajectory.

Key Report Takeaways

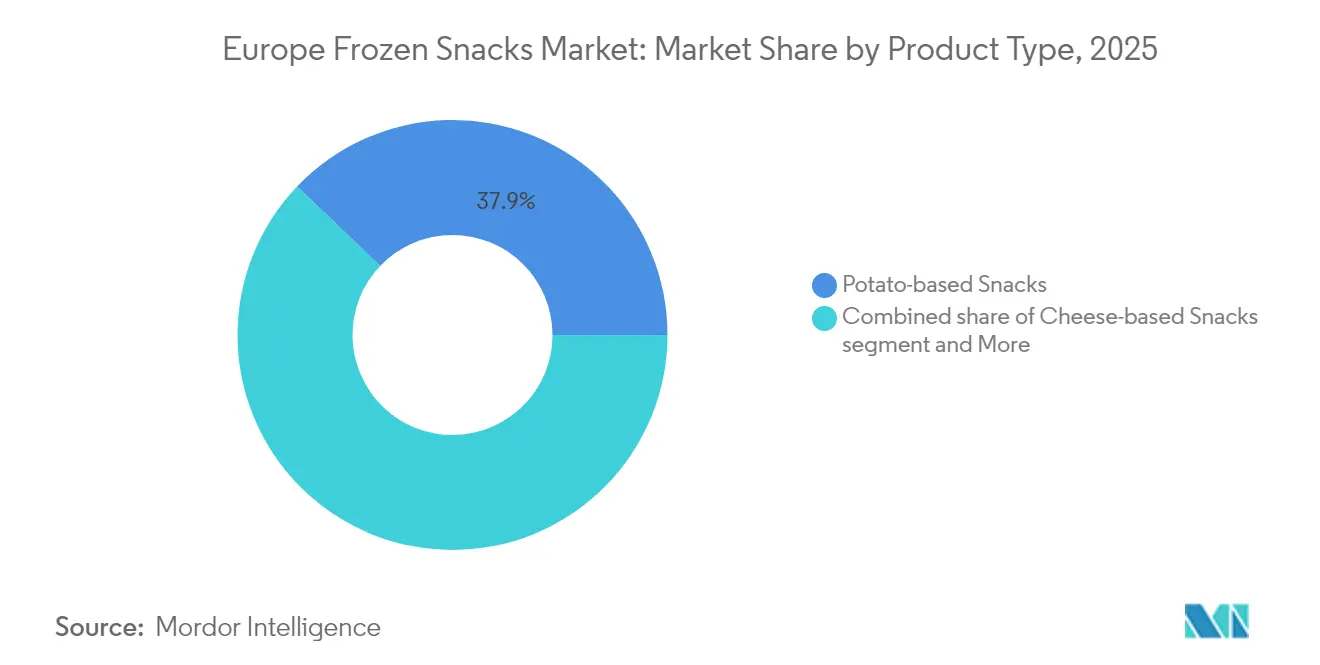

- By product type, potato-based snacks led with 37.86% revenue share in 2025, whereas fruit and vegetable-based snacks are set to expand at a 5.56% CAGR through 2031.

- By category, conventional SKUs captured 77.92% of the Europe frozen snacks market size in 2025, while organic variants are poised to grow at a 7.05% CAGR.

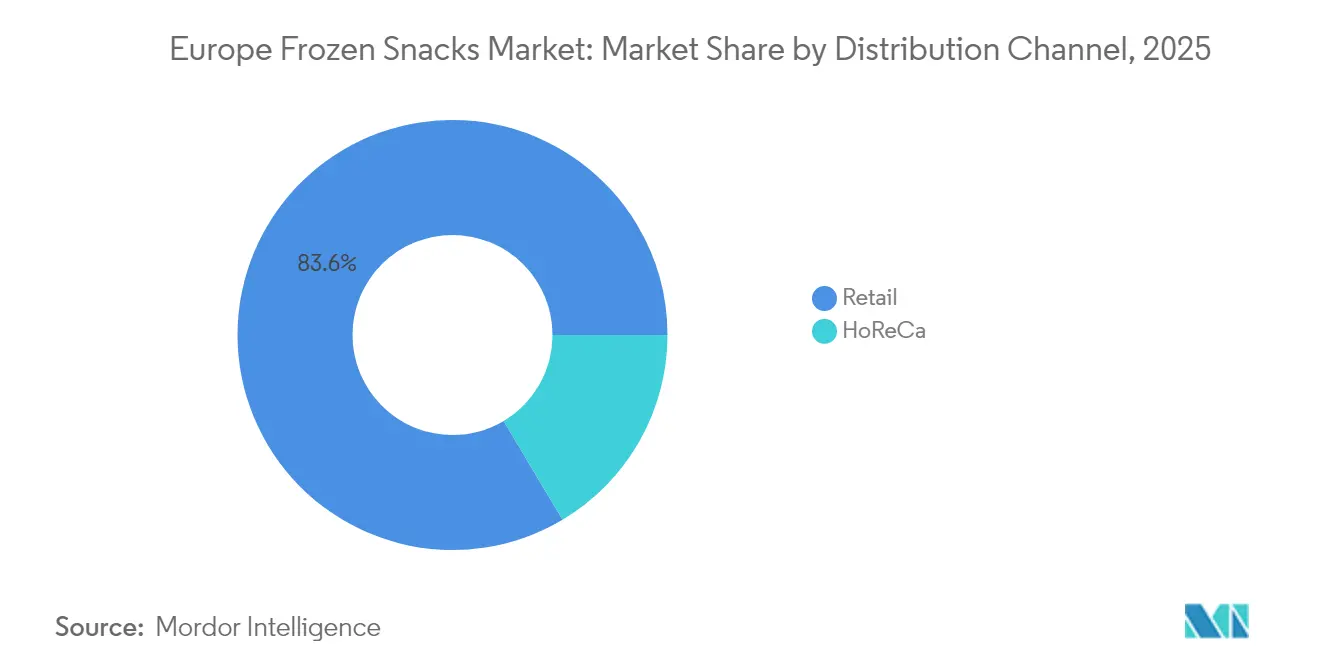

- By distribution channel, retail outlets collectively held 83.55% of the Europe frozen snacks market share in 2025; HoReCa is projected to log the fastest 6.12% CAGR to 2031.

- By geography, the United Kingdom accounted for 23.10% of the Europe frozen snacks market size in 2025; Poland is expected to record a leading 7.18% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Frozen Snacks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Millennial and Gen Z Demand for On-the-Go Snacks | +0.8% | EU-wide, strongest in urban centers | Medium term (2-4 years) |

| Rising Urbanization and Disposable Income | +0.7% | Eastern Europe, Nordic regions | Long term (≥ 4 years) |

| Clean Label and Free-From Products Gain Traction | +0.6% | Western Europe, Germany, France | Medium term (2-4 years) |

| Boost in Potato Production Fuels Frozen Snack Expansion | +0.5% | Germany, Netherlands, France | Short term (≤ 2 years) |

| Growing Appetite for Ethnic and Global Flavors | +0.4% | UK, Germany, metropolitan areas | Medium term (2-4 years) |

| Advancements in Freezing Technologies | +0.3% | EU manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Millennial and Gen Z Demand for On-the-Go Snacks

Millennials and Gen Z, with their fast-paced lifestyles, are driving the surge in demand for on-the-go snacks, propelling the Europe Frozen Snacks Market. These demographics prioritize convenience, gravitating towards quick meal solutions that seamlessly fit into their busy routines. With their extended shelf life, ease of storage, and simple preparation, frozen snacks have emerged as the go-to choice for these consumer groups. In 2024, the World Bank noted that 56% of the working population in Germany and 57% in the UK were female, highlighting a significant segment of consumers seeking convenient food options [1]Source: World Bank, "Labor force participation rate, female (% of female population ages 15+) (modeled ILO estimate)", data.worldbank.org. The rising trend of snacking between meals, combined with a broader array of frozen options—from pizzas and pastries to finger foods—bolsters this market's expansion. Additionally, the growing diversity in product offerings caters to varying taste preferences and dietary needs, further enhancing market appeal. The retail sector's growth further amplifies this demand, ensuring frozen snacks are readily available in supermarkets, hypermarkets, and online platforms. This evolving consumer behavior underscores the pivotal influence of Millennials and Gen Z on Europe's frozen snacks landscape.

Rising Urbanization and Disposable Income

The increasing rate of urbanization and the rise in disposable income are significant drivers of the Europe frozen snacks market. According to World Bank data, urbanization in the European Union reached 76% in 2023, highlighting the growing shift of populations toward urban areas [2]Source: World Bank, “Urban population (% of total population)- European Union”, data.worldbank.org. This urban migration has led to a transformation in consumer lifestyles, with a heightened preference for convenient and ready-to-eat food products. Urban dwellers, particularly the working population, often face time constraints, making frozen snacks an appealing choice due to their ease of preparation and time-saving attributes. Additionally, higher disposable income levels across the region empower consumers to explore premium and diverse frozen snack options, further fueling market growth. The combination of these factors is expected to drive the expansion of the frozen snacks market in Europe during the forecast period.

Growing Appetite for Ethnic and Global Flavors

A growing demand for ethnic and global flavors drives Europe's frozen snacks market. Influenced by globalization, travel, and exposure to international cuisines, consumers are seeking diverse and authentic taste experiences. This has increased demand for frozen snacks featuring unique flavors from Asian, Middle Eastern, and South American cuisines. Manufacturers are responding with innovative products that retain the authenticity of ethnic recipes. As of December 2024, the Office for National Statistics reported 266,000 non-EU nationals moved to the UK for study-related purposes, closely following 262,000 for work [3]Source: Office for National Statistics, “Long-term international migration provisional year ending December 2024”, ons.gov.uk. This influx has introduced new culinary preferences, encouraging manufacturers to expand their offerings. These trends are expected to drive market growth during the forecast period.

Boost in Potato Production Fuels Frozen Snack Expansion

The significant increase in potato production is a key driver of the European frozen snacks market. Potatoes serve as a primary raw material for various frozen snack products, including French fries, potato wedges, and hash browns. For instance, countries like Germany, France, and the Netherlands have reported consistent growth in potato yields due to advancements in agricultural practices and favorable climatic conditions. This rise in production ensures a steady supply of high-quality raw materials, enabling manufacturers to meet the growing consumer demand for frozen snacks. Additionally, the availability of surplus potatoes has encouraged innovation in product offerings, such as seasoned potato-based snacks and healthier frozen options, further fueling market expansion. The robust potato supply chain in Europe also supports cost efficiency, making frozen snacks more accessible to a broader consumer base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Scrutiny of Ultra-Processed Foods | -0.9% | EU-wide, strongest in Nordic countries | Short term (≤ 2 years) |

| Increasing Inclination Toward Healthy Snacking Options | -0.7% | Western Europe, urban areas | Medium term (2-4 years) |

| Stringent EU Regulation Limiting Additive Use | -0.4% | EU-wide regulatory compliance | Long term (≥ 4 years) |

| High Concerns Over High Trans Fat and Sodium Content | -0.6% | Health-conscious markets, Germany, Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Scrutiny of Ultra-Processed Foods

Consumer awareness campaigns and scientific research are reshaping the landscape for traditional frozen snack formulations. As perceptions shift, manufacturers face the challenge of reformulating products to meet consumer expectations for taste and shelf stability. This scrutiny now extends beyond individual health concerns, with consumers increasingly weighing environmental and social responsibility in their food choices. In response, regulators are tightening labeling requirements and considering taxation mechanisms, both of which could influence product positioning and pricing. Yet, the research highlights a significant gap: many consumers struggle to accurately identify ultra-processed foods. This confusion opens doors for educational marketing and transparent communication. Manufacturers that swiftly adapt through reformulation and clear labeling stand to gain market share, outpacing competitors who cling to traditional formulations without evolving to meet these new consumer expectations.

Increasing Inclination Toward Healthy Snacking Option

Health-conscious consumers are reshaping the market by demanding products with added fiber, reduced sodium, and no artificial ingredients. EU regulations, through mandatory nutrition labeling, support this shift by enabling informed choices and driving product improvements. In response, the market is introducing hybrid products like vegetable-based snacks and protein-enriched formulations, combining convenience with nutrition. This trend creates opportunities for premium branding as consumers are willing to pay more for perceived health benefits. However, competition from fresh and minimally processed options is intensifying, pushing frozen snack manufacturers to innovate and justify convenience premiums while addressing health concerns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Potato Dominance Faces Health-Driven Disruption

In 2025, potato-based snacks dominated the Europe frozen snacks market, capturing a 37.86% revenue share. This significant share highlights the strong consumer preference for potato-based products, driven by their versatility, taste, and widespread availability across the region. The segment benefits from continuous product innovation and the introduction of healthier options, catering to evolving consumer demands. Additionally, the convenience offered by frozen potato-based snacks, such as easy preparation and longer shelf life, has further contributed to their popularity. Key players in the market are focusing on launching new flavors and formats to attract a broader consumer base, ensuring sustained growth in this segment.

Meanwhile, fruit and vegetable-based snacks in the Europe frozen snacks market are projected to grow at a 5.56% CAGR through 2031. This growth is fueled by increasing consumer awareness of health and wellness, leading to a rising demand for nutrient-rich and natural snack options. The segment is also benefiting from the growing trend of plant-based diets, as consumers seek alternatives to traditional snack options. Manufacturers are focusing on expanding their product portfolios with innovative offerings, such as organic and minimally processed frozen snacks, to meet this growing demand. Furthermore, advancements in freezing technologies are helping to preserve the nutritional value and taste of fruit and vegetable-based snacks, enhancing their appeal to health-conscious consumers and driving the segment's expansion.

By Category: Organic Segment Capitalizes on Premium Positioning

In 2025, conventional frozen snacks dominate the Europe frozen snacks market with a substantial 77.92% market share. This dominance can be attributed to their widespread availability, affordability, and established consumer preference for traditional snack options. Conventional frozen snacks benefit from extensive distribution networks and strong brand loyalty, making them a staple in households across the region. Additionally, advancements in freezing technology and product innovation have enabled manufacturers to enhance the taste and quality of these snacks, further solidifying their position in the market. Despite the growing interest in healthier alternatives, conventional frozen snacks continue to cater to a broad consumer base seeking convenience and familiarity.

On the other hand, organic frozen snacks are emerging as a high-growth segment within the Europe frozen snacks market. From 2026 to 2031, this segment is projected to grow at a notable CAGR of 7.05%, driven by increasing consumer awareness of health and environmental sustainability. Organic frozen snacks appeal to a niche but expanding demographic willing to pay a premium for products perceived as healthier and eco-friendly. Factors such as the rising demand for clean-label products, stringent regulations promoting organic farming, and growing environmental consciousness are fueling this growth. Manufacturers are responding to this trend by introducing innovative organic snack options, leveraging certifications, and emphasizing transparency in sourcing and production processes. This shift reflects a broader consumer inclination toward sustainable and high-quality food choices.

By Distribution Channel: HoReCa Recovery Drives Growth Acceleration

The retail channel dominated the Europe frozen snacks market in 2025, accounting for an 83.55% market share. This dominance can be attributed to the widespread availability of frozen snacks in supermarkets, hypermarkets, and convenience stores, which cater to the growing consumer demand for quick and easy meal solutions. Retailers have also benefited from advancements in cold chain logistics, ensuring the consistent quality and availability of frozen snacks. Additionally, promotional activities and discounts offered by retail outlets have further strengthened their position in the market. The increasing penetration of e-commerce platforms has also contributed to the retail channel's growth, as online grocery shopping becomes more prevalent across Europe.

In contrast, the HoReCa segment is expected to exhibit significant growth, with a projected CAGR of 6.12% during the forecast period of 2026-2031. This growth is driven by the increasing preference for dining out and the rising adoption of frozen snacks by foodservice providers to reduce preparation time and maintain consistency in quality. The HoReCa segment's resilience is further supported by the growing trend of quick-service restaurants and cafes incorporating frozen snacks into their menus to meet consumer demand for convenience and variety. Additionally, the expansion of the tourism and hospitality industry across Europe is fueling demand for frozen snacks in hotels, restaurants, and catering services. The ability of frozen snacks to offer extended shelf life and reduce food waste makes them an attractive option for HoReCa operators, further driving the segment's growth in the Europe frozen snacks market.

Geography Analysis

The United Kingdom maintains market leadership with a 23.10% share in 2025, leveraging strong consumer acceptance of convenience foods and established retail infrastructure that supports frozen product distribution. Post-Brexit supply chain adaptations demonstrate market resilience, as manufacturers develop alternative sourcing strategies and distribution networks that maintain product availability and competitive pricing. The market benefits from cultural preferences for ready-to-eat products and snacking occasions that align with frozen snack positioning. However, economic uncertainties and inflation pressures create consumer price sensitivity that challenges premium product positioning and may favor value-oriented alternatives.

Germany represents Europe's largest economy and demonstrates substantial frozen snack consumption driven by busy lifestyles and acceptance of convenience foods across demographic segments. The market benefits from advanced cold chain infrastructure and retail sophistication that enables product innovation and premium positioning. France leverages culinary expertise and quality expectations to drive demand for sophisticated frozen snack formulations that meet elevated taste standards. Italy's market growth reflects changing consumption patterns as traditional meal structures adapt to modern lifestyle demands, creating opportunities for frozen snacks that complement rather than replace traditional food culture. Poland emerges as the fastest-growing market with a 7.18% CAGR during 2026-2031, driven by rapid economic development and rising disposable incomes that enable increased convenience food consumption. The market benefits from EU integration and foreign investment that modernizes retail infrastructure and introduces international brands and product formats. Spain, Netherlands, and Sweden demonstrate steady growth patterns supported by urbanization trends and demographic changes that favor convenience food adoption. Russia faces market uncertainties due to geopolitical tensions and economic sanctions that impact supply chains and consumer purchasing power, creating volatility in demand patterns and distribution strategies.

Competitive Landscape

The European frozen snacks market demonstrates a moderate consolidation, with established players such as Nomad Foods Ltd, McCain Foods Limited, Dr Oetker Group, and Nestlé S.A. leveraging vertical integration strategies and investing in advanced technologies to strengthen their market positions. These companies are focusing on controlling multiple stages of the supply chain, from sourcing raw materials to distribution, ensuring cost efficiency and quality consistency. Such strategies help them maintain a competitive edge against emerging disruptors and private-label brands, which are gaining traction due to their affordability and localized offerings.

Market leaders are also prioritizing brand portfolio optimization to cater to diverse consumer preferences. For instance, Nestlé has expanded its frozen snacks portfolio by introducing plant-based options under its Garden Gourmet brand, addressing the growing demand for healthier and sustainable food choices. Similarly, McCain Foods has invested in product innovation, such as its range of oven-ready frozen snacks, to meet the increasing consumer demand for convenience. These companies are also enhancing supply chain efficiency by adopting digital tools and automation, enabling them to respond quickly to market dynamics and reduce operational costs.

Innovation capabilities remain a critical focus for market leaders as they navigate evolving consumer preferences and stringent regulatory requirements. Companies are investing in research and development to create new product formulations that align with health trends, such as low-fat and gluten-free options. For example, Dr. Oetker has introduced frozen snacks with reduced sugar content to appeal to health-conscious consumers. Additionally, these players are actively monitoring regulatory changes, such as labeling requirements and sustainability mandates, to ensure compliance and maintain consumer trust. By combining these strategies, established players are solidifying their positions in the competitive European frozen snacks market.

Europe Frozen Snacks Industry Leaders

-

Nomad Foods Ltd

-

McCain Foods Limited

-

Dr Oetker Group

-

Nestle S.A

-

General Mills Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: McCain Foods UK has launched a new potato snack that blends the satisfying crunch of a crisp with the light, fluffy texture of a fry. This latest offering reflects the company’s commitment to innovation and quality, catering to changing consumer tastes with distinctive, potato-based snacking experiences.

- November 2024: Ferrero UK introduced the Kinder Bueno ice cream cone to its frozen dessert lineup, tapping into the surging appetite for novel frozen treats. The new offering, available in single cones and multipacks, boasts two enticing flavors: Kinder Bueno Classic and Kinder Bueno White.

- July 2024: Bibigo expanded its distribution of frozen Korean food products across Europe. The company's products are now available through major retailers including Edeka, Rewe, Tegut, and Globus in Germany; Asda, Sainsbury's, and Ocado in the United Kingdom; and Albert Heijn, Jumbo, and Hoogvliet in the Netherlands. In addition to its core products of mandu (traditional Korean dumplings) and Korean-style chicken, Bibigo is introducing vegetarian mandu and gimbap (Korean seaweed rice rolls) to the European market.

- April 2024: McCain Foods expanded its strategic partnership with Strong Roots to accelerate growth in the vegetable-forward frozen food segment, responding to increasing consumer demand for plant-based options. The collaboration aims to leverage Strong Roots' innovation capabilities with McCain's global distribution network to capture emerging market opportunities.

Europe Frozen Snacks Market Report Scope

Frozen snacks are pre-packaged, bite-sized food items that are preserved by freezing for extended shelf life. The Europe frozen Snacks market is segmented by type, snack format, end user, freezing technique, distribution channel, and geography. By type, the market studied is segmented into potato-based snacks, meat & poultry-based snacks, fruit & vegetable-based snacks, cheese-based snacks, bakery & confectionery-based snacks, and others. By end user, the market is segmented into household/retail consumers and Horeca/foodservice. Based on freezing technique, the market is segmented into individually quick frozen, blast frozen and other techniques. By distribution channel, the market studied is segmented by hypermarket/supermarket, convenience store, online retail stores, discount stores, speciality frozen food stores and other distribution channels. The market study also includes geographical analysis. By geography, the market covers country level analysis of United Kingdom, France, Germany, Spain, Netherlands, Poland, Italy, Sweden, Russia and Rest of Europe. The report offers market size and values (in USD Million) for the above segments.

By Type

| Potato-based Snacks |

| Meat and Poultry-based Snacks |

| Seafood-based Snacks |

| Fruit- and Vegetable-based Snacks |

| Cheese-based Snacks |

| Bakery and Confectionery-based Snacks |

| Other Types |

By Category

| Conventional |

| Organic |

By Distribution Channel

| HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Retail Channel |

By Geography

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Poland |

| Sweden |

| Russia |

| Rest of Europe |

| By Type | Potato-based Snacks | |

| Meat and Poultry-based Snacks | ||

| Seafood-based Snacks | ||

| Fruit- and Vegetable-based Snacks | ||

| Cheese-based Snacks | ||

| Bakery and Confectionery-based Snacks | ||

| Other Types | ||

| By Category | Conventional | |

| Organic | ||

| By Distribution Channel | HoReCa | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Retail Channel | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Sweden | ||

| Russia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current size of the Europe frozen snacks market?

The market is valued at USD 34.24 billion in 2026 and is projected to hit USD 41.83 billion by 2031.

Which product type leads sales today?

Potato-based snacks hold the top position with 37.86% revenue share in 2025.

Which distribution channel is expanding the fastest?

The HoReCa sector is forecast to grow at a 6.12% CAGR through 2031 as foodservice rebounds and delivery formats scale.

How quickly is the organic category growing?

Organic frozen snacks are expected to post a 7.05% CAGR between 2026 and 2031, outpacing conventional lines.

Page last updated on: