Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

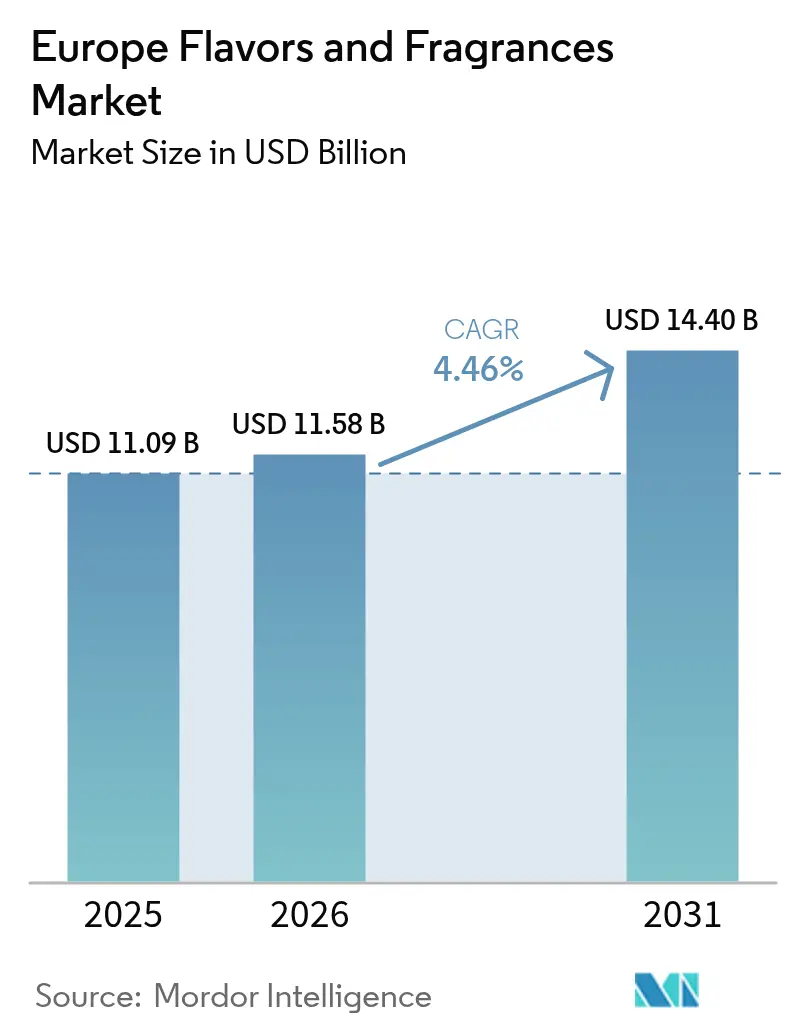

| Base Year Market Size (2025) | USD 11.09 Billion |

| Market Size (2026) | USD 11.58 Billion |

| Market Size (2031) | USD 14.4 Billion |

| Growth Rate (2026 - 2031) | 4.46% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Flavors And Fragrances Market Analysis by Mordor Intelligence

Europe flavors and fragrances market size in 2026 is estimated at USD 11.58 billion, growing from 2025 value of USD 11.09 billion with 2031 projections showing USD 14.4 billion, growing at 4.46% CAGR over 2026-2031. This steady climb reflects demand for premium, sustainable and health-aligned ingredients across food, beverage, personal care and household categories. Growth pivots on three structural forces: progressive regulation that encourages clean-label reformulation, rapid technology adoption in biotechnology and digital product design, and a consumer shift toward wellness, personalization and ethical sourcing. Germany anchors scale and innovation while Spain supplies outsized momentum, mirroring its competitive energy costs and expanding food-processing base. Consolidation, such as the DSM-Firmenich combination, signals the need for size to navigate compliance and finance R&D, yet a concentration score of 3/10 still points to ample room for specialist entrants.

Key Report Takeaways

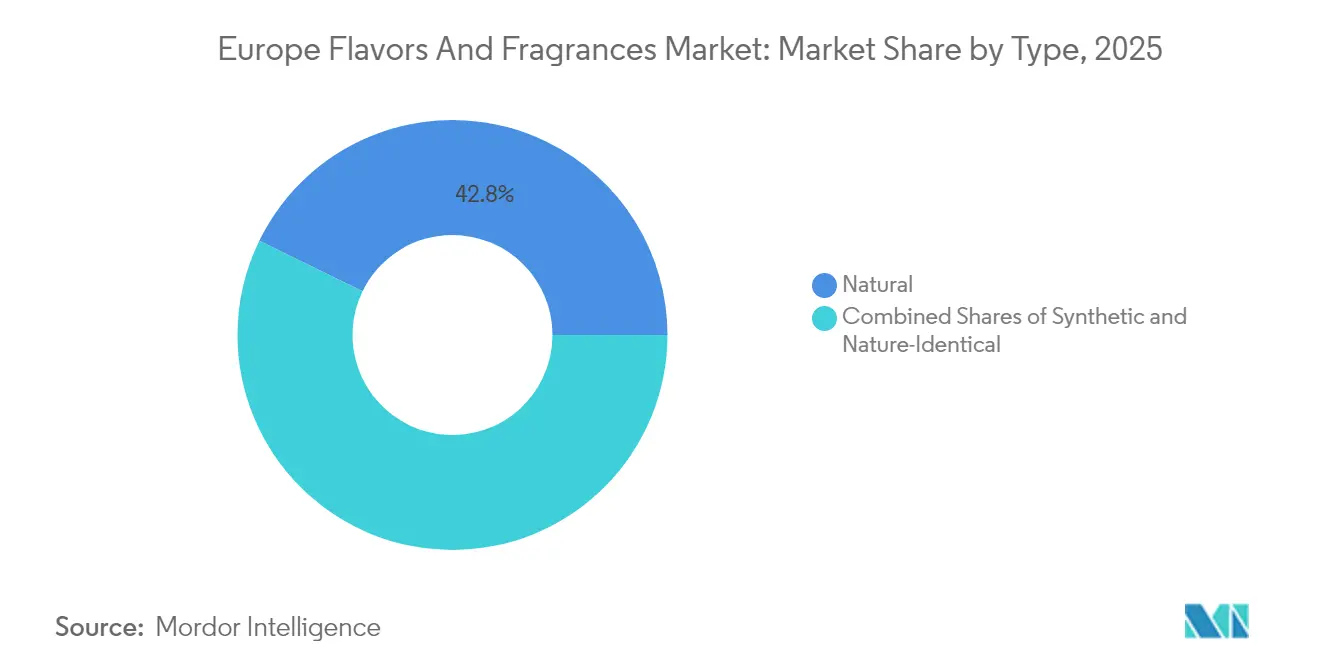

- By type, natural ingredients captured 42.78% of Europe's flavors and fragrances market share in 2025 and are advancing at a 5.88% CAGR through 2031.

- By form, liquid products led with a 33.65% share of the European flavors and fragrances market size in 2025; powder formats are projected to expand at a 5.31% CAGR between 2026-2031.

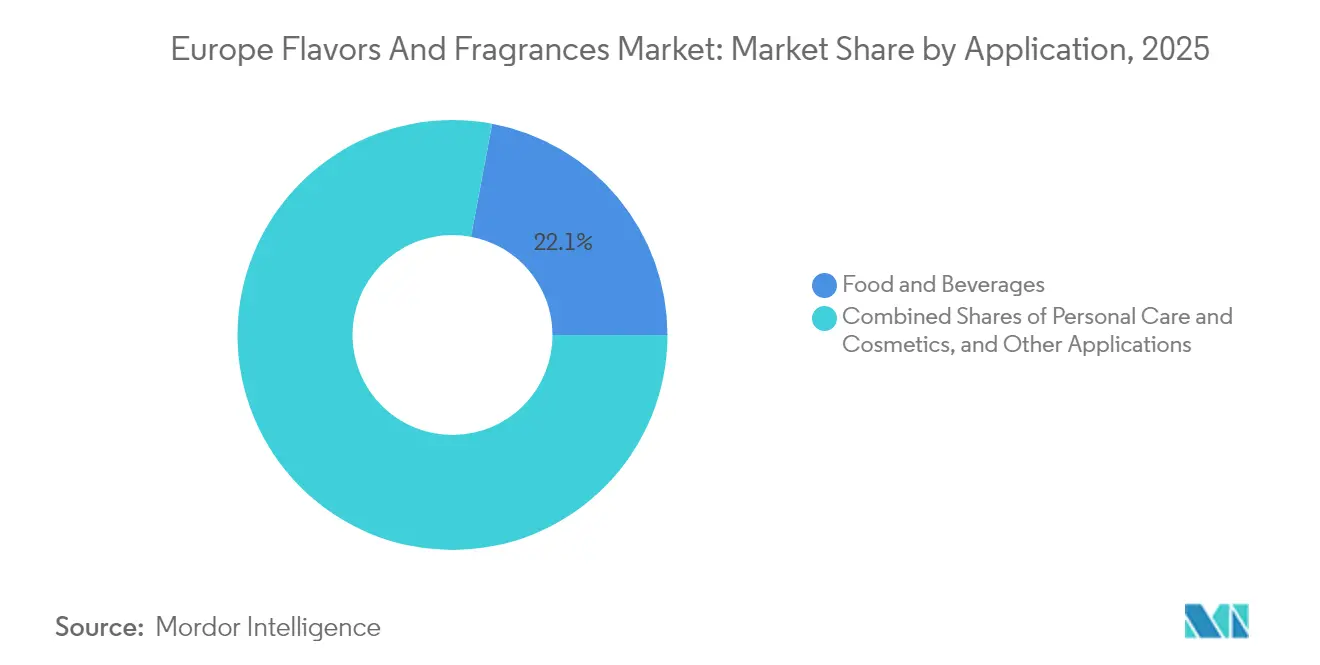

- By application, beverages held 22.05% revenue share in 2025, while personal care and cosmetics recorded the highest projected CAGR at 6.29% through 2031.

- By geography, Germany commanded 25.30% of the European flavors and fragrances market in 2025, whereas Spain is forecast to post the fastest 6.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Flavors And Fragrances Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural and clean-label ingredients | +1.2% | Global, strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| Growth of functional foods, beverages, and wellness products | +0.9% | Western Europe core, expanding to Eastern Europe | Long term (≥ 4 years) |

| Increasing popularity of personalized and customized flavor/fragrance solutions | +0.7% | Germany, France, UK leading adoption | Medium term (2-4 years) |

| Expansion of processed food & beverage industry | +0.8% | Spain, Italy showing strongest growth | Short term (≤ 2 years) |

| Increasing Use of Fragrances in various cosmetics and personal care products | +1.1% | France, Germany, Italy premium segments | Long term (≥ 4 years) |

| Growing interest in vegan and cruelty-free ingredients | +0.6% | Northern Europe, spreading to Mediterranean | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for natural and clean-label ingredients

In Germany, 69% of organic food sales now occur through conventional retail outlets, highlighting a significant consumer shift toward transparency and naturalness and signaling the mainstream adoption of natural products. This trend extends beyond the food market. For example, Symrise AG launched the Mindera® platform, featuring 100% plant-based product protection technology designed for cosmetic formulations. Regulatory developments further support this transition. The EFSA recently approved naringenin as a food flavoring, citing no genotoxicity concerns, in stark contrast to its ban on artificial smoke flavorings. Companies investing in biotechnology-derived natural ingredients are aligning with evolving regulatory standards that increasingly favor naturally-sourced alternatives while positioning themselves to capture premium pricing.

Growth of functional foods, beverages, and wellness products

European beverage manufacturers are heeding the Union of European Beverage Associations' pledge to cut added sugars by 10% between 2019 and 2025. This commitment has spurred a demand for advanced flavor systems that not only preserve taste but also align with health-centric branding. A notable advancement in this realm is the rise of protein-based sweeteners. For instance, the X3 sweetener from the Fraunhofer Institute boasts a sweetness level 10,000 times that of table sugar, all while delivering flavor profiles reminiscent of honey. This blend of heightened health awareness and cutting-edge technology paves the way for flavor houses to craft multifunctional ingredients, ensuring both taste satisfaction and wellness advantages. Furthermore, the growing inclination towards botanicals and herbal extracts in functional applications underscores a consumer preference for naturally health-associated ingredients over synthetic ones.

Increasing popularity of personalized and customized flavor/fragrance solutions

Artificial intelligence and digital technologies are reshaping the landscape of flavor creation. Companies like Estée Lauder are harnessing AI for tailored fragrance suggestions, simultaneously inaugurating innovation hubs such as the Fragrance Atelier in Paris. Givaudan's Digital Factory, also in Paris, stands as a testament to this evolution, boasting state-of-the-art collaborative spaces and tools like the Mini Scent Piano, elevating sensory experiences. The push for customization isn't confined to premium segments. AI Palette's 2025 trends report underscores hyper-personalization as a pivotal trend, spotlighting features like allergen detection and tailored nutrition. Gen Z, with their penchant for unique and whimsical flavors, is at the forefront of this demand, further fueled by the rapid-fire nature of social media. This blend of technology not only facilitates smaller batch productions but also accelerates the market entry of these bespoke solutions, making once-exclusive personalized products accessible to a broader audience.

Expansion of processed food & beverage industry

In 2023, Spain's food processing sector imported USD 2.2 billion worth of agricultural products from the US. Projections indicate that Spain's agro-food sector will grow by 4% in 2025, driven by a strong demand for flavoring ingredients, as noted by the USDA Foreign Agricultural Service[1]USDA Foreign Agricultural Service, “Food Processing Ingredients Annual,” usda.gov. Spanish manufacturers in the processed food industry enjoy a competitive edge in energy-intensive flavoring processes, thanks to lower energy costs compared to global rivals, as highlighted by CaixaBank Research. Kerry Group's innovative salt and sugar reduction technologies are boosting their margins, with EBITDA margins hitting 16.1% in H1 2025. This surge comes as retailers impose stricter standards on added sugars and salt content. As the processed food sector expands, there's a rising demand for advanced flavoring systems. These systems not only mask off-notes from reformulated products but also ensure they remain appealing to consumers. Companies specializing in natural masking agents and flavor enhancement technologies stand to gain the most, as they enable healthier product formulations without sacrificing taste.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent European regulations on the use of additives | -0.8% | EU-wide, particularly affecting Germany, France | Short term (≤ 2 years) |

| Volatility in raw material prices | -0.6% | Global impact, acute in Mediterranean regions | Short term (≤ 2 years) |

| Challenges in scaling up new sustainable or biotechnology-derived ingredients | -0.4% | Northern Europe biotech hubs | Medium term (2-4 years) |

| Rising Health Concerns over the use of Artificial Flavoring | -0.5% | EU-wide consumer sentiment shift | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent European regulations on the use of additives

The European Union's ban on artificial smoke flavorings impacts approximately USD 34.91 billion in sales. Manufacturers have only two years to reformulate products containing these additives, while traditional smoking replacements are allowed a five-year phase-out period. EFSA's identification of genotoxicity in eight primary smoke flavoring products underscores the EU's increasingly stringent safety assessments, creating uncertainty for companies developing new synthetic ingredients, as highlighted by the European Commission[2]European Commission, "Information on the procedure for the renewal of existing authorisations for smoke flavourings", www.food.ec.europa.eu. The new EU Regulation 2023/1545 expands fragrance allergen labeling requirements to 56 ingredients, with compliance deadlines set for July 2026 for existing products and July 2028 for new formulations. These regulatory pressures provide a competitive edge to companies with strong natural ingredient portfolios while imposing significant reformulation costs on those dependent on synthetic alternatives. The regulatory environment's shift toward precautionary principles indicates a continued tightening of approval processes, favoring established natural ingredients over novel synthetic compounds.

Volatility in raw material prices

Between January and July 2024, Madagascar exported 4,300 metric tons of vanilla, exceeding global demand by nearly 50%. This oversupply has resulted in historically low prices for industrial-grade vanilla. In the cocoa market, supply is expected to fall short by 11% in 2024, with prices rising approximately 300% over the past year due to the swollen shoot virus and illegal gold mining in key production regions. Climate events are disrupting orange juice markets, affecting both the availability and pricing of citrus-based flavoring ingredients. This volatility is driving flavor houses to explore alternative sourcing strategies and invest in synthetic or biotechnology-derived substitutes, leading to higher R&D costs and increased supply chain complexity. Companies with diversified ingredient portfolios and flexible formulation capabilities are better positioned to withstand raw material price shocks. Conversely, those dependent on single-source natural ingredients are facing margin pressures and potential supply chain disruptions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Natural Ingredients Drive Premium Positioning

In 2025, natural ingredients hold a 42.78% market share and are expected to grow at a 5.88% CAGR through 2031. This growth reflects consumers' willingness to pay a premium for clean-label products, supported by regulatory encouragement for sustainable options. Advances in biotechnology further drive this segment. For example, Newcastle University has developed highly efficient biocatalysts for solvent-free flavor ester production, showcasing the potential for sustainable manufacturing. On the other hand, synthetic ingredients face stricter regulatory oversight. The European Food Safety Authority (EFSA), as noted by Food Compliance International, has removed several flavoring substances from the Union list, including 2-Phenylpent-2-enal and certain thiazoline compounds. Nature-identical ingredients offer a middle ground, delivering cost advantages over natural alternatives while avoiding the regulatory challenges linked to synthetic compounds.

Biotechnology-derived ingredients face uncertainty due to the EU's evolving definition of natural flavors. The Standing Committee on Plants, Animals, Food, and Feed is evaluating whether flavors produced by genetically modified microorganisms should qualify as 'natural.' This regulatory ambiguity influences investment decisions and market strategies, particularly for companies focusing on fermentation-based natural alternatives. The shift toward natural ingredients is accelerating, as demonstrated by major players like Symrise, which has achieved 95% sustainable sourcing of raw materials, proving the scalability and commercial viability of natural ingredient strategies.

By Form: Liquid Dominance Challenged by Powder Innovation

In 2025, liquid formulations hold a 33.65% market share, attributed to their easy incorporation into beverages and superior sensory performance in personal care products. Meanwhile, powder formulations are experiencing growth at a 5.31% CAGR through 2031, driven by their stability and cost benefits in industrial applications. The expansion of the powder segment is supported by innovations in microencapsulation technology, which enable controlled release and improved shelf-life stability for sensitive flavor compounds. Sensient Technologies' launch of the BioSymphony platform highlights advancements in natural flavor solutions, addressing challenges related to ingredient masking and taste balancing across various applications.

Micro-encapsulated formulations are the fastest-growing sub-segment within powder applications, offering protection for volatile compounds and enabling time-release functionality in functional foods and nutraceuticals. The adoption of this technology is accelerating as manufacturers strive to differentiate products by enhancing sensory experiences and functional benefits. Liquid formulations continue to dominate premium fragrance applications, where their immediate sensory impact and complex scent profiles justify higher costs and handling challenges. The choice of form factor increasingly depends on specific application requirements: powders are gaining traction in cost-sensitive industrial applications, while liquids maintain their dominance in premium consumer markets.

By Application: Personal Care Surges Ahead of Traditional Food Applications

Personal care and cosmetics are expected to grow at a 6.29% CAGR through 2031, surpassing the beverages segment, which is projected to hold a 22.05% market share in 2025. The fragrance market in Western Europe is experiencing strong growth, with a 4% CAGR anticipated from 2023-2028, driven by premiumization trends and increasing sustainability demands, as highlighted by Perfumer & Flavorist. Premium fragrances dominate the market, accounting for 83% of the European fragrance sector, and recorded a significant 12% year-on-year growth in 2023. This growth reflects consumers' willingness to invest in products that emphasize personal expression and wellness. Furthermore, the growing appeal of unisex fragrances and smaller multipack options supports scent experimentation, particularly among Gen Z consumers seeking tailored experiences.

Food and beverage sectors are under margin pressure due to health-focused reformulations. For instance, the Union of European Beverage Associations' 10% sugar reduction target has created a need for advanced masking and enhancement technologies. While dairy and bakery sectors benefit from the clean-label trend, meat products face challenges, particularly regulatory issues related to smoke flavoring bans. Although the beverages segment maintains a significant market share, its growth rates lag behind personal care due to commoditization pressures and regulatory constraints. Meanwhile, emerging opportunities in sectors like home care and fine fragrances are gaining traction as manufacturers expand fragrance applications to deliver multisensory brand experiences beyond traditional categories.

Geography Analysis

In 2025, Germany holds a 25.30% market share, highlighting its advanced chemical and pharmaceutical infrastructure, strong regulatory compliance, and consumer preference for high-quality natural ingredients. While Germany benefits from robust industrial demand and proximity to major flavor houses' R&D centers, its growth is constrained by market maturity and economic challenges affecting consumer spending. Spain, however, is the fastest-growing market, with a 6.12% CAGR projected through 2031. This growth is driven by Spain's expanding food processing industry and competitive energy costs, which provide a manufacturing advantage over other European regions. Additionally, the Spanish pharmaceutical sector's anticipated 5% growth in 2025 and 7% in 2026 is expected to boost demand for premium flavoring ingredients, particularly in nutraceutical applications.

France continues to lead as a global hub for fragrance innovation. Key players like Estée Lauder and Givaudan are making significant investments in Paris, establishing facilities such as the Fragrance Atelier and the Digital Factory to leverage France's expertise in perfumery and its luxury brand ecosystem. Italy's fragrance market is thriving in the artistic perfumery segment, which now accounts for over 2% of the beauty market. Companies like Lumson are entering the fragrance packaging space to capitalize on the segment's 10.2% global growth rate. Meanwhile, the UK, Netherlands, and Belgium markets remain stable despite Brexit-related trade challenges. The Netherlands benefits from its role as a European distribution hub, while Belgium leverages its expertise in the chemical industry. Russia's market remains restricted by geopolitical tensions and sanctions, creating opportunities for other Eastern European markets to capture redirected demand. The "Rest of Europe" category shows varied performance: Nordic countries lead in sustainability initiatives, while Eastern European markets exhibit strong growth potential as consumer preferences increasingly align with Western European trends. Additionally, regional regulatory harmonization under EU frameworks provides a competitive advantage for companies with pan-European operations. However, success in culturally distinct segments, such as traditional foods and regional fragrance preferences, requires a deep understanding of local market dynamics.

Competitive Landscape

The European flavors and fragrances market showcases moderate fragmentation, paving the way for both consolidation and niche specialization. The recent merger of DSM and Firmenich, resulting in a USD 14.32 billion entity operating in over 60 countries, underscores the scale advantages essential for navigating intricate regulatory landscapes and championing biotechnology innovations. Major players are increasingly leaning towards vertical integration; for instance, Givaudan's acquisition of b.kolormakeup & skincare not only bolstered its sales by USD 95.69 million but also enhanced its beauty formulation and production capabilities.

In the race for a competitive edge, technology adoption stands out. Companies are channeling investments into digital tools for flavor development and harnessing AI for personalized offerings. Symrise's push towards digital transformation and its strategic investments in specialized biotech firms highlight the paramount importance of tech prowess in staying relevant. There's a burgeoning demand for biotechnology-derived natural ingredients, tailored formulation services, and eco-friendly packaging solutions.

Mane, for instance, is carving a niche by emphasizing its family-centric culture and ethical standards, setting itself apart from its larger counterparts. The market increasingly favors players with robust regulatory compliance, sustainable sourcing, and innovations in natural ingredient technologies. In contrast, those specializing in traditional synthetic ingredients grapple with shrinking margins and dwindling market shares.

Europe Flavors And Fragrances Industry Leaders

-

International Flavors & Fragrances

-

Symrise AG

-

Sensient Technologies Corporation

-

DSM-Firmenich

-

Givaudan SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Parfex opened its state-of-the-art Creation Center in Grasse, combining 800m² of laboratory space and 1,750m² of offices and featuring high-performance insulation, climate-responsive façades, and a ventilation system that cut laboratory energy use by 95%.

- October 2024: MANE inaugurated its Fine Fragrance Creative Centre in Levallois, near Paris, equipping the facility with advanced technologies, including a volumetric weighing robot and innovation spaces designed for collaboration and eco-responsibility.

- April 2024: IFF inaugurated its Co-Creation Center in Wageningen, aiming to boost global innovation through closer cooperation with customers and partners. The facility was designed to foster creativity and integrated solutions for food ingredients, supporting IFF’s commitment to delivering industry-leading consumer experiences.

- March 2023: Kerry Group officially opened its Southern Europe Innovation Centre in Barcelona, combining its existing office with new customer suites and application labs to serve Spain, Portugal, Italy, and France, and strengthen partnerships for developing food and beverage solutions.

Europe Flavors And Fragrances Market Report Scope

Flavors and fragrances create scents and tastes for use in a broad range of consumer products, including prepared foods, personal care and household products, fine fragrances, cosmetics, and beverages. The scope of the flavor and fragrance market includes segmentation of the market based on product type, form, application, and geography. By product type, the market is segmented as food flavors and fragrances. The food flavors are further segmented into natural flavors and synthetic flavors. By form, the market is segmented as liquid and powder. By application, the market is segmented as food flavors and fragrances. The food flavors segment is further sub-segmented into the bakery, confectionery, dairy products, meat and meat products, soups, pasta and noodles, beverages, and other applications. The beverages segment is further segmented into alcoholic beverages and non-alcoholic beverages. The fragrances segment is segmented into cosmetics and toiletries, household cleaners and air fresheners, fine fragrances, soaps and detergents, and other fragrances. By geography, the market is segmented into the United Kingdom, France, Spain, Italy, Germany, Russia, and the Rest of Europe. The market sizing has been done in value terms in USD for all the abovementioned segments.

Type

| Synthetic |

| Natural |

| Nature-Identical |

Form

| Powder |

| Liquid |

| Micro-Encapsulated |

Application

| Food and Beverages | Dairy products |

| Bakery and Confectionery | |

| Snacks and Savory Products | |

| Meat Products | |

| Beverages | |

| Other Types | |

| Personal Care and Cosmetics | |

| Other Applications (Home Care, Fine Fragrances) |

Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Netherlands |

| Belgium |

| Russia |

| Rest of Europe |

| Type | Synthetic | |

| Natural | ||

| Nature-Identical | ||

| Form | Powder | |

| Liquid | ||

| Micro-Encapsulated | ||

| Application | Food and Beverages | Dairy products |

| Bakery and Confectionery | ||

| Snacks and Savory Products | ||

| Meat Products | ||

| Beverages | ||

| Other Types | ||

| Personal Care and Cosmetics | ||

| Other Applications (Home Care, Fine Fragrances) | ||

| Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Belgium | ||

| Russia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How big is the Europe flavors and fragrances market in 2026?

It is valued at USD 11.58 billion in 2026 and is forecast to reach USD 14.4 billion by 2031 at a 4.46% CAGR.

Which segment grows fastest through 2031?

Personal care and cosmetics applications lead with a 6.29% CAGR, outpacing food and beverage uses.

Why are natural ingredients gaining share?

Regulatory bans on certain synthetics and consumer trust in clean-label products drive naturals to 42.78% share and a 5.88% CAGR.

Which country shows the highest growth?

Spain is projected to expand at a 6.12% CAGR due to competitive energy costs and food-processing investments.

Page last updated on: