Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.92 Billion |

| Market Size (2026) | USD 6.16 Billion |

| Market Size (2031) | USD 7.52 Billion |

| Growth Rate (2026 - 2031) | 4.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Feed Premix Market Analysis by Mordor Intelligence

The Europe feed premix market size is expected to grow from USD 5.92 billion in 2025 to USD 6.16 billion in 2026 and is forecast to reach USD 7.52 billion by 2031 at 4.06% CAGR over 2026-2031. Precision-formulated blends that align with animal welfare rules, methane reduction targets, and antibiotic-free programs continue to displace bulk vitamin-mineral concentrates. Demand expands fastest where digital rationing tools, circular economy traceability, and insect protein reformulations intersect with retailer sustainability mandates. Concentration remains moderate because regional specialists that bundle enzymes, probiotics, and phytogenics still capture niches overlooked by vertically integrated multinationals. Supply-chain security has become a strategic priority as the market absorbs the shock of China’s 2024 vitamin A export cap, prompting manufacturers to add European capacity and enter into dual-source contracts.

Key Report Takeaways

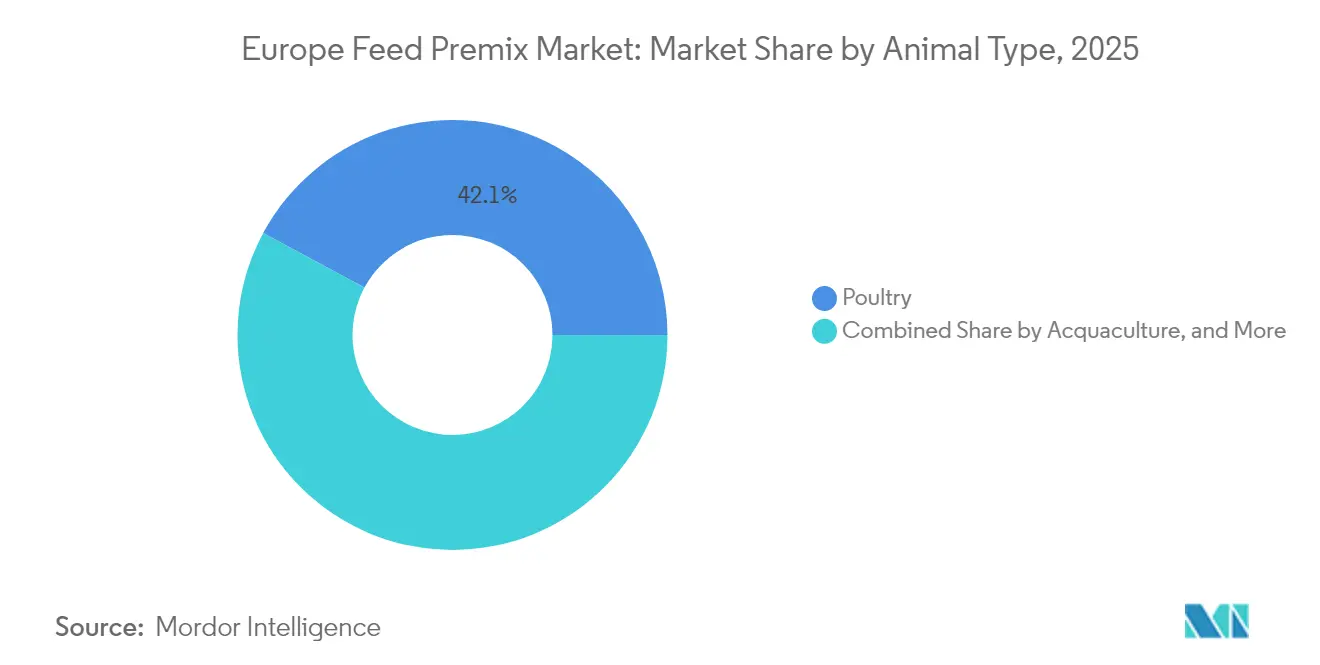

- By animal type, poultry led with 42.14% Europe feed premix market size in 2025, while aquaculture premixes are forecast to expand at a 6.72% CAGR through 2031.

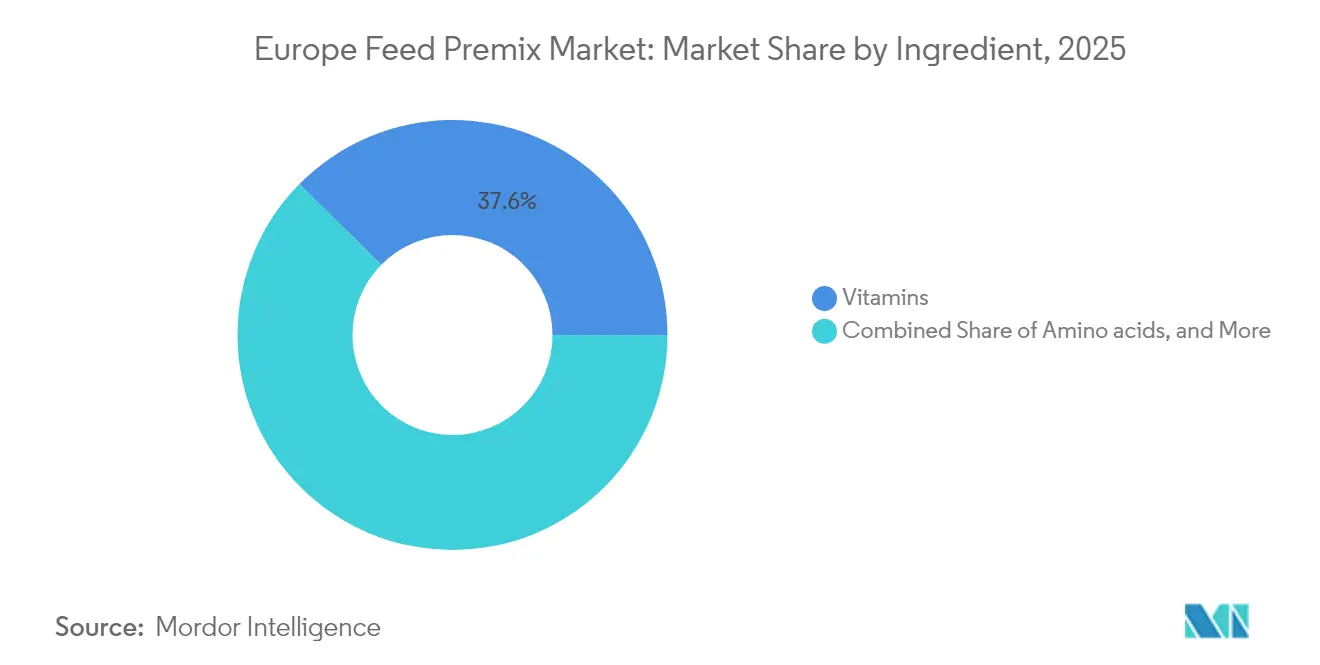

- By ingredient, vitamins accounted for 37.62% of the Europe feed premix market size in 2025, while amino acids were projected to have the highest growth rate of 6.45% from 2025 to 2031.

- By Geography, Germany holds 22.18 % of the Europe feed premix market share in 2025, while Spain is projected CAGR of 5.55 % through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Feed Premix Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High demand for premium animal protein | +1.2% | Western Europe core, spillover to Central Europe | Medium term (2‒4 years) |

| Focus on animal health and nutrition | +0.9% | Pan-European, strongest in Benelux and Nordics | Long term (≥ 4 years) |

| Government-led sustainability incentives | +0.7% | Europe Union-27, concentrated in France, Germany, Netherlands | Medium term (2‒4 years) |

| Precision-feeding digital twins | +0.5% | Netherlands, Denmark, Germany early adopters | Long term (≥ 4 years) |

| Circular-economy micronutrient traceability | +0.4% | Europe Union-27 with pilot programs in Benelux and Nordics | Long term (≥ 4 years) |

| Rapid expansion of insect protein requiring premix reformulation | +0.6% | France, Netherlands, Spain leading commercial scale | Medium term (2‒4 years) |

| Source: Mordor Intelligence | |||

High Demand for Premium Animal Protein

European consumers continue to prioritize animal protein sources that meet elevated welfare, environmental, and nutritional standards, prompting livestock producers to adopt premix formulations that enhance meat quality, eggshell strength, and milk composition. Per-capita poultry consumption in the Europe Union reached 24.8 kilograms in 2024, up from 23.1 kilograms in 2020, while organic dairy sales climbed 9% year-over-year, reflecting willingness to pay premiums for traceable production. This demand shift compels feed mills to specify higher-grade vitamin E, selenium yeast, and omega-3-enriched premixes that deliver measurable improvements in oxidative stability and shelf life. Retailers such as Carrefour and Lidl now require antibiotic-free labels on private-label poultry, a mandate that elevates the role of immune-supporting trace minerals like zinc and copper in starter and grower premixes[1]Source: European Commission, “Feed Market Data and Outlook,” ec.europa.eu. The protein premiumization trend also extends to aquaculture, where Norwegian and Scottish salmon farmers adopt astaxanthin-fortified premixes to achieve the deep red flesh color that commands export premiums in Asian markets.

Focus on Animal Health and Nutrition

Livestock health management has evolved from reactive disease treatment to proactive nutrition strategies, positioning premixes as the primary vehicle for delivering functional additives that modulate gut microbiota, reduce inflammation, and improve feed conversion ratios. The Europe Union ban on prophylactic antibiotic use, fully enforced since 2022, accelerated the incorporation of organic acids, essential oils, and yeast cell wall extracts into premix matrices, with phytogenic inclusion rates in broiler premixes rising from 0.3% to 0.8% of total formulation weight between 2022 and 2024. Dairy producers in Germany and France are increasingly specifying premixes containing rumen-protected methionine and choline to mitigate ketosis and fatty liver syndrome in high-yielding cows, interventions that reduce veterinary costs by an estimated EUR 50 (USD 54) per cow per lactation.

Government-Led Sustainability Incentives

The Europe Union Common Agricultural Policy for 2023 to 2027 allocates EUR 387 billion (USD 418 billion) to support climate-smart farming, with eco-schemes rewarding producers who adopt low-emission feed practices, including the use of methane-inhibiting premix additives and nitrogen-efficient amino acid blends. France's Plan Protéines, launched in 2024, offers subsidies covering 40% of the capital cost for on-farm feed mixing equipment, incentivizing livestock operations to purchase concentrated premixes and blend them with locally sourced grains, thereby reducing transport emissions and import dependency. he Netherlands' nitrogen reduction mandate, targeting a 50% cut by 2030, drives dairy farmers toward precision premix formulations that balance rumen-degradable protein with bypass protein, minimizing ammonia volatilization from manure.

Precision-Feeding Digital Twins

Advanced livestock operations in the Netherlands, Denmark, and Germany utilize digital twin platforms that simulate individual animal metabolism, allowing for real-time premix adjustments based on milk yield, growth rate, and health status data streamed from wearable sensors and automated milking systems. Wageningen University's Dairy Digital Twin project, piloted across 50 Dutch farms in 2024, demonstrated that dynamic copper and zinc dosing, recalibrated daily via machine learning algorithms, reduced trace mineral excretion by 18% while maintaining milk production targets. This approach addresses both environmental compliance and cost efficiency, as copper and zinc account for 12% to 15% of the total premix ingredient expense. Danish pork producer Danish Crown partnered with software firm Seges Innovation in 2024 to roll out a swine growth model that predicts optimal lysine-to-energy ratios for each pen, cutting premix waste by 8% and improving feed conversion by 0.12 points.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Europe Union additive regulations | -0.8% | Europe Union-27, most acute in Germany and France | Long term (≥ 4 years) |

| High premix formulation costs | -0.6% | Pan-European, pressure highest in Southern Europe | Medium term (2‒4 years) |

| Vitamin-supply dependence on China | -0.5% | Europe Union-27 with acute exposure in Germany, Netherlands, Poland | Short term (≤ 2 years) |

| Lowered Europe Uniomycotoxin limits raising R&D costs | -0.4% | Europe Union-27, enforcement concentrated in France, Italy, Spain | Medium term (2‒4 years) |

| Source: Mordor Intelligence | |||

Stringent Europe Union Additive Regulations

The European Food Safety Authority's 10-year dossier renewal cycle for feed additives, introduced in 2024, imposes a compliance burden that disproportionately affects smaller premix manufacturers, who often lack in-house toxicology and efficacy testing capabilities. Each renewal dossier costs between EUR 500,000 and EUR 1.5 million (USD 540,000 to USD 1.62 million), a threshold that has already prompted three mid-tier German formulators to exit the market and consolidate into larger entities[2]Source: European Food Safety Authority, “Feed Additives Renewal Requirements,” efsa.europa.eu. France's French Agency for Food, Environmental, and Occupational Health & Safety (ANSES), the national food safety agency, introduced a supplementary national review layer in 2024, requiring French-language documentation and domestic field trials for any additive not previously marketed in the country. This move fragments the single market and raises entry costs for non-French suppliers.

High Premix Formulation Costs

Premix production entails high fixed costs for micro-dosing equipment, quality control laboratories, and inventory management systems that track hundreds of raw material SKUs with varying shelf lives and storage requirements. The capital outlay for a mid-scale premix plant, capable of producing 50,000 metric tons annually, ranges from EUR 15 million to EUR 25 million (USD 16.2 million to USD 27 million), a barrier that limits new entrants and concentrates capacity among established players. Southern European producers in Spain and Italy face additional pressure from higher energy costs, with electricity tariffs for industrial users averaging EUR 0.18 per kilowatt-hour (USD 0.19 per kilowatt-hour) in 2024, 30% above the Northern European average, eroding competitiveness in export markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Aquaculture Premixes Outpace Traditional Livestock

Poultry captured 42.14% of the European feed premix market size in 2025, reflecting the sector's scale, with the Europe Union producing 13.2 million metric tons of poultry meat annually and maintaining 360 million layer hens . Broiler premixes emphasize rapid growth and feed efficiency, incorporating elevated levels of methionine, lysine, and vitamin E to support breast muscle development and immune function. In contrast, layer formulations prioritize calcium, phosphorus, and vitamin D3 to maintain eggshell integrity and laying persistence beyond 80 weeks of age. Turkey premixes represent a smaller niche, concentrated in Germany and France, where producers specify higher niacin and biotin levels to prevent leg disorders in heavy toms.

Aquaculture is the fastest-growing segment, surge at a 6.72% CAGR through 2031, propelled by the expansion of recirculating aquaculture systems in Denmark, the Netherlands, and Scotland, which demand highly digestible micronutrient blends to maintain water quality and fish health in closed-loop environments. Salmon and seabass dominate fin-fish premix demand, requiring astaxanthin for pigmentation and high-potency vitamin C to prevent spinal deformities, while crustacean premixes for shrimp and crayfish incorporate copper and selenium to support molting and disease resistance. The Europe Union 2024 methane reduction roadmap, targeting a 30% cut in enteric emissions by 2030, accelerates the adoption of ruminant premixes containing seaweed extracts and 3-nitrooxypropanol, additives that inhibit methanogen activity in the rumen and qualify for carbon credit schemes.

By Ingredient: Amino Acids Gain as Protein Precision Rises

Vitamins accounted for 37.62% of Europe feed premixes market size in 2025, split between fat-soluble vitamins A, D, E, and K, which stabilize cell membranes and support bone development, and water-soluble vitamins B-complex and C, which drive energy metabolism and stress resilience. Vitamin A remains the single largest line item, used at inclusion rates of 10,000 to 15,000 international units per kilogram in poultry premixes to maintain epithelial integrity and immune response. Vitamin D3 is critical for calcium absorption in layers and dairy cows, preventing rickets and milk fever. Minerals accounted for a substantial share, with macro-minerals like calcium carbonate and dicalcium phosphate providing structural support for bones and eggshells, and trace minerals including zinc, copper, manganese, and selenium serving as enzyme cofactors and antioxidants.

Amino acids expand at 6.45% CAGR through 2031, driven by the Europe Union nitrogen efficiency mandates and the economic logic of replacing expensive soybean meal with crystalline lysine, methionine, threonine, and tryptophan. Lysine, the second-limiting amino acid in swine diets, is increasingly supplied in sulfate form to reduce hygroscopicity and improve flowability in premix blending. Antibiotics, once a staple growth promoter, have declined to trace levels following the Europe Union 2022 ban, with remaining use confined to therapeutic applications under veterinary prescription.

Geography Analysis

Germany commanded 22.18% of the Europe feed premix market in 2025, the largest country share. The country's premix sector benefits from proximity to major ingredient suppliers, including BASF's vitamin complex in Ludwigshafen and Evonik's amino acid plants in Hanau and Wesseling, which reduce logistics costs and enable just-in-time delivery to feed mills. German producers are increasingly specifying premixes containing methane-inhibiting additives to comply with the federal government's 2024 climate protection law, which assigns a carbon budget to livestock operations and levies penalties for exceedances.

Spain posts a 5.55% CAGR through 2031, the fastest country-level growth rate, driven by modernization investments in Catalonia and Aragon, where aging swine facilities are being replaced with climate-controlled barns equipped with automated feeding systems that require precision premixes tailored to real-time growth curves. The acceleration stems from three converging forces: first, the consolidation of fragmented pig farms into 5,000-head operations that justify dedicated nutritionists and custom premix protocols, second, the expansion of vertical integrators like Grupo Fuertes and Vall Companys, which internalize premix blending to capture formulation margins; and third, rising poultry exports to North Africa and the Middle East, markets that demand antibiotic-free certifications achievable only through functional premix strategies.

Italy's premix market, historically fragmented among small regional mills, consolidates as retailers impose traceability requirements that favor larger suppliers with certified quality management systems, a shift that benefits Veronesi and Martini Alimentare, domestic leaders with ISO 22000 and GMP+ certification.

The Benelux region, encompassing Belgium, the Netherlands, and Luxembourg, punches above its geographic weight, hosting ForFarmers, De Heus, and Nutreco, three of Europe's top 10 feed companies, which operate premix plants in Lochem, Ede, and Ghent that serve pan-European customers.

Competitive Landscape

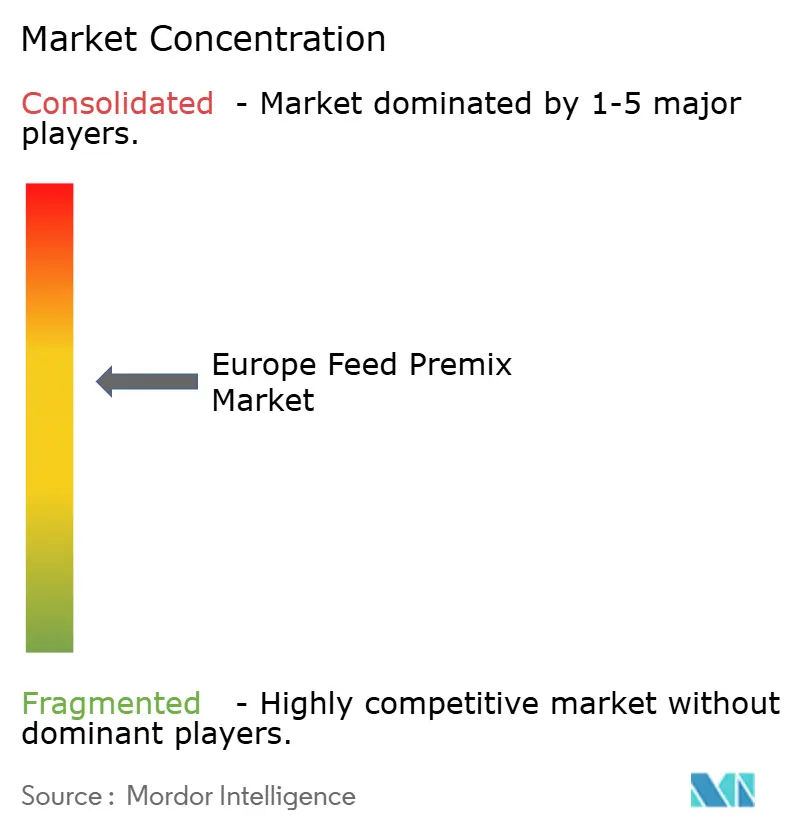

The Europe feed premix market exhibits moderate concentration, with the top five players, DSM-Firmenich N.V., Cargill, Incorporated, Nutreco N.V., ADM, and BASF SE are commanding significant combined revenue share in 2024, a structure that balances scale economies in vitamin and amino acid procurement against regional specialists who tailor formulations to local livestock breeds and regulatory nuances. Vertical integration defines the competitive playbook, as leading suppliers operate captive vitamin synthesis plants, trace mineral chelation facilities, and enzyme fermentation units, insulating margins from spot-market volatility and enabling bundled offerings that combine core micronutrients with functional additives.

Opportunities cluster around organic-certified premixes, where stringent sourcing rules for non-GMO and pesticide-free carriers limit supply, and insect-based formulations, where incumbents lack the entomology expertise to optimize chitin digestibility, creating openings for startups like Ynsect and Protix to partner with traditional feed mills. Technology adoption separates leaders from laggards, with Cargill's 2024 rollout of a cloud-based premix configurator allowing feed mill customers to input real-time milk yield and body condition scores, then receive optimized vitamin-mineral prescriptions within seconds, a tool that deepens customer lock-in and generates data on herd performance trends.

Smaller players, including Kaesler Nutrition and Danish Agro, counter with hyper-local service models, stationing nutritionists on-farm to conduct ration audits and adjust premix specifications weekly, a high-touch approach that commands loyalty in markets where livestock operations distrust algorithm-driven recommendations. The competitive landscape also features enzyme and probiotic specialists, such as Novozymes and Chr. Hansen, who license proprietary strains to premix manufacturers under co-branding agreements, a strategy that transfers R&D risk while capturing ingredient margin.

Europe Feed Premix Industry Leaders

DSM-Firmenich N.V.

Cargill, Incorporated

Nutreco N.V.

BASF SE

Archer Daniels Midland Company (ADM)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: BASF initiated a EUR 80 million (USD 86 million) investment to expand its trace mineral chelation plant in Gunzenhausen, Germany, doubling output of zinc methionine and copper proteinate to meet rising demand for organic mineral premixes. The expansion includes a pilot line for iron amino acid complexes, targeting aquaculture applications.

- September 2024: ForFarmers and Team Agrar, a division of the DLG Group, partnered to operate jointly on animal feed and feed premix in Germany. The resulting joint venture will operate under the name ForFarmers team agar and will offer a comprehensive feed premix portfolio for various animals.

- March 2024: Kemin Industries received EFSA approval for its Clostat probiotic strain, Bacillus subtilis PB6, for use in poultry premixes across Europe Union. The strain demonstrated a 6% improvement in feed conversion ratio in broiler trials conducted in Italy and Spain, positioning Kemin to capture share in the antibiotic-free segment.

Europe Feed Premix Market Report Scope

Feed premixes are mixtures of one or more essential animal nutrients mixed by livestock farmers with home-grown feed to provide their animal's optimum nutrition and other major feed industries in the region. The feed premix market is segmented by Animal Type (Ruminant, Poultry, Swine, Aquaculture, and Other Animal Types), Ingredients (Antibiotics, Vitamins, Antioxidants, Amino Acids, Minerals, and Other Types), and Geography (Spain, United Kingdom, Germany, France, Italy, Russia, and Rest of Europe). The report offers the market size and forecasts in value (USD) for all the above segments.

By Animal Type

| Ruminants |

| Poultry |

| Swine |

| Aquaculture |

| Other Animal Types |

By Ingredient

| Vitamins |

| Minerals |

| Amino Acids |

| Antibiotics |

| Antioxidants |

| Other Ingredients |

By Geography

| Germany |

| France |

| United Kingdom |

| Spain |

| Italy |

| Russia |

| Rest of Europe |

| By Animal Type | Ruminants |

| Poultry | |

| Swine | |

| Aquaculture | |

| Other Animal Types | |

| By Ingredient | Vitamins |

| Minerals | |

| Amino Acids | |

| Antibiotics | |

| Antioxidants | |

| Other Ingredients | |

| By Geography | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe feed premix market in 2026?

The Europe feed premix market size stands at USD 6.16 billion in 2026 and is forecast to reach USD 7.52 billion by 2031 at a 4.06% CAGR.

Which animal segment dominates premix demand?

Poultry holds the largest 42.14% revenue share in 2025 because meat and table-egg supply chains rely on dense vitamin and amino acid supplementation.

What ingredient category is growing fastest?

Amino acids lead growth at a 6.45% CAGR as precision protein nutrition helps producers meet Europe Union nitrogen-efficiency targets.

Which country offers the strongest growth outlook?

Spain posts the fastest country-level expansion, driven by modernized swine and poultry complexes that install automated feeding and precision premix systems.

Page last updated on: