Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

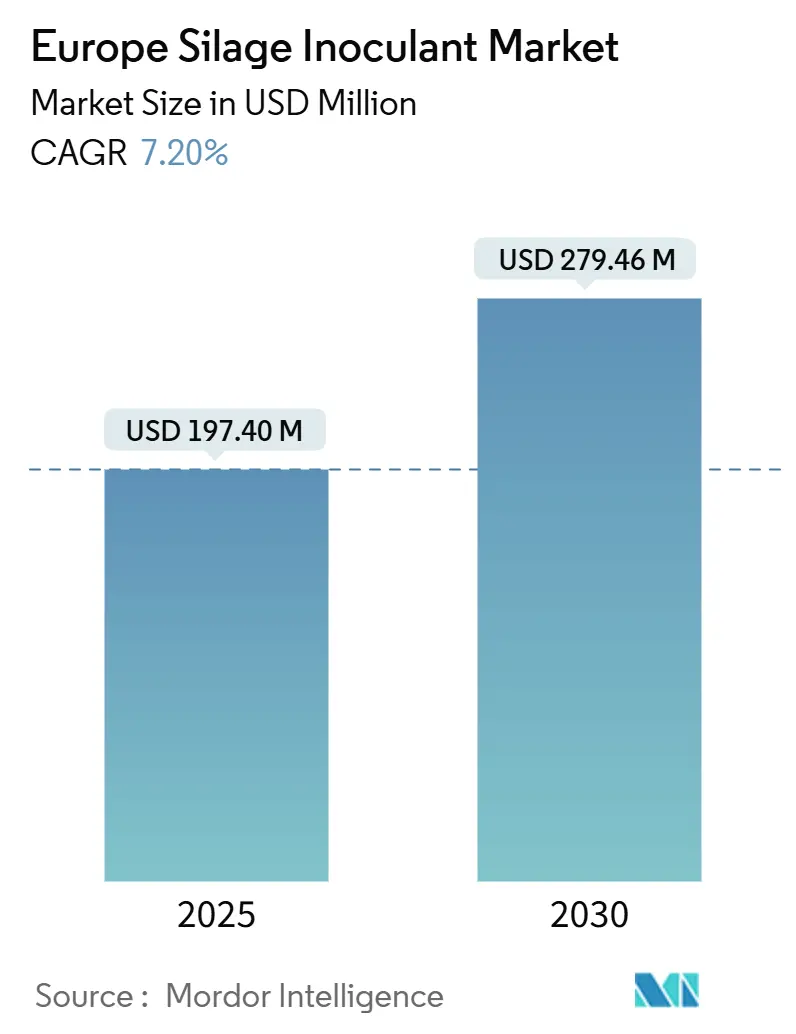

| Market Size (2025) | USD 197.40 Million |

| Market Size (2030) | USD 279.46 Million |

| Growth Rate (2025 - 2030) | 7.20% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Silage Inoculant Market Analysis by Mordor Intelligence

The Europe silage inoculant market size stands at USD 197.4 million in 2025 and is projected to reach USD 279.46 million by 2030, reflecting a 7.20% CAGR over the forecast period. Rising livestock intensification, stricter European Union greenhouse-gas targets, and the wide rollout of precision agriculture platforms collectively create a favorable demand environment. Product innovation now centers on multi-strain blends that enhance aerobic stability, a feature valued in Mediterranean production zones that face warmer feed-out conditions. Market consolidation accelerated in 2024 following the Novozymes-Chr. Hansen merger forming Novonesis, creating a biosolutions powerhouse with an estimated annual revenue of USD 217 million[1]Source: Animal Biosolutions,"Important and Integrated Part' of Novonesis, Says EVP." novonesis.com. Supportive policy instruments, including Common Agricultural Policy (CAP) eco-schemes and national biomethane strategies, further accelerate adoption by shortening payback periods for on-farm fermentation improvements

Key Report Takeaways

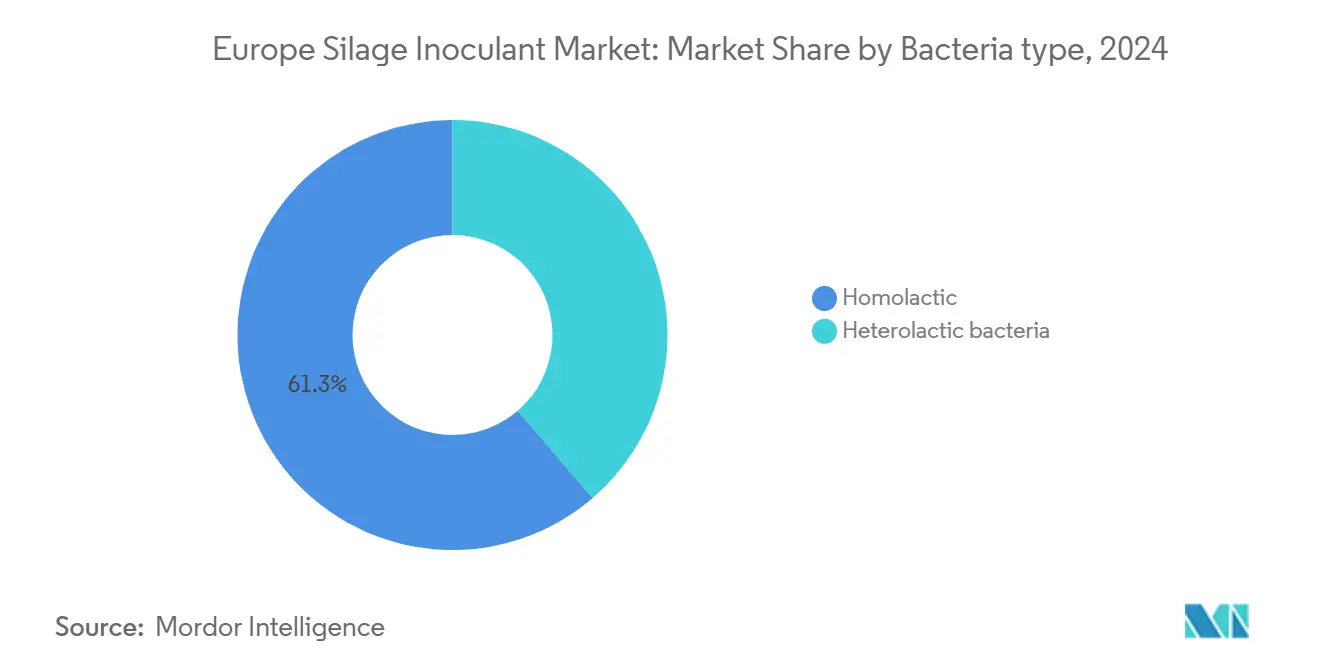

- By bacterial type, homolactic bacteria captured 61.30% of the Europe silage inoculant market share in 2024, while heterolactic bacteria are projected to expand at a 7.80% CAGR to 2030.

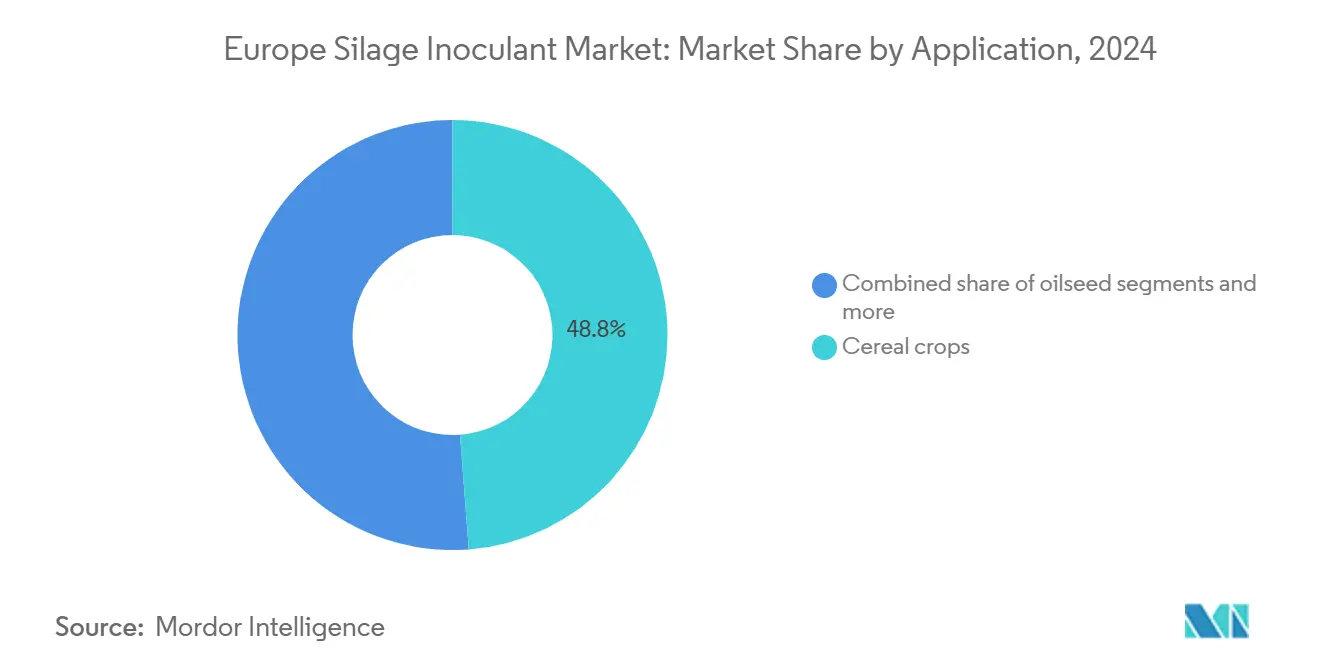

- By application, cereal crops accounted for a 48.80% share of the Europe silage inoculant market size in 2024. Oilseeds are projected to advance at an 8.60% CAGR through 2030.

- By geography, germany led with 24.40% revenue share in 2024, and Spain records the highest projected CAGR at 7.40% through 2030.

Europe Silage Inoculant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of high-quality animal nutrition | +1.2% | Germany, France, and the Netherlands core markets | Medium term (2-4 years) |

| Rising demand for animal protein | +1.0% | Pan-European with Eastern Europe acceleration | Long term (≥ 4 years) |

| Government subsidies for on-farm fermentation efficiency | +0.8% | Europe, and United Kingdom Green Gas Support Scheme | Short term (≤ 2 years) |

| Push for methane-mitigation protocols | +1.1% | European Green Deal compliance | Medium term (2-4 years) |

| Expansion of on-farm biogas plants using silage residues | +0.7% | Germany, Italy, and France biogas clusters | Long term (≥ 4 years) |

| AI-driven crop-specific inoculant prescriptions | +0.4% | Northern Europe digital agriculture leaders | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing adoption of high-quality animal nutrition

European livestock producers increasingly prioritize feed quality optimization as milk prices remain volatile and production costs escalate. Premium silage inoculants enable farmers to preserve higher dry matter content and improve digestibility, directly translating to enhanced milk yields and reduced feed conversion ratios. The German dairy sector exemplifies this trend, where average milk yields reached 8,059 kilograms per cow in 2024, supported by advanced silage preservation techniques. This nutritional focus extends beyond traditional dairy regions, with Eastern European producers adopting similar strategies as they modernize operations to compete in integrated European markets.

Rising demand for animal protein

European protein consumption patterns drive sustained livestock expansion, particularly in poultry and aquaculture sectors, where silage-based feed systems support cost-effective production. Annual European protein consumption is set to rise 2.1% until 2030, sustaining livestock expansion in poultry and aquaculture segments[2]Source: European Food Safety Authority, “Animal Nutrition,” Efsa.europa.eu. This demand surge creates downstream pressure for efficient forage preservation, as feed costs represent 60-70% of total livestock production expenses. Silage inoculants become essential tools for maintaining consistent feed quality year-round, reducing spoilage losses that can reach 15-20% without proper preservation.

Government subsidies for on-farm fermentation efficiency

The Common Agricultural Policy 2023-2027 allocates USD 420 billion across member states, with specific eco-schemes supporting technologies that reduce greenhouse gas emissions from agriculture[3]Source: European Commission, “CAP 2023-27,” EC.europa.eu. France's FranceAgriMer program provides up to USD 43,400 per farm for anaerobic digestion equipment, while Germany's Federal Office for Agriculture and Food offers investment grants covering 40% of eligible costs for fermentation infrastructure. These subsidies directly incentivize silage inoculant adoption by reducing payback periods for improved preservation systems from 3-4 years to 18-24 months.

Push for methane-mitigation protocols

Silage inoculants containing specific bacterial strains can reduce methane emissions during fermentation by 8-12% compared to untreated silage, creating compliance pathways for farms facing carbon pricing mechanisms. The European Methane Strategy targets 35% emission reductions by 2030, positioning silage preservation technology as a cost-effective mitigation tool compared to dietary additives or housing modifications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of premium inoculant blends | -0.9% | Price-sensitive Eastern Europe, smallholder regions | Short term (≤ 2 years) |

| Limited awareness among smallholder and hobby farms | -0.6% | Rural areas across all geographies | Medium term (2-4 years) |

| Post-Brexit regulatory divergence is slowing United Kingdom approvals | -0.3% | The United Kingdom market specifically | Short term (≤ 2 years) |

| Supply-chain exposure to live bacteria cold-chain failures | -0.4% | Distribution-dependent, rural logistics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High cost of premium inoculant blends

Advanced multi-strain products cost USD 1.30-1.63 per metric ton of treated silage, equaling 3% of production costs in some systems. Eastern European producers operating on tighter margins often defer adoption despite demonstrated return on investment ratios of 10:1, particularly when commodity grain prices remain elevated. This cost sensitivity creates market segmentation where basic single-strain products dominate price-conscious segments while premium multi-active formulations gain traction in intensive dairy and beef operations with higher profit margins.

Limited awareness among smallholder and hobby farms

Roughly 10.5 million European farms operate on under 5 ha, many lacking extension services. These producers often rely on traditional preservation methods and may not understand the economic benefits of bacterial inoculants, particularly regarding reduced dry matter losses and improved feed quality. Knowledge transfer mechanisms remain fragmented across member states, with some regions lacking dedicated silage management advisory services that could demonstrate inoculant value propositions to smaller operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bacteria Type: Shift toward Aerobic Stability

Homolactic strains account for 61.30% of the Europe silage inoculant market in 2024, reflecting their rapid pH-reduction capability that suppresses spoilage microbes in high-moisture grass silage. This dominance positions the segment's Europe silage inoculant market size prominently, with established adoption among dairy producers driving consistent incremental growth. However, farms increasingly contend with larger bunker faces and slower daily removal rates, which expose silage to oxygen for longer periods.

Heterolactic blends are therefore growing at a 7.80% CAGR, the fastest in the Europe silage inoculant market, because they generate acetic and propionic acids that inhibit yeasts and molds during aerobic exposure. Trials demonstrate shelf-life extensions of three to five days compared to homolactic-only controls. Mediterranean dairies report feed-out temperature reductions of 6°C, which curbs heat damage and nutrient losses. Suppliers are bundling rapid-fermentation strains with heterofermentative bacteria to capture both pH control and aerobic stability in a single sachet, commanding high price premium.

By Application: Oilseeds Gain Momentum

Cereal crops hold 48.80% share of the Europe silage inoculant market size in 2024. High-dry-matter corn silage remains ubiquitous because it provides concentrated energy to high-yielding dairy cows. Variable harvest moisture and sugar content in cereals provide inoculants with a clear role in reducing fermentation risk, resulting in adoption rates exceeding 70% in Germany and the Netherlands. Pulse crops maintain steady demand as protein sources for livestock rations, while other applications, including root crops and specialty forages, serve niche market segments.

Oilseed silage, chiefly rapeseed and sunflower, is advancing at an 8.60% CAGR and is the most dynamic application in the Europe silage inoculant market. Biodiesel capacity across the European Union increases yearly, and crushers sell deoiled press cake back to the feed chain. Preserving oilseed forage requires specialized inoculants that address elevated lipid content, which can otherwise hamper lactic-acid bacteria growth. Suppliers are formulating high-buffering-capacity blends to stabilize pH in rapeseed silage, opening a premium niche with margins higher than conventional products.

Geography Analysis

Germany represents 24.40% of value sales in 2024 and forms the anchor of the Europe silage inoculant market. The dairy herd numbers are high, and more than half of farms employ GPS-guided harvesters that enable precise inoculant dosing. Germany’s 9,500 biogas units create an additional incentive for well-preserved forage, which maximizes methane yield. Common Agricultural Policy (CAP)-backed incentives channel capital toward fermentation efficiency, reinforcing demand growth. France ranks second, benefitting from integrated cattle systems in Brittany and Normandy, where silage supplies up to half of the annual ration volume.

Regional cooperatives are increasingly bundling inoculant sales with agronomy advice, which is pushing up adoption rates. The country’s biomethane feed-in tariff offers farmers an alternate revenue stream, linking silage quality to energy output. Spain is forecast to compound at 7.40% through 2030, the highest among major economies, as intensive beef and dairy feedlots proliferate in Castilla y León and Aragón. Southern Spain’s hot climate heightens the risk of spoilage, making heterolactic blends particularly attractive.

Italy and the United Kingdom form mature but steadily expanding markets. Italy’s biomethane push under the National Recovery and Resilience Plan finances new anaerobic digesters that depend on high-quality forage. The United Kingdom's growth is tempered by diverging regulatory processes, yet premium dairy enterprises in Northern Ireland and Scotland maintain adoption momentum. Eastern Europe, encompassing Poland, Hungary, and Romania, offers significant white space. Modernization initiatives closely linked to the EU accession drive have sparked interest in cost-effective single-strain products, making the sub-region an emerging battleground for tier-two suppliers.

Competitive Landscape

The Europe silage inoculant market shows moderate fragmentation with the top five suppliers together hold roughly half of the market share, while numerous regional specialists serve localized agronomic niches. Novonesis (Novonesis A/S) holds the largest individual share following its 2024 merger, leveraging 38 research centers and 23 manufacturing sites to shorten product development cycles. Lallemand emphasizes proprietary bacteria such as Lactobacillus buchneri NCIMB 40788, supported by on-farm application audits that boost customer retention. Cargill Inc. and Archer Daniels Midland Company integrate inoculants into broader feed-additive portfolios, using cross-selling to penetrate large accounts.

Strategic moves center on technology differentiation and digital integration. Volac International Limited expanded its Ecosyl line with formulations designed for extended feed-out windows, pairing product sales with moisture sensors that trigger automated dosing recommendations in the year 2024. EW Group GmbH strengthened its animal nutrition position through targeted acquisitions, enlarging strain banks used in inoculant products. Entry barriers remain high because European Registration, Evaluation, Authorisation, and Restriction of Chemicals (REACH) protocols require expensive safety dossiers, favoring incumbents with regulatory expertise.

Collaborations with precision-agriculture platforms create new lock-in mechanisms. Suppliers bundle inoculants with variable-rate applicator software, capturing granular usage data to fine-tune formulations. The resulting feedback loops accelerate strain optimization, cementing competitive advantage among players that can afford continuous R&D investment.

Europe Silage Inoculant Industry Leaders

-

Alltech, Inc.

-

Cargill Inc.

-

Lallemand Inc.

-

Archer Daniels Midland Company

-

Novonesis (Novonesis A/S)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Kemin Industries launched PROSIDIU, a peroxy-acid feed pathogen control product cleared in Brazil and South Asia while filings proceed in Europe and North America.

- March 2024: EW Nutrition acquired the European company BIOMIN BIOSTABIL product line from DSM-Firmenich. The acquisition transfers ownership of an established silage inoculants product line to EW Nutrition and expands its presence across Europe.

- January 2024: The European Commission allocated USD 1.1 billion to German State aid schemes for animal welfare improvement. These policies, along with feed safety regulations and incentives for advanced feed technologies, encourage the adoption of silage inoculants in feed formulations.

Europe Silage Inoculant Market Report Scope

Silage inoculants are additives containing anaerobic lactic acid bacteria (LAB) that are used to manipulate and enhance fermentation in silage. The Europe Silage Inoculant Market is segmented by Type (Homolactic bacteria, and Heterolactic bacteria), Application (Cereal Crops, Pulse Crops, Oilseeds, and Other Applications), and Geography (Spain, United Kingdom, France, Germany, Russia, Italy, and Rest of Europe). The Report Offers Market Estimation and Forecast in Value (USD) for the Above-mentioned Segments.

By Bacterial Type

| Homolactic bacteria |

| Heterolactic bacteria |

By Application

| Cereal crops |

| Pulse crops |

| Oilseeds |

| Other applications |

By Geography

| Germany |

| France |

| United Kingdom |

| Spain |

| Italy |

| Russia |

| Rest of Europe |

| By Bacterial Type | Homolactic bacteria |

| Heterolactic bacteria | |

| By Application | Cereal crops |

| Pulse crops | |

| Oilseeds | |

| Other applications | |

| By Geography | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe silage inoculant market by 2030?

The market is forecast to reach USD 279.46 million by 2030, growing at a 7.20% CAGR.

Which bacterial type holds the largest share in Europe?

Homolactic bacteria led with 61.30% share in 2024, supported by rapid acidification benefits.

Why are heterolactic inoculants growing faster?

They offer superior aerobic stability during feed-out, a critical need in warmer Mediterranean climates, driving a 7.80% CAGR.

Which crop segment is expanding the quickest?

Oilseed silage, notably rapeseed and sunflower, is advancing at an 8.60% CAGR due to biodiesel industry growth.

Which country leads market demand in Europe?

Germany accounts for 24.40% of total revenue, underpinned by its large dairy herd and biogas sector.

How do silage inoculants contribute to methane reduction goals?

Specific bacterial strains cut fermentation-stage methane by up to 12%, supporting compliance with the European Methane Strategy.

Page last updated on: