Cladding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

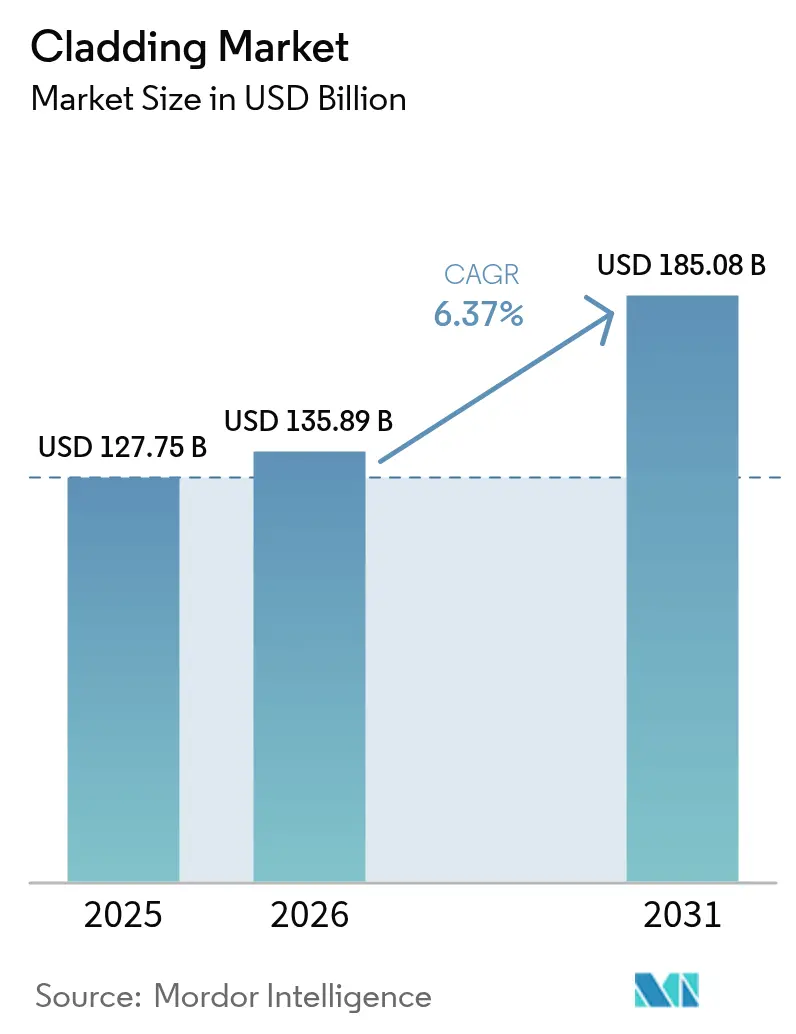

| Market Size (2026) | USD 135.89 Billion |

| Market Size (2031) | USD 185.08 Billion |

| Growth Rate (2026 - 2031) | 6.37% CAGR |

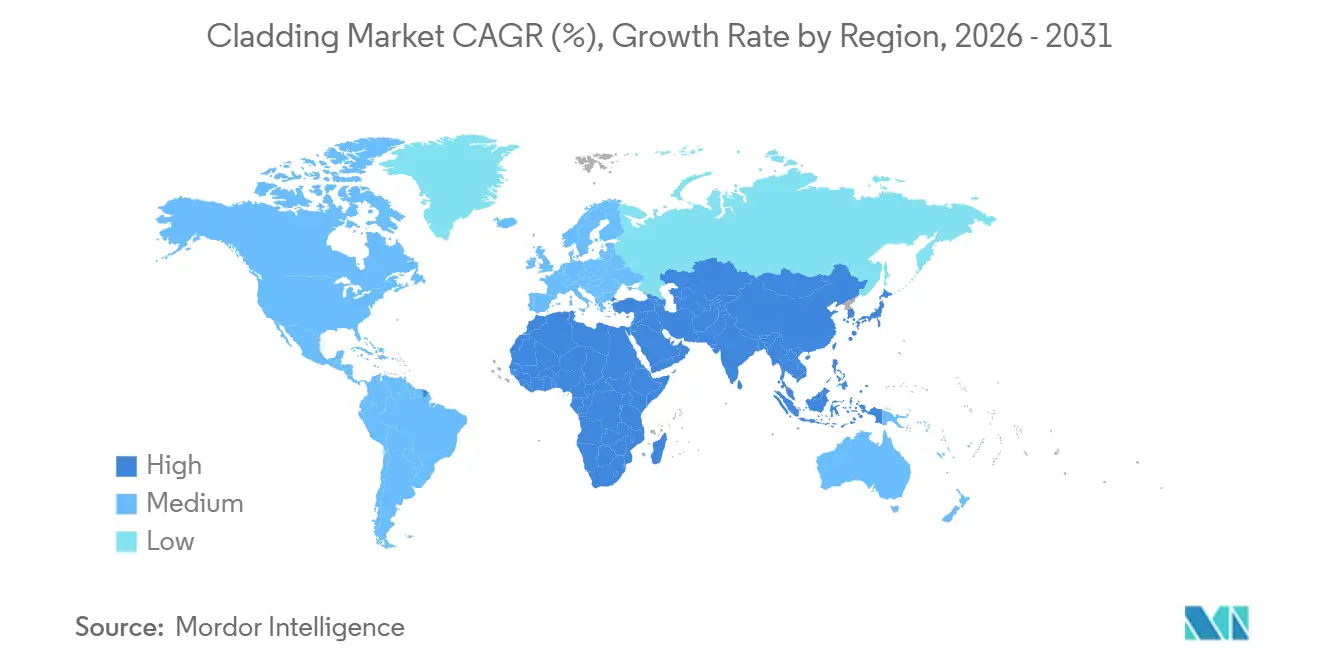

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cladding Market Analysis by Mordor Intelligence

The Cladding Market size is expected to increase from USD 127.75 billion in 2025 to USD 135.89 billion in 2026 and reach USD 185.08 billion by 2031, growing at a CAGR of 6.37% over 2026-2031.

Momentum is building as governments tighten energy-performance codes, insurers press for proven fire resistance, and owners of aging properties shift spending from new builds to façade upgrades. Metal systems still dominate specifications because of durability and high post-consumer recycling rates, yet bio-based solutions are gaining attention as embodied-carbon rules widen. Funding linked to Saudi Arabia’s Vision 2030 pipeline and U.S. Inflation Reduction Act energy-efficiency programs is expanding the addressable base, while rising aluminum and steel premiums continue to squeeze installers’ margins. Digital workflows that connect building-information-modeling (BIM) files directly with panel fabrication are shortening bid-to-field cycles, reinforcing first-mover advantage for suppliers with proprietary configurators.

Key Report Takeaways

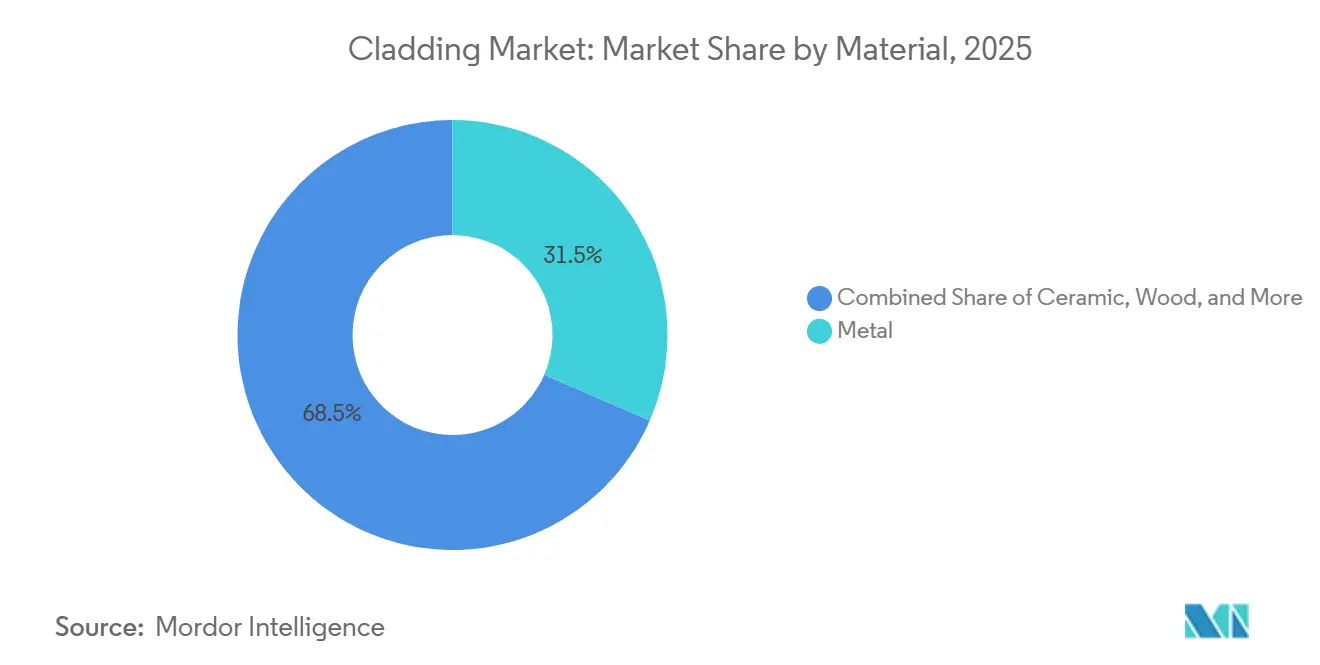

- By material, metal panels held 31.5% of the cladding market share in 2025, whereas wood cladding is forecast to expand at a 6.89% CAGR through 2031.

- By construction type, new construction accounted for 62.3% of the cladding market size in 2025, while renovation is projected to rise at a 6.71% CAGR over 2026-2031.

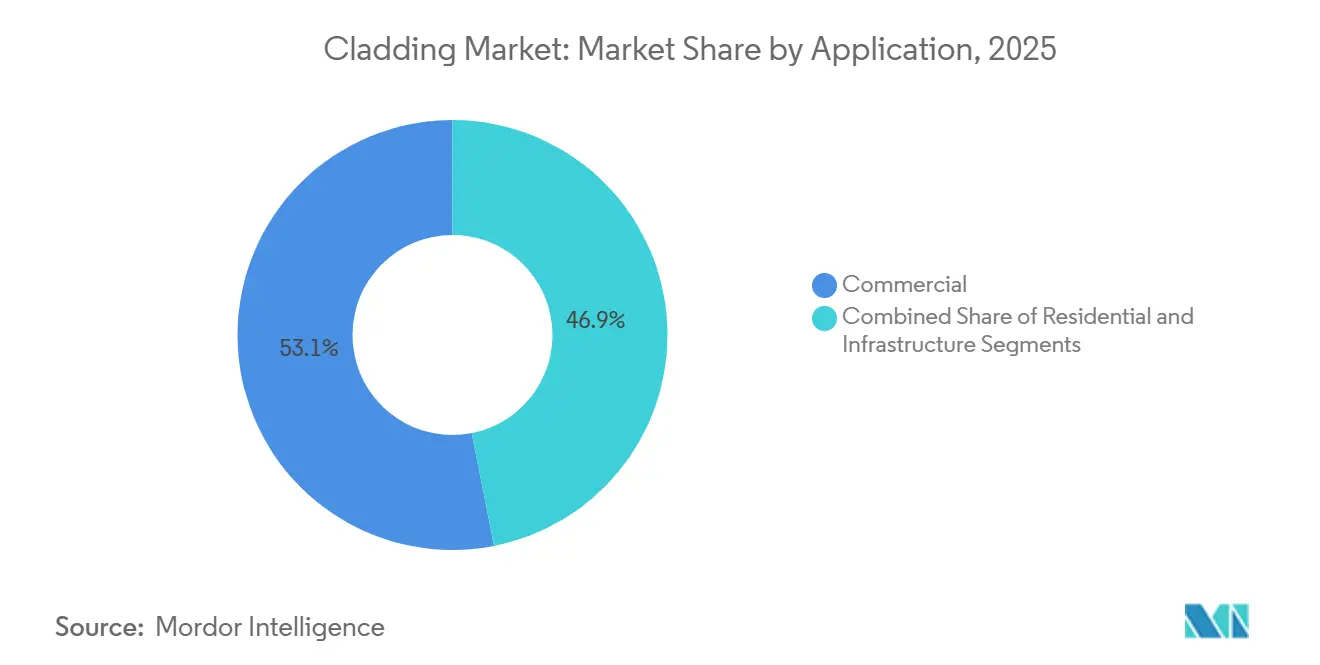

- By application, commercial buildings led with 53.1% revenue share in 2025; residential is expected to post the fastest 6.68% CAGR to 2031.

- By geography, Asia-Pacific captured 35.9% share of the cladding market size in 2025, whereas the Middle East and Africa region is set to grow at a 7.02% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cladding Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficiency upgrades are increasing demand for insulated cladding and rainscreen systems | +1.8% | Europe, North America, China, Japan, South Korea | Medium term (2–4 years) |

| Commercial and high-rise construction growth is boosting exterior-envelope installations | +1.5% | China, India, United Arab Emirates, Saudi Arabia | Short term (≤ 2 years) |

| Stricter fire-safety requirements are accelerating the shift to non-combustible cladding materials | +1.3% | United Kingdom, European Union, Australia, Global | Long term (≥ 4 years) |

| Rising renovation and retrofit activity driving replacement of aging façades | +1.2% | United States, Canada, Western Europe | Medium term (2–4 years) |

| Architectural preference for modern finishes, increasing use of metal, composite, and fiber-cement panels | +0.9% | Urban centers worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficiency Upgrades Increasing Demand for Insulated Cladding and Rainscreen Systems

Governments now tie climate goals directly to building-envelope performance, and that linkage is pulling insulated rainscreens into mainstream procurement. The 2024 recast of the European Union Energy Performance of Buildings Directive obliges member states to renovate the poorest-performing 16% of non-residential stock by 2030, translating into roughly 35 million m² of façades that need new skin every year[1]European Commission, “Energy Performance of Buildings Directive (recast),” europa.eu . Parallel rules in the United Kingdom raised wall U-value limits to 0.18 W/m²K for new projects and 0.26 W/m²K for retrofits, effectively sidelining single-skin assemblies[2]U.K. Department for Levelling Up, “Building Regulations Part L 2024 Amendment,” gov.uk . In the United States, the Department of Energy awarded USD 1.5 million in 2024 to develop MonoInsu, a spray-on retrofit cladding designed for R-5+ thermal resistance, aiming for 30% operational-energy savings in existing homes[3]U.S. Department of Energy, “BTO 2024 Funding Opportunity Selections,” energy.gov . Certification bodies increasingly cite ISO 6946 heat-flow calculations and ASTM C1363 guarded-hot-box tests, making thermal data as critical to bids as aesthetics or price. Taken together, codified performance and grant funding have pushed owners to treat façades as the quickest route to hit 2030 emissions targets.

Commercial and High-Rise Construction Growth Boosting Exterior-Envelope Installations

Large-scale projects across Asia and the Gulf are consuming vast volumes of metal, glass, and composite panels even as some marquee schemes adjust scope. Saudi Arabia’s Vision 2030 capital plan still tops USD 1.3 trillion, with annual construction spending projected at USD 175-181 billion through 2028. While the Line megaproject was trimmed to 2.4 km in late 2024, metro expansions and secondary cities keep orders flowing to façade contractors. The United Arab Emirates surpassed Saudi Arabia in new project awards during 2025 on the back of Expo 2020 legacy work. In India, infrastructure output rose 7.8% year-on-year in December 2025, underpinned by 13.5% growth in cement production and 6.9% growth in steel output. Asia’s long-term need for USD 1.7 trillion per year of infrastructure through 2030, as estimated by the Asian Development Bank, ensures a sustained pipeline for exterior-envelope systems.

Stricter Fire-Safety Requirements Accelerating Shift to Non-Combustible Cladding Materials

Post-Grenfell legislation reshaped acceptable material lists across multiple markets. The United Kingdom banned combustible façades above 18 m in 2018 and extended the trigger height to 11 m in Wales and Scotland by 2024. ISO filled a long-standing gap by publishing ISO 13785-1 and ISO 13785-2 in February 2024, giving manufacturers common intermediate- and large-scale fire-test methods. Timber is re-entering mid-rise designs after Fraunhofer WKI released halogen-free flame-retardant coatings in August 2025 that deliver Euroclass B-s1,d0 classification. Architects, insurers, and lenders now routinely reject aluminum composite panels with polyethylene cores, accelerating switches to mineral wool-filled metal cassettes, terracotta, and non-combustible fiber-cement. As certification cycles lengthen up to 18 months, vendors that clear the new standards early are locking in five-year supply agreements with contractors keen to de-risk bids.

Rising Renovation and Retrofit Activity Driving Replacement of Aging Building Façades

Europe and North America host most of the world’s pre-1980 building stock, and that stock is now central to climate and safety policy. The European Investment Bank approved USD 11 billion in 2024 for deep-energy retrofits that must hit at least 60% savings, often requiring full façade replacement. The UK Building Safety Fund, worth USD 6.5 billion, identified 4,630 buildings needing combustible-panel removal as of December 2024. In the United States, Liatris Inc. secured USD 1.18 million to commercialize clay-cellulose insulated panels that can be installed without displacing occupants, trimming retrofit labor by roughly 25%. Public-sector tenders increasingly bundle solar-ready façades so owners capture operational-energy cuts and renewable-generation credits in the same contract. As financing frameworks reward energy and carbon performance, façade replacement is moving from discretionary spend to regulated necessity.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High material and installation costs are limiting adoption in price-sensitive projects | -0.9% | South America, Africa, Southeast Asia | Short term (≤ 2 years) |

| Volatility in aluminum, steel, and resin input prices is impacting margins and pricing | -0.7% | United States, European Union, China | Medium term (2–4 years) |

| Compliance testing and certification timelines are delaying product approvals and project execution | -0.5% | European Union, United Kingdom, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Material and Installation Costs Limiting Adoption in Price-Sensitive Projects

Cladding packages represent 12-18% of total building shell cost, so inflation in metals and labor quickly cools demand in emerging regions. U.S. construction outlays slipped 0.4% year-on-year in December 2025 as single-family housing weakened. Section 232 tariffs lifted domestic aluminum and steel prices by 1.7-2.2% in the same window, reducing subcontractor margins and prompting shorter quotation validity periods. Canadian housing starts increased 5.6% to 259,028 units in 2025, yet Toronto starts tumbled 31% as buyers waited for interest-rate clarity. Smaller contractors across Latin America and Africa often skip ventilated rainscreens in favor of cheaper stucco or uninsulated masonry, postponing thermal-upgrade benefits. Until governments extend green-financing incentives to private rental developers, uptake in cost-constrained segments will lag.

Volatility in Aluminum, Steel, and Resin Input Prices Impacting Margins and Pricing

Spot premiums on U.S. Midwest aluminum rose above USD 660 per metric ton in November 2024, more than double their 10-year mean, as consumers stockpiled ahead of possible tariff hikes. London Metal Exchange hot-rolled-coil prices whipsawed between USD 650 and USD 750 per metric ton through mid-2025, a range wide enough to erase pricing discipline in lump-sum contracts. The World Bank expects aluminum to settle near USD 2,450 per metric ton in 2026 and steel near USD 730, but even those forecasts carry high bands of uncertainty. Composite-panel producers also wrestle with 8-12% swings in polyethylene and polypropylene resin costs when oil or naphtha markets spike. To cope, fabricators are quoting projects for 15-30 days instead of the historical 90, transferring risk to owners, who in turn defer award decisions and slow pipeline velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Durability of Metal Meets Bio-Based Disruption

Metal retained 31.5% of the cladding market share in 2025, thanks to aluminum and steel panels that combine long service life with easy recycling. Wood, however, is predicted to expand at a 6.89% CAGR to 2031, the fastest clip among all materials, fueled by mass-timber towers that require façade continuity with structural cross-laminated-timber cores. Researchers at Oak Ridge National Laboratory confirmed in 2024 that insulated CLT walls can deliver U-values below 0.20 W/m²K while locking in 200-300 kg of carbon dioxide equivalent per cubic meter. Fraunhofer WKI’s halogen-free intumescent coating, launched in 2025, allows timber façades to meet Euroclass B-s1,d0, easing insurer concerns for mid-rise installations. The cladding industry is watching whether North American code bodies accept similar large-scale fire tests over the next two years, a decision that could extend bio-based momentum to Chicago and Vancouver markets. For now, metal remains the default for high-rise façades, especially where owners value low maintenance and proven fire ratings.

Ceramic, brick, and stone stay niche, appealing mainly to heritage restorations and prestige mixed-use sites. Within composites, fiber-cement is consolidating around larger platforms: James Hardie’s USD 8.8 billion bid for AZEK in 2025 signals a pivot toward integrated exterior-envelope offerings that combine siding, trim, and decking under one roof. Vinyl, dominant in 1990s U.S. suburbs, is retreating as municipalities bake lifecycle-carbon metrics into façade guidelines. Glass curtain walls continue to headline commercial skylines but rarely compete on price with opaque rainscreens that now reach similar daylighting ratios through strip windows.

By Construction Type: Renovation Narrows the Gap

New construction maintained 62.3% of the cladding market size in 2025, yet renovation is forecast to post a 6.71% CAGR between 2026 and 2031, faster than greenfield activity. The European Union’s Renovation Wave aims to double annual retrofit rates to 2% by 2030, a target that transforms façades into the linchpin of decarbonization financing. U.S. retrofit innovators such as MonoInsu promise to install R-5+ insulated skins directly over aged vinyl or asbestos cement without tenant relocation, trimming install costs by roughly one-quarter. That value proposition resonates with owners facing higher interest rates that make demolition-rebuild economics less attractive.

Greenfield pipelines still rely on government agendas for megaprojects and on e-commerce logistics hubs that require fast-track envelopes. ConstructConnect forecasts 4.1% growth in U.S. non-residential starts during 2025, powered by data centers and advanced-manufacturing facilities. Canadian rental housing starts hit a record 43% share of total new units in 2025, and builders there increasingly specify fiber-cement rainscreens for aesthetics and durability. However, renovation’s policy-driven certainty is luring large contractors to pivot crews toward recladding programs that carry less demand volatility than speculative offices.

By Application: Residential Catches Up to Commercial

Commercial buildings generated 53.1% of 2025 demand, backed by office towers, mixed-use precincts, and institutional projects. Yet residential is set to advance at a 6.68% CAGR to 2031 as planners encourage higher-density housing with modern façades that outperform legacy vinyl on both thermal and visual metrics. Canada’s surge in purpose-built rental starts, up to 43% of all new units, exemplifies the shift toward mid-rise apartment blocks that favor panelized cladding over traditional brick. In the United States, multifamily permits rose 3% year-on-year in February 2025, even as single-family permits slipped 6%, underscoring the trend toward urban infill.

Commercial outlooks vary by sub-sector. U.S. office vacancy exceeded 19% in key metros by late 2025, stalling speculative towers and nudging retrofit budgets toward repositioning older glass façades with hybrid opaque-vision systems. Logistics developers, by contrast, continue to demand insulated metal panels (IMPs) that merge speed of erection with R-value compliance for cold-chain operations. Infrastructure projects in Asia—airports, metro stations, stadiums—remain a small but growing slice of the cladding market, propelled by India’s metro-rail push and Southeast Asia’s aviation upgrades.

Geography Analysis

Asia-Pacific held 35.9% of 2025 revenue, owing to China’s still-sizable infrastructure queue and India’s 7.8% year-on-year infrastructure output growth in December 2025. Yet financing headwinds in China’s private-developer segment and reviews of Belt and Road Initiative projects are tempering forward order books. India’s federal capital expenditure jumped 92% in fiscal 2024-25, funneling funds into metro expansions and affordable housing that specify metal and fiber-cement rainscreens. Southeast Asian nations continue to attract Chinese and Japanese contractors for airport and high-speed rail stations, but payment certainty dictates that many material suppliers insist on letters of credit before shipping.

The Middle East and Africa are forecast to register the fastest 7.02% CAGR through 2031, powered by Saudi Arabia’s Vision 2030 commitments and the United Arab Emirates’ post-Expo tourism build-out. Saudi outlays remain high—USD 175-181 billion per year—yet planners have trimmed marquee schemes such as The Line and shelved the Mukaab cube, reallocating spend to transport corridors and industrial zones that still require robust metal-panel envelopes. The UAE captured the most new awards in 2025, and its contractors often specify mineral-wool-core aluminum cassettes that meet regional fire-code updates. Sub-Saharan Africa, led by Nigeria and South Africa, shows modest façade demand concentrated in high-end commercial hubs where currency swings and import tariffs raise landed costs for European or Gulf suppliers.

Europe and North America are pivoting toward renovation as climate legislation and fire-safety statutes accelerate recladding cycles. The European Union’s directive to upgrade the poorest non-residential buildings by 2030 opens a recurring pipeline of roughly 35 million m² of façades each year. The United Kingdom’s Building Safety Act, in tandem with PAS 9980:2022, effectively bans combustible panels on structures over 11 m, driving wholesale replacement demand. U.S. construction spending slipped 0.4% in December 2025, but federal energy-efficiency grants cushion retrofit activity in multifamily and public buildings. Canada’s overall starts rose 5.6%, yet regional divergence persists as Toronto volumes dropped on affordability issues while Alberta’s energy corridor posted gains. South America remains smaller; Brazil’s USD 200 million Bahia Sustainable Project illustrates how multilateral loans are inching towards public-sector procurement.

Note: Segments share of all individual segments available upon report purchase

Competitive Landscape

The ten largest vendors collectively account for a significant share of the cladding market revenue, indicating moderate concentration with robust regional fragmentation. Vertical integration is the primary defense: Kingspan manufactures both insulation cores and finished panels, enabling 48-hour lead times on bespoke orders. Compagnie de Saint-Gobain deepened its Asia-Pacific exposure by purchasing CSR Limited for USD 3.0 billion in 2024, folding fiber-cement and plasterboard into an existing gypsum and glass portfolio. James Hardie’s USD 8.8 billion offer for AZEK in 2025 would create a cross-channel platform spanning fiber-cement siding and polymer-composite decking, giving large builders a single point of contact for entire exterior envelopes.

Technological capability is increasingly the battleground. Arconic and Tata Steel have invested in continuous coil-coating lines that apply fire-retardant and self-cleaning finishes in one pass, trimming downstream labor. Rockwool and Dow are collaborating to embed proprietary insulation cores into metal panels, locking in multi-year supply deals with contractors who prefer single-warranty systems. Digital configurators that plug directly into Revit or Archicad are capturing specification influence early, a shift that rewards firms like Kingspan and Trespa with large libraries of parametric objects.

Chinese challengers such as Guangzhou Xingfa Aluminium and Yaret Industrial Group are exporting aluminum extrusions at 20-30% price discounts, but inconsistent documentation for ISO 13785 fire tests limits acceptance on Grade-A commercial towers. Start-ups in Scandinavia and the U.S. are commercializing bio-based composites that combine flax fibers with mineral binders to meet non-combustibility requirements, yet scaling beyond boutique volumes remains a hurdle. Overall, incumbents that pair in-house testing capacity with diversified material portfolios appear best placed to manage regulatory and raw-material volatility.

Cladding Industry Leaders

Kingspan Group

Compagnie de Saint-Gobain SA

Arconic Corporation

Etex Group

Tata Steel Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Fraunhofer WKI unveiled halogen-free flame-retardant coatings that give timber façades Euroclass B-s1,d0 ratings.

- April 2025: The World Bank approved a USD 200 million loan for the Bahia Sustainable and Inclusive Project, including façade upgrades.

- March 2025: James Hardie offered USD 8.8 billion to acquire AZEK, aiming to build an integrated façade, trim, and decking platform.

- December 2024: EBRD allocated USD 22 million to retrofit public buildings in Kosovo with insulated façades and photovoltaics.

Global Cladding Market Report Scope

| Ceramic |

| Wood |

| Brick and Stone |

| Metal |

| Others (Stucco, Glass, Fibre Cement, Vinyl) |

| New Construction |

| Renovation |

| Commercial |

| Residential |

| Infrastructure |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Material | Ceramic | |

| Wood | ||

| Brick and Stone | ||

| Metal | ||

| Others (Stucco, Glass, Fibre Cement, Vinyl) | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Application | Commercial | |

| Residential | ||

| Infrastructure | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

How great will global cladding demand be by 2031?

The cladding market size is expected to reach USD 185.08 billion by 2031, reflecting a 6.37% CAGR over 2026-2031.

Which material currently commands the biggest share?

Metal systems led with 31.5% of 2025 revenue due to durability, recyclability, and ready compliance with fire codes.

What is driving the surge in façade renovation?

EU and U.K. regulations now require energy-efficient and non-combustible envelopes on existing stock, while U.S. and Canadian grant programs help owners finance deep retrofits.

Why are aluminum and steel prices such a concern for façade contractors?

Spot premiums rose sharply in 2024-2025, forcing suppliers to shorten bid validity and pass cost risk to project owners.

Which region is expected to grow fastest through 2031?

The Middle East and Africa are projected to post a 7.02% CAGR, fueled by Saudi Vision 2030 and the UAEs ongoing tourism and logistics projects.

How are vendors responding to stricter fire tests?

Leading producers invest in ISO 13785-compliant labs and roll out mineral-core panels, while timber specialists apply new flame-retardant coatings that achieve Euroclass B-s1,d0 ratings.

Page last updated on: