Europe Embedded Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.05 Billion |

| Market Size (2026) | USD 4.11 Billion |

| Market Size (2031) | USD 18.29 Billion |

| Growth Rate (2026 - 2031) | 34.80% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Embedded Insurance Market Analysis by Mordor Intelligence

The Europe embedded insurance market size is expected to grow from USD 3.05 billion in 2025 to USD 4.11 billion in 2026 and is forecast to reach USD 18.29 billion by 2031 at 34.8% CAGR over 2026-2031. This acceleration mirrors the region’s maturing digital infrastructure, regulatory modernization, and consumer preference for friction-free protection that travels with every digital interaction. Online distribution maintains overwhelming primacy as API-driven platforms push insurance from an optional add-on to an invisible feature, while buy-now-pay-later (BNPL) adoption strengthens attachment rates in personal lines. Traditional carriers defend relevance by white-labeling capacity for fintechs at the point of sale, yet they face intensifying competition from specialist providers offering micro-ticket cover through single-call integrations. Harmonized data-sharing frameworks under PSD3 and the Financial Data Access Regulation (FIDA) promise richer underwriting inputs, positioning embedded protection as a foundational layer of Europe’s fintech stack.

Key Report Takeaways

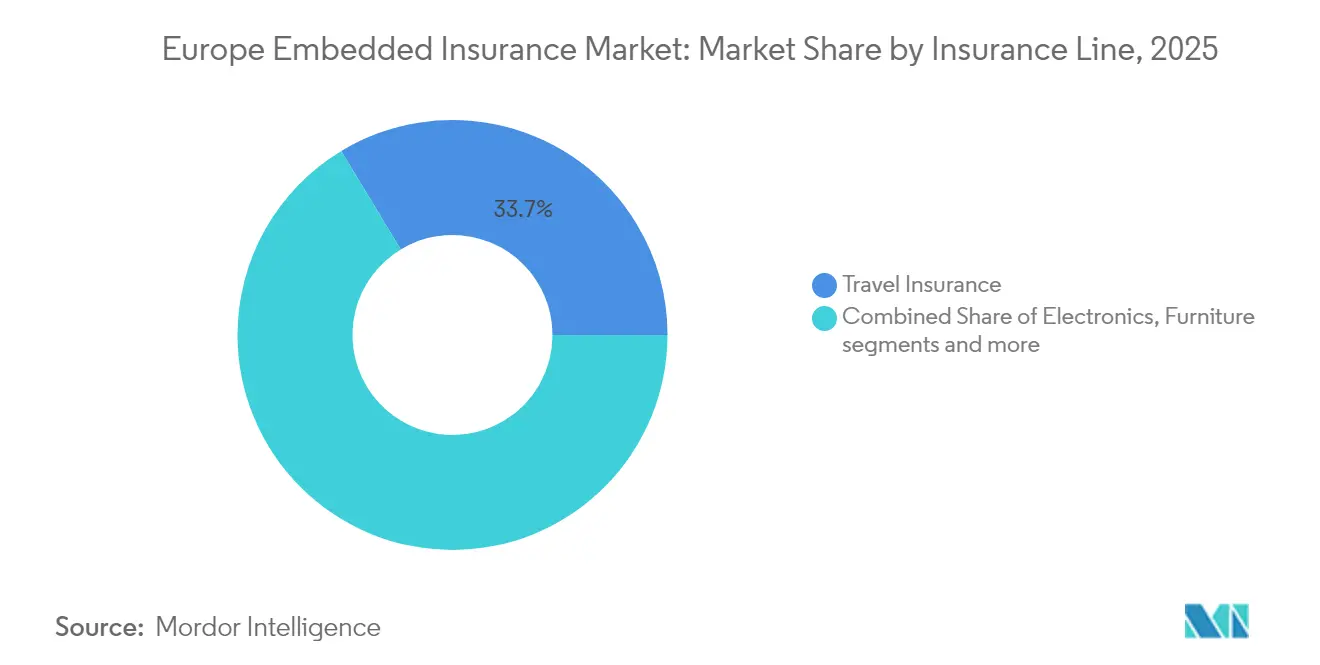

- By insurance line, travel products held 33.65% of the Europe embedded insurance market share in 2025. Electronics protection is projected to grow at a 35.72% CAGR through 2031, the fastest among all insurance lines.

- By distribution channel, online platforms captured 93.10% revenue share of the Europe embedded insurance market size in 2025. Offline channels are forecast to expand at only 6.2% CAGR to 2031, underscoring sustained digital dominance.

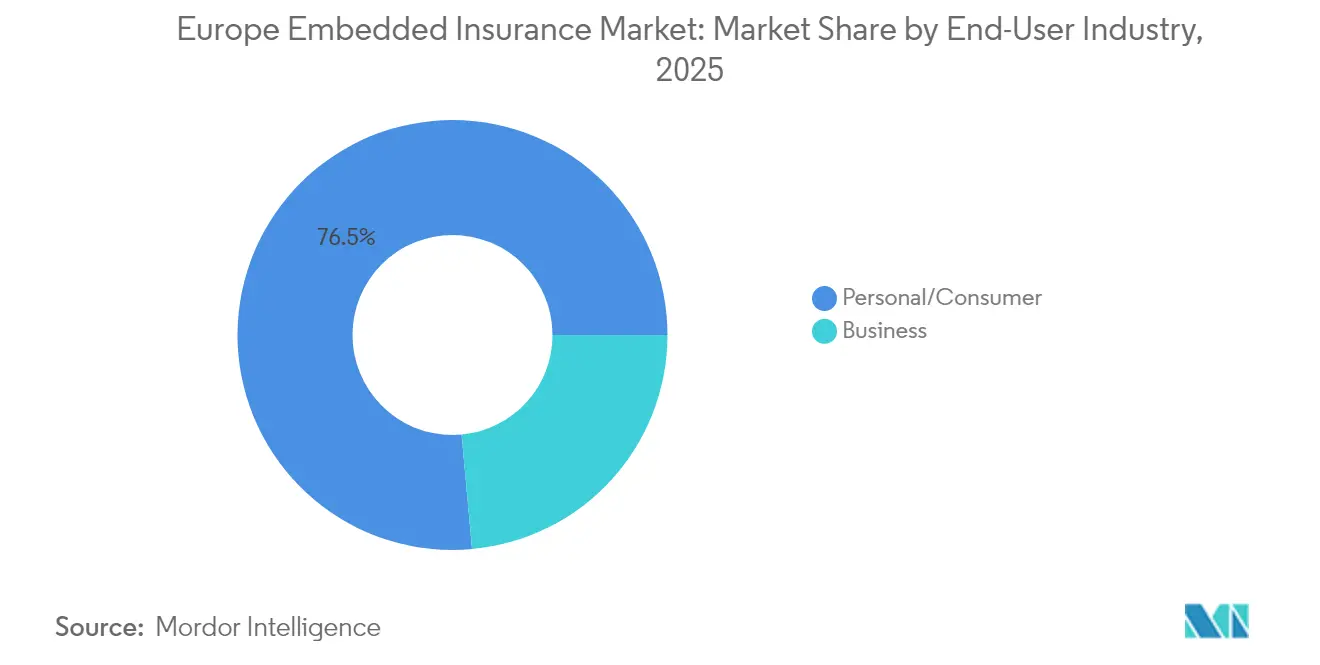

- By end-user industry, personal and consumer applications commanded 76.45% of the Europe embedded insurance market in 2025. SME-focused offerings are advancing at 26.3% CAGR through 2031, outpacing large-corporate adoption.

- By geography, the United Kingdom led with 17.30% of the Europe embedded insurance market share in 2025. Spain is advancing at a region-best 37.6% CAGR through 2031, reflecting rapid fintech adoption.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on embedded insurance market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Embedded Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BNPL-driven electronics protection surge | +8.2% | Northern Europe, Germany, France | Short term (≤ 2 years) |

| EU Digital Finance Package & PSD3 mandates | +6.8% | EU-wide; strongest in Germany, France, the Netherlands | Medium term (2-4 years) |

| E-commerce push for recurring ancillary gain | +7.1% | The UK, Germany, France, and Spain | Short term (≤ 2 years) |

| API-first insurer-fintech integration | +5.9% | The UK, Germany, Nordics | Medium term (2-4 years) |

| OEM data-sharing for pay-per-use pricing | +4.3% | Germany, France, the UK | Long term (≥ 4 years) |

| Cross-border passporting under Solvency II | +3.4% | EU-27, excluding the UK | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of BNPL-Driven Electronics Coverage

BNPL penetration reached 25% in Sweden and 19.7% in Germany during 2024, creating natural insurance touchpoints at checkout that exceed attachment rates in traditional retail. Electronics replacement-cost inflation heightens consumer sensitivity to device downtime, making low-friction cover appealing. Digital banks such as N26 bundle EUR 4 (USD 4.16) monthly protection, while platform providers like Extend report 40% take-up on shipping cover and 15% on product cover across Europe[1]N26 GmbH, “N26 Insurance Products,” n26.com. CCD II transparency rules standardize disclosures, smoothing cross-border rollout. Northern Europe benefits first because BNPL usage skews highest, cementing early-mover advantage for platforms that integrate insurance during financing rather than post-purchase.

Rise of EU Digital Finance Package & PSD3 Mandates

The EU Digital Finance Package extends open-banking logic to insurance, granting regulated parties consent-based access to account and claims data. PSD3 harmonizes authentication standards, while FIDA will enforce interoperability by 2026. Together, they permit real-time underwriting, micro-duration policies, and dynamic pricing at the moment of need. Effective January 17, 2025, the Digital Operational Resilience Act (DORA) imposes stringent operational resilience mandates, favoring established tech platforms adept at meeting high cybersecurity and operational continuity benchmarks. This regulatory alignment is especially advantageous for the markets in Germany, France, and the Netherlands, where the digitization of financial services is propelling European adoption trends.

E-commerce Platforms’ Shift to Recurring Ancillary Revenue

European e-commerce platforms are turning to embedded insurance to generate recurring revenue, helping to counteract the margin compression seen in their primary retail operations. This shift underscores a larger trend in platform economics, highlighting insurance premiums can offer stable cash flows, regardless of transaction volume fluctuations. Qover’s partnership with Revolut illustrates how purchase protection converts one-time card spending into recurring revenue when priced per package rather than per transaction. TaskRabbit embeds gig-worker liability insurance at onboarding, turning a compliance cost into a loyalty feature. GDPR obligations create entry barriers; only marketplaces with strong data governance can safely store claims-related personal data across multiple jurisdictions. Investors reward this model because revenue scales with user base, not inventory turnover.

API-First Insurer–Fintech Partnerships Accelerating Go-Live Speed

API-first integration architectures are slashing embedded insurance deployment timelines from months to mere weeks, reshaping the economic dynamics between insurers and their distribution platforms. Gone are the days of traditional integration methods that relied on custom development and protracted testing. Now, standardized API frameworks pave the way for swift product launches. Zurich’s April 2025 alliance with Ominimo launched AI-tuned motor insurance across three countries within eight weeks, validating the template. Allianz Partners’ tie-up with Cosmo Connected demonstrates similar agility in micromobility cover. Speed matters because launch timing often dictates platform selection; distributors prefer insurers that can co-ship with their own feature releases. Nordic markets benefit disproportionately due to mature payment and identity rails that simplify KYC orchestration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented national MGA licensing | −4.7% | EU-wide; acute in Germany, Italy | Medium term (2-4 years) |

| Low attach-rate in furniture & luxury goods | −2.8% | Western Europe, the UK, and France | Short term (≤ 2 years) |

| Consumer data-privacy backlash | −3.9% | Germany, France, the Netherlands | Short term (≤ 2 years) |

| Re-insurance capacity tightening | −2.1% | EU-wide; London market | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented National Licensing for MGA Structures

Managing General Agent (MGA) licensing requirements vary widely across Europe, creating operational challenges that limit embedded insurance scalability. Germany's BaFin, France's ACPR, and Italy's IVASS enforce distinct frameworks, complicating pan-European operations. Brexit exacerbates this fragmentation, as UK-based MGAs lost EU passporting rights, requiring costly subsidiaries or complex branch structures. Smaller insurtech platforms face significant compliance burdens, giving established carriers with European footprints a competitive edge. Embedded insurance partnerships further intensify challenges, as MGAs must navigate varying consumer protection standards, capital requirements, and supervisory expectations, often necessitating jurisdiction-specific legal entities that increase costs and risks.

Consumer Data-Privacy Backlash After High-Profile Leaks

High-profile data breaches, such as General Motors alleged unauthorized sharing of driver behavioral data with LexisNexis Risk Solutions, have increased European consumer skepticism toward data collection in embedded insurance. April 2024 litigation highlighted unauthorized collection of acceleration, braking, and late-night driving data, exposing reputational risks for providers. GDPR awareness has made consumers more critical of offerings requiring extensive personal data. February 2025 European Court of Justice ruling in C-203/22 further complicates matters by mandating detailed disclosures on how personal data influences pricing[2]Court of Justice of the European Union, “Judgment in Case C-203/22,” curia.europa.eu. This regulatory tightening, especially in privacy-conscious markets like Germany, France, and the Netherlands, creates challenges for customer acquisition and data-driven underwriting.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Line: Electronics Cover Gains Momentum

Travel policies generated the largest slice of premium at 33.65% in 2025, yet electronics protection is on track to post a market-leading 35.72% CAGR, expanding the Europe embedded insurance market size for device cover faster than any peer line. Attachment flourishes because BNPL checkout flows surface insurance as an optional tick box timed precisely to consumer liability concerns. The shifting mix pressures travel incumbents to modernize distribution through single-trip micro-policies tailored to age-specific mobility patterns. Furniture, sports equipment, and pet lines contribute niche but growing pockets that round out platform offerings. As device-as-a-service models proliferate, embedded protection converts depreciation anxiety into predictable revenue, reinforcing electronics’ climb within the product hierarchy.

Mandatory return schemes, part of e-waste regulations, heighten the perceived hassle of replacing electronics. This, in turn, promotes a preference for repair-first coverage. These schemes encourage consumers to consider repairing their devices before opting for replacements, aligning with sustainability goals. Brands are now intertwining their marketing narratives, positioning insurance not just as a safety net but as a commitment to sustainability and lifecycle stewardship. By co-marketing protection plans with sustainability initiatives, companies are reshaping consumer perceptions of product lifecycles. As a result, electronics are garnering significantly more attention compared to traditional categories, which typically have longer replacement cycles.

By Distribution Channel: Digital Pre-eminence Intensifies

Online distribution held a 93.10% share in 2025, anchoring the Europe embedded insurance market. A 35.1% CAGR through 2031 sustains this hegemony as open-banking APIs normalize real-time quote-to-bind in under two seconds. Offline brokers remain relevant for commercial marine and specialty aviation lines where bespoke wording matters, but their consumer footprint shrinks. The Europe embedded insurance market size attributable to brick-and-mortar is projected to slip below USD 320 million by 2031. Platforms deploy in-app claim-filing and instant-refund tools that reinforce digital stickiness, while regulators push e-ID frameworks that streamline onboarding. Consequently, distributors without native mobile presence struggle to preserve volume.

In France and Germany, sovereign-cloud mandates compel hyperscale companies to run local data centers. This requirement ensures compliance with regional regulations and addresses earlier concerns about latency in full-stack digital issuance. These infrastructure advancements significantly enhance operational efficiency and reliability. As a result, the importance of physical touchpoints continues to diminish, with the exception of intricate business classes that still rely on them.

By End-User Industry: Consumer Centricity Endures

Personal lines comprised 76.45% of 2025 premiums and will sustain a 34.95% CAGR as lifestyle apps, neobanks, and BNPL providers incorporate risk cover into everyday experiences. SME propositions lag because procurement gates lengthen sales cycles and require board-level approval, dampening the immediacy central to embedded value. Even so, the Europe-embedded insurance market share for SME bundles is inching upward, aided by banks embedding business interruption or cyber cover into account packages. Consumer momentum benefits from gamified risk-prevention nudges that deepen engagement and reduce loss ratio, an outcome investors reward with higher valuations.

Regulatory guardrails diverge: consumer disclosures must meet IDD pre-contractual requirements, while corporate buyers enjoy greater negotiating flexibility. This divergence significantly influences product architecture. Platforms are required to uphold two distinct underwriting stacks to address these differences. One stack is rules-intensive and tailored for personal lines, ensuring compliance with stringent regulations. The other is a lighter, API-callable engine designed specifically for micro-SME bundles, offering greater adaptability.

Geography Analysis

The United Kingdom controlled 17.30% of the 2025 premium, leveraging its open-banking maturity and dense insurtech cluster around London. The United Kingdom leverages a sophisticated fintech ecosystem, but the loss of EU passporting compels additional licensing steps for continental expansion. QBE established a Belgian base to preserve freedom of services, while Lloyd’s Brussels writes specialty risks on behalf of syndicates. London retains appeal for complex placement due to its deep capital pools, ensuring the city’s relevance even as embedded distribution shifts routine personal lines online.

Germany offers fertile ground, given the household preference for comprehensive cover. BaFin’s stricter solvency tests raise barriers yet create trust in domestic underwriters. High BNPL penetration supplies ready distribution for device and ticket-cancellation insurance. The Digital Operational Resilience Act elevates cybersecurity standards; carriers able to certify compliance early gain marketing leverage over slower rivals.

Spain will register the fastest expansion at 37.6% CAGR, lifting its slice of the Europe embedded insurance market by more than 4% by 2031. Spain’s momentum reflects national strategies to digitize financial services and attract foreign fintech investment. Lower historical insurance penetration means embedded offerings fill genuine protection gaps rather than cannibalize existing policies. Regulatory modernization under Spain’s FinTech Sandbox accelerates product testing, compressing time to market relative to peer states.

France’s bancassurance giants, notably Crédit Agricole, bundle auto, home, and health cover into banking apps, defending share against neobank challengers. PSD3 alignment and a well-developed TPP ecosystem ensure continued innovation. Italy, meanwhile, uses mandatory catastrophic cover to inject new premiums into mortgage transactions, giving banks another embedded upsell opportunity. Nordic countries continue to pilot usage-based mobility cover tethered to national digital-ID schemes, making them test beds for pan-EU rollouts.

Competitive Landscape

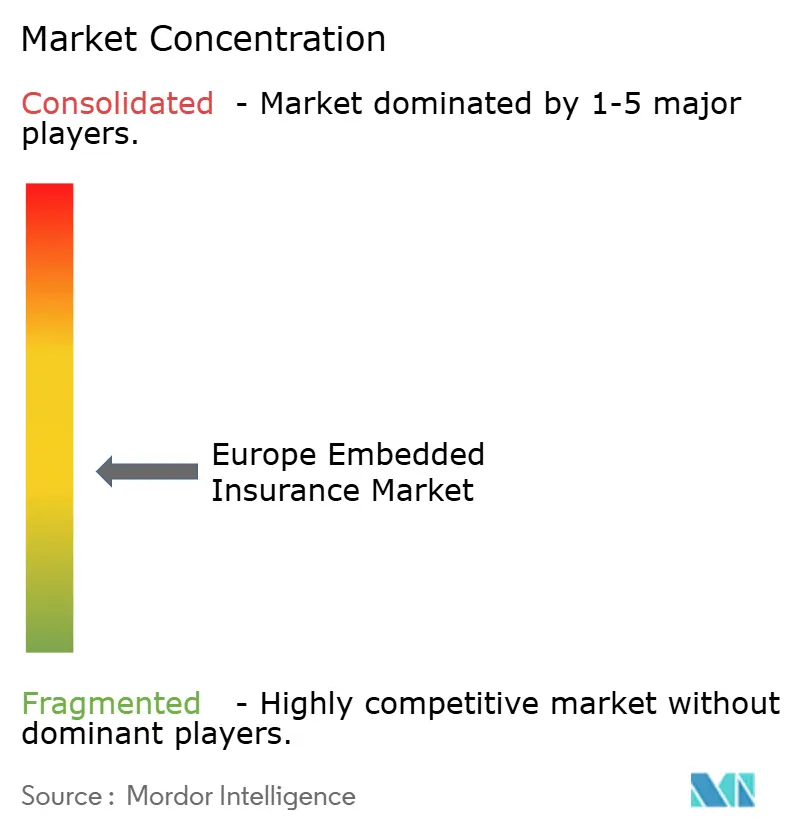

The Europe embedded insurance market maintains moderate concentration: the top five carriers control about 48% of premiums but face nimble Insurtech’s specializing in narrow verticals. Zurich, Allianz Partners, and AXA Partners activate network effects by plugging into banking super-apps and ride-share platforms. Qover, Cover Genius, and Simplesurance differentiate via flexible API orchestration layers that sit between carrier capacity and merchant checkout flows.

Munich Re’s USD 2.6 billion acquisition of Next Insurance underscores reinsurers’ appetite for distribution playbooks. Tokio Marine closed a strategic stake in French MGAs to secure an embedded share in mobility. Strategic alliances outnumber outright takeovers because carriers prefer optionality amid evolving regulations. Technology remains critical: white-label portals that expose pre-integrated product catalogs increase partner stickiness and reduce switching incentives.

Capital strength still matters; large balance sheets absorb start-up volatility in micro-ticket lines where claim frequency can spike. Yet regulatory moats narrow as cloud-native compliance services let smaller MGAs pass supervisory audits without large back-office teams. The decade to 2030 will likely witness further convergence where incumbent carriers acquire front-end tech while offering their licenses as rails for third-party brands.

Europe Embedded Insurance Industry Leaders

Allianz Partners

Cover Genius

AXA Partners

Qover

Zurich Insurance Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Munich Re finalized its USD 2.6 billion takeover of Next Insurance, integrating SME-focused embedded solutions into ERGO’s continental channels.

- January 2024: German carriers projected aggregate premiums to reach EUR 250 billion (USD 260.3 billion) in 2025, attributing growth to expanded embedded distribution and digital-first direct channels.

- January 2025: Zurich Insurance purchased a GBP 150 million (USD 188.4 million) stake in M&A specialist Icen Risk, broadening its embedded transaction cover portfolio across European corporate finance workflows.

- January 2025: Wefox raised EUR 170 million (USD 177 million) led by Searchlight Capital and divested its Liechtenstein insurer, signaling a pivot to pure technology enablement for embedded partnerships.

Europe Embedded Insurance Market Report Scope

Embedded insurance involves incorporating insurance services into non-insurance products or services, like mobile applications, online retail platforms, or interconnected devices. It focuses on many product and application types, market dynamics, and emerging trends in the segments and regional markets. It also examines the competitive environment and the major players. The market is segmented by insurance line, channels, and geography. By insurance line, the market is segmented into electronics, furniture, sports equipment, travel insurance, and other insurance lines. By channel, the market is segmented into online and offline channels. The market is geographically segmented into the United Kingdom, France, Germany, Italy, Spain, and Rest of Europe. The report offers market sizes and forecasts in terms of revenue (USD) for all the above segments.

| Electronics |

| Furniture |

| Sports Equipment |

| Travel Insurance |

| Others (Mobility, Pet, Luxury Items) |

| Online |

| Offline |

| Personal / Consumer |

| Business |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Insurance Line | Electronics |

| Furniture | |

| Sports Equipment | |

| Travel Insurance | |

| Others (Mobility, Pet, Luxury Items) | |

| By Distribution Channel | Online |

| Offline | |

| By End-User Industry | Personal / Consumer |

| Business | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe embedded insurance market?

The market is valued at USD 4.11 billion in 2026 and is forecast to reach USD 18.29 billion by 2031, reflecting a 34.8% CAGR.

Which insurance line is expanding the fastest within Europe?

Electronics protection is growing at a 35.72% CAGR through 2031, outpacing travel, furniture, and other segments.

Why are online channels so dominant in European embedded insurance?

APIs let insurers bind policies inside e-commerce, banking, and mobility apps, giving online channels a 93.10% share of 2025 premiums.

What level of market concentration exists among Europe’s embedded insurance players?

The sector earns a concentration score of 6, meaning the top five carriers write just below half of total premium, leaving room for insurtech challengers.

Page last updated on: