Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

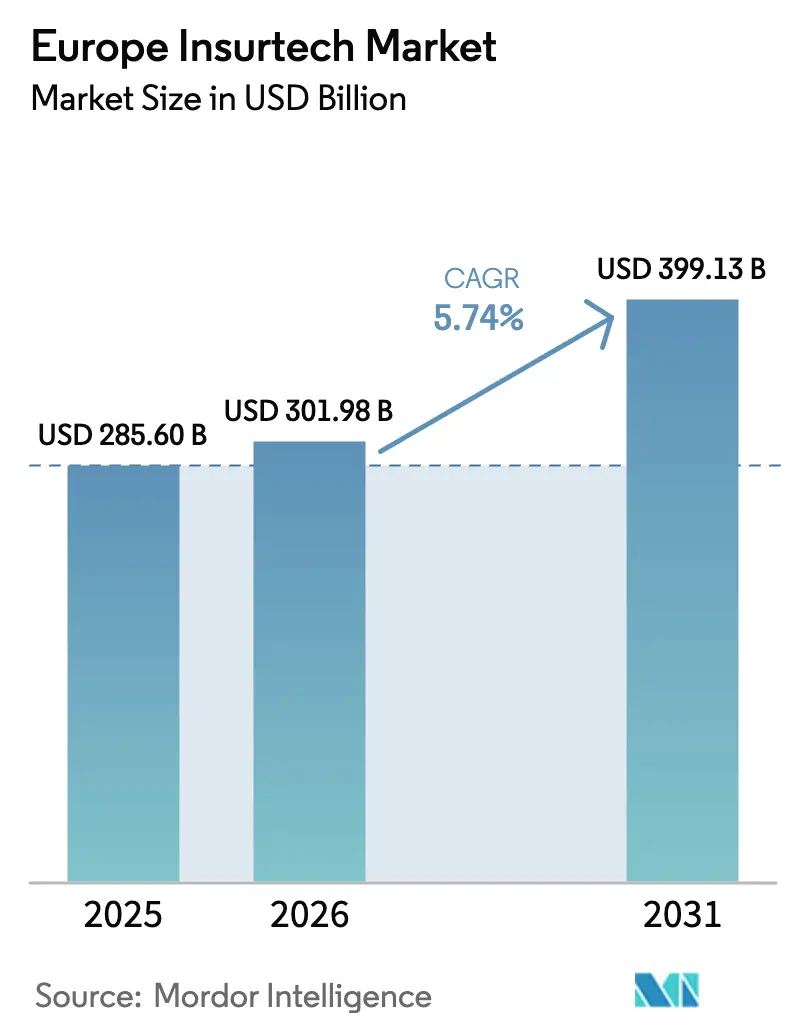

| Base Year Market Size (2025) | USD 285.60 Billion |

| Market Size (2026) | USD 301.98 Billion |

| Market Size (2031) | USD 399.13 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Insurtech Market Analysis by Mordor Intelligence

The European insurtech market size was valued at USD 285.60 billion in 2025 and estimated to grow from USD 301.98 billion in 2026 to reach USD 399.13 billion by 2031, at a CAGR of 5.74% during the forecast period (2026-2031). Migration to API-enabled open-insurance, expansion of generative-AI underwriting, and fast-growing embedded distribution models reinforce the upward trajectory. Climate-related loss events, mounting cyber exposures, and rapid aging of the population unlock fresh premium pools through parametric and longevity covers. Funding flows have become more selective, so capital now gravitates toward carriers that can show disciplined loss ratios and strong regulatory compliance. Competitive intensity is moderate because data governance obligations under the EU AI Act raise entry barriers, favoring firms with sophisticated model-validation toolkits.

Key Report Takeaways

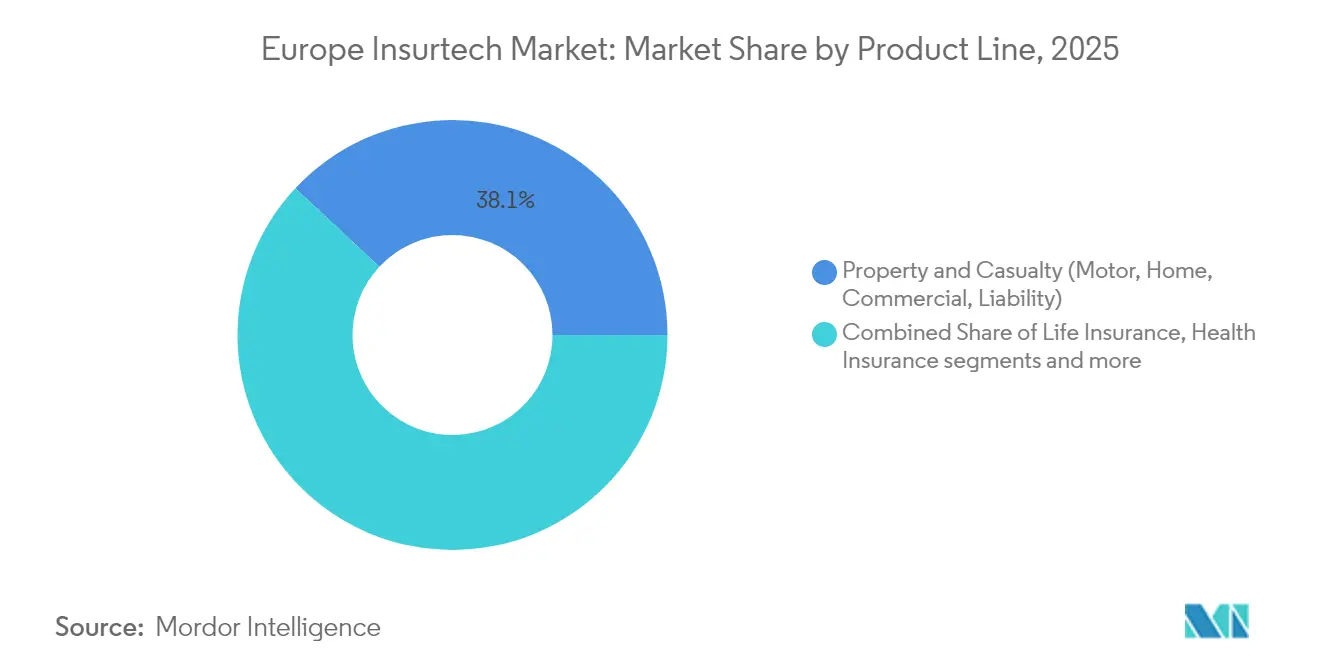

- By product line, specialty policies advanced at a 7.34% CAGR while property & casualty retained 38.05% of the European insurtech market share in 2025.

- By distribution channel, agents and brokers controlled 42.60% of the European insurtech market size in 2025, and embedded insurance platforms are projected to expand at a 6.28% CAGR.

- By end user, retail buyers generated 64.05% of premium in 2025, while SME commercial demand rises at a 6.65% CAGR.

- By geography, the United Kingdom held 17.12% of premium in 2025, and Spain leads growth with a 6.74% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Insurtech Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-first adoption and open-insurance APIs | +1.2% | UK, Netherlands, Germany, EU-wide | Medium term (2-4 years) |

| Embedded insurance with e-commerce and mobility | +1.4% | DACH, UK, France | Short term (≤ 2 years) |

| Generative-AI underwriting and claims automation | +1.1% | London, Munich, Zurich | Medium term (2-4 years) |

| Climate-driven parametric coverage expansion | +1.3% | Mediterranean, Alpine, Northern Europe | Short term (≤ 2 years) |

| Usage-based insurance via telematics and IoT | +0.7% | Italy, Spain, Nordic region | Medium term (2-4 years) |

| API-led bancassurance partnerships | +0.6% | France, BENELUX, Central Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital-first adoption and open-insurance APIs

European consumers now expect end-to-end digital journeys for quoting, binding, servicing, and claims after pandemic lockdowns accelerated channel migration. The EU Financial Data Access law that comes into force in 2027 mandates standardized APIs, which will slash switching friction and open multi-carrier comparison on any device. Incumbents, therefore, divert larger IT budgets to customer-facing micro-services in order to preserve share. Fintech sandboxes in the United Kingdom and Netherlands shorten product-testing cycles and encourage start-ups to plug directly into core-banking ecosystems. As open insurance matures, pricing transparency will reward firms that can pipe in alternative data sets for more granular risk scoring.

Embedded insurance with e-commerce and mobility

Premium written at checkout on ride-hailing, car-subscription, and online retail platforms more than doubled from 2023 to 2024, outpacing all other distribution formats. Qover and Allianz each extended white-label programs that package motor coverage in under 60 seconds for customers buying electric vehicles. Contextual offers lift conversion and keep acquisition cost below EUR 10 per policy, far lower than comparison-site averages. Regulatory sandboxes allow rapid proof-of-concept deployment while preserving product-suitability checks mandated by the Insurance Distribution Directive. E-commerce partners now request bundled cyber and warranty policies, broadening embedded use cases beyond travel and gadget lines.

Generative-AI underwriting and claims automation

Large language models analyze photos, sensor feeds, and policy wording so underwriters can issue quotes in minutes and trigger low-touch claims payouts. Munich Re reports a 4% drop in loss-adjustment expense after integrating satellite and weather data into generative-AI severity prediction modules. The EU AI Act classifies underwriting engines as high-risk, which demands robust audit trails and model explainability[1]European Central Bank, “Financial Stability Review 2024,” ecb.europa.eu. Firms with dedicated validation teams gain a compliance moat. Smaller MGAs increasingly license pre-validated AI stacks to avoid long approval cycles and capital, letting them stay competitive despite scale disadvantages.

Climate-driven parametric coverage expansion

Weather-related losses in Europe reached new highs during the 2024 summer, pushing demand for parametric products that rely on independent triggers rather than lengthy adjustment[2]University of Mannheim, “Climate Insurance Losses Study 2024,” uni-mannheim.de. AXA launched heat-index covers that pay within 72 hours when temperature thresholds are breached. Descartes Underwriting added multi-peril contracts for vineyard owners, capitalizing on agritech sensors that supply real-time weather data. Regulated capital requirements for property carriers rise when catastrophe frequency climbs, so risk transfer to parametric specialists becomes attractive. Satellite and IoT proliferation strengthens trigger integrity and paves the way for broader corporate adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented regulation across EU member states | -0.8% | EU-wide, especially DACH | Long term (≥ 4 years) |

| Venture-capital pullback and valuation compression | -0.6% | London, Berlin, Paris | Medium term (2-4 years) |

| Data scarcity, quality gaps, and AI bias risks | -0.5% | Global, strictest scrutiny in Europe | Short term (≤ 2 years) |

| Heightened cybersecurity threats to insurtech platforms | -0.4% | Global, high incidence in UK and France | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented regulations across EU member states

Insurtechs must juggle 28 licensing regimes across the EU, the United Kingdom, and EFTA, each with unique capital buffers and consumer-protection nuances[3]BaFin, “Solvency II Guidelines 2024,” bafin.de. Solvency II transposition varies, so a passported license rarely removes local reporting duties. Brexit doubled compliance workload for United Kingdom-based firms that sell into Europe, forcing many to establish dual entities. EIOPA’s harmonization roadmap runs to 2030, which delays relief for start-ups seeking continental reach. Larger incumbents can amortize additional governance costs, widening the resource gap and cooling competitive heat.

Venture-capital pullback and valuation compression

European insurtech investment plummeted by more than 40% between 2021 and 2023, echoing broader tech repricing trends. Late-stage rounds saw sharper markdowns, with Wefox raising capital in 2025 at a lower per-share price than in 2022. Investors now demand near-term profitability, lengthening due diligence time, and inserting liquidation preferences. Seed funding remains available, though founders must show regulatory roadmaps and robust reinsurance capacity from day one. The tightened funnel risks starving promising analytics vendors that serve incumbents but lack immediate premium revenue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Line: Specialty Lines Outpace Core P&C

Property & casualty generated 38.05% of premium in 2025, yet specialty categories enjoy the fastest 7.34% CAGR, adding meaningful dollars to the Europe insurtech market size through 2031. Early movers leverage external telemetry, supply-chain data, and pet-health APIs to shape granular risk pools and deliver combined ratios below 90%. Life and health policy growth holds steady as e-health records speed up underwriting in Germany and France. P&C automation funnels straightforward motor and home quotes into digital funnels, while marine and cyber underwriters handle complex exposures at higher margins. The NIS2 cybersecurity mandate and pet-ownership upticks both fuel premium expansion, enhancing diversification.

Past years show similar trends. From 2020 to 2024, specialty premiums more than doubled in absolute terms, aided by cloud-native pricing engines. Insurtech fleet products, for example, price kilometer usage in real time and rebate safe-driving behaviors monthly. Specialty underwriters also tap reinsurance sidecars to manage tail risk, enabling further appetite without straining capital. Collectively, these factors keep specialty lines the core growth engine of the Europe insurtech market.

By Distribution Channel: Embedded Platforms Capture Incremental Share

Agents and brokers still controlled 42.60% of premium in 2025, illustrating strong personal relationship value in motor fleets and mid-market corporate lines. Yet embedded models, projected at 6.28% CAGR, will gradually chip away at this dominance, directing more flows into the Europe insurtech market. Checkout integration inside retailer and mobility apps drives sub-10-euro acquisition cost and double-digit conversion lifts. Direct-to-consumer portals also gain share as price-comparison sites add robo-advice layers to aid policy selection. Digital MGAs distribute white-label capacity through API endpoints and manage compliance programmatically.

Hybrid advisory structures are rising. Brokers feed quote data from comparison engines to provide scenario guidance while still earning commissions. Bancassurance grows more slowly due to tighter cross-sell rules but modernizes by surfacing personalized offers in bank apps rather than branch desks. Regulatory parity across channels means embedded providers must maintain suitability and disclosure, a hurdle addressed via automated rule engines. Over time, cost leadership and frictionless UX help consolidate share, magnifying the overall European insurtech market value.

By End User: SME Digital Uptake Narrows Protection Gaps

Retail buyers remained dominant at 64.05% in 2025, but SMEs lifted their proportion fastest with a 6.65% CAGR through 2031. Digital portals let entrepreneurs bind liability cover in hours, transforming historically low penetration. Platforms like Allianz Commercial Digital price professional-indemnity and cyber in one checkout journey and credit premiums to cashback wallets. Large corporate procurement stays bespoke and broker-driven, reflecting complex exposures across multiple jurisdictions. Public-sector entities bolster climate-resilience spending, procuring parametric flood covers for municipal infrastructure.

SME momentum reflects two structural forces. First, pandemic interruptions raised awareness of business-continuity insurance, while embedded offers inside accounting packages removed discovery friction. Second, late-payment regulation heightens demand for trade-credit insurance, a product historically geared to large exporters. Digital onboarding drives cost efficiency, making smaller policies profitable on a larger scale. Altogether, these ingredients expand the Europe insurtech market while diversifying risk away from crowded personal lines.

Geography Analysis

The United Kingdom retained 17.12% of Europe insurtech market share in 2025, buoyed by long-standing regulatory sandboxes and deep venture-capital pools that accelerate piloting of AI-enabled underwriting tools. Spain is forecast to post a 6.74% CAGR through 2031 as Mediterranean climate risk elevates demand for parametric weather covers and as digital-banking giants such as BBVA embed micro-policies at checkout. In absolute terms, the United Kingdom still contributes the largest slice of Europe's insurtech market size, yet the gap narrows each year as Iberian, Italian, and French players capture freshly monetized climate and cyber exposures. London’s post-Brexit duplication of reporting duties slows some cross-border deals, but insurers offset friction by setting up EU-domiciled subsidiaries in Dublin and Luxembourg. As a result, premium outflows from the United Kingdom core increasingly re-enter the bloc via reinsurance sidecars booked in continental hubs.

Germany and France together command a sizeable premium pool that rivals the United Kingdom, although Germany’s BaFin requires extra solvency buffers that temper aggressive product experimentation. France gained momentum after PACTE reforms simplified licensing for digital brokers and allowed API-based life-insurance distribution inside neobank apps. Italy follows Spain’s trajectory as pension-gap awareness and state digitalization grants push mobile health and longevity covers into mainstream channels. BENELUX markets outperform on a per-capita basis because Dutch and Belgian carriers adopted open-insurance APIs early, enabling banks to cross-sell policies in under two minutes. Nordic countries show steadier single-digit growth; penetration is already high, yet usage-based motor and smartwatch-driven health products still carve profitable niches.

Central and Eastern Europe offer the largest white space, given low historic insurance density and rapid smartphone adoption that lowers distribution cost. Insurtech MGAs passport policies into Poland, Czechia, and the Baltics while partnering with local third-party administrators to handle claims in native languages. EIOPA’s planned harmonization of consumer-consent templates—expected by 2027—could shave months off new-market launches once implemented, though national sovereignty debates keep timelines fluid. Climate-adaptation funds earmarked for Eastern European transport corridors are already triggering tenders for flood and business-interruption parametric covers, attracting specialist MGAs with satellite analytics. Taken together, these dynamics broaden geographic premium diversity and reduce reliance on legacy Western European strongholds.

Competitive Landscape

Europe’s insurtech arena remains moderately fragmented; the five largest underwriters capture roughly 35% of written premium, leaving ample room for niche specialists and new MGAs to scale. Competitive differentiation now centers on data-engineering sophistication and AI governance, because the forthcoming EU AI Act demands audit trails that smaller firms often struggle to fund. Consequently, technology-forward incumbents are purchasing explainability toolkits or partnering with reg-tech vendors to preserve speed without tripping compliance alarms. Embedded-insurance orchestrators leverage single-API integrations to secure merchant partnerships at sub-EUR-10 acquisition costs, tightening pressure on traditional brokers. Meanwhile, reinsurers deepen venture arms to secure early access to climate-risk and longevity datasets that improve facultative pricing.

wefox continues to scale broker-enablement software across DACH markets, while Alan focuses on pan-European digital health plans that bundle telemedicine and AI symptom checks. Lemonade entered Germany with renters and contents covers running on behavioural-economics-driven claims flows that approve many payouts in under a minute. Allianz, Munich Re, and Swiss Re invest heavily in computer-vision partners such as Tractable to automate motor and property damage appraisal, shaving claim-cycle times by up to 40%. Several incumbents also back parametric start-ups like Descartes Underwriting to hedge catastrophe exposure and meet rising corporate demand for rapid-payout triggers. These collaborations illustrate a growing symbiosis in which legacy carriers provide balance-sheet strength while tech players supply data pipelines and rapid-iteration culture.

Funding discipline tightened after the 2021 boom; late-stage rounds close only when pathway to underwriting profitability is clear, and investors insist on AI-audit readiness as a due-diligence checkbox. Midsize insurers now hunt for tuck-in acquisitions that deliver proven embedded pipelines rather than pure software IP, reflecting a pivot toward revenue accretion over speculative tech bets. Simultaneously, MGAs with multi-country regulatory passports assume more balance-sheet risk through fronting-carrier partnerships, aiming to capture extra economics and raise enterprise value ahead of an IPO window projected for 2027–2028. Cybersecurity readiness has become another competitive wedge, with firms advertising zero-trust architectures to reassure corporate buyers wary of vendor breaches. Overall, the race is shifting from pure customer-acquisition velocity to holistic mastery of data governance, capital efficiency, and cross-border compliance—factors likely to decide long-term winners in the Europe insurtech market.

Europe Insurtech Industry Leaders

Wefox

Alan

Zego

Lemonade

Getsafe

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Alan secured EUR 173 million in Series D financing led by Coatue, funding geographic expansion in Italy and Spain, and development of a multilingual symptom-checker. The round valued the company close to EUR 3 billion and included an employee share-buyback program to improve retention.

- February 2025: wefox raised EUR 170 million in an extension to its Series D, channeling most proceeds toward core-system refactoring that will improve underwriting margin in DACH markets. Management reported the group reached monthly profitability for the first time since inception.

- January 2025: Akur8 closed a USD 120 million Series B to scale its automated pricing suite across 15 European carriers. The firm will open a Zurich R&D hub focused on AI explainability to satisfy upcoming EU AI Act audits.

- December 2024: Lemonade officially launched in Germany, offering renters and contents policies that integrate with the country’s client-identification standard VideoIdent. Early KPI filings show a sub-30-second claim-approval median and an NPS above 70.

Europe Insurtech Market Report Scope

Insurtech refers to the use of technological innovation to improve the efficiency of the current insurance business model. The growing digitization has led various participants of the insurance industry value chain toward technological innovations. These rapid technological advancements are leading to an expansion of the insurtech market.

The European insurtech market is segmented by business model and geography. By business model, it can be segmented into carrier, enabler, and distributor. By geography, it can be segmented into the United Kingdom, Germany, France, Italy, Switzerland, Sweden, the Netherlands, and Other Countries. The report also offers a complete background analysis of the European insurtech market, including market sizes, market segments, industry trends, and growth drivers. The market sizes and forecasts for the above segments are provided in value (USD Billion) terms.

By Product Line (Insurance Type)

| Life Insurance |

| Health Insurance |

| Property & Casualty (Motor, Home, Commercial, Liability) |

| Specialty Lines (Cyber, Pet, Marine, Travel) |

By Distribution Channel

| Direct-to-Consumer (Digital) |

| Aggregators / Marketplaces |

| Digital Brokers / MGAs |

| Embedded Insurance Platforms |

| Traditional Agents / Brokers (digitally enabled) |

| Bancassurance (digitally enabled) |

| Other Channels |

By End User

| Retail / Individual |

| SME / Commercial |

| Large Enterprise / Corporate |

| Government / Public Sector |

By Region

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Product Line (Insurance Type) | Life Insurance |

| Health Insurance | |

| Property & Casualty (Motor, Home, Commercial, Liability) | |

| Specialty Lines (Cyber, Pet, Marine, Travel) | |

| By Distribution Channel | Direct-to-Consumer (Digital) |

| Aggregators / Marketplaces | |

| Digital Brokers / MGAs | |

| Embedded Insurance Platforms | |

| Traditional Agents / Brokers (digitally enabled) | |

| Bancassurance (digitally enabled) | |

| Other Channels | |

| By End User | Retail / Individual |

| SME / Commercial | |

| Large Enterprise / Corporate | |

| Government / Public Sector | |

| By Region | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

How large will the European insurtech market be in 2031?

It is projected to reach USD 399.13 billion.

Which product segment is expanding fastest?

Specialty lines such as cyber, pet, and marine policies grow at a 7.34% CAGR.

What makes embedded insurance appealing to merchants?

It embeds cover at checkout, cuts acquisition cost to under EUR 10, and lifts conversion rates.

Which country currently holds the biggest share of premium?

The United Kingdom leads with 17.12% of the total written premium.

What regulation will standardize insurance data APIs?

The EU Financial Data Access framework, effective 2027, mandates open-insurance interfaces.

How does generative AI benefit underwriting?

It produces quote-ready risk scores in minutes and reduces loss-adjustment expenses by several percentage points.

Page last updated on: