Europe Electric Fireplace Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

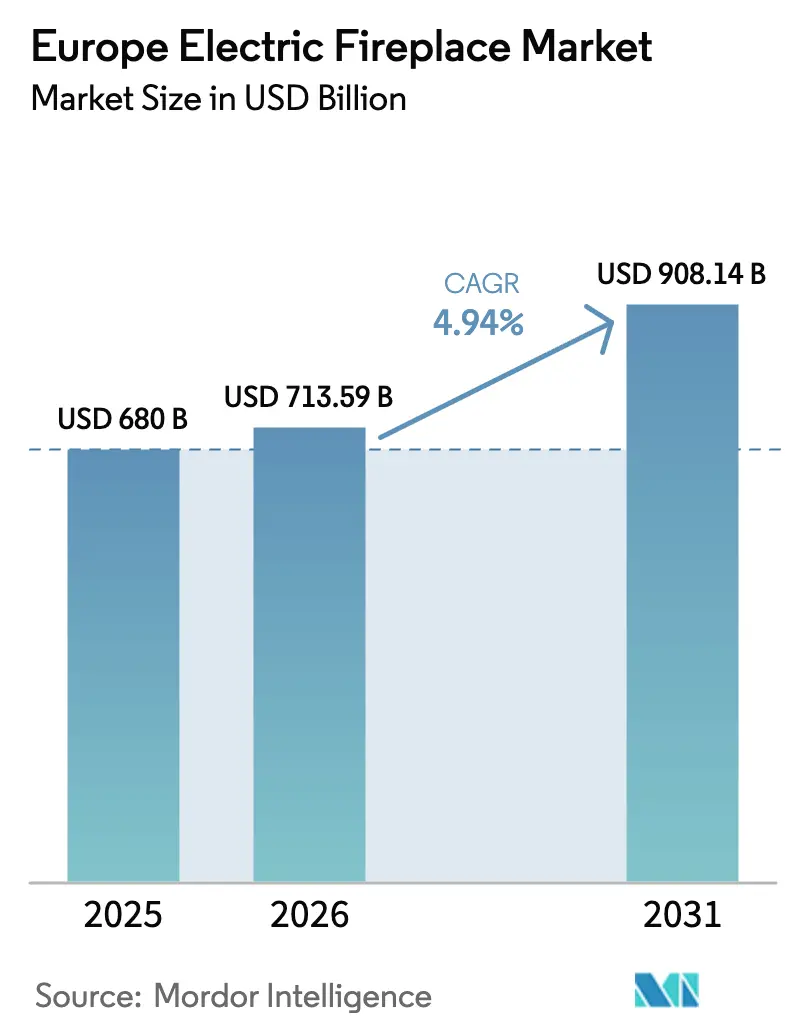

| Base Year Market Size (2025) | USD 680 Billion |

| Market Size (2026) | USD 713.59 Billion |

| Market Size (2031) | USD 908.14 Billion |

| Growth Rate (2026 - 2031) | 4.94% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Electric Fireplace Market Analysis by Mordor Intelligence

The Europe electric fireplace market size was valued at USD 680 million in 2025 and estimated to grow from USD 713.59 million in 2026 to reach USD 908.14 million by 2031, at a CAGR of 4.94% during the forecast period (2026-2031). Growing enforcement of EU-wide decarbonization mandates, urban housing stock that lacks functional chimneys, and continuous product upgrades in LED flame realism are shifting the category from niche décor to mainstream secondary heating. Demand also benefits from a simple plug-and-play installation that avoids the structural work and permitting hurdles seen with gas or wood options. Competitive intensity remains moderate because established heating majors and emerging smart-home specialists share shelf space, yet no single participant holds a blocking position that would deter new entrants. Price sensitivity is rising due to electricity tariff inflation, but time-of-use pricing schemes and integrated energy-management apps are helping end users rationalize running costs. Regulations such as the European Sustainable Products Regulation (ESPR) are favouring electric formats over combustion models, and they are accelerating product standardization that improves cross-border distribution economies. Altogether, a balanced mix of regulatory pull and technology push underpins steady upward volume momentum.

Key Report Takeaways

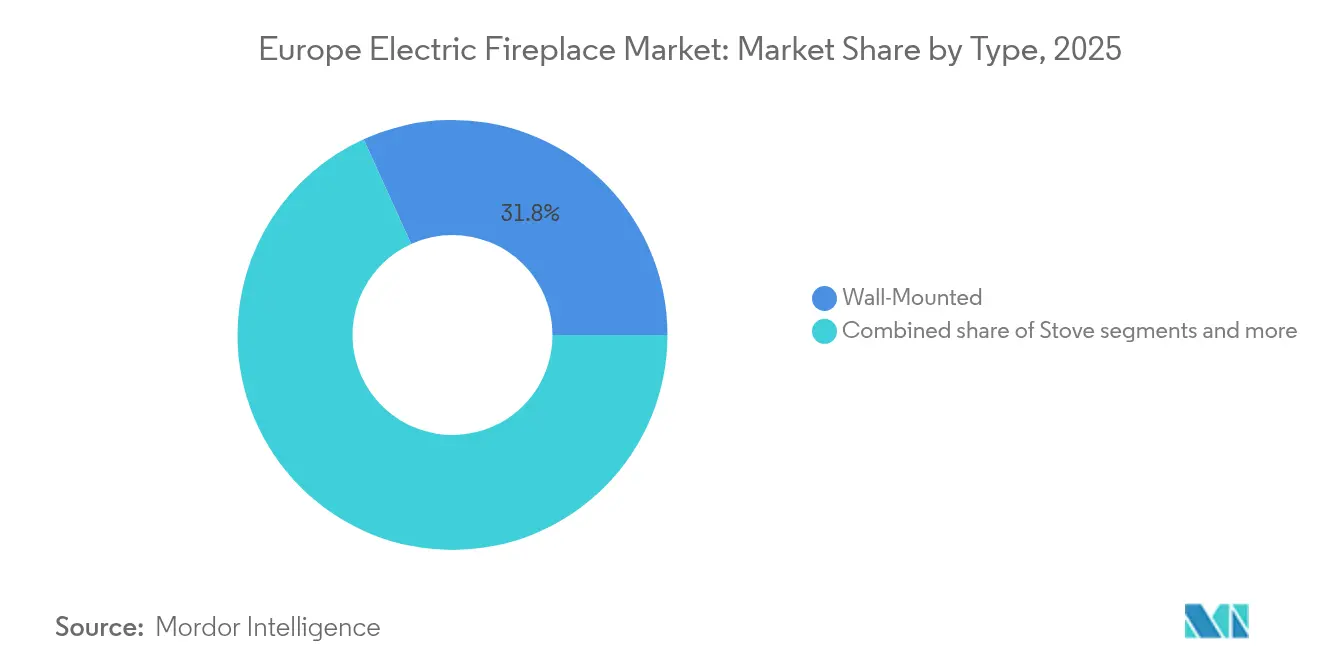

- By type, wall-mounted units held 31.78% of the Europe electric fireplace market share in 2025, whereas table-top models are forecast to post the fastest 12.03% CAGR through 2031.

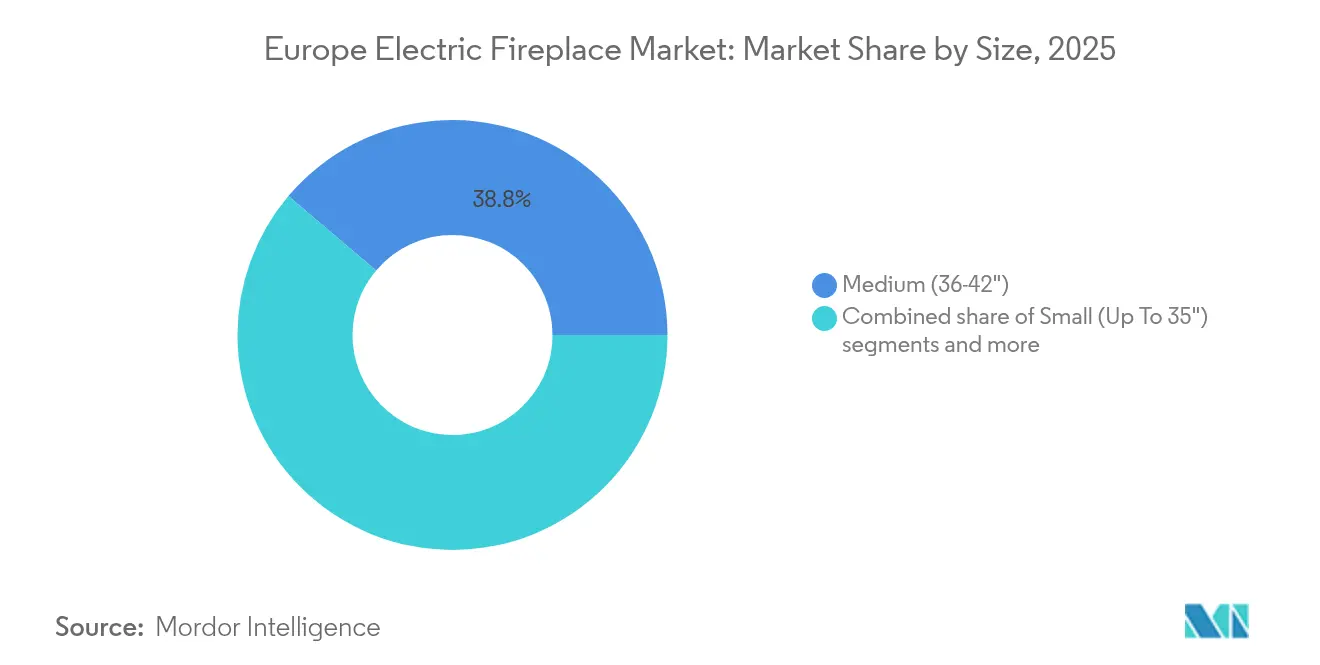

- By size, medium 36-42-inch units commanded 38.82% share of the Europe electric fireplace market size in 2025, while extra-large 49-inch-plus models are slated to expand at 10.52% CAGR to 2031.

- By application, residential installations accounted for 66.55% share of the Europe electric fireplace market size in 2025, and commercial projects are advancing at a 9.42% CAGR through 2031.

- By geography, Germany led with 24.93% of the Europe electric fireplace market share in 2025, but BENELUX is expected to register the highest 8.63% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France contributes to a system defined not by any single country or region but by the interaction of many. The global electric fireplace market data by Mordor Intelligence represents that combined structure.

Europe Electric Fireplace Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decarbonization push and electrification of home heating | +1.8% | EU-wide, strongest in Germany, Netherlands, Denmark | Long term (≥ 4 years) |

| Retrofit demand from chimney-less dwellings | +1.2% | Urban centers across EU, concentrated in UK, Germany, France | Medium term (2-4 years) |

| Smart-home and LED flame realism innovations | +0.9% | Global, early adoption in Nordics, BENELUX | Short term (≤ 2 years) |

| Build-to-rent and micro-apartment boom | +0.7% | Major EU cities, particularly London, Berlin, Amsterdam | Medium term (2-4 years) |

| Fire-safety driven insurance incentives | +0.6% | EU-wide, especially in multi-unit residential buildings | Short term (≤ 2 years) |

| 3D-printed customised fascia options | +0.5% | Western Europe, notably Germany, UK, Netherlands | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Decarbonization Push and Electrification of Home Heating

European Union climate packages such as Fit for 55 obligate member states to reduce carbon emissions by 55% before 2030, and national bans on new gas boilers are accelerating the shift toward electric space-heating formats[1]European Commission, “REPowerEU: Affordable, Secure and Sustainable Energy for Europe,” commission.europa.eu. . Electric fireplaces qualify as zero-direct-emission appliances, which lets builders meet carbon-budget targets without installing costly flues or exhaust fans. Manufacturers are responding by redesigning heating elements to maximize radiant output per kilowatt so that operating costs stay manageable. Financial incentives that support heat-pump deployments are indirectly creating awareness of non-combustion heating, and that halo effect benefits decorative electric options in retrofit situations. Energy-labelling rules under ESPR, effective since 2024, award favorable ratings to products with integrated thermostats and timers, pushing brands to embed smart controllers in all mid-to-premium models. Over the long term, the regulatory environment is therefore expected to keep the Europe electric fireplace market on a stable expansion path.

Retrofit Demand from Chimney-less Dwellings

60% of EU apartment buildings erected after World War II were designed without chimneys, forcing homeowners to choose electric systems when they seek a flame effect[2]Dutch Government, “Housing and Spatial Planning,” government.nl. . In dense cities such as Paris, Berlin, and Amsterdam, heritage preservation codes restrict new flue construction, making electric inserts the only realistic way to replicate a hearth. Insurance firms in multi-family buildings often discount premiums when occupants opt for non-combustion appliances, creating a measurable economic nudge. Product engineering has adapted by offering ultrathin wall-mounted frames that sit almost flush, allowing installations even in hallway corridors where space is tight. Retail chains promote these products aggressively during autumn renovation seasons, bundling them with quick-install mounting kits to widen the do-it-yourself addressable market. Because electric units plug into standard 230-volt outlets, landowners avoid the downtime and tenant disruption associated with gas-line extensions. The combined spatial and administrative conveniences sustain solid mid-term growth for the Europe electric fireplace market.

Smart-Home and LED Flame Realism Innovations

Voice-assistant compatibility and app-based timers transform electric fireplaces from standalone heaters into connected devices that integrate with broader home-energy dashboards. Early adopters in the Nordics and BENELUX report that Wi-Fi scheduling trims electricity bills by shifting usage away from peak-rate windows. Visual upgrades are equally important; three-dimensional holographic flame engines now reproduce ember beds and variable colour temperatures that consumers rate as almost indistinguishable from real wood burners[3]Kalfire, “E-one Holographic Fireplace Technology,” kalfire.com. . These cosmetic advances have elevated consumer willingness to pay and are expanding distributor margins. Manufacturers differentiate premium SKUs by bundling multi-zone heating elements that let users warm only the immediate seating area, enhancing efficiency. Retailers leverage online configurators that overlay fireplace images onto room photos, further easing the purchase journey. Collectively, connectivity and realism are cementing the perception of electric fireplaces as future-forward lifestyle products rather than stopgap heaters.

Build-to-Rent and Micro-Apartment Boom

Institutional investors poured USD 8.77 billion (EUR 8.2 billion) into European build-to-rent assets during 2024, and developers of compact studios actively specify electric fireplaces as a plug-and-play amenity[4]CBRE, “European Build-to-Rent Investment Report 2024,” cbre.com. . Landowners value the absence of mandatory annual gas-safety inspections, which lowers operating costs over the building life cycle. Wall-mounted and table-top layouts fit within the tight footprints typical of 25 square-meter micro-units, preserving rentable floor area while adding a perceived luxury element. Because electric fireplaces run quietly and generate minimal surface heat, they comply with stringent landowner liability rules for kid-safe interiors. Many new projects pre-install smart plugs so tenants can monitor consumption via branded apps, turning energy transparency into a selling point. Micro-apartment architects also leverage shallow recesses in partition walls to host flush mounts that function as visual anchors in an otherwise small living zone. These design decisions help sustain a favorable demand funnel among urban millennials who prioritize convenience and aesthetics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising electricity tariffs inflate running costs | -1.4% | EU-wide, acute in Germany, Denmark, Belgium | Short term (≤ 2 years) |

| Competition from heat-pump and infrared panels | -0.8% | Northern EU markets, strongest in Nordics, Germany | Medium term (2-4 years) |

| Grid-constrained historic city centres | -0.6% | Southern and Central Europe, especially Italy & Spain | Medium term (2–4 years) |

| Post-pandemic dip in hospitality refurb capex | -0.5% | Urban EU tourism hubs, notably France & Spain | Short to Medium term (1–3 years) |

| Source: Mordor Intelligence | |||

Rising Electricity Tariffs Inflate Running Costs

Average residential electricity prices reached USD 30.92 (EUR 28.9) per 100 kWh across the EU during the first half of 2024, a 14% year-over-year jump that compresses the cost advantage previously held over gas. German households now routinely pay more than USD 34.24 (EUR 32) per 100 kWh, turning electric fireplaces into discretionary rather than primary heating choices. Consumer forums increasingly advise pairing usage with off-peak tariff windows, but behaviour change remains inconsistent. Brands respond by adding eco-mode settings that throttle output once ambient temperatures stabilize, yet such technical fixes cannot fully offset macro-price pressures. Retailers have started to finance purchases with zero-interest installment plans to soften sticker shock, though high running costs may still limit repeat usage. In markets with dynamic pricing, integration with smart meters can automate on/off cycles, but adoption of those meters is uneven. Unless European wholesale power costs retreat, elevated tariffs will continue to weigh on short-term uptake.

Competition from Heat-Pump and Infrared Panels

Heat pump shipments in Europe exceeded 3 million units during 2024, and coefficients of performance above 4.0 give them a decisive operating-cost edge over electric fireplaces’ 1.0 conversion ratio. Subsidies, especially in the Nordics and Germany, drive installed prices close to premium fireplace ticket values, reducing the relative appeal of decorative products for primary heating roles. Infrared panel heaters, which also mount flat against walls, claim lower hourly consumption and provide broader room coverage, further diluting purchase intent. Commercial building codes increasingly reward high-efficiency systems with tax rebates, steering architects away from electric fireplaces except as lobby accents. Manufacturers attempt to defend their share by highlighting aesthetic benefits and introducing hybrid units that combine infrared panels with flame visuals, but market reception is still nascent. The net result is intensified competition that chips away at potential growth, especially in energy-conscious northern markets over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Wall-Mounted Units Sustain Lead Through Versatility

Wall-mounted configurations generated 31.78% of Europe's electric fireplace market share in 2025, underscoring their traction among apartment dwellers who favor installations that do not encroach upon floor area. These units often ship with slim brackets and can plug into existing sockets, sidestepping costly electrical rewiring. Designers value the clean lines that align with minimalist Scandinavian and German interior themes, and the segment is further boosted by hotel refurbishments where surface-mount units minimize construction downtime. Smart-home compatibility appears first on wall-mounted price lists, signaling a premium position that sustains attractive margins. While traditional stove-style products still resonate in rural France and Scandinavia, their aggregate shipment volume lags the highly urban wall-mounted category. Table-top models, projected to post a 12.03% CAGR, are emerging in short-term rental furnishings where landowners prefer portable solutions. Insert and freestanding formats together round out the portfolio, targeting heritage properties that already feature unused hearth cavities.

Second-generation wall-mounted designs now integrate variable-width air outlets that distribute warmth more uniformly, a feature praised in consumer reviews. Many models also allow users to deactivate heating and run flames for ambiance only, a flexibility that aligns with energy-saving behaviour when room temperatures are already comfortable. Suppliers differentiate on visual depth by layering LED panels behind reflective glass to create a sense of distance between logs and the backplate. Price bands stretch from USD 321(EUR 300) for entry-level plastic-trim units to well over USD 2,140 (EUR 2,000) for widescreen metal-framed systems with touch-panel controllers. Service networks partner with big-box retailers to offer white-glove delivery and wall-mounting packages, making ownership frictionless for busy urban professionals. As a result, the Europe electric fireplace market continues to find its volume anchor in the wall-mounted segment even while smaller niches grow around it.

By Size: Medium Units Align With European Room Dimensions

Medium 36-42-inch models secured a 38.82% share of the Europe electric fireplace market size in 2025 because they balance visual prominence with practical footprint in typical 15–20 square-meter living rooms. Builders in Germany and France often wire living spaces on 10-amp circuits, which comfortably support medium outputs without requiring panel upgrades. Retail displays underscore this sweet spot by arranging medium units at eye level, whereas larger sizes frequently sit too close to the floor for ideal viewing height. Shipping costs rise sharply for packages wider than 48 inches, creating another natural brake on extra-large adoption. Nonetheless, the aspirational pull of cinematic-scale flames is fuelling a 10.52% CAGR for models 49 inches and above, especially in luxury villas around Lake Como and the Algarve. Small units up to 35 inches cater to micro-apartments and bedrooms, while large 43-48-inch variants carve out a share in suburban homes seeking a focal point without overpowering the wall.

Future medium units will converge on frameless designs with edge-to-edge glass that maximizes flame area inside the same external dimensions. Manufacturers experiment with modular log sets so buyers can refresh aesthetics seasonally, a tactic expected to lengthen replacement cycles. Energy regulators may tighten standby-power limits, and early compliance testing shows medium units meeting forthcoming thresholds more easily than larger, high-output peers. As room dimensions in new urban builds continue to shrink, medium sizes will remain the default specification for developers outfitting living spaces under 35 square meters. Consequently, the segment is poised to anchor revenue streams even as premium extra-large screens pull the category’s top-line in absolute value terms.

By Application: Residential Base Dominates, Commercial Growth Accelerates

Households drove 66.55% of Europe's electric fireplace market size in 2025 because owner-occupiers prioritize visual ambiance and low maintenance during home renovation cycles. The residential uptake also reflects execution ease: products usually ship in a single carton and can be self-installed in under one hour. Marketing campaigns highlight health safety versus wood smoke and carbon monoxide, themes that resonate strongly with families. Over the last two winters, electric fireplace sales spiked during promotional weeks when gas prices surged, indicating direct fuel price substitution behaviour. Builders increasingly pre-wire living rooms with recessed connections in anticipation of buyer demand, further embedding electric fireplaces into standard amenities lists. DIY retail chains hold seasonal workshops demonstrating simple mounting techniques, which ease consumer anxiety and accelerate the sales funnel. Looking ahead, integration with whole-home energy dashboards is expected to migrate down into mainstream price points, reinforcing residential dominance.

Commercial deployments spanning hotels, cafés, and office lobbies are set for 9.42% CAGR to 2031 as operators retrofit spaces for post-pandemic experiential appeal. Hospitality chains appreciate the ability to adjust flame colours to match branding schemes, adding a subtle marketing touch. Insurance premiums fall because electric units eliminate open flames, and that cost reduction offsets incremental electricity expenditure. Corporate offices favor electric fireplaces in reception areas to soften otherwise austere environments while still meeting strict building-code fire-safety rules. Retail showrooms employ them as seasonal décor, and the ability to deactivate heat prevents discomfort during warmer months. Some facility managers deploy networked units that switch off automatically outside of business hours, aligning with ISO 50001 energy-management standards. Collectively, commercial demand is granting manufacturers a buffer against residential cyclicality.

Geography Analysis

Germany captured 24.93% of Europe's electric fireplace market share during 2025, reflecting both the scale of its housing stock and forward-leaning electrification policies under the Gebäudeenergiegesetz. Retailers enjoy mature nationwide distribution, enabling two-day delivery even in secondary cities such as Leipzig and Bremen. Nevertheless, elevated power tariffs cap operating-hour growth, pushing brands to emphasize ambiance-only modes for budget-conscious users. Product localization includes language-specific app interfaces and compliance documentation tailored to German safety standards, which boosts consumer trust. Extended warranties are popular because German buyers associate longevity with environmental stewardship. Local manufacturers leverage proximity to supply chains for faster model refresh cycles, giving them a branding edge. Overall, Germany will remain the value cornerstone of the Europe electric fireplace market revenue through 2031.

The BENELUX bloc, Belgium, Netherlands, Luxembourg, sets the pace with 8.63% CAGR, propelled by ultra-dense urban development and progressive bans on new residential gas connections. Real-estate investors embed electric fireplaces in high-end rental portfolios to create boutique ambiance in units as small as 28 square meters. Public awareness campaigns on indoor air quality also sway buyers toward non-combustion solutions. Because national grids show high renewable penetration, consumers perceive electric fireplaces as a green choice, reinforcing demand. Retailers operate omnichannel strategies that combine online customization tools with experience centers, making purchase journeys seamless. Benelux’s compact geography streamlines after-sales service, boosting customer satisfaction. These structural tailwinds suggest the region will punch above its population weight in incremental dollar contribution.

Other mature markets like the United Kingdom and France collectively account for another 35.58% of revenue, buoyed by large renovation pipelines and consumer familiarity with hearth aesthetics. The Nordics contribute a smaller absolute volume but sustain premium average selling prices courtesy of high disposable incomes. Southern Europe, led by Italy and Spain, is emerging from a low base as urban dwellers recognize electric fireplaces as an air-quality-friendly alternative to gas heaters. Cross-regional e-commerce platforms are shortening delivery lead times, which is expected to smooth out seasonal demand fluctuations across the continent.

The electric fireplace market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for North America. This is complemented by country-specific insights for United States, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The Europe electric fireplace market demonstrates moderate consolidation, with the top five players accounting for just over half of total industry revenue. This leaves ample room for new and emerging brands to carve out market share, particularly through design-forward innovation and niche positioning. Glen Dimplex leads the market, supported by its multi-brand strategy and a USD 53.5 million low-carbon R&D investment completed in 2024, which enhances both its innovation capabilities and sustainability profile. Other notable players like Stovax, Kalfire, Planika, and Modern Flames differentiate through specialized technologies, premium designs, and selective channel strategies. Despite strong incumbents, the market remains open to disruption, especially in underserved or design-sensitive consumer segments.

Barriers to entry are shaped by vertical integration, with top players often controlling heating element production and proprietary LED flame technologies advantages not easily matched by smaller assemblers reliant on third-party components. However, direct-to-consumer brands are making inroads by leveraging social commerce, influencer marketing, and rapid product iteration. Integration with smart-home platforms is becoming a critical differentiator, as seen with Touchstone’s native Alexa compatibility and Modern Flames’ open API model that appeals to home automation professionals. In parallel, hospitality-focused players like Focus Creation are securing long-term agreements with hotel chains, locking in demand, and minimizing price-based competition. Regulatory compliance, particularly under the EU's Ecodesign and ESPR directives, is proving more manageable for large-volume players, while smaller brands may struggle with cost and documentation requirements.

The pricing spectrum across the market is wide, ranging from budget-friendly units under USD 214 (EUR 200) to luxury installations exceeding USD 5,350 (EUR 5,000). New entrants often begin with freestanding models that have fewer installation and code restrictions, later moving into built-in categories as brand recognition and trust build. After-sales service is becoming a pivotal factor in consumer decision-making, driving investments in localized support infrastructure such as European call centers and regional parts warehouses. This professionalization trend is helping to elevate consumer expectations and industry standards alike. Overall, while the market is maturing, it retains a dynamic and competitive edge, with room for innovation across product design, connectivity, and service delivery.

Europe Electric Fireplace Industry Leaders

Glen Dimplex Group

Stovax Heating Group

Be Modern Group

Planika Sp. z o.o.

Charlton & Jenrick Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Glen Dimplex Group completed its USD 53.5 million investment program in low-carbon heating technology development, establishing new R&D facilities in Ireland focused on smart electric heating solutions. The investment positions the company to capture growing demand for connected home heating systems across European markets.

- December 2024: Modern Flames launched its TruWood series featuring advanced LED flame technology and smartphone app integration, targeting premium residential segments with realistic wood-burning visual effects. The product line addresses consumer preferences for authentic flame appearance while maintaining electric heating benefits.

- November 2024: Kalfire introduced the E-one holographic fireplace system in European markets, utilizing advanced projection technology to create three-dimensional flame effects. The innovation represents a significant technological advancement in visual realism for electric fireplace applications.

- October 2024: Focus Creation completed major hotel installations across 15 European properties, demonstrating commercial sector adoption of electric fireplace solutions in hospitality applications. The projects span luxury resorts to boutique hotels seeking fire-safe heating alternatives.

Europe Electric Fireplace Market Report Scope

Electric fireplaces are electric heaters used to heat rooms or workplaces rapidly in residential and commercial buildings. These heating devices are convenient to use, more cost-effective, safer, eco-friendly, and more efficient than other gas and real wood-burning fireplaces. Europe Electric Fireplace Market is segmented By Type (Stove, Insert, Table-top, Wall-mounted and freestanding), By Size (Small (Up to 35"), Medium (36" - 42"), Large (43" - 48"), Extra Large (49" & above), By Application (Residential and Commercial), By Geography (Germany, UK, Italy and Rest of Europe). The report offers market size and forecasts for the European electric Fireplace Market in value (USD) for all the above segments.

| Stove |

| Insert |

| Table-Top |

| Wall-Mounted |

| Freestanding |

| Small (Up To 35") |

| Medium (36-42") |

| Large (43-48") |

| Extra Large (49" & Above) |

| Residential |

| Commercial |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Type | Stove |

| Insert | |

| Table-Top | |

| Wall-Mounted | |

| Freestanding | |

| By Size | Small (Up To 35") |

| Medium (36-42") | |

| Large (43-48") | |

| Extra Large (49" & Above) | |

| By Application | Residential |

| Commercial | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

How large will the Europe electric fireplace market be by 2031?

It is projected to reach USD 908.14 million, reflecting a 4.94% CAGR from 2026.

Which product type currently leads unit sales in Europe?

Wall-mounted electric fireplaces hold the top position with 31.78% share in 2025.

Which European region shows the fastest growth potential?

BENELUX is forecast to grow at 8.63% CAGR through 2031 due to urban densification and gas-connection bans.

What is the primary growth driver behind adoption?

EU decarbonization mandates are pushing homeowners and developers toward non-combustion heating solutions that meet carbon targets.

How do rising electricity prices affect consumer demand?

Higher tariffs increase running costs and may limit use to ambiance rather than primary heating, though smart scheduling partially offsets the impact.

Page last updated on: