Electric Fireplace Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.76 Billion |

| Market Size (2031) | USD 3.38 Billion |

| Growth Rate (2026 - 2031) | 4.13% CAGR |

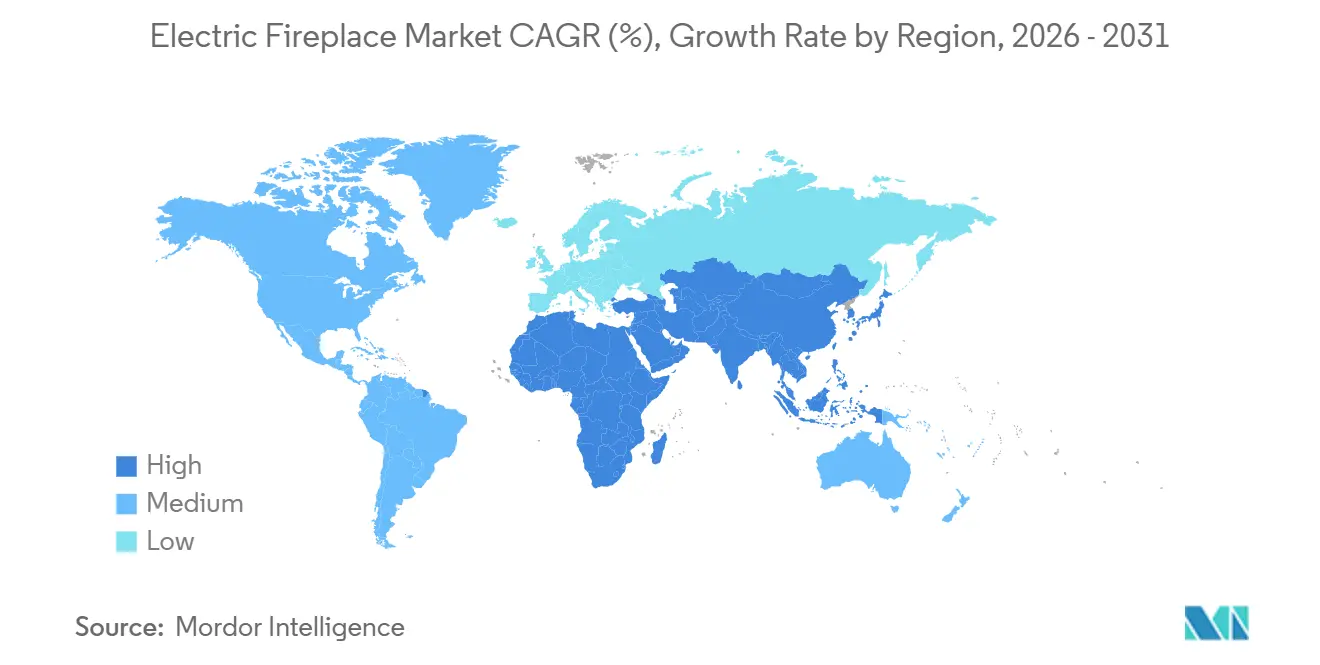

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Fireplace Market Analysis by Mordor Intelligence

The electric fireplace market size is expected to grow from USD 2.65 billion in 2025 to USD 2.76 billion in 2026 and is forecast to reach USD 3.38 billion by 2031 at a 4.13% CAGR over 2026–2031. Market growth is driven by building decarbonization policies and construction codes that favor all-electric heating systems, encouraging developers and retrofitters to adopt wall-mounted and built-in electric fireplaces for aesthetics and zone heating without combustion risks. Premium flame-effect technologies and smart-home integration are driving price differentiation and sustaining margins in the mid-to-upper segments, while entry-level products face price pressure from online retail and overseas OEMs. Regional trends indicate that North America leads in revenue due to a mature retrofit market and higher average selling prices, whereas Asia-Pacific shows the fastest growth, supported by urban housing demand and air-quality regulations that promote electrified heating solutions. In Europe, adoption continues at a steady pace, although energy tariffs and a focus on heat pumps limit electric fireplaces primarily to decorative or supplemental use. Compliance with Ecodesign requirements, such as electronic thermostats and open-window detection, further shapes product design and functionality.

Key Report Takeaways

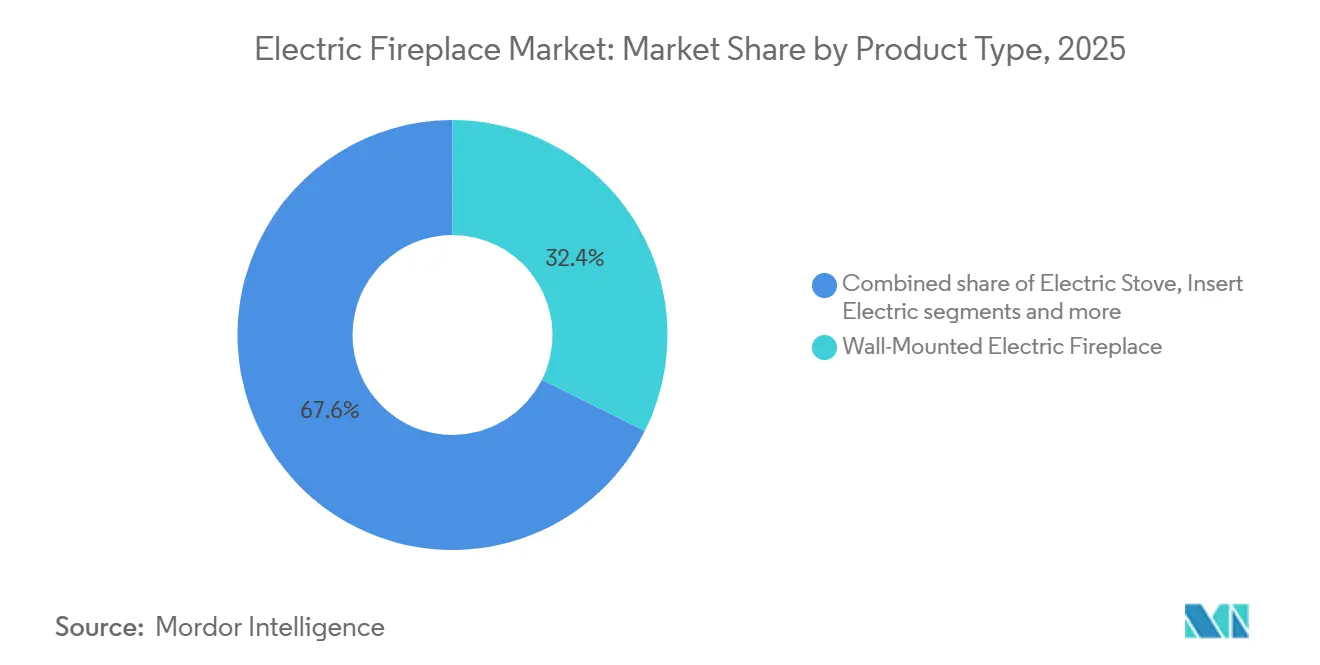

- By product type, wall-mounted electric fireplaces led with 32.37% of the electric fireplace market share in 2025 and posted the fastest 7.24% CAGR toward 2031.

- By size, small units under 32 inches held 38.37% of the electric fireplace market share in 2025, while medium-format fireplaces between 45 and 60 inches recorded the fastest 7.84% CAGR through 2031.

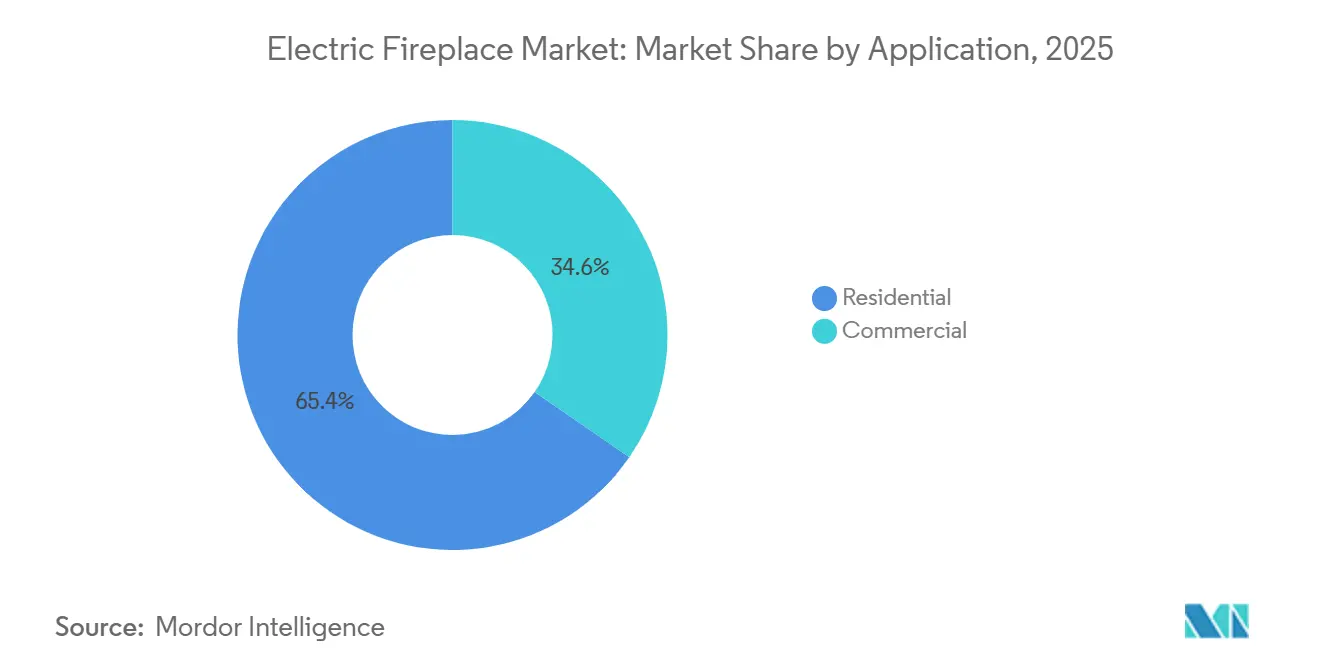

- By application, residential installations accounted for 65.37% of the electric fireplace market share in 2025, and commercial sites advanced at a 5.1% annual growth rate.

- By distribution channel, B2C retail represented 63.37% of the electric fireplace market share in 2025, and B2B project sales posted the fastest 6.65% CAGR.

- By geography, North America commanded 41.74% of the electric fireplace market share in 2025, and Asia-Pacific achieved the fastest 8.27% CAGR to 2031 in line with urban housing activity and stricter air-quality measures in major cities.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electric Fireplace Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Carbon-reduction mandates favoring electric heat | +1.2% | North America, Europe, rapidly urbanizing APAC metros | Medium term (2-4 years) |

| Post-pandemic renovation surge demanding plug-in hearths | +0.9% | Global developed urban centers | Short term (≤2 years) |

| Smart-home integration uplift for connected fireplaces | +1.1% | North America, Europe, affluent APAC markets | Medium term (2-4 years) |

| Municipal bans on wood and gas hearths | +0.8% | Europe, North America, selected APAC cities | Short term (≤2 years) |

| Advanced flame visuals boosting premium sales | +0.5% | Global luxury residential and commercial segments | Medium term (2-4 years) |

| Expansion of e-commerce channels enhancing product reach | +0.4% | Global, with strongest impact in digitally mature regions | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Carbon-reduction mandates favoring electric heat

State and city regulations limiting fossil-fuel systems in new buildings are driving growth in the electric fireplace market, as developers increasingly plan all-electric layouts and incorporate decorative zone-heating solutions to maintain aesthetic and functional value. ACEEE’s April 2025 analysis found that electrifying building energy uses with efficient electric heating is far more cost-effective than relying on alternative fuels, which are more expensive and limited in supply, making electrification the preferred strategy for decarbonizing buildings[1]American Council for an Energy Efficient Economy (ACEEE), “Report: Electrification Costs Less than Alternative Fuels for Hardest to Decarbonize Buildings,” aceee.org. In New York, all-electric mandates for many mid-rise projects beginning in 2026 are encouraging the substitution of gas inserts with electric fireplaces, aligning with emissions targets while preserving design intent for common areas and apartments. California’s updated building codes and utility programs further strengthen the electric-first pathway, expanding the retrofit market for non-combustion space heating devices in dense urban areas. Air quality measures restricting wood-burning in sensitive regions support the adoption of electric fireplaces by eliminating the need for chimneys and reducing particulate compliance risks.

Worldwide Urban Remodeling Demanding Plug-and-Play Fireplaces

Remodeling activity and retrofit cycles are fueling demand for electric fireplaces, as plug-in or hardwired units can be integrated into existing interiors with minimal disruption and without the need for gas-line permits or flues. In the Netherlands, the share of homes heated without natural gas rose to about 11% in 2024, with hybrid gas-electric systems also increasing, reinforcing the shift away from gas boilers toward electric and district-heating solutions[2]: Centraal Bureau voor Statistics (CBS), Steeds meer woningen aardgasvrij, cbs.nl, 2025. In the United States, softer permit trends encouraged homeowners to prioritize upgrades and replacements over new construction, favoring electric units that fit media walls and masonry openings. Wood-to-electric inserts eliminate ash and soot while preserving the fireplace as a focal point and supporting compliance with stricter particulate regulations in urban areas. In Asia-Pacific’s dense urban cores, compact apartments drive the adoption of slim, wall-mounted electric fireplaces aligned with entertainment-wall design trends. Brands that simplify recessed installation, standardize framing, and offer low-profile designs are well-positioned to capture demand across retrofit and remodeling projects.

Post-pandemic renovation surge demanding plug-in hearths

Smart-home connectivity has become a standard feature in many higher-volume electric fireplace models, supporting premium pricing through app-based scheduling, voice control, and coordinated lighting scenes. Brands are increasingly pre-installing Wi-Fi modules and integrating with popular voice assistants, making units easier to operate and appealing to younger households investing in connected living spaces. In 2024, about 70.9 % of people in the European Union used internet-connected “smart” devices, including home automation systems, with 12.8 % using smart home appliances and 14.2 % using home energy management systems, highlighting growing readiness for connected electric fireplaces and smart heating integration[3]Eurostat, Internet-connected devices in the EU, etc. europa.EU, 2025. In regions with higher utility costs, consumers favor zone heating and timed operation, leveraging connected fireplaces to provide ambiance while managing energy bills. European trade shows and contractor events highlight growing acceptance of hybrid-electric setups, where electric fireplaces serve both functional and decorative roles during shoulder seasons. These smart features enhance market appeal among style-conscious homeowners and hospitality operators seeking consistent ambiance, low maintenance, and remote management capabilities.

Carbon-reduction mandates favoring electric heat

City and regional regulations limiting wood burning are reducing the appeal of solid-fuel fireplaces in urban areas with poor winter air quality, steering consumers toward electric alternatives that avoid combustion. In Amsterdam, authorities are evaluating restrictions on wood-burning fireplaces after identifying wood smoke as a major contributor to urban soot pollution around one-fifth of particulate emissions and linking it to respiratory conditions such as asthma and COPD. Proposed measures include banning wood-burning installations in new homes and encouraging cleaner alternatives[4]NL Times, Amsterdam eyeing ban on wood burning to improve air quality, nltimes.nl, 2024. Seasonal burn bans and air-quality alert programs also create uncertainty for homeowners and hospitality operators who need reliable, year-round ambiance, making electric fireplaces a practical solution. Commercial buildings face tightening emissions and indoor-air-quality requirements, where zero-combustion electric units align with permitting standards and ESG policies. In Asia’s dense cities, stricter air-quality rules similarly constrain solid-fuel use, allowing electric fireplaces to fill decorative and supplemental heating roles without flues. Collectively, these regulations support sustained demand for electric fireplaces among multifamily developers, boutique hotels, and urban homeowners seeking dependable, low-maintenance solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated power tariffs versus gas alternatives | -0.7% | Europe, parts of North America, developing APAC | Medium term (2-4 years) |

| Skepticism over electric flame authenticity | -0.5% | Global, more acute in traditional fireplace regions | Short term (≤2 years) |

| LED and chip supply instability | -0.3% | Global, manufacturing concentrated in APAC | Short term (≤2 years) |

| Limited consumer awareness in developing markets | -0.2% | South Asia, Africa, parts of Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Elevated power tariffs versus gas alternatives

Rising electricity prices influence operating costs and can reduce the attractiveness of using electric fireplaces for daily heating in regions with high power rates. The cost gap between electricity and natural gas varies by jurisdiction, and households in high-rate areas often limit usage to flame-only modes for ambiance, reducing heating operation. In Europe, persistent electricity-to-gas tariff differentials slow adoption of electric space heating, which also impacts demand for decorative electric fireplaces as buyers weigh total energy costs. At the same time, electric units offer safety, convenience, and low-maintenance benefits, but higher running costs temper repeat purchases among price-sensitive consumers who have access to cheaper gas alternatives. Features like eco modes, flame-only operation, and open-window detection help balance visual appeal with energy efficiency, allowing the market to maintain relevance despite tariff pressures.

Skepticism over electric flame authenticity

Many buyers continue to associate authentic flames with traditional wood-burning fires, which can slow the adoption of electric fireplaces. Cultural expectations for realistic flame visuals strongly influence consumer decisions in several markets. Recent advances in holographic and water-vapor technologies have improved flame depth and created more convincing three-dimensional effects. Despite these improvements, the higher cost of such systems limits their use primarily to premium residential projects rather than mass-market apartments. Manufacturers are also incorporating features like crackling sounds and dynamic ember beds to enhance the sensory experience and make electric fireplaces more appealing as living-room focal points. Differences in regional priorities, including safety, zero emissions, and ease of maintenance, further shape market demand. As technology continues to improve, electric fireplaces are gradually closing the perception gap with traditional fires. Nevertheless, these factors remain important constraints on near-term market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wall-Mounted Units, Anchor Smart-Home Retrofit Wave

Wall-mounted electric fireplaces captured a 32.37% market share in 2025 and grew at a 7.24% CAGR, leading the category as developers and renovators pair them with media walls that do not require gas lines or flues. Buyers favor these models for their installation simplicity, with standard framing and plug-in 120V options that reduce labor and inspection costs. High-end three-sided bay configurations enhance flame visibility from multiple angles, positioning the fireplace as a sculptural element in living rooms and boutique hospitality spaces. The segment also benefits from decoupled heat modes, allowing ambiance without thermal load, which supports year-round use in warm climates or smaller apartments. Smart-home integration, including voice control and app scheduling, further increases appeal as fireplaces are incorporated into lighting scenes and daily routines. Overall, wall-mounted units combine ease of installation, aesthetic flexibility, and technology features, driving strong adoption among both new builds and renovations.

Insert and retrofit formats are increasingly popular as households convert from wood-burning to electric to eliminate ash cleanup and reduce particulate exposure in dense metropolitan areas. Log-set and linear insert options preserve the traditional focal-point look while enabling flame-only modes and on-demand heat, fitting renovation schedules without major structural changes. Freestanding models and mantel packages cater to renters or aging-in-place scenarios where permanent build-ins are not feasible, broadening market reach across diverse housing types. Portable and tabletop options serve niche needs in compact spaces or RVs, though their overall volume remains smaller than recessed or insert models. Smart integration remains a key differentiator, with connected units achieving higher engagement and sell-through online as buyers seek combined ambiance and convenience. Together, these varied formats allow electric fireplaces to meet a wide range of functional and aesthetic demands across residential markets.

By Size: Medium-Format Fireplaces Surge Amid Media-Wall Boom

Small electric fireplaces under 32 inches accounted for 38.37% of the market size in 2025, driven largely by first-time buyers and compact apartments that favor slim designs and simple wiring. Medium formats between 45 and 60 inches recorded the fastest growth at a 7.84% CAGR, reflecting their compatibility with 65-inch televisions and the visual balance they provide in open-plan living rooms. Online popularity of 50-inch smart models highlights the trend toward connected mid-size units featuring multiple flame colors, app control, and voice integration at accessible prices. Designers and installers have shifted from traditional 36 to 42-inch dimensions toward 55 to 65-inch formats to better align with modern TV sizes and wall proportions. These dynamics make mid-size fireplaces central to living-room design while reinforcing their practical role in everyday home life. Overall, small and mid-size units remain key drivers of adoption, combining convenience, aesthetics, and technology integration.

Large fireplaces ranging from 72 to 100 inches are primarily used in hospitality lobbies and upscale residential great rooms, where dramatic visuals justify higher prices and custom installations. Extra-large models over 100 inches rely on modular systems and dedicated circuits, making them more common in commercial and luxury projects rather than typical apartments. Across all sizes, price tiers generally reflect feature sets and installation complexity, with premium models offering advanced flame realism, materials, and smart connectivity. Mid-size adoption continues to grow as households prioritize value, installation simplicity, and the seamless integration of fireplace and media walls. These usage patterns help normalize electric fireplaces as both decorative and supplemental heating solutions. Collectively, the size-based dynamics strengthen the electric fireplace market as part of a broader trend toward electrified interiors in urban settings.

By Application: Residential Dominance Masks Commercial Hospitality Surge

Residential applications represented 65.37% of electric fireplace installations in 2025, as homeowners and developers incorporated them for visual warmth, supplemental heating, and smart-home compatibility in family rooms and bedrooms. Buyers appreciate the absence of combustion byproducts and chimney maintenance, which lowers ongoing costs and reduces compliance risks while maintaining a traditional focal point in interiors. Features such as smart controls, flame-only modes, and compact footprints enable use in smaller apartments that lack ventilation for gas fireplaces. New product launches highlighting realistic flame effects, immersive soundscapes, and customizable media beds further enhance perceived quality and strengthen purchase intent among design-conscious homeowners. These trends reinforce residential demand as the core driver of the electric fireplace market. Connected models are increasingly positioned as mainstream appliances for home décor, comfort, and everyday convenience.

Commercial installations grew at a 5.1% CAGR, with hospitality operators retrofitting lobbies and lounges using linear electric fireplaces to elevate ambiance and simplify operations compared with solid-fuel or gas options. Large-format displays with 3D flame effects enhance brand experiences and guest satisfaction while reducing maintenance and ventilation needs. Office and mixed-use properties with ESG targets and local emissions regulations also prefer electric fireplaces to avoid combustion in shared spaces. Tightening building codes have led facility managers to adopt electric fireplaces in reception areas and amenity lounges, ensuring consistent performance, safety, and year-round uptime. These commercial dynamics complement the residential base by expanding adoption into public-facing environments. Overall, both residential and commercial applications support long-term growth for the electric fireplace market.

By Distribution Channel: B2C Retail Channels Lead, B2B Project Sales Gain Traction

B2C retail channels accounted for 63.37% of the electric fireplace market size in 2025, as online marketplaces and home centers expanded assortments of connected models with competitive pricing and fast delivery. E-commerce supports long-tail SKUs and smart features that appeal to tech-savvy buyers, with many listings highlighting app control, voice integration, and multi-color flame options. Brand-direct websites showcase slim built-ins and premium finishes that are difficult to stock in all physical stores, improving price transparency and market access. Big-box and specialty retailers feature larger units and connected options for DIY installation, aligning with the growing adoption of media-wall integrations in living rooms. This combination reinforces B2C leadership, allowing consumers to discover, compare, and purchase feature-rich electric fireplaces through digital and retail channels. Overall, B2C platforms continue to drive awareness and adoption among residential buyers.

B2B project sales are expanding due to decarbonization regulations and multifamily design trends that standardize built-ins across units and shared spaces. Hospitality chains and boutique hotels often secure volume discounts and warranties for large-format installations, making B2B attractive for both buyers and suppliers under predictable construction timelines. Manufacturers offer programs for architects and contractors, including specification support, site consultation, and compliance documentation that streamline approvals in regulated areas. As building codes evolve, established B2B relationships become crucial for ensuring certified components and clear installation guidance. These dynamics strengthen the project pipeline for built-in models across commercial and multifamily settings. Together, B2B and B2C channels provide broad market access with differentiated products and services tailored to residential and commercial needs.

Geography Analysis

North America accounted for 41.74% of the global electric fireplace market size in 2025, driven by higher average selling prices, a mature replacement cycle, and city-level air quality regulations limiting solid-fuel use in dense metropolitan areas. U.S. building-permit data indicated pressure in 2025, favoring remodeling over new construction and benefiting plug-and-play electric models in existing homes and condos. Electricity tariffs influence the use of heating modes, encouraging homeowners to rely on flame-only settings and timers or eco features that manage energy draw. Local wood-smoke rules and air-quality alert programs push consumers away from wood stoves toward non-combustion alternatives, eliminating particulate emissions and chimney maintenance. As municipal rules and building codes expand electrification, contractors and developers increasingly incorporate electric fireplaces in all-electric projects. These factors collectively support steady demand for electric fireplaces throughout the forecast period.

Asia-Pacific is the fastest-growing region, with an 8.27% CAGR projected through 2031, as urban apartments and air-quality priorities drive demand for decorative and supplemental electric heating solutions. Consumers favor small to medium-sized units that integrate with media walls, offer multi-color flames, and support app control, while local brands in Japan and Australia target early adopters with connected designs. High-density living and limited ventilation in many apartments make electric fireplaces practical for ambiance, while tech-forward buyers value integration with lighting and HVAC systems. Premium lines that emphasize realistic flames and multiple sizes indicate increased investment from regional suppliers seeking to balance style and performance. These regional conditions expand the reach of electric fireplaces in APAC’s largest cities. Products are increasingly designed with slim profiles, quiet operation, and controllable heat to meet urban consumer needs.

Europe maintains meaningful adoption due to safety, ease of use, and low-maintenance features, although electricity tariffs and heat pump priorities position electric fireplaces primarily as decorative or supplemental heating options. Policy environments favor efficient electric systems in new buildings, with standards requiring electronic thermostats and open-window detection that align with higher-quality fireplace offerings. In Germany, the 2025 energy policy emphasizes decarbonizing building heat, creating tension between electricity costs and the desire for low-emission, simple indoor comfort. Consumers often rely on flame-only modes for year-round ambiance and activate heat on demand, supporting consistent use in living rooms and hospitality areas. Regional regulations restricting combustion help maintain steady traction for electric fireplaces. Property owners increasingly prioritize low-maintenance design features for modern interiors, further supporting market growth.

Mordor Intelligence provides coverage of the electric fireplace market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United States and France incorporating local coverage and market participation, as required.

Competitive Landscape

The electric fireplace market exhibits moderate concentration, as the combined share of the leading players represents less than half of the total market. This reflects a moderately fragmented landscape, providing opportunities for regional and niche competitors to grow and capture market share. Glen Dimplex leads in water-vapor and LED-based flame realism, offering linear formats with year-round ambiance and controllable heat for both residential and commercial spaces. Hearth & Home Technologies expands connected offerings aimed at contractors and custom-home builders, providing turnkey specifications and reliable performance across multiple sizes. Premium brands emphasize flame fidelity and layered visual effects, while mainstream brands focus on installation ease, safety, and value through online channels. This diverse landscape sustains market momentum as aesthetics, compliance, and digital control strongly influence buyer decisions.

The electric fireplace market also prioritizes safety as a key differentiator, with manufacturers integrating overheat monitoring and certifications to meet multi-market compliance standards. Twin-Star’s branded line with built-in overheating sensors addresses both consumer expectations and B2B risk management in high-traffic areas. Modern Flames’ Orion series sets benchmarks for LCD-based flames and continues to evolve toward higher realism and motion fidelity for premium applications. Product features that combine smart-home compatibility, flame realism, and flexible installation depth guide channel strategies and assortment decisions in retail and project markets. These approaches strengthen brand positioning across price points and sustain category growth as regulations and consumer preferences align with electric solutions. Overall, safety, performance, and digital features remain central to competitive differentiation.

The electric fireplace market continues to see investment in scale, logistics, and regional assembly to stabilize delivery and manage component supply risks. Product roadmaps emphasize smarter controls, more natural flame movement, and improved media beds and trim materials, enhancing perceived value in living rooms and hospitality spaces. Retailers expand connected assortments, while project channels prioritize certified systems with strong installation support, driving repeat specification from architects and designers. These strategies keep competition active as brands respond to evolving codes, styling trends, and demand for low-maintenance ambiance. The market remains dynamic, consolidating around smart, realistic, and code-compliant designs that deliver consistent performance. Collectively, these efforts ensure the electric fireplace market continues to grow across both residential and commercial applications.

Electric Fireplace Industry Leaders

Glen Dimplex Group

Twin-Star Home (Duraflame)

Napoleon Fireplaces

Hearth & Home Technologies

Empire Comfort Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Twin-Star Home expanded its collaboration with Duraflame and launched a line of full-size electric fireplaces integrating SaferPlug overheating sensors, with ten new designs presented at High Point Spring Market for furniture retailers and curated selections for e-commerce.

- October 2025: Acucraft Fireplaces introduced its new Vapor line featuring patent‑pending MaxFlow™ Technology, which produces tall, full, and highly realistic cool‑touch flames powered by water and light. The collection launched in late 2025 with options for luxury homes, hotels, and commercial spaces, offering customizable sizes and safer, zero‑emission operation.

- April 2025: Litedeer Homes released the Latitude 55-inch built-in smart electric fireplace with five flame colors, WiFi control, and GT-Xview HD LED, part of a 2025 collection of slim designs for media-wall installations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global electric fireplace market as the yearly revenue earned from factory-built electric heaters that recreate a flame effect via LED, infrared, or water-vapor technology while supplying up to 5 kW of space heat in residential and light-commercial interiors. Units sold as wall-mounted panels, inserts, freestanding stoves, mantels, and built-in boxes are counted at manufacturer selling price in U.S. dollars.

Scope Exclusions: replacement heating elements, decorative displays without an integrated heater, and spare parts are outside this scope.

Segmentation Overview

- By Product Type

- Electric Stove

- Insert Electric Fireplace

- Tabletop Electric Fireplace

- Wall-Mounted Electric Fireplace

- Freestanding Electric Fireplace

- By Size

- Small

- Medium

- Large

- Extra-Large

- By Application

- Residential

- Commercial

- By Distribution Channel

- B2C/Retail Channels

- Supermarkets and Hypermarkets

- Home Centers

- Specialty Stores/Fireplace Stores (Including Exclusive Brand Outlets)

- Online

- Other Distribution Channels

- B2B/Project

- B2C/Retail Channels

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team interviewed heater OEM engineers, specialty retailers on three continents, and building-code inspectors; their views on average selling prices, channel shifts, and imminent regulations sharpened findings and closed gaps.

Desk Research

Mordor analysts began by matching HS 8516.29 trade codes across UN Comtrade, Eurostat, and U.S. Census files, creating a verifiable production pool. Household-spend series from the World Bank and the OECD, plus energy-efficiency rules from the U.S. DOE, Environment Canada, and the EU Ecodesign directive shaped regional demand. Industry cues flowed through the Hearth, Patio & Barbecue Association, Building Products Council briefs, company 10-Ks, Dow Jones Factiva feeds, and Questel patent clusters. The sources named are illustrative; many others guided validation.

Market-Sizing & Forecasting

A top-down construct starts with global production plus net exports for HS 8516.29, then converts volumes to revenue using blended ASPs from interviews. Selective bottom-up checks on nine major manufacturers and e-commerce sellers test totals before lock-in. Forecasts draw on housing completions, renovation outlays, electricity tariffs, smart-home penetration, and bans on solid-fuel fireplaces; all run through a multivariate regression. Scenario analysis flexes the baseline when electricity prices or construction cycles deviate.

Data Validation & Update Cycle

Outputs face automated variance flags, peer review, and senior sign-off. Reports refresh each year, with interim updates when tariffs shift or codes change.

Why Mordor's Electric Fireplace Baseline Earns Reliance

Published values differ because providers group products differently, apply varied price ladders, and refresh at uneven intervals.

Mordor Intelligence sizes 2025 revenue at USD 2.53 billion. A global consultancy quotes USD 2.45 billion for 2024. A regional publisher lists USD 2.14 billion for 2024. A trade journal states USD 2.46 billion for 2024.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.53 B (2025) | Mordor Intelligence | None |

| USD 2.45 B (2024) | Global Consultancy A | Decorative units included; single-region ASP used globally |

| USD 2.14 B (2024) | Regional Publisher B | Inserts omitted; constant 2020 FX |

| USD 2.46 B (2024) | Trade Journal C | Web survey only; no trade-data check |

Taken together, the comparison shows our production-anchored, annually refreshed baseline offers a balanced midpoint that decision-makers can trace to observable variables and repeatable steps.

Key Questions Answered in the Report

What is the electric fireplace market size and expected growth by 2031?

The electric fireplace market size is USD 2.76 billion in 2026 and is projected to reach USD 3.38 billion by 2031 at a 4.13% CAGR, reflecting steady code-driven adoption across regions.

Which region leads and which region grows fastest within the electric fireplace market?

North America leads with a 41.74% revenue share due to retrofits and higher selling prices, while Asia-Pacific grows fastest with an 8.27% CAGR, supported by urban apartments and air-quality rules.

Which product and size segments show the strongest momentum in the electric fireplace market?

Wall-mounted units lead with 32.37% share and a 7.24% CAGR, and medium formats between 45 and 60 inches grow fastest at a 7.84% CAGR as they pair with large televisions in open-plan rooms.

What channel dynamics are shaping sales in the electric fireplace market?

B2C retail accounts for 63.37% with strong online momentum for connected models, and B2B projects grow faster at a 6.65% CAGR as developers standardize built-ins for compliance.

Page last updated on: