Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 28.80 Billion |

| Market Size (2026) | USD 30.37 Billion |

| Market Size (2031) | USD 39.61 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Customs Brokerage Market Analysis by Mordor Intelligence

The Europe Customs Brokerage Market size was valued at USD 28.80 billion in 2025 and estimated to grow from USD 30.37 billion in 2026 to reach USD 39.61 billion by 2031, at a CAGR of 5.45% during the forecast period (2026-2031).

The expansion stems from the post-Brexit surge in customs declarations, e-commerce’s escalating low-value import volumes, and the European Union’s Customs Reform 2028 data-hub program, which is automating real-time risk analysis. Integrated freight forwarders are accelerating acquisitions to capture scale benefits, while traditional brokerages upgrade digital capabilities to defend share. The adaptive response of brokers to new Import One-Stop Shop (IOSS) rules, dual-use export-control audits, and AI-based HS-code tools is reshaping service portfolios. Geographically, Germany’s manufacturing core and Poland’s near-shoring momentum anchor short-term opportunities, whereas pan-EU API connectivity promises long-term efficiency gains. Across these dynamics, the Europe customs brokerage market continues to pivot from paper-centric clearance toward data-centric compliance.

Key Report Takeaways

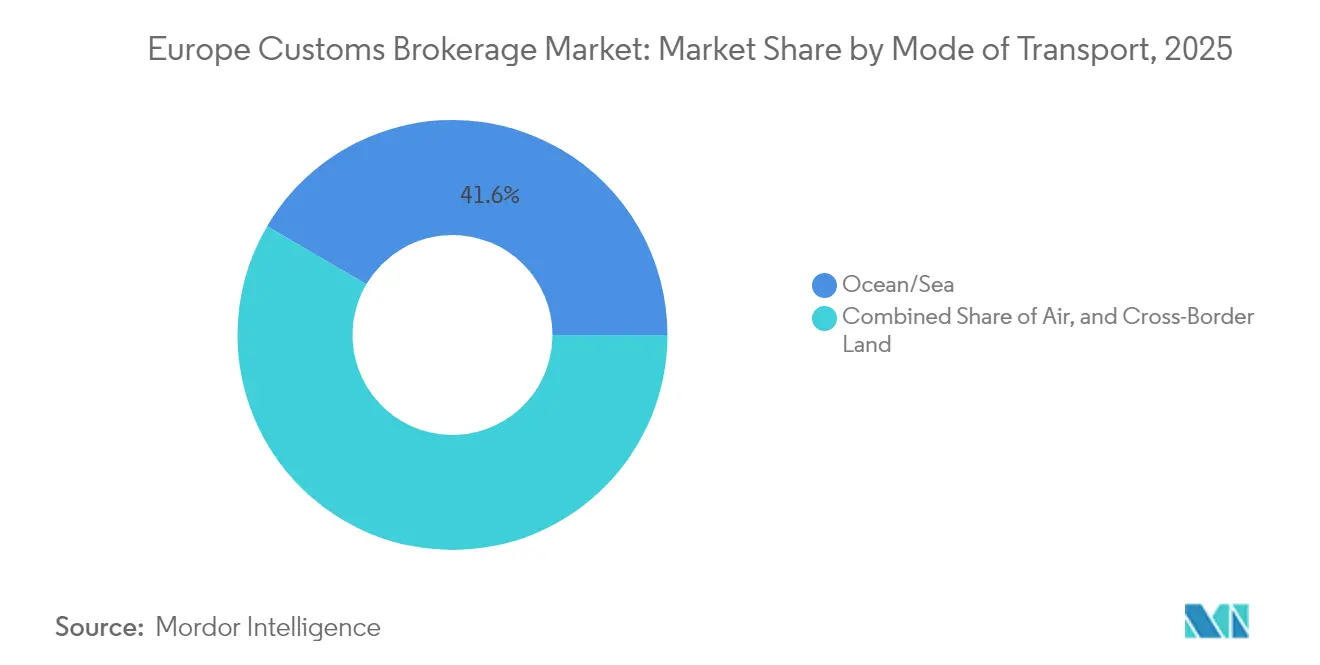

- By mode of transport, ocean/sea led with 41.55% revenue share in 2025; cross-border land is projected to expand at a 4.62% CAGR through 2031.

- By broker type, freight forwarder/3PL-integrated brokers held 50.40% of the Europe customs brokerage market share in 2025, whereas traditional brokerages are advancing at a 5.12% CAGR to 2031.

- By importer size, large enterprises accounted for 38.45% share of the Europe customs brokerage market size in 2025, and mid-market is forecast to grow at 3.98% CAGR between 2026-2031.

- By end-use industry, retail and e-commerce captured 22.70% share in 2025 while automotive and EV segment is poised to register a 4.92% CAGR through 2031.

- By geography, Germany commanded 20.65% share of the Europe customs brokerage market size in 2025, with Poland anticipated to expand at 4.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Customs Brokerage Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Brexit surge in customs declarations | +1.2% | UK, Ireland, Netherlands, Belgium | Short term (≤ 2 years) |

| E-commerce-driven rise in low-value import clearances | +0.8% | Global, with concentration in Germany, Netherlands, France | Medium term (2-4 years) |

| EU Customs Reform 2028 data-hub roll-out | +1.1% | EU27, with early adoption in Netherlands, Germany | Long term (≥ 4 years) |

| AI-based HS-code classification adoption | +0.9% | Global, led by Netherlands, Germany, UK | Medium term (2-4 years) |

| Near-shoring to Eastern Europe boosting cross-border volumes | +1.0% | Poland, Romania, Czech Republic, with spillover to Germany | Medium term (2-4 years) |

| Tightening dual-use export-control compliance | +0.7% | EU27, UK, with focus on technology hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-Brexit Surge in Customs Declarations

The United Kingdom’s departure from the EU triggered a multi-fold rise in declaration volumes, driving sustained demand for brokerage expertise. New rules of origin checks, risk-based sanitary controls under the Border Target Operating Model, and Northern Ireland’s Windsor Framework two-lane system have multiplied document touchpoints per shipment[1]“EU Customs Reform,” European Commission, EUROPA.EU. Specialized brokers now package consulting, data validation, and automated audit trails to help traders avoid duty misclassification penalties. Integrated providers are embedding API links to HMRC’s Customs Declaration Service, cutting processing time and reducing manual errors. As UK-EU traffic normalizes, complexity rather than sheer volume will sustain brokerage revenue, ensuring the Europe customs brokerage market continues to rely on human expertise for high-risk commodities.

E-Commerce-Driven Rise in Low-Value Import Clearances

Elimination of the EUR 22 de minimis threshold and the mandatory IOSS regime shifted VAT collection to the point-of-sale, compelling platforms and sellers to integrate customs workflows[2]“UK Trade Bulletin,” HM Revenue & Customs, GOV.UK. Brokers with robust IT interfaces are onboarding marketplaces that ship thousands of daily parcels into Germany and the Netherlands. Parcel operators leverage network reach, yet niche brokers gain share by offering rule-based product classification, dynamic VAT calculation, and automated returns documentation. The Europe customs brokerage market is therefore witnessing intensified competition, with technology literacy overtaking scale as the main differentiator in B2C clearances.

EU Customs Reform 2028 Data-Hub Roll-Out

The EU’s single data-hub platform will consolidate declarations, duties, and risk profiles across member states via standardized APIs. Early pilots in the Netherlands demonstrated multi-country clearance within minutes, prompting brokers to fast-track API investment. Enhanced Authorized Economic Operator (AEO) benefits such as fewer inspections motivate brokers and their clients to adopt higher compliance tiers. Companies offering full-stack e-Customs solutions already position themselves as indispensable partners for traders navigating the pending “customs as a service” environment. Over the long term, platform readiness will determine competitive survival in the Europe customs brokerage market.

AI-Based HS-Code Classification Adoption

Machine-learning models embedded in brokerage platforms are slashing classification errors by double-digit margins, significantly reducing customs holds and post-entry amendments. Major ocean carriers and integrators have rolled out global AI customs tools that suggest optimal duty mitigation paths based on historic trade data. Early adopters integrate sensors and IoT feeds to forecast compliance risks before goods arrive at EU borders, enhancing customer visibility. Smaller independent brokers, while recognizing the productivity upside, face capital constraints that impede full AI deployment. Divergent adoption speeds are widening the capability gap, contributing to consolidation waves in the Europe customs brokerage market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geopolitical trade disruptions in EU border corridors | -0.6% | Eastern EU borders, Middle Corridor routes | Short term (≤ 2 years) |

| EU customs-talent shortages & ageing workforce | -0.5% | Germany, Netherlands, France, with spillover effects | Medium term (2-4 years) |

| Rising IT & automation fee burden on small brokers | -0.4% | Small independent brokers across EU | Medium term (2-4 years) |

| Parcel operators cannibalising low-value clearances | -0.3% | High e-commerce volume countries: Germany, France, UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Geopolitical Trade Disruptions in EU Border Corridors

Conflict-driven rerouting from the Northern route to the Middle Corridor has increased transit times and customs congestion at Turkish, Georgian, and Kazakh borders[3]“VAT E-Commerce,” European Commission, EUROPA.EU. Brokers face volatile regulatory environments, currency swings, and emerging sanctions checks, which collectively raise processing costs. Automotive and electronics importers in Germany confront uncertainty incompatible with just-in-time norms, thereby dampening shipment volumes. The resulting unpredictability restrains the Europe customs brokerage market’s short-term growth.

EU Customs-Talent Shortages and Ageing Workforce

A sizable share of senior declarants in Germany and the Netherlands are nearing retirement, and training pipelines lag behind regulatory change. Wage inflation for specialized customs knowledge inflates operating costs, particularly for small and mid-sized firms. While automation alleviates repetitive tasks, complex advisory functions still depend on human expertise. This talent gap restrains service capacity in the Europe customs brokerage industry and could slow onboarding of new clients until workforce renewal stabilizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Transport: Ocean Commanding, Land Accelerating

Ocean/sea services owned 41.55% of the Europe customs brokerage market in 2025, mirroring Europe’s heavy reliance on Asian imports through Rotterdam, Hamburg, and Antwerp. Port-centric brokers generate premium revenue by managing intricate documentation for automotive components, electronics, and industrial machinery. Cross-border land services are forecast to grow at a 4.62% CAGR, benefiting from factory relocations into Poland and Romania that shorten supply routes. Tightened truck security checks and the digitalization of road transit procedures encourage brokers to integrate e-TIR and NCTS-Phase 5 modules, reinforcing land-mode relevance. Over the forecast horizon, Europe customs brokerage market momentum will hinge on synchronized port-to-inland digital corridors that balance sea dominance with growing intra-European trucking flows.

By Broker Type: Scale vs. Specialism

Freight forwarder/3PL-integrated brokers captured 50.40% of 2025 revenue as shippers gravitated toward single-provider logistics solutions. Their technology budgets, global network reach, and ability to bundle warehousing create formidable entry barriers. Traditional pure brokers defend share through niche expertise in pharmaceutical imports, dual-use goods, and AEO consultancy. The Europe customs brokerage market size for integrated brokers is set to compound at 4.26% CAGR, but pure specialists still attract clients needing tailored compliance. As mega-deals such as DSV’s USD 15.9 billion acquisition of DB Schenker close, competitive intensity will pivot on advisory depth rather than freight capacity.

By Importer Size: Enterprise Volume, Mid-Market Upside

Large enterprises drove 38.45% of brokerage revenue in 2025 thanks to complex multi-country supply chains, but mid-market firms are the fastest risers at 3.98% CAGR. ERP-API integrations, dashboard analytics, and duty-optimization audits make brokerage indispensable to mid-cap manufacturers expanding cross-border sourcing. SMEs favor simplified digital portals, yet remain price-sensitive. As EU data-hub standardization lowers procedural friction, mid-market adoption will deepen, broadening the Europe customs brokerage market’s addressable client base.

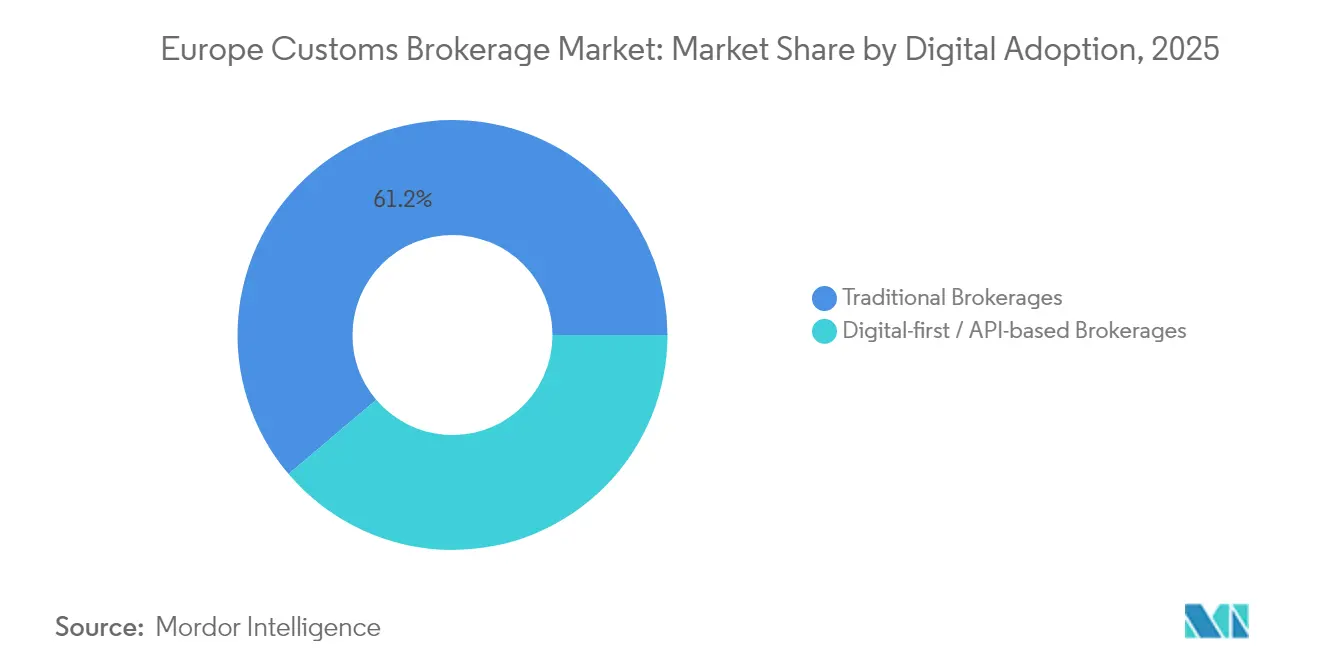

By Digital Adoption: Hybrid Winning Formula

Traditional brokerages still command 61.20% share and post a surprising 5.12% CAGR, illustrating that digital upgrades reinforce not replace relationship-centric models. Investments in automated tariff classification, client-facing portals, and single-window submission tools enhance service speed while preserving human oversight. Digital-first/API-centric providers attract fast-growing e-commerce shippers but struggle with multi-jurisdictional exceptions. The Europe customs brokerage industry therefore prizes a hybrid value proposition that marries cloud automation with regulatory expertise.

By End-User Industry: Retail Dominant, Automotive Surging

Retail and e-commerce led 2025 revenue at 22.70%, propelled by IOSS compliance, reverse-logistics filings, and rapid-cycle B2C clearances. Automotive and EV shipments are projected to grow 4.92% CAGR as battery rules, origin requirements, and anti-dumping duties on Chinese EVs complicate filing structures. Electronics and semiconductors, pharmaceuticals, and aerospace demand deep regulatory knowledge, ensuring multi-sector resilience for the Europe customs brokerage market.

Geography Analysis

Germany maintained the largest regional footprint with 20.65% market share in 2025, supported by strong manufacturing exports and premier port infrastructure in Hamburg and Bremen. High-value industrial cargoes intensify demand for end-to-end clearance services, and the government’s drive to digitize customs transactions positions Germany as a reference market for technology pilots. The United Kingdom remains a pivotal node; ongoing CHIEF-to-CDS migration obliges brokers to manage dual systems, sustaining advisory revenues.

Poland is the fastest-growing geography with a 4.55% CAGR as manufacturers relocate assembly lines closer to Western Europe, boosting truck and rail traffic across Eastern borders. Investments in road-rail intermodal hubs and simplified transit procedures reinforce Poland’s ascent within the Europe customs brokerage market. France and the Netherlands benefit from gateway roles Calais and Rotterdam funnel Asian imports inland while Italy leverages Mediterranean routes for fashion and perishables. Spain capitalizes on Valencia’s port upgrades to serve North African trade lanes. Collectively, these shifts underscore a pan-European pivot toward shorter, digitally-orchestrated supply chains that expand brokerage opportunities beyond legacy hubs.

Competitive Landscape

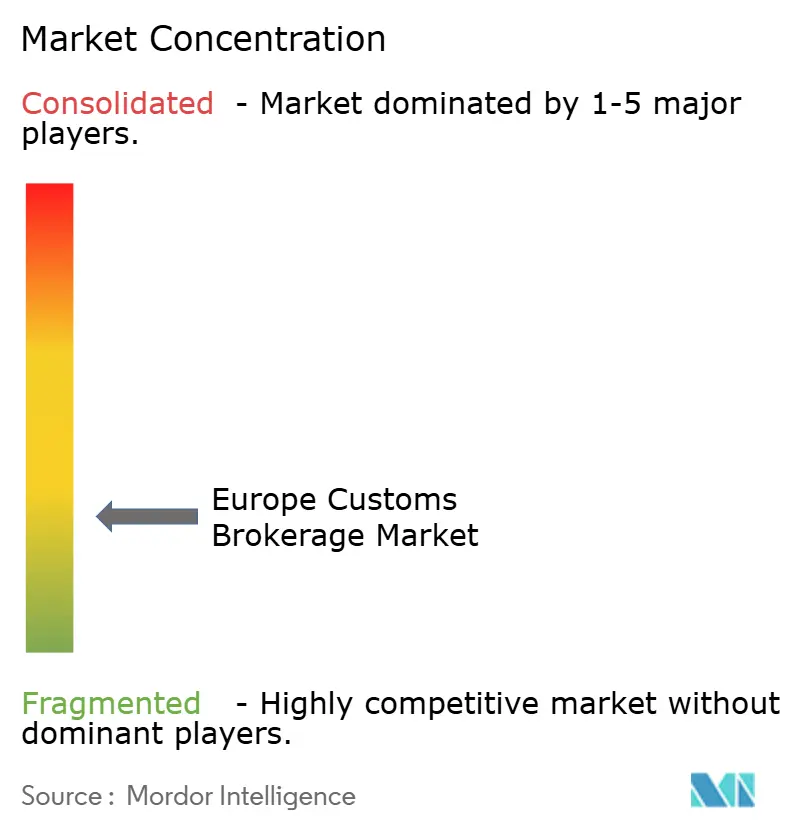

The market is moderately fragmented. The DSV-DB Schenker merger creates the world’s largest freight forwarder, amplifying integrated customs offerings across Europe. Customs Support Group has pursued a bolt-on strategy, adding targeted brokers in Italy, Norway, the UK, and Switzerland to build a pan-regional digital platform. Technology adoption differentiates leaders; firms deploy AI classification engines, IoT-linked risk analytics, and SaaS client dashboards to descend processing times from hours to minutes. Authorized Economic Operator certification further consolidates demand among compliant networks.

Mid-tier specialists focus on high-complexity verticals such as dual-use goods, life-science cold chains, or defense logistics, niches less sensitive to commoditized pricing. API-first challengers penetrate B2C segments by automating low-value clearances, yet struggle to scale human expertise for exception management. Overall, the Europe customs brokerage market gravitates toward hybrids that unify data-driven speed with regulatory mastery. Intensifying capital requirements and talent shortages are likely to accelerate M&A activity through 2030, gradually raising market concentration.

Europe Customs Brokerage Industry Leaders

Livingston International

DHL Group

Kuehne + Nagel

Rhenus Logistics

Gerlach Customs

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSV announced a USD 15.9 billion takeover of DB Schenker, lifting combined annual revenue above USD 39 billion and expanding Europe-wide customs capacity.

- January 2025: WiseTech Global acquired Swedish customs-software firm CargoIT, bolstering Nordic digital brokerage coverage

- January 2025: Customs Support Group bought UK Customs Solutions, adding 150 staff across Felixstowe, Nottingham, Glasgow, and Dover.

- January 2025: Customs Support deepened Swiss reach via Zollimpex acquisition, securing five border offices for high-speed clearances.

Europe Customs Brokerage Market Report Scope

Customs brokerage firms facilitate the shipment and delivery of goods across geographical borders for individuals and organizations.

The European customs brokerage market is segmented by mode of transport and geography. By mode of transport, the market is segmented into sea, air, and cross-border land transport, and by geography, the market is segmented by Germany, United Kingdom, France, Netherlands, Italy, and the Rest of Europe.

The report offers market size and forecasts for the Europe customs brokerage market in value (USD) for all the above segments.

By Mode of Transport

| Ocean / Sea |

| Air (Express and General Cargo) |

| Cross-Border Land (Truck and Rail) |

By Broker Type

| Pure Customs Broker |

| Freight Forwarder / 3PL-Integrated Brokers |

By Importer Size

| Large Enterprisess |

| Mid-Market |

| SMEs / Micro-shippers |

By Digital Adoption

| Traditional Brokerages |

| Digital-first / API-based Brokerages |

By End-Use Industry

| Retail and E-commerce |

| Automotive and EV |

| Electronics and Semiconductors |

| Pharmaceuticals and Life Sciences |

| Aerospace and Defense |

| Chemicals and Industrial Goods |

| Others |

By Country

| Germany |

| United Kingdom |

| France |

| Netherlands |

| Italy |

| Spain |

| Poland |

| Rest of Europe |

| By Mode of Transport | Ocean / Sea |

| Air (Express and General Cargo) | |

| Cross-Border Land (Truck and Rail) | |

| By Broker Type | Pure Customs Broker |

| Freight Forwarder / 3PL-Integrated Brokers | |

| By Importer Size | Large Enterprisess |

| Mid-Market | |

| SMEs / Micro-shippers | |

| By Digital Adoption | Traditional Brokerages |

| Digital-first / API-based Brokerages | |

| By End-Use Industry | Retail and E-commerce |

| Automotive and EV | |

| Electronics and Semiconductors | |

| Pharmaceuticals and Life Sciences | |

| Aerospace and Defense | |

| Chemicals and Industrial Goods | |

| Others | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Netherlands | |

| Italy | |

| Spain | |

| Poland | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe customs brokerage market by 2031?

The market is expected to reach USD 39.61 billion by 2031.

Which transport mode currently generates the most brokerage revenue across Europe?

Ocean and sea shipments lead with a 41.55% share of customs brokerage revenue.

How will EU Customs Reform 2028 affect brokers?

The reform’s centralized data-hub will standardize declarations across member states, rewarding brokers that integrate API connections for real-time processing.

Why is Poland viewed as the fastest-growing national market?

Near-shoring of manufacturing to Eastern Europe and upgraded border infrastructure push Poland’s brokerage market toward a 4.55% CAGR through 2031.

What differentiates traditional brokers from digital-first providers?

Traditional firms combine deep regulatory expertise with newly adopted automation tools, whereas digital-first providers emphasize API-driven speed but may lack complex advisory capacity.

Which end-use industry is expected to grow fastest through 2031?

Automotive and EV shipments are forecast to expand at a 4.92% CAGR due to battery regulations and origin-based duty calculations.

Page last updated on: