Commercial Satellite Imaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

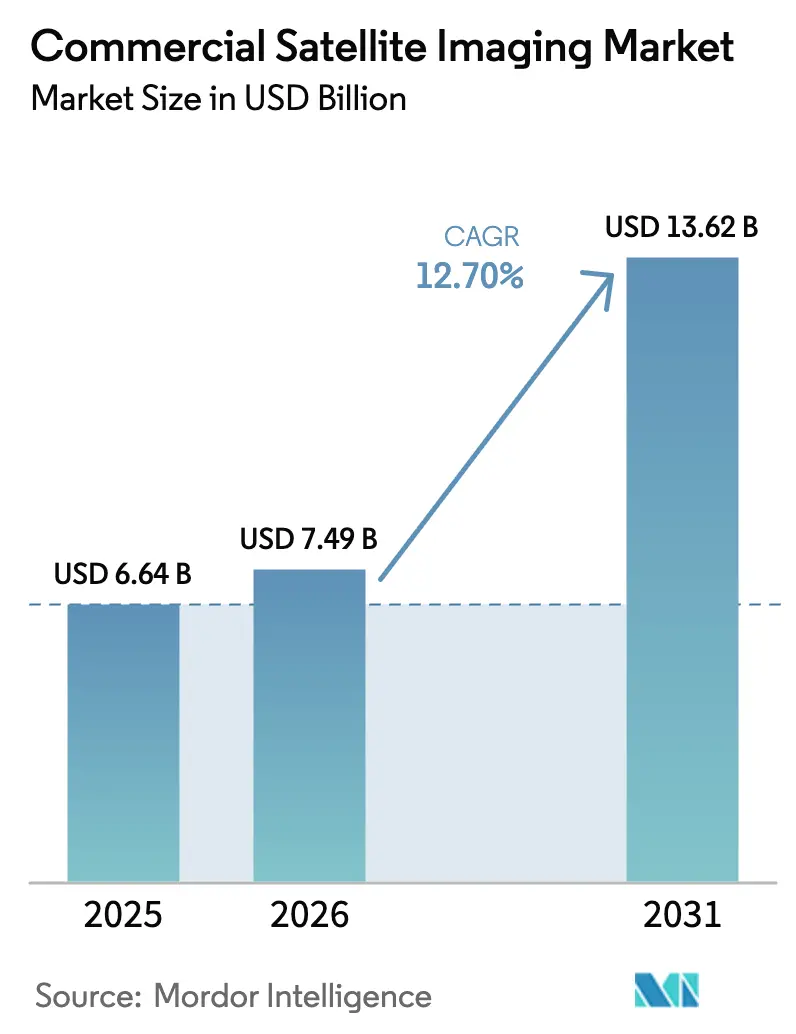

| Market Size (2026) | USD 7.49 Billion |

| Market Size (2031) | USD 13.62 Billion |

| Growth Rate (2026 - 2031) | 12.70% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Satellite Imaging Market Analysis by Mordor Intelligence

The commercial satellite imaging market size reached USD 7.49 billion in 2026 and is projected to attain USD 13.62 billion by 2031, reflecting a 12.7% CAGR. Mandatory methane-emissions verification, AI-driven tip-and-cue tasking, rapid expansion of synthetic-aperture-radar (SAR) microconstellations, and adoption of big-data analytics are reshaping procurement behavior among government and enterprise buyers. Momentum is reinforced by the European Union Methane Regulation, which has converted voluntary monitoring into a compliance obligation across North Sea and Mediterranean basins. Venture-backed operators undercut incumbents on price while delivering higher temporal resolution, accelerating commoditization yet widening the addressable customer base. Rising smart-city projects in Asia-Pacific, persistent Arctic surveillance requirements, and cloud-native analytics subscriptions are broadening use cases and supporting long-run demand elasticity. Capital-intensive constellation builds, data-sovereignty constraints, and orbital-safety bottlenecks, however, continue to strain margins and elongate payback periods, prompting providers to seek differentiated sensor modalities and proprietary analytics.

Key Report Takeaways

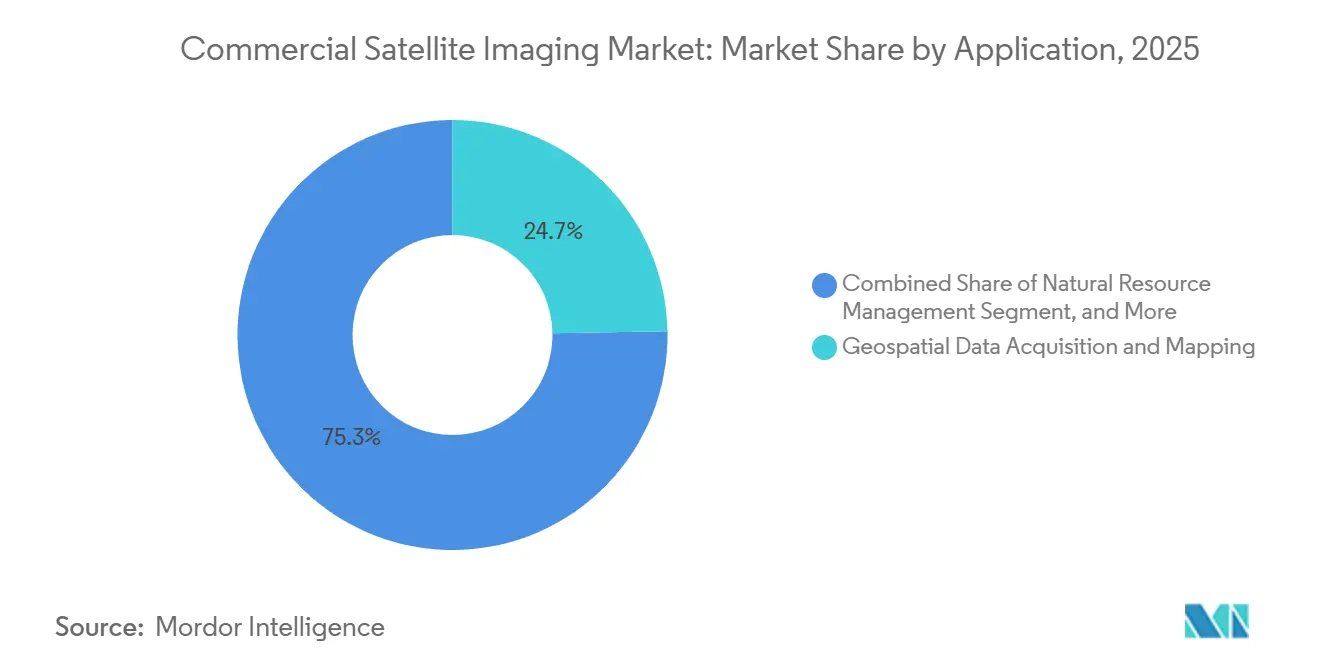

- By application, geospatial data acquisition and mapping led with 24.73% revenue share in 2025; defense and intelligence is forecast to expand at a 13.04% CAGR through 2031.

- By end-user, government agencies held 23.72% of 2025 revenue, while military and defense buyers are projected to grow at 13.11% over the same period.

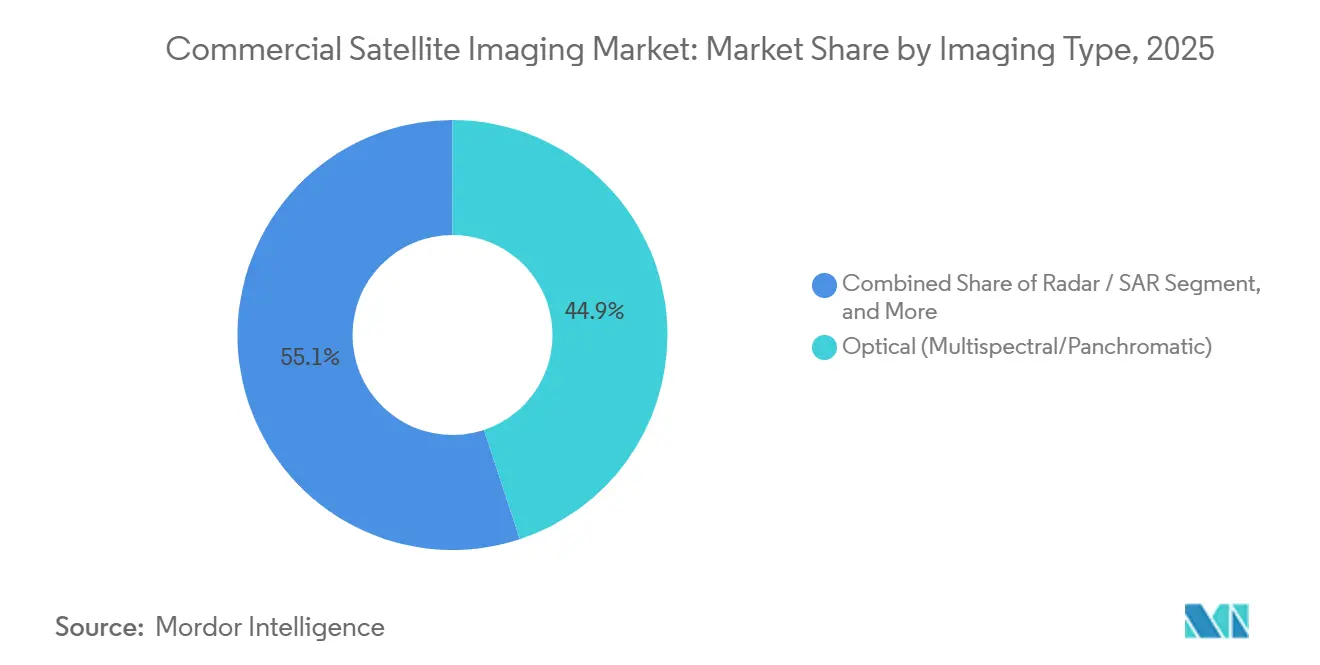

- By imaging type, optical multispectral and panchromatic systems captured 44.92% of 2025 demand; SAR platforms are projected to increase at a 13.78% CAGR.

- By spatial resolution, imagery below 0.3 meters accounted for 43.72% of 2025 sales and is expected to grow at 13.84% through 2031.

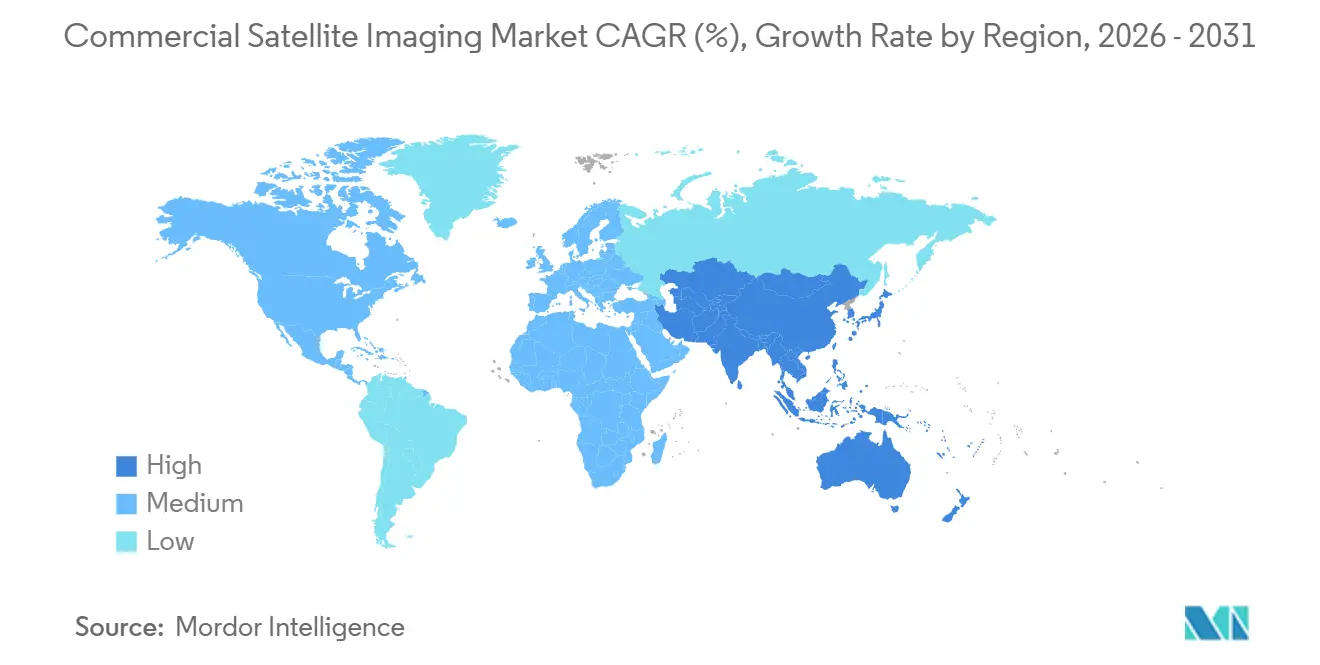

- By geography, North America commanded 38.73% of 2025 revenue, while Asia-Pacific is anticipated to register the fastest 13.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Commercial Satellite Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory methane-emissions verification via satellite (post-2025 ESG rules) | +2.8% | Global, concentrated in North America, Europe, Middle East oil and gas basins | Medium term (2-4 years) |

| AI tip-and-cue tasking driving sub-hour revisit economics | +2.3% | Global, early adoption in United States, Europe, Asia-Pacific defense sectors | Short term (≤ 2 years) |

| Proliferation of SAR micro-constellations enabling all-weather revisit | +2.1% | Global, highest demand in Northern Europe, Canada, Southeast Asia monsoon regions | Medium term (2-4 years) |

| Big-data and imagery-analytics adoption across industries | +1.7% | Global, led by North America and Europe, expanding in Asia-Pacific | Long term (≥ 4 years) |

| Rising smart-city initiatives fueling geospatial demand | +1.5% | Asia-Pacific core, spillover to Middle East and South America | Medium term (2-4 years) |

| Increasing requirement for efficient monitoring of vast land areas | +1.3% | Global, particularly South America, Africa, Australia for agriculture and resource management | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Methane-Emissions Verification Via Satellite

Regulatory mandates have transformed satellite imaging from an optional sustainability measure into a compliance necessity. The United States Environmental Protection Agency Super Emitter Program obliges oil and gas operators to respond within five days to third-party satellite alerts that detect discharges above 100 kilograms per hour, redirecting spend from voluntary offsets to contracted satellite services.[1]United States Environmental Protection Agency, “EPA Finalizes Rule on Super Emitter Response Program to Cut Methane Emissions,” epa.gov The European Union Methane Regulation introduced quarterly reporting duties that underpin multi-year subscriptions for dedicated methane-detection constellations.[2]European Union, “Regulation on Methane Emissions Reduction in the Energy Sector,” eur-lex.europa.eu GHGSat operates 17 satellites focused on shortwave-infrared sensing, reducing revisit over major basins to three days. The International Energy Agency projects satellite-verified super-emitter events will halve by 2028, implying sustained demand for high-cadence thermal imagery. Operators in the Permian Basin and North Sea now allocate annual budgets of USD 200-300 million for third-party verification, securing recurring revenue and insulating suppliers from commodity imagery price swings.

AI Tip-and-Cue Tasking Driving Sub-Hour Revisit Economics

Artificial-intelligence tasking shortens the interval between event detection and high-resolution capture, creating near-real-time intelligence value. NASA’s ConstellAI project demonstrated autonomous wildfire monitoring that cues higher-resolution satellites within 30 minutes, cutting latency by 80%.[3]NASA Jet Propulsion Laboratory, “ConstellAI Project Demonstrates Autonomous Satellite Coordination,” jpl.nasa.gov Planet Labs integrates Dove cubesats with SkySat assets to deliver sub-meter imagery inside one hour, a premium service tier priced 40% above daily revisit. United States Space Force contracts illustrate military appetite for AI-driven tasking that supports dynamic targeting. The economic upside arises from fewer unnecessary collects, lower downlink costs, and faster actionable insights, a combination that can cut acquisition cost per intelligence event by roughly 60%. Insurance underwriters, emergency-response agencies, and logistics firms are beginning to replicate defense-grade workflows, signaling broader commercial adoption.

Proliferation of SAR Micro-Constellations Enabling All-Weather Revisit

SAR technology overcomes cloud and illumination limits, enabling persistent coverage in high-latitude or monsoon regions. ICEYE’s 62-satellite fleet images any point every four hours, supporting Arctic monitoring and maritime surveillance. Capella Space operates a 14-satellite network that provides 50-centimeter-resolution data to United States federal agencies in contested theaters. Umbra Lab has achieved 25-centimeter resolution, offering optical-class detail through adverse conditions. Northern European governments integrate SAR feeds into Arctic infrastructure dashboards where optical systems deliver usable imagery less than one-third of the time. Falling launch prices and on-orbit compression have improved SAR unit economics, pushing optical-centric providers toward joint ventures or sensor diversification.

Big-Data and Imagery-Analytics Adoption Across Industries

Value creation is shifting from pixels to analytics-as-a-service. United States National Spatial Data Infrastructure policy requires agencies to procure analysis-ready geospatial products rather than raw scenes, elevating cloud-native providers. NOAA mandates that climate datasets be compatible with Amazon Web Services and Microsoft Azure, spurring investment in automated, scalable processing pipelines. Energy Department initiatives prioritize geospatial analytics for renewable-site planning, driving demand for fused multi-spectral and terrain intelligence. Commercial agriculture is following suit; for example, South American cooperatives purchase crop-stress indices at three-to-five-times the price of equivalent raw imagery. The analytics premium rewards providers with machine-learning pipelines and cross-domain data partnerships, yet raises capital barriers for smaller operators that cannot sustain cloud and talent investment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-intensive constellation deployment and launch costs | -1.9% | Global, acute for venture-backed startups in North America and Europe | Short term (≤ 2 years) |

| Data-privacy regulations slowing commercial licensing | -1.4% | Europe (GDPR), United States (NDAA), China (data-sovereignty laws) | Medium term (2-4 years) |

| High-resolution imagery available from alternative airborne platforms | -0.9% | Regional, concentrated in North America and Europe where drone regulations permit commercial operations | Medium term (2-4 years) |

| Orbital-congestion and spectrum-management bottlenecks | -0.7% | Global, most acute in low Earth orbit bands below 600 kilometers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Constellation Deployment and Launch Costs

Satellite manufacturing, launch, and ground infrastructure consume USD 100-500 million before first revenue, burdening balance sheets. Satellogic disclosed an additional USD 400 million in funding requirements to achieve its 300-satellite vision following a USD 25 million Series D round. BlackSky’s 2024 net loss of USD 48 million, despite top-line growth, illustrates depreciation drag under rapid expansion. Launch remains a gating cost even as SpaceX rideshare pricing approaches USD 1 million per 200 kilograms, implying USD 50 million in lift fees for a 100-satellite network. Insurance premiums add another 10-15%, and on-orbit anomalies can erase years of investment. Venture funding for space technology fell 35% in 2024, forcing operators to prioritize cash preservation and strategic partnerships.

Data-Privacy Regulations Slowing Commercial Licensing

Legislative constraints are elongating sales cycles and complicating cross-border data flows. United States National Defense Authorization Act Section 1260H bars federal agencies from sourcing imagery from vendors with significant Chinese, Russian, North Korean, or Iranian ownership, excluding constellations such as Jilin-1 from western government tenders. The European Union General Data Protection Regulation (Article 6) compels providers to implement automated face- and license-plate obfuscation, thereby inflating processing costs by up to 30%. China’s Data Security Law forces localization of raw geospatial data, delaying foreign licensing by more than a year in some cases. Federal Communications Commission licensing backlogs reached 18 months in 2024, compressing the revenue runway for venture-backed entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Diversifying Intelligence Spending Outpaces Mapping Demand

Defense and intelligence spending is projected to expand at a 13.04% CAGR, reflecting a strategic pivot toward commercial subscriptions that furnish higher revisit rates at lower cost compared with bespoke government satellites. Geospatial data acquisition and mapping, which secured 24.73% of 2025 revenue, remains the largest slice of the commercial satellite imaging market, yet its growth is moderating as global basemap coverage approaches saturation. Surveillance and security contracts across Asia and the Middle East are scaling, favoring SAR and tip-and-cue workflows that deliver actionable intelligence during night or adverse weather. Disaster-relief agencies increasingly integrate ultra-high-resolution captures with drone footage to expedite damage assessments, aligning civil-protection budgets with military-grade imaging standards.

The defense buyer community views commercial feeds as both gap-filler and disrupter, reallocating classified budgets to obtain responsive tasking without lifecycle ownership risk. Intelligence analysts now consume multi-sensor mosaics comprising optical, SAR, and hyperspectral layers stitched in cloud platforms, an evolution that elevates analytics value over raw pixels. Geospatial startups partner with integrators to deliver domain-specific dashboards for border security, maritime domain awareness, and illicit-activity detection. Meanwhile, mapping agencies migrate from periodic nationwide refresh cycles to continuous update models, employing automated change-detection algorithms that flag infrastructure growth, land-use shifts, and environmental compliance violations. These workflows ensure that the commercial satellite imaging market remains integral to governmental modernization even as free public-sector datasets proliferate.

By End-User: Military Outlays Lead, Civilian Buyers Widen Use-Case Portfolio

Military and defense entities are forecast to record a 13.11% CAGR, reinforcing their premium-priced weighting within the commercial satellite imaging market. Government civil agencies, holding 23.72% of revenue in 2025, maintain demand for environmental monitoring, cadastral updates, and disaster response, but face budget scrutiny that pressures per-scene pricing. Energy companies have emerged as growth accelerants, purchasing methane-detection and infrastructure-integrity subscriptions that convert compliance pain points into predictable operating expenses. Logistics operators deploy daily imagery for route-optimization and port-congestion forecasting, using AI-derived vessel counts and traffic heat maps. Forestry and agriculture cooperatives in South America buy normalized-difference vegetation index dashboards priced on acreage rather than pixels, creating volume-based but lower-margin revenue streams.

The construction and telecom sectors exploit frequent, medium-resolution imagery for site selection and network coverage planning, particularly in Asia-Pacific smart-city projects. Insurance underwriters embrace edge-processed damage assessments that accelerate claims resolution and reduce fraud. Defense prime contractors integrate commercial feeds into command-and-control software, reinforcing demand for assured-access contracts that insulate providers from commodity cycles. Non-governmental organizations leverage open-source analytics to monitor humanitarian corridors and conflict-zone violations, although these engagements generate limited revenue. Overall, diversification lowers concentration risk while intensifying competition for enterprise accounts, compelling providers to balance high-margin defense deals with scalable civilian volumes.

By Imaging Type: SAR Acceleration Challenges Optical Supremacy

Optical multispectral and panchromatic systems retained 44.92% revenue share in 2025, underscoring their centrality for color-faithful, high-resolution tasks. The commercial satellite imaging market share held by radar and SAR platforms is, however, expanding quickly as customers recognize their all-weather advantage and relatively low incidence of unusable scenes. SAR’s 13.78% projected CAGR reflects fleet expansions by ICEYE, Capella Space, and Umbra Lab, each combining short revisit with improving resolution. Hyperspectral sensors, although nascent, are attracting capital for mineral exploration, crop nutrient analysis, and atmospheric-pollution detection, use cases that optical and SAR cannot unlock. Thermal constellations fill a growing niche in methane leak detection and wildfire early warning, leveraging infrared physics that complement visible and radar modalities.

Platform economics increasingly depend on fusion; buyers seek sensor-agnostic outputs that integrate optical clarity, radar persistence, and spectral depth. This convergence drives alliance formation, as optical incumbents license SAR data, and SAR entrants partner for color layers. Edge computing further differentiates imaging types such as SAR providers compress raw phase history on-orbit, slashing downlink volume, while optical operators run onboard cloud-masking to deliver analysis-ready scenes. The interplay among modalities elevates switching costs and cements multi-sensor procurement as the default architecture for enterprise and government programs.

By Spatial Resolution: Ultra-High Clarity Commands Premium Pricing

Ultra-high-resolution captures below 0.3 meters, which accounted for 43.72% of 2025 sales, are forecast to grow at 13.84% through 2031, reinforcing their critical role in defense reconnaissance, critical-infrastructure surveillance, and insurance claims validation. Maxar’s WorldView Legion and Airbus’s Pléiades Neo constellations furnish 30-centimeter scenes with daily or twice-daily revisit, setting performance benchmarks for peer providers. High-resolution imagery between 0.3–1 meter remains pivotal for urban planning, right-of-way monitoring, and logistics, balancing cost and detail. Medium-resolution data in the 1–5 meter range dominates agriculture and forestry analytics, delivering field-level insights at cost points acceptable to price-sensitive sectors. Low-resolution scenes above 5 meters continue to lose relevance as Sentinel-2 and Landsat Next raise the free-data performance floor.

Price-performance dynamics increasingly hinge on revisit rather than resolution alone. Defense actors pay premiums for 30-centimeter data refreshed multiple times per day, whereas agribusiness prefers 10-meter imagery every five days if bundled with seasonality models. Providers responding to this spectrum tailor tasking queues, allocating optical apertures to defense windows and dedicating medium-resolution fleets to broad-acre demands. The commercial satellite imaging market thus segments not only by spatial clarity but also by temporal cadence and analytical context.

Geography Analysis

North America captured 38.73% of 2025 revenue, anchored by United States government procurement frameworks that guarantee multi-year volume commitments. The National Geospatial-Intelligence Agency’s Commercial GEOINT Strategy diversified suppliers beyond legacy monopolies, channeling funds toward BlackSky, Planet, and Capella feeds. Canada employs SAR imagery for Arctic sovereignty patrols, leveraging ICEYE and MDA services to complement limited icebreaker fleets. Mexico’s metropolitan governments integrate medium-resolution optical scenes into heat-island mitigation programs, signaling spillover demand across the continent. Regulatory clarity under NOAA remote-sensing and Federal Communications Commission licensing has encouraged venture investment, although International Traffic in Arms Regulations still curb high-resolution exports.

Asia-Pacific is projected to grow at a 13.67% CAGR, the fastest among regions. India’s Bhuvan-NICES 2.0 portal combines domestic and commercial data for urban-planning and disaster-relief dashboards. China’s Jilin-1 constellation of 108 satellites supplies sub-meter coverage across Belt and Road corridors, challenging western vendors in Southeast Asian tenders. Japan’s ALOS-4 SAR platform supports national disaster countermeasures and adjacent commercial services. Smart-city network pilots across Indonesia, Thailand, and Vietnam employ daily imagery for flood-risk mitigation, urban-transport modeling, and environmental compliance, translating infrastructural expansion into enduring imaging demand. Currency stability and digital-government mandates further underpin spending momentum.

European demand benefits from the Copernicus open-data backbone and Common Security and Defence Policy procurements. Germany’s Cartography and Geodesy agency complements Sentinel-1 with commercial SAR as flood events intensify. United Kingdom defense procurement favors regional providers to ensure sovereignty following data-localization debates. France’s CNES co-invests in hyperspectral ventures to support agricultural competitiveness. Elsewhere, Brazil and Argentina leverage vegetation-index analytics for soy and corn production despite macroeconomic volatility. Middle East and Africa growth centers on Saudi Arabia and the United Arab Emirates, where space-agency initiatives channel oil-derived capital into domestic imaging capability.

Competitive Landscape

The commercial satellite imaging market exhibits moderate concentration, as the top five players accounted for a substantial portion of 2025 revenue, while more than 60 operators fought for the remainder. Vertically integrated incumbents such as Maxar and Airbus defend their share with deep-queue government contracts and proprietary ground networks. Micro-constellation entrants, Planet, BlackSky, ICEYE, Capella, and Umbra, gain ground by offering higher revisit and usage-based pricing that attract agencies seeking agility. Analytics-first firms like Orbital Insight and SpaceKnow differentiate through machine-learning toolkits that consume imagery from multiple providers, monetizing insights rather than pixels.

Innovation cycles now focus on sensor fusion, on-orbit processing, and automated licensing compliance. Planet’s edge-compute modules cut data volume by 80%, supporting sub-hour delivery of change-detection alerts. ICEYE’s radar beams leverage cloud-based apertures to sharpen resolution without increasing satellite mass, sustaining daily revisit economics. Pixxel’s 150-band hyperspectral cubesats attract mining and agricultural customers whose requirements exceed the capabilities of broadband optical and SAR systems. GHGSat exploits regulatory tailwinds, locking in multi-year subscriptions for methane monitoring under new environmental rules.

Regulation is an emerging moat. Western ownership requirements under United States legislation and European data-privacy rules favor operators with transparent capital structures and automated anonymization pipelines. Chinese, Russian, and Iranian affiliated platforms find themselves restricted from lucrative government procurements, ceding share to compliant western constellations. Margin pressure persists, however, as commodity price erosion in raw imagery outpaces cost declines in launch and manufacturing, compelling providers to upsell analytics, sell capacity wholesale, or specialize in niche spectral bands.

Commercial Satellite Imaging Industry Leaders

Planet Labs PBC

BlackSky Technology Inc.

Maxar Technologies Inc.

Airbus Defence and Space SAS

L3Harris Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: ICEYE secured a multi-year contract with the European Maritime Safety Agency worth EUR 18 million (USD 19 million) to supply SAR imagery for oil-spill detection and illegal-fishing enforcement.

- November 2025: Satellogic partnered with Microsoft Azure to cloud-host its Earth-observation archive, enabling customers to access imagery and analytics without large downloads.

- October 2025: BlackSky reported USD 26 million in Q3 revenue, a 32% year-over-year increase, attributing growth to AI-driven processing efficiencies.

- September 2025: Airbus Defence and Space completed the Pléiades Neo constellation, delivering 30-centimeter imagery with twice-daily revisit for European government clients.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the commercial satellite imaging market as the global revenue that arises when earth-observation imagery captured by privately operated satellites is licensed to civilian, government, or defense clients for applications such as mapping, resource monitoring, and security analytics. Coverage spans optical, radar, hyperspectral, and thermal payloads across very-high to low spatial resolutions and every orbit class.

Scope Exclusion: Military satellites that are launched, owned, and used exclusively for in-house defense missions lie outside our scope.

Segmentation Overview

- By Application

- Geospatial Data Acquisition and Mapping

- Natural Resource Management

- Surveillance and Security

- Conservation and Research

- Construction and Development

- Disaster Management

- Defense and Intelligence

- By End-User

- Government

- Construction

- Transportation and Logistics

- Military and Defense

- Energy

- Forestry and Agriculture

- Other End-Users

- By Imaging Type

- Optical (Multispectral / Panchromatic)

- Radar / SAR

- Hyperspectral

- Thermal

- By Spatial Resolution

- Below 0.3 m (Ultra-High)

- 0.3 m – 1 m (High)

- 1 m – 5 m (Medium)

- Above 5 m (Low)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of South Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed satellite operators, downstream analytics firms, defense procurement officials, and geospatial consultants across North America, Europe, and Asia-Pacific. The discussions validated usable constellation sizes, acceptable price tiers by resolution, and adoption hurdles that do not surface in public literature, thereby closing data gaps identified during desk work.

Desk Research

We began with open datasets from agencies such as NASA, ESA, the United States Geological Survey, and the National Reconnaissance Office, which outline active satellite inventories, revisit rates, and sensor capabilities. Trade associations, for example, the Global Spaceport Alliance and the Satellite Industry Association, provided annual launch counts, insurance premiums, and price trends. Customs shipment records, public filings, and investor decks of key imagery providers revealed average selling prices for archival and tasking products. To complete the picture, news archives in Dow Jones Factiva, patent snapshots from Questel, and multiyear science journals on synthetic-aperture radar adoption supplied velocity indicators for emerging payloads. These references illustrate but do not exhaust the material we reviewed.

Market-Sizing & Forecasting

A top-down construct starts with launch manifests and active satellite counts, which are then multiplied by average images captured per day and monetized through region-specific price bands. Supplier roll-ups and selected channel checks provide a bottom-up cross-check. Key variables in the model include new small-sat launches, average price per square kilometer, defense intelligence budgets, cloud-free revisit frequency, and the shift from optical to SAR. Multivariate regression combined with scenario analysis projects each driver forward, and missing bottom-up datapoints are bridged through expert-agreed penetration assumptions.

Data Validation & Update Cycle

Outputs pass through variance screening, senior-analyst peer review, and re-contact of sources when deviations exceed preset bands. Reports refresh every twelve months, with mid-cycle updates triggered by launches, mergers, or major regulatory shifts. A final sweep ensures the client receives the latest calibrated view.

Why Mordor's Commercial Satellite Imaging Baseline Commands Confidence

Published estimates often diverge because providers choose different sensor mixes, price decks, and refresh cadences, and because some fold in free imagery while others do not.

Key gap drivers include narrower definitions that drop sub-0.5 m products, static ASP assumptions that ignore falling launch costs, conservative adoption curves for SAR, and infrequent currency re-baselining.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.64 B (2025) | Mordor Intelligence | - |

| USD 3.10 B (2024) | Global Consultancy A | Excludes very-high-resolution and SAR segments; limited Asia coverage |

| USD 4.73 B (2024) | Industry Association B | Uses constant ASP and omits inflation conversion; last update eighteen months old |

| USD 4.60 B (2024) | Regional Consultancy C | Bundles non-commercial government imagery; employs 2022 exchange rates |

These contrasts show that Mordor's disciplined scope selection, driver-based modeling, and yearly refresh cycle deliver a balanced and repeatable baseline that executives can trust for strategic planning.

Key Questions Answered in the Report

What is the current value of the commercial satellite imaging market?

The commercial satellite imaging market size was USD 7.49 billion in 2026 and is on course to reach USD 13.62 billion by 2031.

Which application segment is expanding the fastest?

Defense and intelligence is projected to grow at a 13.04% CAGR, outpacing all other application categories through 2031.

Why are SAR satellites gaining share against optical systems?

SAR delivers day-night, all-weather coverage, and recent micro-constellation launches have cut revisit times to hours, making it attractive for defense, maritime, and Arctic monitoring.

How do environmental regulations influence demand?

Post-2025 methane-emissions rules in the United States and Europe require satellite-verified reporting, driving recurring contracts for dedicated methane-detection constellations.

What is the main barrier to entry for new providers?

Capital-intensive constellation deployment, including manufacturing, launch, and insurance expenses that can exceed USD 100 million before first revenue, remains the primary obstacle.

Page last updated on: