Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

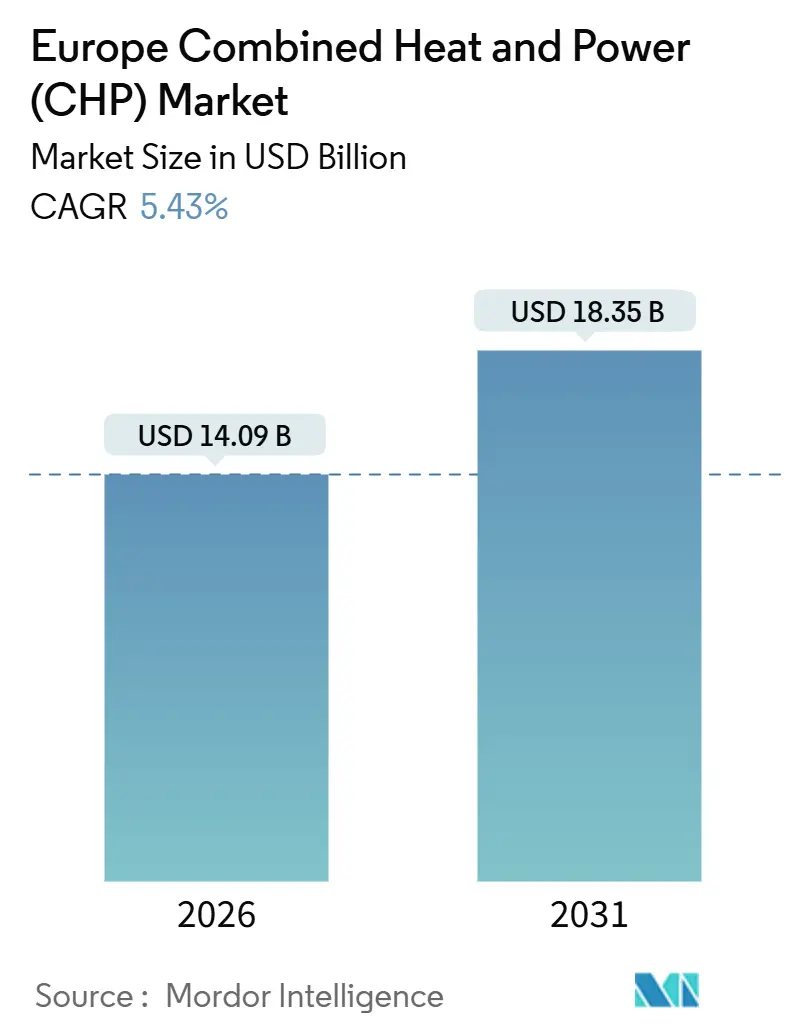

| Market Size (2026) | USD 14.09 Billion |

| Market Size (2031) | USD 18.35 Billion |

| Growth Rate (2026 - 2031) | 5.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Combined Heat And Power (CHP) Market Analysis by Mordor Intelligence

The Europe Combined Heat And Power Market size is estimated at USD 14.09 billion in 2026, and is expected to reach USD 18.35 billion by 2031, at a CAGR of 5.43% during the forecast period (2026-2031).

Natural gas retained the largest fuel footprint, yet hydrogen blends, renewable gases, and advanced biofuels are set to expand at 13.5% annually, underscoring the region’s pivot toward low-carbon cogeneration.[1]Federal Ministry for Economic Affairs and Climate Action, “BEG Funding Statistics 2025,” bmwk.de Combined-cycle configurations deliver 30.3% of installed capacity, while fuel cells, propelled by micro-CHP subsidies, are advancing fastest at 14.8% growth. Germany remains the revenue anchor, but Nordic countries are outpacing the average with 7.9% growth as district-heating policies accelerate fossil-free goals.[2]Nordic Energy Research, “Nordic District-Heating Outlook 2025,” nordicenergy.org Mounting carbon-pricing pressure, negative wholesale power prices, and electrification incentives squeeze legacy gas assets, yet on-site generation still appeals to energy-intensive industries seeking price stability and resilience.

Key Report Takeaways

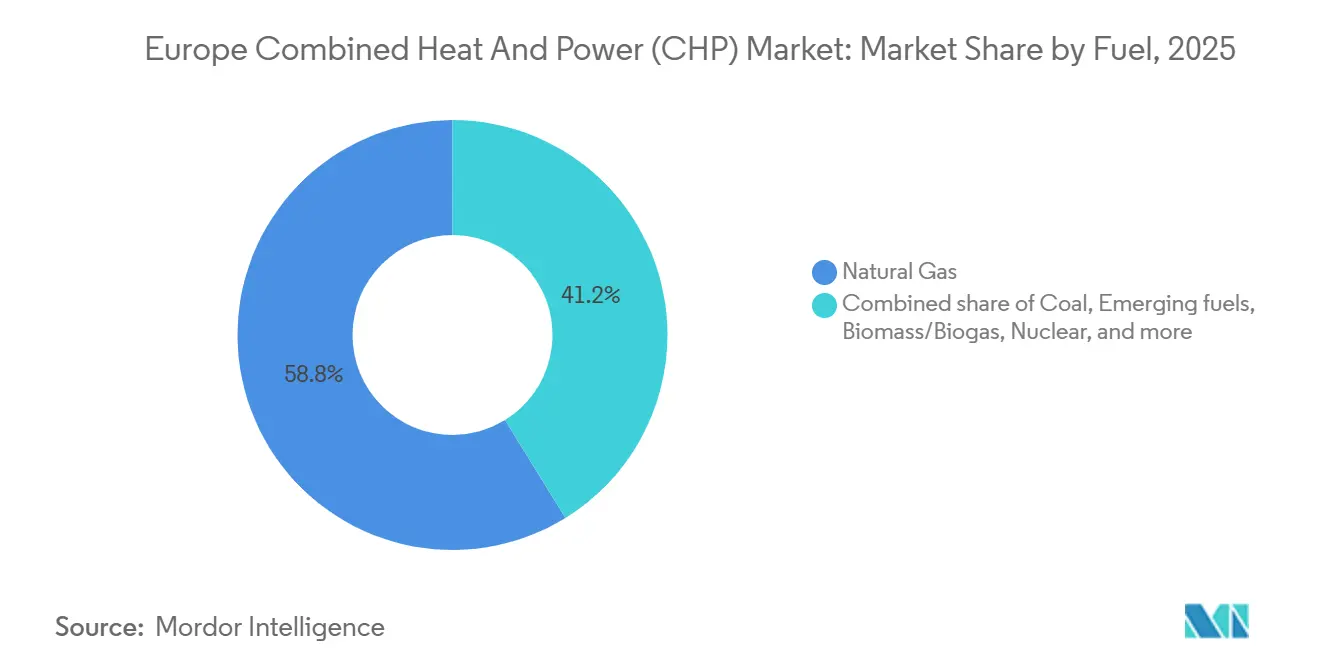

- By fuel, natural gas held 58.8% of the European combined heat and power market share in 2025; emerging fuels are forecast to grow at a 13.5% CAGR to 2031.

- By prime mover, combined-cycle units delivered 30.3% of capacity in 2025, while fuel cells recorded the fastest 14.8% CAGR through 2031.

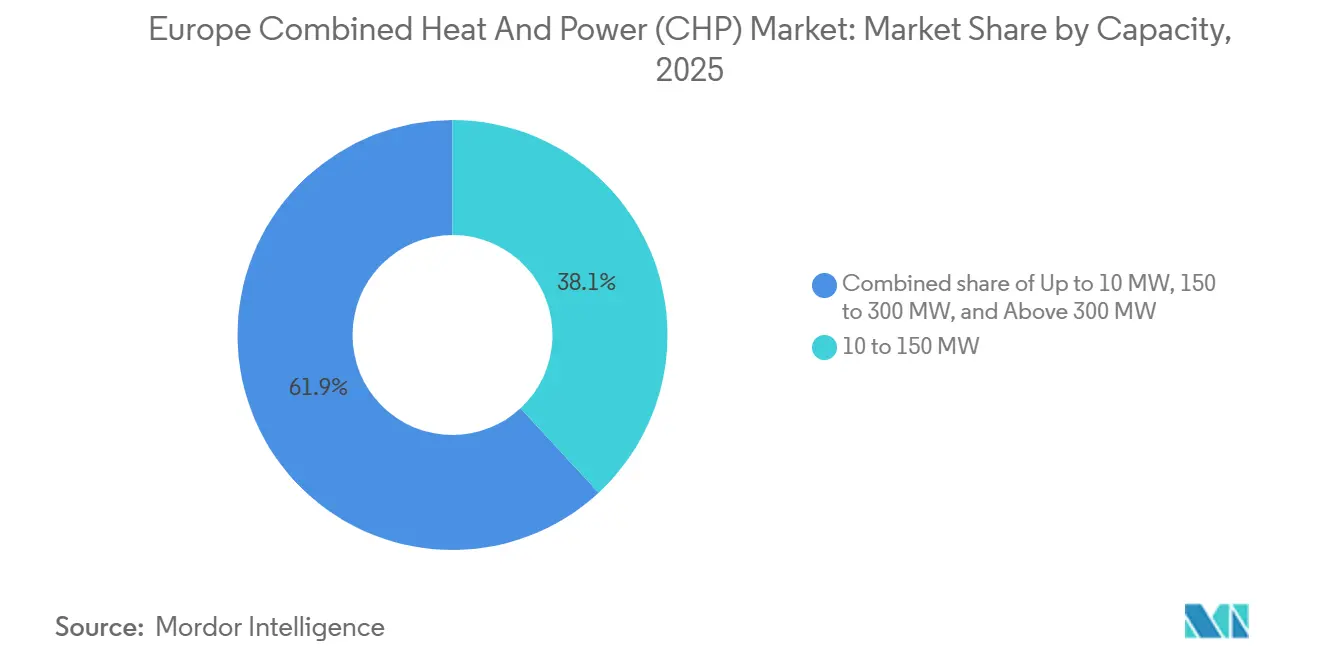

- By capacity, 10-to-150 MW systems captured 38.1% of the European combined heat and power market size in 2025; units up to 10 MW are expanding at an 8.3% CAGR through 2031.

- By end-user sector, the industrial sector commanded a 40.4% share of the European combined heat and power market size in 2025, whereas the residential micro-CHP advances at an 8.1% CAGR.

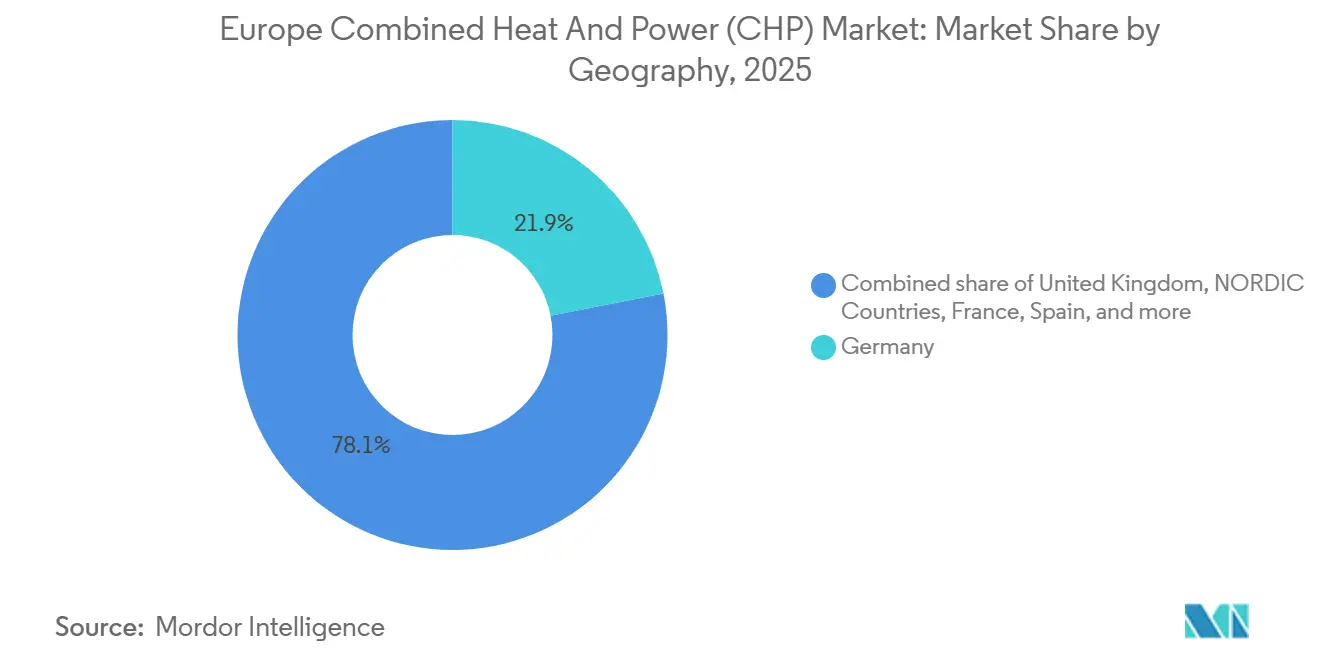

- By geography, Germany delivered 21.9% of 2025 revenue; Nordic countries are advancing at a 7.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Combined Heat And Power (CHP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Green Deal-linked energy-efficiency & CHP subsidies | 1.20% | EU-wide, strongest in Germany, Netherlands, Belgium | Medium term (2-4 years) |

| Rapid district-heating network expansions in CEE & Nordics | 1.50% | Poland, Czech Republic, Finland, Sweden, Denmark | Medium term (2-4 years) |

| Biogas/biomethane scale-up unlocking renewable-gas CHP | 0.80% | Germany, France, Italy, Netherlands | Medium term (2-4 years) |

| Hybrid CHP + high-temp heat-pump retrofits in energy-intensive industry | 0.60% | Germany, France, Nordics | Long term (≥ 4 years) |

| Price-volatility hedging via on-site generation/resilience | 0.90% | Germany, Italy, Spain, CEE manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU Green Deal-Linked Energy-Efficiency & CHP Subsidies

The REPowerEU package channels EUR 300 billion through 2027, with roughly 15% reserved for high-efficiency cogeneration and district-heating upgrades, translating into a multi-GW near-term tender pipeline.[3]European Commission, “Cogeneration and District Heating,” energy.europa.eu Germany’s BEG program reimburses up to 40% of eligible costs for biogas or hydrogen-ready units, lifting sub-5 MW reciprocating-engine orders by 22% year-on-year in 2025. The Netherlands’ SDE++ scheme guarantees a 15-year tariff of EUR 95 per MWh for biomethane-fueled CHP, stimulating new dairy-sector capacity RVO.NL. Belgium’s Flanders raised its cogeneration certificate floor to EUR 28, boosting micro-CHP viability in pharmaceutical campuses. Article 14 of the Energy Efficiency Directive mandates waste-heat cost-benefit studies, sending municipal budgets toward CHP retrofits in chemicals, pulp and paper, and food processing.

Renewable-Gas Incentives Fueling CHP Conversions

Multiple member states deploy generous feed-in tariffs, investment grants, and carbon-intensity bonuses that directly subsidize biogas, biomethane, and hydrogen-ready cogeneration units. Germany’s BEG program reimburses up to 40% of capital outlays for engines firing renewable gases, while the Netherlands’ SDE++ scheme locks in a 15-year premium of EUR 95 per MWh for biomethane-based CHP.[4]Federal Ministry for Economic Affairs and Climate Action, “BEG Funding Statistics 2025,” bmwk.de These incentives shorten payback to fewer than five years for sub-5 MW plants and underpin a double-digit order surge among reciprocating-engine manufacturers. Utilities also pivot legacy gas turbines toward hydrogen blends to retain capacity-market revenues and avoid rising ETS costs. The policy certainty encourages long-term offtake contracts between anaerobic-digestion developers and industrial heat users, anchoring fuel supply and de-risking financing. As a result, renewable gases are positioned to claim a growing share of incremental CHP additions through 2031.

District-Heating Decarbonization Mandates in Nordics and CEE

Finland, Sweden, and Denmark legislate fossil-free district heat by 2030, while Poland and the Czech Republic channel EU cohesion funds into modern networks that prioritize biomass, waste heat, and hydrogen-ready CHP. Municipal utilities respond by retiring coal boilers and installing medium-sized combined-cycle or reciprocating-engine plants that co-generate electricity and hot water with efficiency above 85%. Tender documents now specify hydrogen co-firing thresholds and lifecycle-emissions ceilings, steering OEMs toward low-carbon hardware. The build-out creates steady demand for 10-to-150 MW packages, heat-pump boosters, and seasonal thermal-storage tanks. Because district-heating customers pay regulated tariffs, project cash flows remain resilient, making this mandate a reliable growth catalyst over the forecast window.

Industrial Resilience and Energy-Price Volatility Hedge

Spot electricity prices swung by more than EUR 200 per MWh during several 2025 cold-weather episodes, exposing manufacturers to sharp operating-cost spikes. On-site CHP enables factories to lock in predictable heat and power costs while safeguarding production from grid outages that doubled year on year in Germany. Automotive, chemicals, and ceramics plants increasingly integrate 5-to-50 MW engines with battery storage and digital controls to maximize self-consumption and capture ancillary-service revenue. Lenders view resilience as a bankable benefit, reflected in green-bond issuances that earmark proceeds for cogeneration. The driver gains extra momentum in Central and Eastern Europe, where transmission bottlenecks and aging substations heighten blackout risk and strengthen the CHP value proposition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fossil-gas phase-down & carbon-pricing squeeze | -0.90% | EU-wide, acute in Germany, UK, France | Short term (≤ 2 years) |

| High CAPEX vs heat pumps & electrification alternatives | -0.70% | Western Europe | Medium term (2-4 years) |

| Large-scale heat-pump substitution of low-/mid-temp heat | -0.60% | Germany, Nordics, Netherlands | Medium term (2-4 years) |

| Shrinking run-hours from negative-price events | -0.40% | Germany, Denmark, Spain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fossil-Gas Phase-Down & Carbon-Pricing Squeeze

EU ETS prices averaged EUR 82 per tCO₂ in 2025, adding EUR 35 per MWh to variable costs for gas-fired CHP and tightening spark spreads. Germany finalized its coal exit without parallel support for gas assets, leaving operators exposed to stranded-asset risk. The UK stacked its Carbon Price Support atop ETS levies, driving combined charges above GBP 40 per tCO₂ and eroding merchant economics. France’s national low-carbon strategy aims to cut industrial gas use by 40% by 2030, pushing glass and steel producers toward electrified heat. Spain’s draft climate plan phases out CHP capacity payments by 2027, redirecting funds to green hydrogen.

Capital-Cost Competitiveness of High-Temperature Heat Pumps

Turnkey industrial heat pumps delivering 120 °C steam now cost roughly EUR 800 per kW-thermal, versus about EUR 1,200 per kW-electric for comparable gas-engine CHP, narrowing the economic gap even before factoring carbon charges. Falling compressor prices, cheap renewable electricity contracts, and preferential financing terms from programs such as Germany’s KfW Energy-Efficiency Loan compress simple payback to five years for many process-heat users. Food, beverage, and paper producers demonstrate willingness to retire aging CHP in favor of all-electric solutions that eliminate Scope 1 emissions and compliance obligations under the EU ETS. As more suppliers scale 150 °C ammonia and CO₂ cycles, capital costs are projected to dip further, reducing the pool of applications where fossil-fired cogeneration remains economically superior.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel: Natural Gas Still Leads, Yet Renewable Molecules Surge

Natural gas retained 58.8% of the European combined heat and power market share in 2025, anchored in legacy turbine fleets and district-heating loops. Biomass and biogas together supplied 18% of output, thanks to abundant forestry residues in Scandinavia and agricultural waste in Central Europe. Coal’s 9% footprint is shrinking under EU Taxonomy retirement deadlines, and diesel plus niche liquids remained below 4% without material growth levers. Emerging fuels, hydrogen blends, biomethane, and advanced biofuels expanded at a brisk 13.5% CAGR and are set to erode natural-gas dominance through 2031. These dynamics indicate a diversifying feedstock mix that will recalibrate capital allocation across the European combined heat and power market.

Policy incentives underpin the pivot. Germany’s EUR 9 billion National Hydrogen Strategy, Italy’s biomethane mandates, and the Netherlands’ 15-year SDE++ tariff directly subsidize fuel switching. Operators retrofit existing engines for up to 30% hydrogen by volume, while new reciprocating packages arrive factory-certified for 100% renewable gas. As a result, the Europe combined heat and power market size attached to emerging fuels is projected to outpace every other category to 2031, widening technology choice for municipal utilities and industrial hosts.

By Prime Mover: Fuel Cells Accelerate as Combined-Cycle Plants Hold Scale

Combined-cycle units delivered 30.3% of installed capacity in 2025, safeguarding heat supply for large district-heating operators and petrochemical complexes. Reciprocating engines followed at 26%, dominating the sub-10 MW class that addresses hospitals, data centers, and mid-sized manufacturers. Fuel cells, while still small in absolute numbers, posted a 14.8% CAGR on the back of residential micro-CHP subsidies and utility-scale orders that value near-zero criteria emissions.

OEM roadmaps now emphasize hydrogen-ready certificates, load-following capability, and hybridization with batteries, positioning prime movers for capacity-market and ancillary-service revenue. Subsidy programs such as Germany’s KfW 433 grant up to EUR 11,200 per fuel-cell installation, while the UK’s capacity market recognizes solid-oxide stacks as a reliable reserve. These mechanisms channel a rising share of the European combined heat and power market toward fuel-cell and advanced engine solutions, even as combined-cycle plants preserve scale advantages in cities with high heat demand.

By Capacity: Distributed Systems Climb, Utility-Scale Plateaus

Installations rated 10-to-150 MW represented 38.1% of the European combined heat and power market size in 2025, serving district-heating grids, universities, and industrial parks. Systems below 10 MW are growing at 8.3% CAGR, buoyed by modular reciprocating engines, microturbines, and fuel cells that require modest permitting and interconnection. Facilities above 150 MW accounted for a combined 30%, but new projects face grid-connection queues and tougher emissions caps.

Smaller units benefit from feed-in premiums, net-metering, and fast-track siting rules, while their ability to island enhances resilience. As capital costs decline and digital controls simplify fleet orchestration, distributed assets are positioned to capture incremental demand across the European combined heat and power market, especially in regions with volatile power prices and aging transmission.

By End-User Sector: Industry Dominates, Residential Micro-CHP Gains Traction

Industrial customers held 40.4% of the installed base in 2025, leveraging simultaneous steam and power to cut energy expense and curb carbon exposure. Utilities followed at 28%, providing district-heating services in Germany, the Nordics, and Central Europe. Commercial facilities, hospitals, hotels, and campuses accounted for 24%, while residential applications, though only 7.6% today, are expanding at 8.1% CAGR on generous micro-CHP rebates.

Fuel-cell stacks of 1 kW to 5 kW size now arrive pre-configured for hydrogen blends, suiting single-family homes in high heating-degree-day regions. Meanwhile, food, chemicals, and pulp-and-paper plants integrate hybrid heat pump-plus-engine packages to reach efficiency above 90%. Together, these shifts reinforce the industrial core even as residential uptake broadens the addressable base for the European combined heat and power market.

Geography Analysis

Germany generated 21.9% of 2025 revenue, propelled by the Federal Funding for Efficient Buildings program that disbursed EUR 1.2 billion in CHP grants. Dense district-heating networks, hydrogen-ready retrofit pilots, and strong industrial demand anchor growth despite rising carbon costs. The United Kingdom ranked second at 14% share, although high Carbon Price Support levies trim gas-engine run-hours and suppress merchant margins.

Nordic countries - Finland, Sweden, Denmark, and Norway - are advancing at a 7.9% CAGR, stimulated by mandates for fossil-free heat by 2030 and ample biomass feedstock. France and Italy each sit near 12% and 11% respectively: France leans on Engie-Veolia biomass projects, while Italy benefits from biomethane incentives tied to its Decreto Biometano policy. Spain’s 9% slice is concentrated in pulp and ceramics clusters but faces subsidy withdrawal for gas CHP post-2027.

Central and Eastern Europe collectively holds 14%, with Poland and the Czech Republic channeling EU cohesion funds into modern district-heating loops, creating a 5 GW near-term project pipeline. Russia accounts for 8%, almost entirely natural-gas and coal-fired cogeneration around major cities, yet limited policy alignment with EU climate rules constrains renewable migration. Across the bloc, recovery-fund inflows and hydrogen-backed infrastructure programs are poised to redistribute future gains, making policy execution the decisive variable for regional shares in the Europe combined heat and power market.

Regulatory Landscape

The EU Energy Efficiency Directive (recast) (EU) 2023/1791 sets the regulatory basis for high-efficiency cogeneration and requires Member States to apply cost-benefit analysis when planning new or substantially refurbished heat and cooling infrastructure. This keeps CHP eligibility tied to primary energy savings versus separate production. In March 2026, the European Commission adopted Recommendation (EU) 2026/839 with guidelines for cost-benefit methodologies to operationalize the energy-efficiency-first principle under Article 3(6) of Directive (EU) 2023/1791, adding more standardized assessment expectations for CHP, district heating, and broader heat system investments.

State-aid design and national support schemes remain central for project bankability, particularly where incentives must align with the 2022 Guidelines on State aid for climate, environmental protection and energy, alongside the Energy Efficiency Directive criteria. In January 2026, the European Commission approved a EUR 3.1 billion Spanish state aid scheme to support electricity production from new or substantially refurbished high-efficiency CHP plants, reinforcing that compliant, high-efficiency configurations can access large-scale support when structured within EU state-aid and energy-efficiency rules. Separately, the Commission adopted Recommendation (EU) 2026/537 on unlocking private investment in energy efficiency, which includes guidance supporting national financing vehicles, such as energy-efficiency funds, for use alongside CHP and district-heating modernization programs.

Competitive Landscape

The market is moderately consolidated: Siemens Energy, GE Vernova, Wärtsilä, Mitsubishi Power Europe, and INNIO together control an estimated 38% of installed capacity. Their portfolios span gas turbines, reciprocating engines, and integrated service contracts that lock in multiyear revenue. Competitive intensity is sharpening as fuel-cell pure plays, Bloom Energy, FuelCell Energy, Ballard, move from pilot to commercial scale, targeting micro-CHP and data-center resiliency niches.

Incumbents respond with hydrogen retrofit offerings and hybrid packages. Wärtsilä partnered with Hitachi Energy in 2025 to couple 10 MW biogas engines with battery storage that secures grid-forming capability. Mitsubishi Power shipped a 220 MW turbine to Poland pre-certified for 30% hydrogen, illustrating how district-heating utilities can future-proof large assets. INNIO’s Jenbacher J624 toggles between methane and pure hydrogen inside a one-minute ramp, a differentiator for ancillary-service markets.

Heat-pump specialists and renewable-gas aggregators now encroach on traditional CHP territory. Danfoss and Johnson Controls bundle 120 °C ammonia heat pumps with waste-heat recovery, challenging gas engines below 10 MW in food and beverage plants. Landwärme leases equipment and supplies biomethane under long-term contracts, lowering entry barriers for mid-cap manufacturers. Digital optimizers such as Limejump aggregate distributed units into virtual power plants, arbitraging wholesale volatility and capturing capacity payments for owners. Collectively, these moves compress margins yet expand solution breadth, reinforcing a dynamic competitive landscape across the European combined heat and power market.

Europe Combined Heat And Power (CHP) Industry Leaders

General Electric Company

Siemens AG

Engie SA

2G Energy AG

Wärtsilä Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity centers on refurbishments and new builds that qualify as high-efficiency cogeneration under Directive (EU) 2023/1791, especially where public support targets compliant CHP and heat-network upgrades. The European Commission's approval of Spain's EUR 3.1 billion scheme for electricity production from new or substantially refurbished high-efficiency CHP plants in January 2026 provides a clear template for subsidy-backed project pipelines where eligibility depends on technical and efficiency criteria rather than simple capacity additions. This supports OEMs and EPCs that can deliver hydrogen-ready, renewable-gas capable engines and turbines, and it also benefits developers that can package CHP with metering, controls, and verified primary-energy-savings documentation needed for permitting and aid compliance.

Project activity in 2026 is also pointing to white-space in biomass and hybridized district-heating solutions that combine CHP with power-to-heat and renewable inputs. In Germany, HoSt Group started construction of a 25 MW wood-waste-fired CHP plant in Osnabrueck in May 2026 to replace a coal facility, while N-Ergie began building an innovative CHP system in Nuremberg in June 2026 that incorporates renewable-heat requirements and power-to-heat integration. The direction is shifting away from standalone gas CHP toward system-level flexibility for heat networks. Large district-heating build-outs continue to create retrofit and services demand for decarbonization-ready CHP, including progress on the Dradenau CHP project in Hamburg (ENKA, first fire scheduled for May 2026, completion targeted in Q4 2026), as well as equipment supply demand such as Valmet’s biomass boiler and flue-gas handling scope at Sweden’s OErtofta CHP (installation start scheduled in 2026).

Recent Industry Developments

- June 2026: N-Ergie began construction of an innovative combined heat and power (iCHP) system in Nuremberg, Germany, designed with renewable integration requirements and power-to-heat capability. The project indicates a shift in district-heating investment toward hybrid architectures where CHP operates alongside electrified heat to manage surplus power and heat demand. It also raises the bar for controls, system integration, and compliance documentation for suppliers targeting German municipal and utility tenders.

- October 2025: Estonia and Latvia inaugurated Europe’s first cross-border district heating interconnection, enabling shared heat supply between their networks. This improves CHP utilization by allowing surplus heat to be transferred across borders and reduces reliance on fossil-based backup during demand peaks. The interconnection also provides a reference case for regional heat-market coupling, supporting additional CHP modernization and network optimization projects.

- April 2024: The EU recast Energy Efficiency Directive (EU) 2023/1791 entered into application across Member States, strengthening the framework for defining and assessing high-efficiency cogeneration through primary energy savings and mandatory cost-benefit analysis in heat and cooling planning. These requirements tighten the eligibility path for support and permitting, pushing projects toward higher-efficiency CHP and better-integrated district-heating solutions. The directive also reinforced a compliance-driven need for standardized methodologies and documentation that affects developers, utilities, and OEMs selling into public procurement.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from combined heat and power systems that produce electricity and usable heat from the same fuel input, across Europe. The sizing reflects equipment and system-level revenues linked to CHP installations serving residential, commercial, industrial, and utility users.

Scope exclusions: Standalone boilers, standalone power-only generation assets, and heat-only district heating plants are excluded when they do not operate as CHP.

Segmentation Overview

- By Fuel

- Natural Gas

- Coal

- Biomass/Biogas

- Diesel and Other Liquid Fuels

- Nuclear

- Emerging fuels

- By Prime Mover

- Combined Cycle

- Gas Turbine

- Steam Turbine

- Reciprocating Engine

- Fuel Cells

- Microturbines and Others

- By Capacity

- Up to 10 MW

- 10 to 150 MW

- 150 to 300 MW

- Above 300 MW

- By End-User Sector

- Utilities

- Commercial

- Industrial

- Residential

- By Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- NORDIC Countries

- Russia

- Rest of Europe

Data Validation & Update Cycle

Validation is done by triangulating modeled revenue against independent signals such as CHP capacity commissioning trends, district heating expansion activity, and the direction of industrial energy consumption. Large variances are flagged, investigated at the assumption level, and then re-checked with a second analyst review before sign-off.

The report is refreshed on an annual cycle, and interim updates are triggered when material events occur, such as major subsidy changes, sharp fuel-price swings, or unusually large project pipelines. Before delivery, a final pass is performed so clients receive an up-to-date view with consistent assumptions carried through the model.

Mordor Intelligence's Europe Combined Heat and Power Market Market Size Versus Other Published Estimates

Published market values for Europe CHP can vary even when the topic name looks the same, since included revenue lines, the year used for the starting point, and how price changes are handled often differ. The differences become clearer once you check whether an estimate is for equipment revenues, installed capacity value, or broader project spending.

CHP installation and construction spending is treated outside Mordor Intelligence's scope, which is one reason some published figures come out higher even for nearby years. Another common driver is how studies handle country coverage inside Europe and whether micro-CHP and fuel cell units are priced using consistent ASP progression, especially when exchange-rate timing and inflation are not aligned to the same base year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.09 B (2026) | |

| Industry Publisher A | USD 18.69 B (2025) | Uses an installation market lens that can fold in wider project and contractor revenue, and it also starts from a different base year, which shifts price and currency assumptions. |

| Industry Publisher B | USD 18.70 B (2026) | Applies a broader country list and a longer forecast window, and it appears to treat distributed generation and district heating deployments with wider inclusions, which can lift the total. |

Across the three figures, the spread is mainly explained by what each source counts as market revenue and how the starting year and pricing path are set. By keeping the model tied to measurable adoption signals like capacity additions, prime mover mix, and replacement timing, the estimate stays traceable and repeatable when assumptions get updated.

Key Questions Answered in the Report

How large is the Europe combined heat and power market today?

The Europe combined heat and power market size reached USD 14.09 billion in 2026 and is forecast to climb to USD 18.35 billion by 2031.

Which fuel will grow fastest through 2031?

Hydrogen blends, renewable gases, and advanced biofuels will expand at a 13.5% CAGR, the quickest pace among all fuels.

Why are Nordic countries outpacing the regional average?

Municipal fossil-free heat mandates and rapid district-heating build-outs lift Nordic growth to a 7.9% CAGR.

What segment leads by capacity band?

Installations rated 10-to-150 MW hold 38.1% of the Europe combined heat and power market share, driven by district-heating utilities and large industrial sites.

How is carbon pricing influencing CHP investment?

EU ETS prices above EUR 80 tCO₂ increase operating costs for unabated gas CHP, encouraging renewable-gas conversions and hybrid heat-pump retrofits.

Page last updated on: