Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

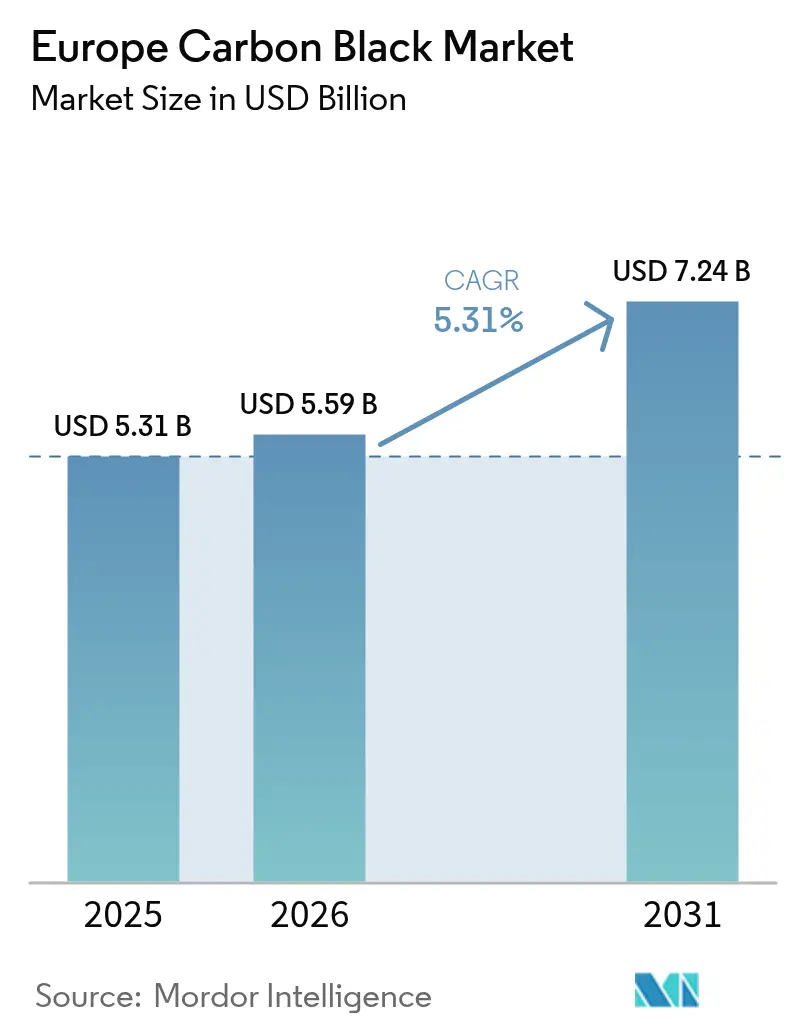

| Base Year Market Size (2025) | USD 5.31 Billion |

| Market Size (2026) | USD 5.59 Billion |

| Market Size (2031) | USD 7.24 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Carbon Black Market Analysis by Mordor Intelligence

The Europe Carbon Black Market size was valued at USD 5.31 billion in 2025 and estimated to grow from USD 5.59 billion in 2026 to reach USD 7.24 billion by 2031, at a CAGR of 5.31% during the forecast period (2026-2031). Market expansion is propelled by the rapid localization of supply that followed the July 2024 import ban on Russian material, the accelerated pivot toward electric-vehicle tires that favor low rolling resistance formulations, and stringent circular-economy regulations that mandate recycled content in new products. Tier-one tire and battery producers are deepening collaboration with regional carbon black suppliers to secure near-site deliveries, hedge feedstock volatility, and align with REACH polycyclic aromatic hydrocarbon (PAH) limits that come into force in 2025. At the same time, production costs are falling in facilities that now crack hydrogen-rich off-gas instead of traditional aromatic oils, allowing them to defend margins despite elevated energy prices. Competitive intensity has intensified as specialty-grade suppliers pursue a higher share in coatings, battery casings, and conductive plastics, while recovered carbon black innovators gain traction through partnerships with major tire OEMs.

Key Report Takeaways

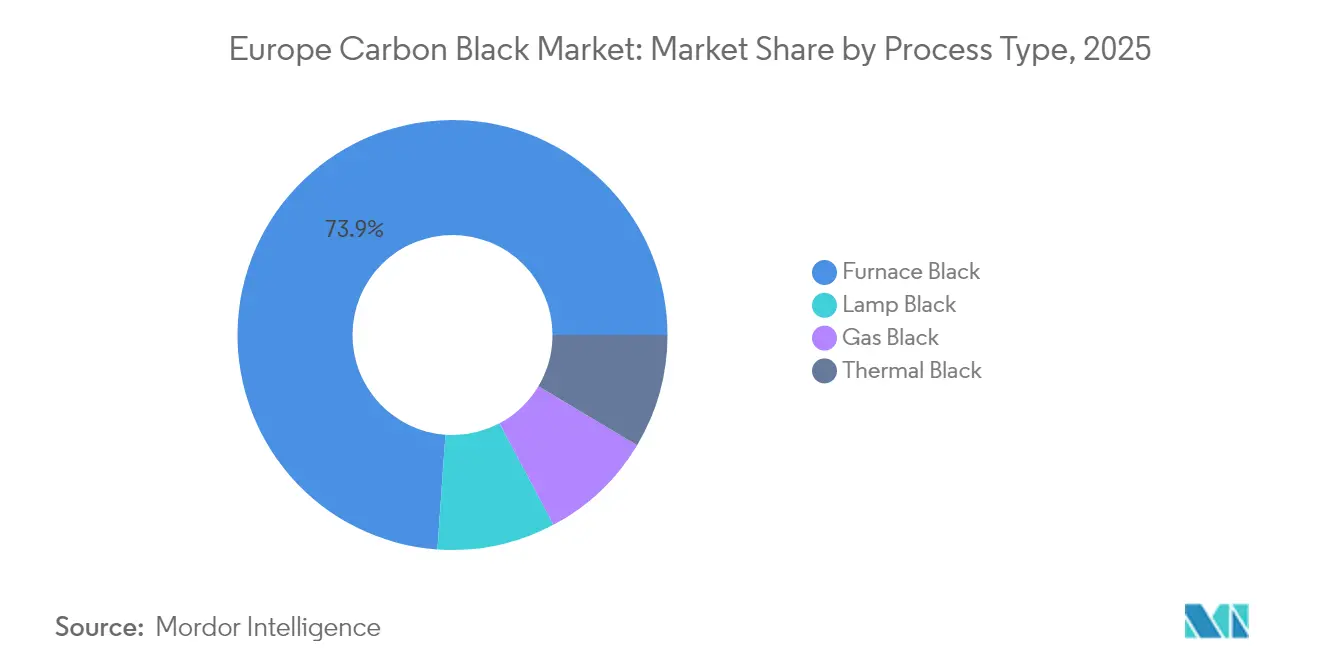

- By process type, furnace black held 73.88% of the Europe carbon black market share in 2025. Lamp black is projected to record the fastest 7.72% CAGR between 2026 and 2031.

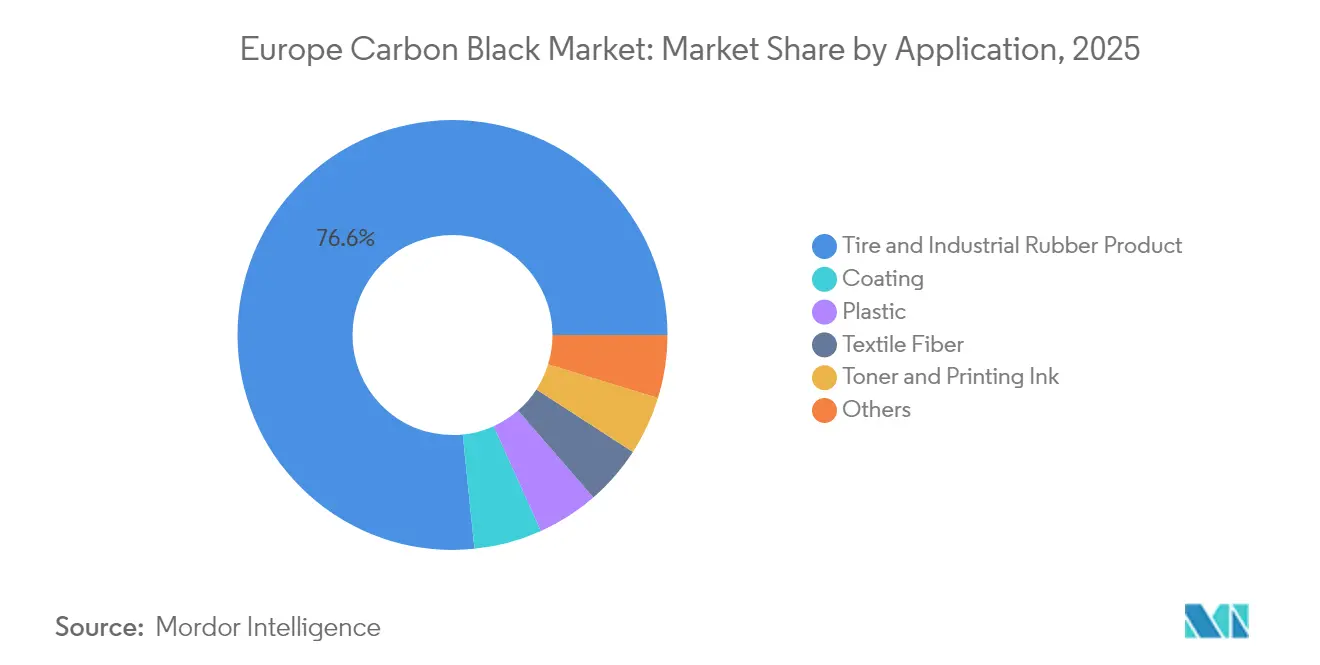

- By application, tires and industrial rubber captured 76.63% of the Europe carbon black market size in 2025. Coating applications are forecast to expand at a 6.92% CAGR to 2031.

- Germany accounted for 23.42% of regional demand in 2025, whereas the United Kingdom is set to advance at a 6.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Carbon Black Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in EV-tire demand for low-rolling-resistance blacks | +1.2% | Germany, France, United Kingdom | Medium term (2-4 years) |

| OEM shift to specialty blacks for Li-ion battery casings | +0.8% | Germany, Sweden | Long term (≥4 years) |

| Circular-economy mandates boost recovered carbon black integration | +1.1% | EU-wide | Long term (≥4 years) |

| Hydrogen-rich cracker off-gas reduces feedstock costs | +0.7% | Netherlands, Germany | Medium term (2-4 years) |

| Smart-factory retrofits enhance production yields | +0.6% | Western Europe industrial corridors | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

EV-tire demand accelerates low rolling resistance applications

Electric-vehicle adoption is rewriting tire compound specifications as OEMs emphasize energy efficiency over conventional performance criteria. Low rolling resistance tires require narrowly controlled particle size distribution and customized surface treatments that cut hysteresis losses, allowing suppliers to command 15–20% price premiums over commodity grades. Europe’s major tire makers are jointly developing bio-based and recycled carbon blacks that retain grip while trimming energy loss, and the collaboration intensity is highest in Germany and France, where EV production scales fastest. These efforts are tightening long-term offtake agreements between tire majors and regional specialty-grade producers, thus improving demand visibility across the European carbon black market.

Battery casing applications drive specialty black demand

Lithium-ion battery pack designers now specify low-ash, high-conductivity carbon blacks to ensure uniform current distribution and electromagnetic interference shielding. Imerys has commercialized grades with finely tuned specific surface areas supporting stable lithium-ion transport in cylindrical, pouch, and prismatic cells. Gigafactories in Sweden, Germany, and Poland stipulate local sourcing as part of supplier scorecards to cut embedded emissions, spurring European specialty producers to add capacity and fast-track product qualification processes.

Circular-economy regulations mandate recovered carbon black integration

EU directives on waste-tire valorization target minimum recycled content thresholds in new tires, reinforcing the technical validation delivered by the BlackCycle project that concluded in 2024[1]European Commission, “BlackCycle Project Final Report,” CORDIS.EUROPA.EU . Tier-one tire manufacturers have begun issuing multiyear supply tenders that combine virgin and recovered grades, pulling pyrolysis pioneers such as Black Bear Carbon into the mainstream. Quality standardization, particularly around particle morphology and surface chemistry, remains a work in progress, yet first-wave commercial runs have met OEM durability benchmarks, narrowing perceived risk for broader adoption across the European carbon black market.

Hydrogen-rich off-gas reduces feedstock dependencies

Switching from imported carbon black feedstock (CBFS) to cracker off-gas rich in hydrogen means producers can secure abundant local feedstocks while lowering carbon intensity. Demonstration plants in the Netherlands and Germany show carbon black unit costs drop, while flared-gas emissions fall materially. Producers integrating this route expect to reach cost parity with Asian competitors despite Europe’s higher energy prices.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green-tire silica substitution in premium segments | -0.9% | Western Europe premium markets | Medium term (2-4 years) |

| Volatile CBFS and coal-tar pitch prices | -0.4% | EU-wide | Short term (≤2 years) |

| Russia–EU conflict disrupts supply chains | -0.7% | Eastern and Central Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Silica substitution challenges premium market share

High-end passenger car tire makers are boosting silica reinforcement to satisfy fuel-efficiency labeling, trimming virgin carbon black content by up to 15% in select tread compounds. The performance gap between silica and advanced hybrid carbon black–silica systems is narrowing, pressuring commodity-grade volumes in premium portfolios. Suppliers are racing to engineer surface-modified blacks that bond efficiently with organosilane coupling agents, hoping to restore their share in these profitable niches.

Feedstock price volatility pressures margins

Coal-tar pitch availability tightened after European blast-furnace output slowed during the green-steel transition, causing more than 40% price swings from 2023 to 2025. Since European carbon black producers lock in multiyear supply contracts with tire customers, they are squeezed whenever spot CBFS costs spike, forcing greater use of hedging and diversification into bio-oils and pyrolysis oils to preserve margin stability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process Type: Furnace black dominance faces specialty pressure

Furnace black accounted for 73.88% of the Europe carbon black market share in 2025, underscoring its versatility in both reinforcement and pigment applications. Despite that dominance, lamp black’s projected 7.72% CAGR through 2031 signals that demand is fragmenting toward high-value niches where color strength and blue undertone are prized. Furnace producers are extending portfolios with low-PAH and surface-modified variants to meet REACH thresholds due in 2025 and fight specialty encroachment.

Sustained growth in coatings, batteries, and plastics encourages suppliers to allocate fresh capital toward smaller gas-black lines that deliver ultra-fine particle topography required in premium pigments. These investments look attractive because coatings command 20–30% pricing premiums over tire grades, and they insulate suppliers from cyclical swings in automotive tire replacement demand. Thermal black maintains a dependable but modest foothold, mainly in sealants and polymer modification, where its larger particle size enhances damping properties.

By Application: Tire leadership challenged by coating growth

Tires and industrial rubber products generated 76.63% of Europe carbon black market revenue in 2025. The category remains the volume anchor, yet the emergence of EV-specific tread compounds is forcing a gradual pivot toward value-added, low-rolling-resistance grades rather than bulk reinforcement. Coating formulations, by contrast, are projected to grow at 6.92% CAGR, fueled by tougher automotive UV-protection standards plus architectural moves to darker, heat-reflective façades.

Plastics hold a steady mid-single-digit growth trajectory, supported by OEM switch-outs from toners and inks to lightweight automotive components that require conductive shielding. The toner and printing ink niche is pressured by digitalization but benefits from higher-resolution specialty blacks that preserve profitability. Textile fiber demand remains small yet promising in technical fabrics where carbon black’s infrared absorptive capability aids protective clothing performance.

Geography Analysis

Germany generated 23.42% of regional demand in 2025, leveraging its integrated automotive and chemical value chain that co-locates tire plants, petrochemical crackers, and advanced material research and development centers. Producers in the Rhineland are piloting cracker off-gas routes that slash feedstock imports and cut emissions intensity. The presence of leading tire OEM research and development divisions also accelerates the qualification of next-generation low-rolling-resistance and recovered grades, reinforcing Germany’s preeminence within the European carbon black market.

The United Kingdom is on course for a 6.55% CAGR to 2031, the fastest among major economies. Post-Brexit localization drives domestic mixing facilities to source within the British Isles wherever feasible, reducing border-related lead-time risk. Sterling weakness has also bolstered specialty black exports for coatings and batteries, improving asset utilization at UK plants and attracting fresh capital commitments from global incumbents and new entrants .

France, Italy, and the Rest of Europe maintain solid positions anchored in automotive and industrial production. France is advancing recovered carbon black integration ahead of many peers, benefiting from Michelin-led demonstration projects that delivered commercial validation in 2024. Italy’s demand aligns closely with replacement-tire cycles, while niche opportunities in the Netherlands, Sweden, and Poland revolve around battery manufacturing and specialty chemical clusters. Eastern Europe is still recalibrating following the Russian import ban, prompting rapid sourcing realignments toward Western European and Asian suppliers.

Competitive Landscape

Regional supply is moderately consolidated. Orion Engineered Carbons, Cabot Corporation, and Birla Carbon are supported by vertically integrated feedstock access and extensive application-development laboratories close to customer sites. Their strategic focus is on specialty-grade expansion, digitalized plant upgrades, and certification for low-PAH compliance to defend share against rising substitutes. The regulatory push for circularity enables new entrants such as Black Bear Carbon and Pyrum Innovations to mount credible competition in recovered carbon black. Their pyrolysis-derived grades now pass OEM endurance tests and secure supply contracts for original equipment tires.

Europe Carbon Black Industry Leaders

Birla Carbon (Aditya Birla Group)

Cabot Corporation

Orion Engineered Carbons

Omsk Carbon Group

Tokai Carbon Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Orion Engineered Carbons announced plans to shut down three to five carbon black production lines across its facilities, including Europe, by the end of 2025. The move is part of a broader strategy to optimize operational efficiency by focusing investments on higher-performing assets and phasing out underutilized lines.

- March 2025: Orion Engineered Carbons was acknowledged by the European Commission’s Innovation Radar as a “Key Innovator” for its breakthrough in producing circular carbon black entirely from tire pyrolysis oil. Developed under the EU-funded BlackCycle project, this innovation positions Orion as a leader in sustainable carbon black solutions within the European market.

Europe Carbon Black Market Report Scope

Carbon black is a fine carbon powder made by incomplete combustion or thermal decomposition of gaseous or liquid hydrocarbons under controlled conditions. The Europe carbon black market is segmented based on type, application, and geography. By type, the market is segmented into furnace black, gas black, lamp black, and thermal black. By application, the market is segmented into tires and industrial rubber products, plastics, toners and printing Inks, coatings, textile fibers, and other applications. The report also covers the market size and forecasts for the carbon black market in 5 countries across the region. The market sizing and forecasts for each segment are based on revenue (USD million) and volume (kilotons).

By Process Type

| Furnace Black |

| Gas Black |

| Thermal Black |

| Lamp Black |

By Application

| Tire and Industrial Rubber Product |

| Plastic |

| Toner and Printing Ink |

| Coating |

| Textile Fiber |

| Others |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Russia |

| Rest of Europe |

| By Process Type | Furnace Black |

| Gas Black | |

| Thermal Black | |

| Lamp Black | |

| By Application | Tire and Industrial Rubber Product |

| Plastic | |

| Toner and Printing Ink | |

| Coating | |

| Textile Fiber | |

| Others | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe carbon black market in 2026?

The market is valued at USD 5.59 billion in 2026 and is predicted to reach USD 7.24 billion by 2031.

What CAGR is the regional market expected to record between 2026 and 2031?

The Europe carbon black market is forecast to register a 5.31% CAGR during the period.

Which process type dominates regional demand?

Furnace black leads with 73.88% of 2025 volume, thanks to its versatility across tire and industrial applications.

Which country is expanding fastest?

The United Kingdom shows the highest growth momentum at a projected 6.55% CAGR to 2031.

How are circular-economy rules affecting supply?

EU directives are driving adoption of recovered carbon black, with new capacity from partnerships such as Bridgestone-BB&G-Versalis adding 30,000 metric tons of recycled material annually.

Page last updated on: