Europe Camping And Caravanning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

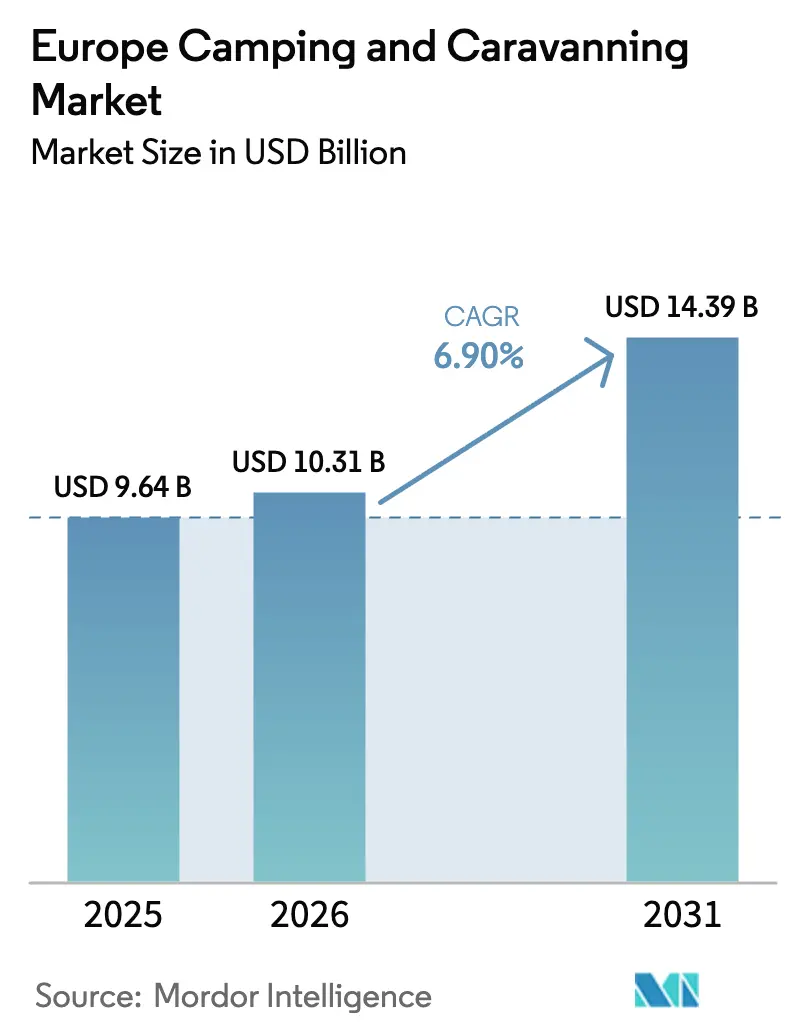

| Base Year Market Size (2025) | USD 9.64 Billion |

| Market Size (2026) | USD 10.31 Billion |

| Market Size (2031) | USD 14.39 Billion |

| Growth Rate (2026 - 2031) | 6.90% CAGR |

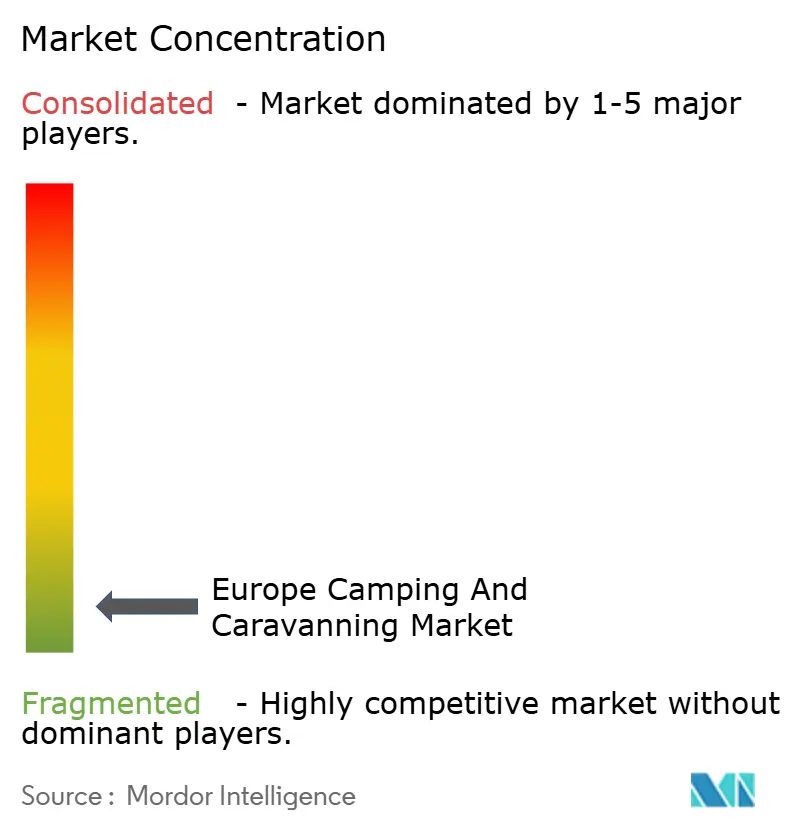

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Camping And Caravanning Market Analysis by Mordor Intelligence

The Europe camping and caravanning market size is expected to grow from USD 9.64 billion in 2025 to USD 10.31 billion in 2026 and is projected to reach USD 14.39 billion by 2031, reflecting a 6.90% CAGR over 2026-2031. EU tourist accommodation recorded 413 million campsite nights in 2025, accounting for 13% of the region’s 3.08 billion total tourism nights, which reinforces the resilience of outdoor stays as a mainstream travel choice[1]Source: Eurostat Editorial Team, “Record Number of Tourism Nights in the EU,” Eurostat, ec.europa.eu. Growth is supported by sustained domestic travel preferences that favor short-haul road trips, the early adoption of electrified recreational vehicles that pull forward premium demand, and the scaling of online booking platforms that compress distribution friction and expand inventory reach. Operators are countering peak-season concentration through investments in all-weather amenities and year-round infrastructure, a strategy validated by winter-oriented portfolio additions in the Nordics and selective municipal partnerships that extend capacity through standardized motorhome stopovers. Technology-enabled yield management and certification-led differentiation remain important levers for operators seeking to protect pricing power and sustain margins as energy and labor costs rise.

Key Report Takeaways

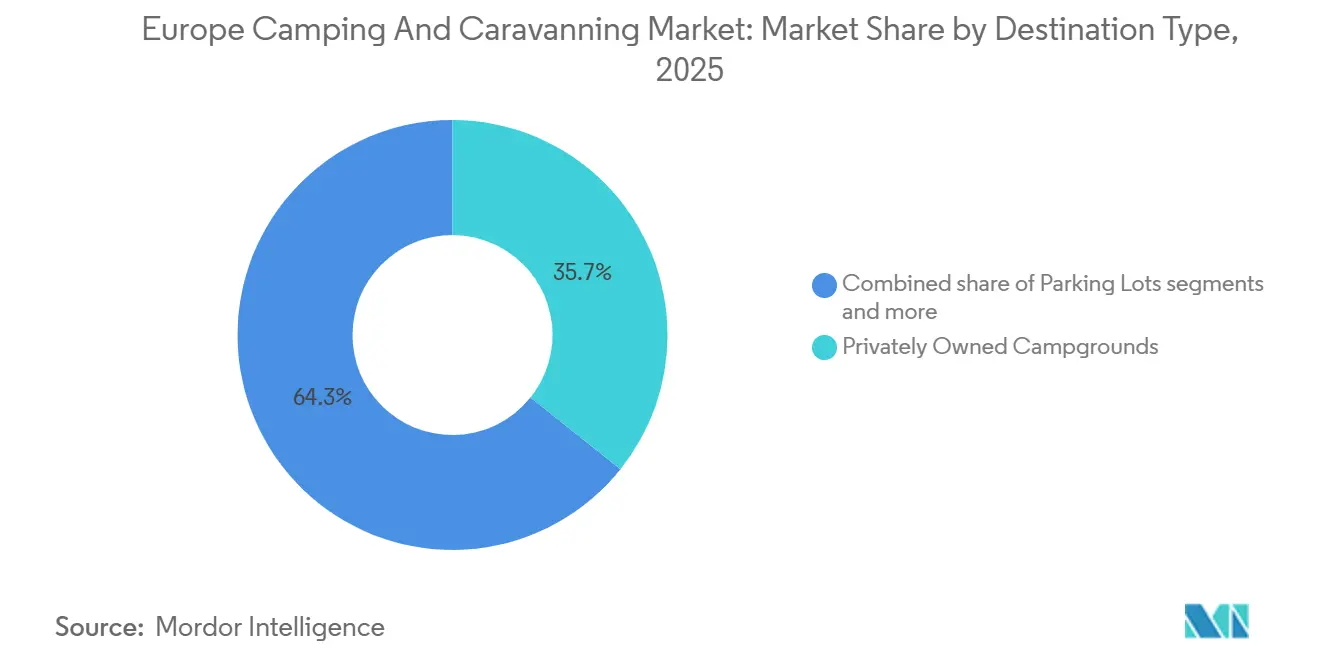

- By destination type, privately owned campgrounds led with 35.74% revenue share in 2025; backcountry and wilderness areas are projected to expand at a 9.12% CAGR through 2031.

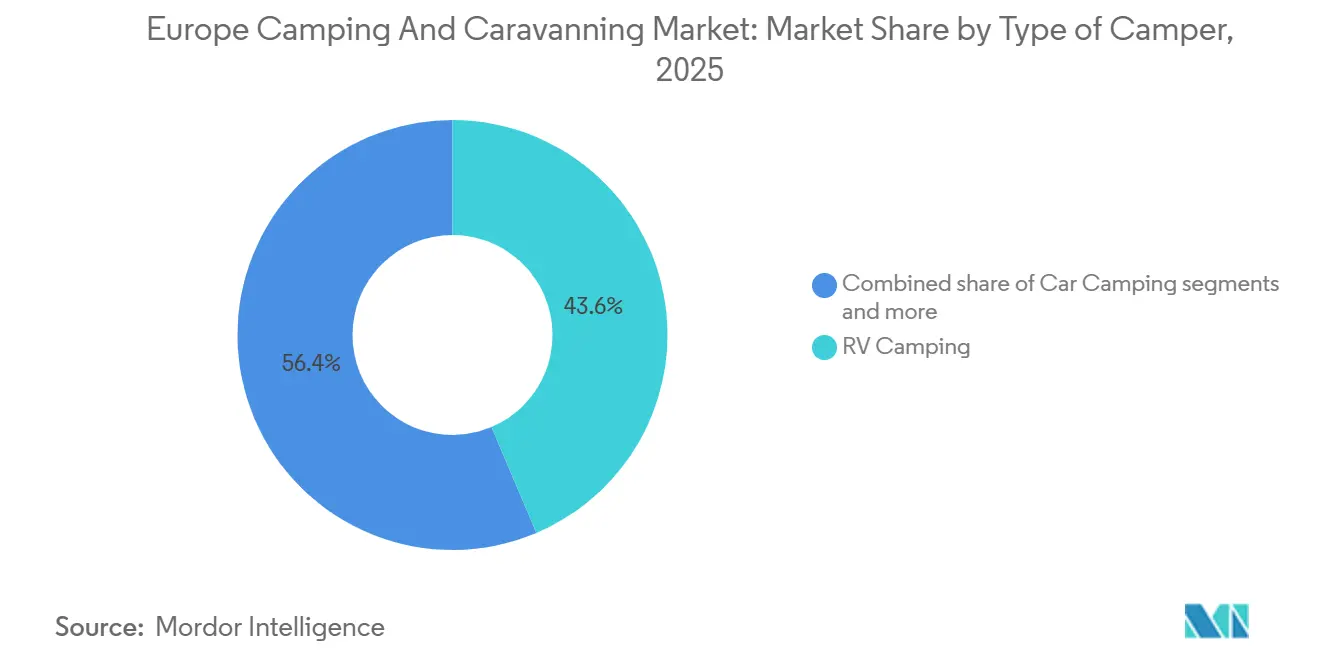

- By type of camper, RV camping captured 43.62% of the European Camping and Caravanning market share in 2025, while backpacking is forecast to post the fastest 10.95% CAGR to 2031.

- By distribution channel, online travel agencies controlled 46.85% share of the European camping and Caravanning market size in 2025 and are advancing at a 11.78% CAGR through 2031.

- By geography, Germany led with 25.05% revenue share in 2025; the Nordic countries are projected to grow at an 7.93% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe contributes to a system defined not by any single geography but by the interaction of many. The global camping and caravanning market data by Mordor Intelligence represents that combined structure.

Europe Camping And Caravanning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domestic tourism sees a surge in nights booked, rebounding from COVID-19 setbacks | +1.8% | Global, strongest in Germany and France | Medium term (2-4 years) |

| Recreational vehicles undergo a green transformation with electrification (eRVs) | +1.2% | EU core markets, led by Germany and Netherlands | Long term (≥ 4 years) |

| Online platforms for campsite bookings witness significant expansion | +1.5% | Global, with Nordic countries leading adoption | Short term (≤ 2 years) |

| Investments pour in for season-extension, introducing all-weather amenities | +0.9% | Northern Europe, BENELUX, and UK | Medium term (2-4 years) |

| High-spending campers drawn in by eco-certifications | +0.7% | Western Europe, particularly France and Germany | Long term (≥ 4 years) |

| Rural tourism redevelopment gets a boost from government incentives | +0.6% | Southern and Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Domestic tourism sees a surge in nights booked, rebounding from COVID-19 setbacks

Domestic guests remained the anchor of Europe’s travel recovery, and 2025 campsite nights equaled 13% of all EU tourism nights, which indicates that outdoor accommodation has continued to benefit from short-haul travel and near-home itineraries. The Europe camping and caravanning market gains from travelers who value space, nature access, and affordability relative to hotels during periods of price pressure in air travel and urban stays. Germany’s broad-based tourism strength in 2025 supported incremental demand for camping nights as drive-to trips stayed popular for families and retirees alike, reinforcing steady occupancy in high-capacity regions. Operators increasingly design amenities that fit blended travel, such as quiet work areas and robust Wi-Fi, which supports longer stays by guests mixing workdays with outdoor leisure[2]Source: ACSI Editorial Team, “ACSI Times Spring 2025,” ACSI, acsi.eu. The Europe camping and caravanning market continues to consolidate domestic loyalty by highlighting value-for-money and showcasing eco-certified sites that match preferences in Northern and Western Europe.

Recreational vehicles undergo a green transformation with electrification (eRVs)

Innovation in eRVs is catalyzing a higher-value segment that benefits the Europe camping and caravanning market over the long term through upgrades to vehicles and on-site power infrastructure. Recent product showcases, including electrified drivetrains and high-capacity lithium battery systems in compact all-wheel-drive models, signal a push toward vehicles that can reach remote pitches while powering modern amenities[3]Source: Dethleffs Communications, “Globebus Performance and Electrified Innovation,” Dethleffs, dethleffs.de. Lightweight caravan concepts optimized for EV towing aim to broaden access among urban consumers, which may increase off-peak travel and diversify site usage. Northern operators are adding EV charging and renewable energy features, which positions certified sites to attract early adopters and sustainability-minded guests. The Europe camping and caravanning market benefits as infrastructure-readiness becomes a booking filter for higher-spend travelers selecting sites that can support electric tow vehicles and silent, battery-based onboard systems.

Online platforms for campsite bookings witness significant expansion

OTAs and aggregated booking platforms continue to gain share because they simplify discovery, payment, and yield management for both operators and guests, with some networks reporting large increases in transactions and revenue heading into 2025. The Europe camping and caravanning market is influenced by platform economics, as intermediaries scale inventory, centralize marketing, and drive conversion through multilingual apps and instant confirmations. Operators retain direct channels for brand-loyal guests, yet OTAs accelerate bookings in shoulder seasons with algorithmic pricing that responds to weather and events. Municipal partnerships that open standardized motorhome stopovers are also enabled by platform operations, which extend capacity near towns and redistribute flows away from saturated coastal areas [4]Source: CAMPING-CAR PARK Press Office, “Bilan 2025 et Perspectives 2026,” CAMPING-CAR PARK, campingcarpark.com. As compliance with EU data and payments rules becomes table stakes, larger platforms convert regulatory costs into moats that smaller, offline operators find hard to cross, reinforcing the channel shift in the Europe camping and caravanning market.

Investments pour in for season-extension, introducing all-weather amenities

Campsite demand is still concentrated in Q3, and official statistics confirm that most annual nights occur in July to September, which leaves under-utilized capacity in the rest of the year. Nordic consolidators demonstrated that targeted acquisitions and winterized amenities can shift revenue into Q4 and Q1, improving asset turns and staffing stability across the year. Investments in heated facilities, insulated sanitary blocks, and indoor pools enable sites to host families and activity seekers beyond summer, which expands booking windows and diversifies occupancy. The Europe camping and caravanning market aligns with public co-funding where regional programs support small-scale eco-lodging and glamping pods that extend seasons without heavy environmental impacts. Dynamic pricing tools allow operators to lift weekend rates and discount mid-week stays, smoothing occupancy while protecting margins across variable weather patterns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Campgrounds face challenges with seasonal fluctuations and under-utilized capacity | -1.4% | Northern Europe, particularly UK and Nordics | Medium term (2-4 years) |

| RVs grapple with strict regulations on emissions and size | -0.8% | EU-wide, strongest impact in Germany and France | Long term (≥ 4 years) |

| Local zoning restrictions lead to conflicts over land use | -0.6% | Western Europe urban peripheries, coastal regions | Long term (≥ 4 years) |

| Operating costs, including energy, labor, and insurance, are on the rise | -0.5% | Global, with acute impact in BENELUX and Nordic countries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Campgrounds face challenges with seasonal fluctuations and under-utilized capacity

Seasonality limits year-round utilization and strains cash flows outside peak months, with official data showing a concentration of stays in Q3 for the EU. Even strong summer performance can waver due to weather or geopolitical sensitivities, and several Mediterranean hubs have highlighted occupancy volatility during peak weeks. In August 2025, Croatia reported a high number of camping nights but also revealed a dip in occupancy compared with the prior year, which highlights exposure to short-term shocks despite seasonal peaks. Financing new amenities becomes more complex when revenue is concentrated in one quarter, as lenders price higher risk into terms and operators weigh returns over a shorter operating window. The Europe camping and caravanning market therefore places a premium on season-extension levers and municipal collaborations that transform idle winter space into shoulder-season stays.

RVs grapple with strict regulations on emissions and size

Environmental zones, emissions limits, and vehicle inspections are changing purchasing criteria for new and used RVs in large European markets, which narrows the accessible pool of older diesel models and affects affordability. Operators and guests adapt by favoring compliant panel-van conversions and compact formats that meet urban access and parking constraints, a pattern visible in vehicle mix trends reported by manufacturers and trade associations. The Europe camping and caravanning market is responding with infrastructure upgrades that anticipate more electrified vehicles and onboard power needs at certified sites. Persistent differences in local rules create uncertainty for cross-border touring, which increases planning costs for multi-country trips. These shifts advantage organized chains and platforms that can help travelers navigate local compliance while offering standardized, bookable pitches across diverse regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Destination Type: Wilderness Areas Challenge Established Campground Models

Privately owned campgrounds captured 35.74% of the 2025 market value, reflecting consistent investments in amenities and branding that sustain price premiums, and this concentration shows how quality and service breadth support share within the Europe camping and caravanning market size in 2025. State and national park campgrounds appeal to guests focused on trails and nature access, yet they often face constraints on dynamic pricing and amenity expansion. Parking lots and standardized stopovers have grown as a convenience layer for itinerant RV users, supported by networks that deliver reliable, year-round pitches near towns and public attractions. Public or privately owned land outside formal campgrounds remains a niche defined by local zoning and conservation rules, which drives uncertainty for operators and travelers. The Europe camping and caravanning market continues to reward professional management where facilities, compliance, and digital distribution converge to keep occupancy steady across variable conditions.

Backcountry, national forest, and wilderness areas are forecast to expand at a 9.12% CAGR to 2031, led by younger travelers who value immersive nature stays and minimal infrastructure, which positions this segment as a fast-growth counterweight to legacy campground formats. Nordic markets exemplify this shift with strong summer camping nights in nature-rich regions and a cultural emphasis on responsible outdoor life, which supports longer itineraries and diversified stay types that blend cabins, tents, and minimalist pitches. As local restrictions tighten in sensitive areas, operators respond with “nature-near” sites that preserve wilderness appeal while delivering basic sanitation and safety aligned to certification frameworks. These formats help municipalities balance environmental stewardship with visitor flows, a trade-off that becomes more important as peak-season crowds concentrate in headline destinations. The Europe camping and caravanning industry adapts by curating low-impact options that meet standards while maintaining the authenticity sought by backcountry-oriented guests.

By Type of Camper: Backpacking Outpaces RV Volumes Despite Asset-Light Model

RV camping held 43.62% in 2025, helped by new registrations across Europe that kept the installed base expanding despite macro headwinds, a sign that vehicle-based touring remains a core pillar of the Europe camping and caravanning market size. In Germany, motorhome stock surpassed the one million mark in 2025, underscoring how panel-van conversions and compact models meet both weekday utility and weekend travel goals for a wide demographic. Product innovation from European manufacturers targets efficiency, safety, and off-grid capability, which reshapes campsite needs for power, water, and service bays. Car camping remains a stable middle option for families preferring tents and flexible transport without the capital intensity of a motorhome. As more sites install EV charging and standardized pitch services, RV owners can plan longer routes with greater certainty across seasons. The Europe camping and caravanning market continues to integrate RV-specific services that raise satisfaction and smooth on-site operations.

Backpacking is projected to advance at a 10.95% CAGR through 2031, led by gear innovation and a preference for experiential travel, which lowers entry costs and increases trip frequency among younger cohorts. Nordic regions report robust summer bed nights, and the right-to-roam culture supports minimalist itineraries that blend wilderness stays with campground services where needed. Operators are responding with amenities for mobile workers and lightweight travelers, including co-working corners and charging hubs, which monetize ancillary services with limited capital outlay. Weather remains a sensitivity for tent-based travelers, yet diversified site formats with simple heated cabins and sheltered kitchens can extend stays into the shoulder months. The Europe camping and caravanning industry aligns to these patterns by adding flexible micro-accommodations that protect value in variable conditions.

By Distribution Channel: OTAs Dominate Through Data-Driven Yield Management

Online travel agencies controlled 46.85% of bookings in 2025 and are growing at an 11.78% CAGR, a level that reflects their role in inventory aggregation, instant confirmations, and dynamic pricing at scale within the Europe camping and caravanning market size. Several platforms reported sharp gains in bookings and revenue through early 2025, which shows sustained consumer preference for mobile-first booking and transparent comparisons across sites and regions. Direct channels remain important for strong brands that nurture loyalty and cross-sell activities, but OTAs excel at capturing impulse demand linked to weather and events. Standardized stopover networks demonstrate how digital operations can activate municipal assets and steer demand to under-served areas in peak periods. The Europe camping and caravanning market therefore reflects a dual channel strategy in which platforms extend reach while operators protect margin and first-party data.

Platform economics rely on network effects, compliance capabilities, and product quality signaling that lifts conversion on premium listings. Yield-management tools elevate average booking values by matching nightly rates to real-time demand drivers, and operators gain access to seasonal demand patterns that inform staffing and maintenance plans. Public-private coordination around standardized motorhome pitches increases capacity without heavy private capital, and deployment kits for ephemeral sites during major events show how platforms manage surge demand reliably. As regional growth accelerates in Central and Eastern Europe, mobile-first booking lowers friction for international travelers using cross-border itineraries. The Europe camping and caravanning market will keep rewarding digital excellence as guests expect instant search, verified reviews, and secure payments across languages.

Geography Analysis

Germany anchored 25.05% of 2025 market value and remains the largest national contributor to the Europe camping and caravanning market, supported by a deep vehicle base and an active domestic travel culture that prefers road-accessible destinations. EU-wide campsite nights totaled 413 million in 2025, equal to 13% of all tourism nights across the bloc, which highlights the scale of the outdoor segment in regional travel balances. Sustained motorhome registrations and a diverse mix of panel-van conversions and compact models have supported camping supply and route flexibility for German and near-market travelers. The Europe camping and caravanning market benefits from Germany’s cross-border trips into the Netherlands, Denmark, France, and Alpine regions, which stabilizes regional demand across peak and shoulder seasons.

The Nordics are projected to grow at a 7.93% CAGR to 2031, led by site winterization, resort-style acquisitions in Lapland, and nature-rich itineraries that extend beyond summer months. Portfolio strategies that add winter-amenitized properties have increased the share of revenue generated in Q4 and Q1 for leading Nordic chains, improving labor continuity and asset productivity. Sweden’s summer camping nights held up well in 2025, and national data support the continued draw of lakes and forests for family and backpacking trips, which balances coastal saturation elsewhere in Europe. As electrified vehicles grow in the region, certification frameworks and EV-ready facilities help Nordic operators attract high-spend travelers who value low-impact operations. The Europe camping and caravanning market therefore sees the Nordics as an engine of mix improvement through longer seasons and higher-value stays.

In Western Europe, France and Italy sustain robust camping flows through a blend of coastal, countryside, and heritage routes, while pricing and regulatory differences shape site development and upgrade timing. Benelux markets illustrate high domestic participation supported by strong certification and quality signaling, which facilitates cross-border trips with neighboring Germany and France. Central and Eastern Europe show rising interest through platform-enabled discovery and favorable value-for-money, which expands route options for budget-conscious and adventure-oriented travelers. The Europe camping and caravanning market is also shaped by municipal collaborations that open standardized motorhome stopovers, which channel visitors to smaller towns and support local spending without heavy private land development.

The camping and caravanning market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Americas.

Competitive Landscape

The Europe camping and caravanning market remains highly fragmented, with no single operator holding more than a low-single-digit share, and thousands of mostly family-run sites spread across the Nordics, DACH, Benelux, the Mediterranean, and Central Europe. European Camping Group operates one of the largest footprints and reported new eco-label certifications and portfolio additions for the 2026 season, which supports premium positioning with Northern and Western European guests. First Camp showed how strategic winter-oriented acquisitions can rebalance revenue across the year and validate season-extension returns in Arctic destinations. The Europe camping and caravanning market also reflects the influence of municipal partnerships for standardized motorhome pitches, which unlocks latent demand and spreads visitor flows more evenly over regions.

RV manufacturers shape demand patterns and site requirements through product innovation and production adjustments. Trigano reported a sales decline in FY2024/25 while maintaining dividend continuity, and Knaus Tabbert adjusted 2025 output in response to supply constraints yet continued to invest in future drivetrains. Dethleffs advanced electrified and 4x4-capable offerings and earned design recognition, which underscores a move toward vehicles that favor backcountry access and on-board energy autonomy. These shifts motivate operators to install EV charging, solar canopies, and durable pitch surfaces to accommodate diversified vehicle types. The Europe camping and caravanning market therefore sees equipment makers and site operators co-evolving standards that lift service quality and guest satisfaction.

Digital intermediaries continue to expand influence with strong booking growth, inventory standardization, and yield-management capabilities. ACSI’s integrated booking engine reported notable increases in both transaction volumes and revenue heading into the 2025 season, while maintaining compliance with EU data and payments rules that underpin consumer trust. CAMPING-CAR PARK reported strong performance in nights and revenue while redistributing funds to partner municipalities, which proves the sustainability of a standardized stopover model at scale. As certification frameworks like EU Ecolabel and ISO 14001 spread, premium platforms and large operators differentiate on environmental performance and infrastructure-readiness, which resonates with Northern European travelers and strengthens year-round appeal. The Europe camping and caravanning market will continue to reward strategies that combine scale, sustainability credentials, and proprietary technology.

Europe Camping And Caravanning Industry Leaders

European Camping Group

Erwin Hymer Group

Trigano

Knaus Tabbert

ACSI

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: European Camping Group (ECG) certified 64 campsites under eco-label frameworks (Green Key, EU Ecolabel) for the 2026 season, reinforcing its positioning as the continent's sustainability leader and attracting high-spend northern European guests who prioritize environmental credentials. The certification portfolio spans France, Netherlands, Germany, Italy, and Spain, with each site meeting ISO 14001 environmental-management standards and achieving waste-diversion rates exceeding 60%.

- December 2025: European Camping Group (ECG) acquired three new wholly owned campsite properties and expanded its partner network by 13 additional locations across southern France, Tuscany, and Costa Brava, lifting its total footprint to 450-plus destinations in 13 countries. The acquisitions financed through operating cash flow and a USD 47.05 million (EUR 40 million) revolving credit facility target high-occupancy coastal sites with year-round operating permits and premium amenity investments exceeding USD 2.3 million (EUR 2 million) per property.

- November 2025: European Camping Group (ECG) completed a comprehensive rebrand to "ECG" alongside a new brand architecture that consolidates marketing spend, unifies digital booking platforms, and creates tier-segmented sub-brands (Premium, Family, Nature) to clarify positioning for OTA algorithms and direct-search users. The rebrand followed PAI Partners' agreement to sell a minority equity stake to Abu Dhabi Investment Authority (ADIA), expected to close in Q2 2025, valuing ECG at an estimated USD 1.76 billion (EUR 1.5 billion).

- August 2025: Knaus Tabbert AG reported Q2 2025 revenue of USD 671.7 million (EUR 571.7 million), down 18.3% year-on-year, alongside adjusted EBITDA of EUR 22.7 million (4.0% margin) and free cash flow of USD 82.3 million (EUR 70.1 million) (+116.2%). The German manufacturer adjusted its 2025 production plan downward to roughly USD 1.17 billion (EUR 1 billion) annual revenue due to chassis-supplier delivery delays from Fiat Professional and Ford, yet maintained investment in electrified motorhome prototypes targeting 2027 commercialization.

Europe Camping And Caravanning Market Report Scope

Camping and caravanning are outdoor recreational activities that involve traveling and staying in tents or recreational vehicles (RVs) or caravans. These activities allow people to explore and experience the great outdoors, often in natural settings such as national parks, forests, beaches, and mountains. Both camping and caravanning offer a range of benefits, including the opportunity to connect with nature, escape from the stresses of daily life, and spend quality time with family and friends. They also provide a flexible and cost-effective travel method, with many camping and RV parks offering affordable accommodations and amenities.

The Europe Camping and Caravanning Market is Segmented by Destination Type (State or National Park Campgrounds, Privately Owned Campgrounds, Public or Privately Owned Land Other than a Campground, Backcountry, National Forest or Wilderness Areas, Parking Lots, and Others), Type of Camper (Car Camping, RV Camping, Backpacking, and Others), Distribution Channel (Direct Sales, Online Travel Agencies, and Traditional Travel Agencies), and Country (Germany, France, United Kingdom, Italy, And Rest Of Europe). The Report Offers Market Size and Forecasts for Europe Camping and Caravanning Market in Terms of Value in (USD) for all the Above Segments.

| State or National Park Campgrounds |

| Privately Owned Campgrounds |

| Public or Privately Owned Land Other Than a Campground |

| Backcountry, National Forest or Wilderness Areas |

| Parking Lots |

| Others |

| Car Camping |

| RV Camping |

| Backpacking |

| Others |

| Direct Sales |

| Online Travel Agencies |

| Traditional Travel Agencies |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Destination Type | State or National Park Campgrounds |

| Privately Owned Campgrounds | |

| Public or Privately Owned Land Other Than a Campground | |

| Backcountry, National Forest or Wilderness Areas | |

| Parking Lots | |

| Others | |

| By Type of Camper | Car Camping |

| RV Camping | |

| Backpacking | |

| Others | |

| By Distribution Channel | Direct Sales |

| Online Travel Agencies | |

| Traditional Travel Agencies | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size and growth outlook for the Europe camping and caravanning market?

The Europe camping and caravanning market size was USD 9.64 billion in 2025 and is projected to reach USD 14.39 billion by 2031 at a 6.90% CAGR.

Which countries lead demand in Europe for camping and caravanning?

Germany led with 25.05% of 2025 market value, and the Nordics are the fastest growing region, projected at a 7.93% CAGR through 2031.

What channels are growing fastest for campsite bookings in Europe?

Online travel agencies controlled 46.85% of bookings in 2025 and are advancing at an 11.78% CAGR due to inventory aggregation, instant confirmation, and dynamic pricing.

Which customer segments are expanding most quickly?

Backpacking is projected to grow at a 10.95% CAGR through 2031, while RV camping held 43.62% share in 2025, supported by continued motorhome and van registrations.

How are operators addressing seasonality across Europe?

Operators invest in heated amenities, winterized cabins, and standardized stopovers, use dynamic pricing, and partner with municipalities, which helps shift nights into Q4 and Q1 and smooth occupancy.

What technology and product shifts are most influential for the next few years?

Electrified RV concepts, on-site EV charging readiness, and OTA-driven yield management are shaping product mix and distribution, which supports premium stays and broader season coverage.

Page last updated on: