Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.49 Billion |

| Market Size (2026) | USD 3.65 Billion |

| Market Size (2031) | USD 4.56 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Wellness Tourism Market Analysis by Mordor Intelligence

The Europe wellness tourism market size was valued at USD 3.49 billion in 2025 and estimated to grow from USD 3.65 billion in 2026 to reach USD 4.56 billion by 2031, at a CAGR of 4.55% during the forecast period (2026-2031). Strong consumer preference for preventive healthcare, deep-rooted spa cultures, and active government support position the Europe wellness tourism market on a durable growth path. Travel suppliers are weaving sustainability and digital detox concepts into itineraries, while hotel groups upscale spa, fitness, and nutrition programs to secure higher yields. Millennial and Gen Z travelers keep demand diversified across premium and mid-range offerings, and technology-enabled personalization continues to raise service expectations. These trends combine to widen the opportunity set for both multinational chains and owner-operated retreats throughout the Europe wellness tourism market.

Key Report Takeaways

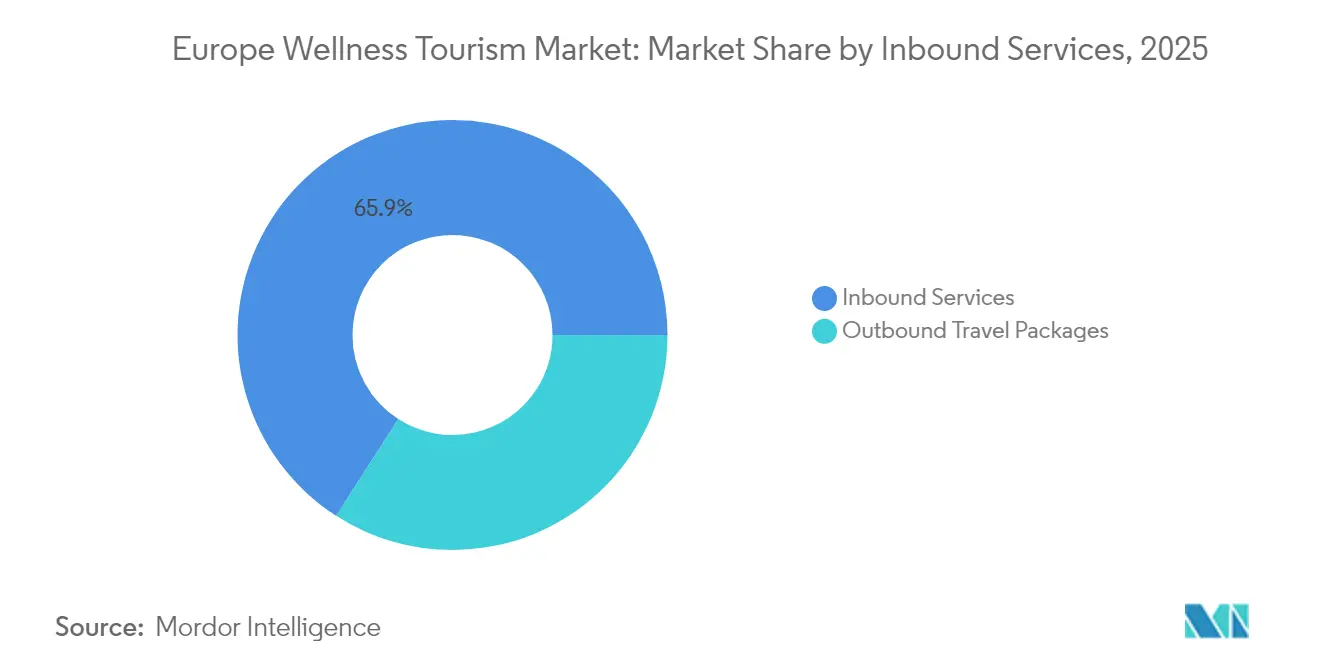

- By service type, inbound services led with 65.90% of Europe wellness tourism market share in 2025; outbound packages are projected to expand at a 6.24% CAGR to 2031.

- By traveler demographic, couples accounted for 39.75% of the Europe wellness tourism market size in 2025, while solo travelers are advancing at a 7.05% CAGR through 2031.

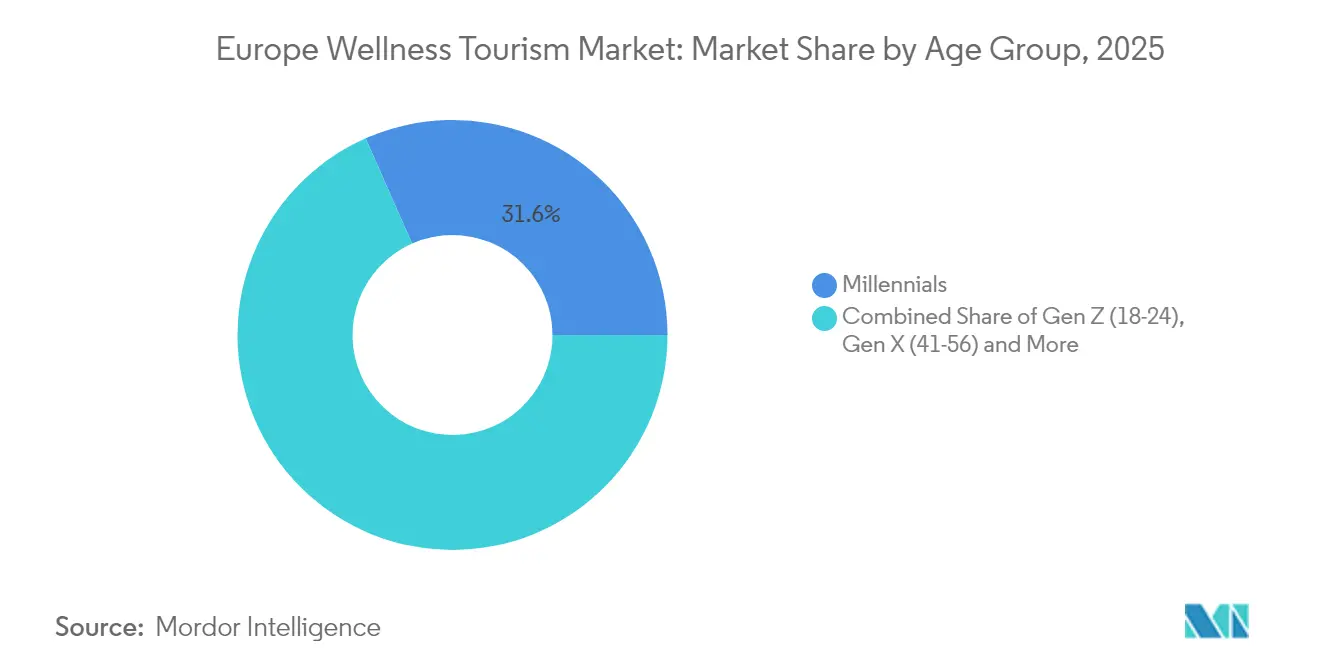

- By age group, millennials represented 31.62% of the Europe wellness tourism market size in 2025; Gen Z is poised for the fastest growth, rising at a 8.92% CAGR between 2026-2031.

- By booking channel, OTAs commanded 44.86% share of the Europe wellness tourism market size in 2025, and wellness tour operators are forecast to grow at an 7.62% CAGR through 2031.

- By geography, Germany held 19.92% of the Europe wellness tourism market share in 2025, whereas Italy is set to expand at a 8.55% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Wellness Tourism Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Health Consciousness & Preventive Healthcare | +5.2% | Global, with particular strength in Northern and Western Europe | Medium term (2-4 years) |

| Strong Infrastructure & Spa Tradition | +3.8% | Central Europe (Germany, Austria), Mediterranean (Italy, Spain, France) | Short term (≤ 2 years) |

| Ageing Population Seeking Wellness Retreats | +2.7% | Germany, UK, France, Italy, Nordic countries | Long term (≥ 4 years) |

| Government & EU Support for Wellness Tourism | +2.1% | EU-wide, with stronger impact in Eastern European countries | Medium term (2-4 years) |

| Growth of Digital Detox and Sustainable Travel | +1.5% | Pan-European, with concentration in Nordic countries and Alpine regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Health Consciousness & Preventive Healthcare

Policy makers echo this trend, the European Commission’s Health at a Glance 2024 stresses preventive healthcare as a priority, reinforcing demand for wellness stays that integrate diagnostics, nutrition, and movement. Operators leverage this momentum by bundling medical checkups, mindfulness sessions, and outdoor activities, enabling the Europe wellness tourism market to capture discretionary spend otherwise allocated to conventional holidays. Wellness villages in Germany and forest-based retreats in Finland illustrate how preventive care packages are becoming mainstream. As consumer education deepens, suppliers that showcase measurable health outcomes continue to secure premium pricing.

Strong Infrastructure & Spa Tradition

Centuries-old bath cultures in Germany, Austria, and Italy anchor a dependable pipeline of domestic and regional visitors. Restored Roman baths, Alpine thermal springs, and Thalassotherapy centers in France offer purpose-built facilities well suited to contemporary wellness programs. The Europe wellness tourism market benefits from these sunk investments: operators add modern diagnostics, sleep labs, and functional training zones without large-scale construction. Municipal governments frequently co-finance upgrades, viewing spa clusters as regional economic stabilizers. This long-standing infrastructure lowers entry barriers for new themed experiences, from biohacking workshops to longevity clinics.

Ageing Population Seeking Wellness Retreats

Chronic illnesses linked to lifestyle choices intensify interest in organized wellness holidays that target mobility, cardiovascular health, and metabolic fitness. Resorts react by adding low-impact exercise, anti-inflammatory menus, and caregiver support. As a result, the Europe wellness tourism market increasingly tailors offerings to joint pain relief, cardiac rehabilitation, and stress management for retirees. Suppliers that adapt room designs, activity timetables, and medical staffing to senior needs secure repeat visitation and higher lengths of stay.

Government & EU Support for Wellness Tourism

The EU tourism transition pathway calls for greener, more digital services, providing technical guidance and funding windows that directly favor wellness operations. The European Parliament urges member states to embed wellness in tourism and health policy, citing its ability to flatten seasonality and raise job quality. Eastern European destinations, from Hungary to Slovenia, are tapping cohesion funds to refurbish historic baths, digitize booking engines, and train therapists. These initiatives enhance service standards and visibility, reinforcing traveler confidence in lesser-known regions. Continuous public-private collaboration gives the Europe wellness tourism market structural resilience against cyclical headwinds.

Restraints Impact Analysis*

| Restraint | (~)-% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Premium Wellness Packages | -2.1% | Pan-European, particularly in luxury destinations | Medium term (2-4 years) |

| Seasonal Demand Fluctuations | -1.8% | Mediterranean and Alpine regions | Short term (≤ 2 years) |

| Stringent Health Regulations & Licensing | -1.3% | EU-wide, with stronger impact in Western Europe | Medium term (2-4 years) |

| Competition from Low-Cost International Destinations | -0.9% | Southern and Eastern Europe primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Premium Wellness Packages

Wellness retreats in Europe’s top spa towns often command daily rates exceeding USD 600, narrowing the addressable base to affluent consumers. The European Parliament cautions that elevated price points exclude mid-income travelers and strain growth potential. Inflation in utilities and skilled labor widens cost gaps versus comparable Thai or Turkish resorts. To defend volume, operators introduce shorter three-night programs, off-season discounts, and tiered service models. Dynamic pricing engines also help right-size tariffs to demand patterns. While price sensitivity weighs on upscale properties, mid-market players that optimize cost structures can still secure share within the Europe wellness tourism market.

Seasonal Demand Fluctuations

Sun-and-sea wellness resorts in Spain, Greece, and Croatia peak in summer, whereas Alpine spas concentrate activity between December and March. Such seasonality drives uneven cash flows, underutilized staff, and higher per-guest overheads. Tourism boards encourage off-season events, fitness festivals, and medical-wellness conferences to smooth occupancy. Multi-functional facilities that host corporate wellness workshops in shoulder months are better insulated. Resolving seasonality remains vital for sustained profitability across the Europe wellness tourism market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Inbound Services Dominate While Outbound Packages Gain Momentum

Inbound services generated 65.90% of 2025 revenue within the Europe wellness tourism market. Thermal baths in Baden-Baden, mud therapies in Abano Terme, and Nordic saunas in Lapland continue to lure regional visitors. The Europe wellness tourism market size for inbound programs is expected to expand at a steady pace as supply upgrades align with new preventive-health expectations. Cross-selling accommodation, gastronomy, and diagnostics elevates average spending and prolongs stays.

Outbound wellness packages show a 6.24% CAGR for 2026-2031. Europeans are pursuing yoga in Portugal, Ayurveda in India, and marine-therapy cruises in the Mediterranean. Flexible work schedules enable shoulder-season travel, supporting load factors for tour operators. The Europe wellness tourism market benefits as outbound specialists leverage dynamic packaging technology, curated practitioner networks, and transparent sustainability labels that appeal to Gen Z explorers.

By Traveler Demographic: Couples Lead While Solo Travelers Show Strongest Growth

Couples represented 39.75% of 2025 transactions in the Europe wellness tourism market. Romantic spa suites, double-occupancy thermal pools, and tailor-made nutrition counseling encourage joint participation. Packages that integrate wine-tasting with mindfulness walks strengthen emotional bonding while enhancing resort margins. The Europe wellness tourism market size derived from couples is poised for incremental gains as the wedding-anniversary and babymoon segments mature.

Solo travelers register a 7.05% CAGR and are reshaping product design. Women account for a sizable share, often booking fitness-centric retreats that blend personal growth with social interaction. Resorts respond by scheduling communal dining tables, group hikes, and life-coaching sessions, balancing autonomy with companionship. Loyalty apps that track health metrics foster repeat stays and advocacy, deepening penetration of solos in the Europe wellness tourism market.

By Age Group: Millennials Dominate While Gen Z Shows Highest Growth Potential

Millennials held a 31.62% stake in the Europe wellness tourism market share during 2025. They value experiential travel and data-driven wellness assessments such as sleep scoring and metabolic testing. Operators deploy wearable integrations and personalized nutrition dashboards to satisfy this cohort. Gamified fitness challenges and community impact projects further reinforce engagement, keeping millennial participation high.

Gen Z bookings accelerate at 8.92% CAGR, propelled by price-sensitive yet purpose-driven preferences. Wallet-friendly hostels with meditation pods, forest classroom workshops, and vegetarian pop-ups resonate with their search for authenticity and environmental stewardship. Knowledge-rich social media storytelling amplifies reach. As a result, the Europe wellness tourism market size linked to Gen Z is expected to expand quickly, especially in countries with sizable youth populations such as France and Poland.

Digital Dominance and Curated Expertise: OTAs vs. Tour Operators in Europe's Wellness Tourism Market

OTAs accounted for 44.86% of bookings across the Europe wellness tourism market in 2025. Rich content libraries, instant confirmation, and peer reviews attract tech-savvy consumers. Meta-search and dynamic bundling features simplify comparison shopping, consolidating OTA influence. Loyalty tie-ins with global hotel groups further entrench their position.

Wellness tour operators expand at an 7.62% CAGR thanks to deep domain expertise and concierge-level personalization. They curate evidence-based programs supervised by medical professionals and source niche locations that OTAs rarely list. Partnerships with national tourism boards provide marketing grants, strengthening their digital footprints. This specialization underpins outsized gains within the Europe wellness tourism market.

Geography Analysis

Germany controlled 19.92% of the Europe wellness tourism market in 2025. State-supported rehabilitation resorts such as Bad Reichenhall blend clinical care with leisure, fostering high domestic repeat rates. Cross-border clients from Switzerland and Austria further lift demand. Competitive packages priced in Euro shield resorts from currency volatility, preserving Germany’s leadership.

Italy is charting a 8.55% CAGR for 2026-2031, boosted by thermal destinations in Tuscany, volcanic mud treatments on the islands, and UNESCO-listed cultural assets that elevate the holistic experience. Government incentives for rural hospitality upgrades extend supply beyond saturated city hubs. Social-media storytelling about slow living galvanizes younger travelers, lifting the Europe wellness tourism market size in Italy.

France, Spain, and the United Kingdom round out the top tier. France blends Thalassotherapy on the Atlantic coast with Alpine spa resorts, attracting both medical-wellness and leisure clients. Spain leverages year-round sun, making Andalusian yoga resorts popular shoulder-season escapes. The United Kingdom capitalizes on heritage bath sites in Bath and Harrogate while integrating modern mindfulness in countryside estates.

BENELUX and NORDIC clusters enrich regional variety. Dutch forest lodges feature cold-water immersion, while Finnish resorts promote nature-based wellbeing aligned with the national concept of “sisu.” Denmark and Sweden pioneer climate-positive spa construction, shaping best practices that ripple across the broader Europe wellness tourism market.

Competitive Landscape

Market concentration is moderate: Accor, Hilton, Marriott, InterContinental Hotels Group, and Hyatt collectively held just over 40% of 2024 revenue. These chains deploy multi-brand strategies to address premium, upscale, and mid-scale tiers, embedding spa, fitness, and nutrition modules across portfolios. Accor’s Handwritten Collection lets independent hotels access global distribution while retaining local identity, expanding wellness capacity in secondary cities.

Regional specialists such as Lanserhof Group, Therme Group, and Lefay Resorts carve demand through signature medical protocols and eco-architecture. Their clinical credibility and sustainability records command high average daily rates, pushing innovation in longevity diagnostics and regenerative design. Small and medium-sized enterprises account for the majority of operators, fostering a diverse supplier base across the Europe wellness tourism market.

Technology is an emerging differentiator. Chain hotels use AI-driven personalization engines to match treatments with biometric data. Digital wallets streamline cashless spa payments, and virtual-reality mindfulness sessions enhance pre-arrival engagement. The European Commission’s tourism platform encourages digital adoption, supplying SMEs with toolkits and funding pointers. As these initiatives scale, competitiveness across the Europe wellness tourism market intensifies further.

Europe Wellness Tourism Industry Leaders

Accor S.A.

Hilton Worldwide

Marriott International

InterContinental Hotels Group

Hyatt Hotels (inc. Miraval)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Accor confirmed expansion of its Handwritten Collection in Europe, enrolling Rocca a Mare Heraklion in Greece to target travelers seeking authentic wellness stays.

- February 2025: Marriott International opened three wellness-centric hotels in Europe, each featuring advanced spa facilities, functional fitness zones, and farm-to-table menus.

- October 2024: European Wellness Biomedical Group inaugurated the European Wellness Premier Center in Kota Kinabalu, offering more than 60 specialized therapies and targeting global clientele.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe wellness tourism market as the gross revenue earned inside the EEA, the United Kingdom, and Switzerland by wellness-focused resorts, thermal and thalasso clinics, yoga or mindfulness retreat centers, and specialist tour operators that sell multi-day wellness packages to travelers whose main trip purpose is physical or mental rejuvenation. According to Mordor Intelligence, this market is valued at USD 3.49 billion in 2025.

We exclude day-spa visits by local residents, beauty salons, routine hotel-spa add-ons, gym memberships, and spending by tourists whose primary purpose is not wellness.

Segmentation Overview

- By Service Type

- Inbound Services (Spa, Therapy, Yoga, etc.)

- Outbound Travel Packages

- By Traveler Demographic

- Solo Travelers

- Couples

- Groups / Corporate Retreats

- Seniors

- By Age Group

- Gen Z (18-24)

- Millennials (25-40)

- Gen X (41-56)

- Seniors (57+)

- By Channel of Booking

- Direct (Resort/Center Website)

- Online Travel Agencies (OTAs)

- Wellness Tour Operators

- By Geography

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with spa-resort directors in Germany and Italy, product heads at online wellness travel agencies, and officials from various tourism ministries. These conversations confirmed price bands, capacity utilization, traveler demographics, and post-pandemic demand swings across domestic and international cohorts.

Desk Research

Our team began with public datasets such as Eurostat overnight-stay statistics, UNWTO inbound arrival tables, the European Spa Association facility census, Global Wellness Institute wellness-expenditure benchmarks, and national Tourism Satellite Accounts, which anchor traveler volumes and spend rates. Company filings, investor decks, and curated news via Dow Jones Factiva and D&B Hoovers then refined operator counts, average package prices, and seasonality. Further color was drawn from cross-border healthcare policy papers and thermal therapy patent trends captured through Questel. The sources named are illustrative; many additional portals and databases were reviewed to verify and enrich the model.

Market-Sizing & Forecasting

We apply a top-down traveler-flow model that multiplies wellness-purpose arrival counts by validated package values, then cross-check with bottom-up samples from twenty providers' revenue disclosures and OTA booking volumes. Key variables include disposable income per capita, Google search interest in "wellness retreats," short-haul airline seat capacity, aging population ratios, and spa room occupancy. A multivariate regression on these indicators drives the 2025-2030 forecast; scenario overlays adjust for energy price shocks and visa policy changes. Gaps in operator data are bridged with weighted averages from the nearest peer group.

Data Validation & Update Cycle

Outputs pass double-blind analyst review, variance checks against WTTC spending indices, and expert re-contact when anomalies exceed five percent. We refresh models each year, with interim updates triggered by any driver moving fifteen percent or more.

Why Mordor's Europe Wellness Tourism Baseline Commands Reliability

Published figures often diverge because firms blend different spending buckets, traveler intents, and update cadences, which is why our traveler purpose filter and package revenue lens produce a tighter, decision-ready baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.49 B (2025) | Mordor Intelligence | - |

| USD 294.3 B (2022) | Global Consultancy A | Includes all lodging, F&B, and retail spend from any tourist who undertakes a single wellness activity |

| USD 298.6 B (2024) | Regional Consultancy B | Derives value from regional share assumptions and counts resident day-spa spending |

| USD 286.5 B (2023) | Industry Association C | Combines primary and secondary wellness motives without isolating package revenue |

The comparison shows that when scope is narrowed to revenue directly controlled by specialized wellness travel providers, Mordor Intelligence offers the most transparent and repeatable baseline for strategic planning.

Key Questions Answered in the Report

What is the current value of the Europe wellness tourism market?

The market stands at USD 3.65 billion in 2026 and is on course to reach USD 4.56 billion by 2031.

Which service type generates the highest revenue in European wellness tourism?

Inbound services such as spa treatments and yoga retreats hold 65.90% of 2025 revenue, the largest share within the market.

Which traveler segment is growing fastest?

Solo travelers are expanding at a 7.05% CAGR through 2031, driven by increased acceptance of independent travel and wellness-focused empowerment programs.

Why is Italy forecast to grow faster than other European wellness destinations?

Thermal resources, cultural heritage, and targeted rural-hospitality incentives support Italy’s projected 8.55% CAGR between 2026-2031.

How are hotel groups enhancing competitiveness in wellness offerings?

Leading chains integrate advanced spas, digital personalization tools, and sustainability initiatives, while independent resorts focus on specialized medical protocols and eco-architecture.

What role does the European Union play in wellness tourism growth?

The EU provides strategic policy guidance, funding, and digital toolkits that encourage greener, more resilient, and data-driven wellness tourism operations across member states.

Page last updated on: