Europe Amusement Park Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 27.09 Billion |

| Market Size (2026) | USD 28.33 Billion |

| Market Size (2031) | USD 35.47 Billion |

| Growth Rate (2026 - 2031) | 4.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Amusement Park Market Analysis by Mordor Intelligence

The Europe amusement park market size is expected to grow from USD 27.09 billion in 2025 to USD 28.33 billion in 2026 and is forecast to reach USD 35.47 billion by 2031 at 4.58% CAGR over 2026-2031. Recovery momentum reflects higher household leisure budgets, the steady return of long-haul tourists, and park operators’ rapid embrace of immersive intellectual-property (IP) theming that commands premium pricing [1]Themed Entertainment Association & AECOM, “Theme Index 2023,” aecom.com. . E-ticketing, AI-based queue management, and 5G-enabled interactive content are further raising per-capita spending while lowering crowd-flow bottlenecks, allowing the Europe amusement park market to grow without proportionate capacity additions. Mechanical rides still headline marketing campaigns, but operators are expanding water attractions, themed hotels, and indoor “retail-tainment” micro-parks to hedge weather risk and seasonality. Competitive intensity is moderate: the top five groups control roughly 60% revenue, yet expansion by Universal in the United Kingdom and Disney in France is set to raise capital requirements and favor scale players. Regulatory costs tied to carbon reduction and insurance premiums remain headwinds, but the Europe amusement park market continues to benefit from experiential tourism, dynamic pricing systems, and multi-day destination strategies that diversify revenue.

Key Report Takeaways

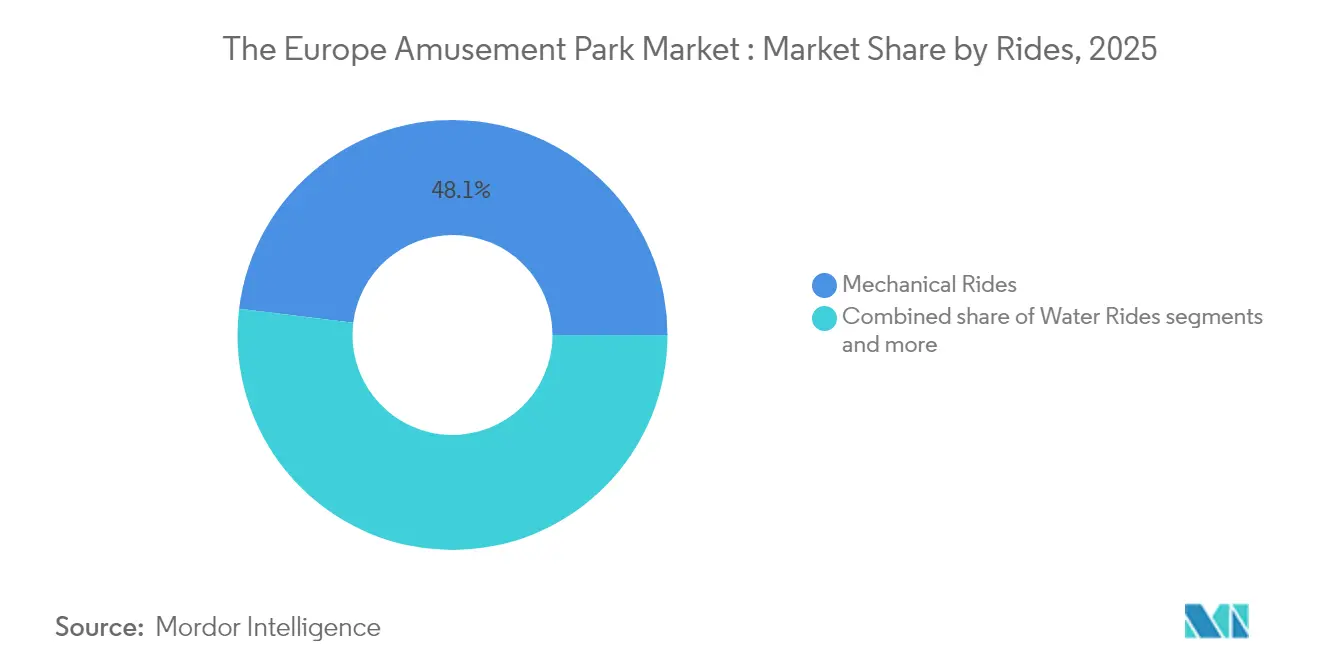

- By rides, mechanical attractions led with 48.05% of Europe amusement park market share in 2025, water attractions are projected to advance at a 7.12% CAGR through 2031.

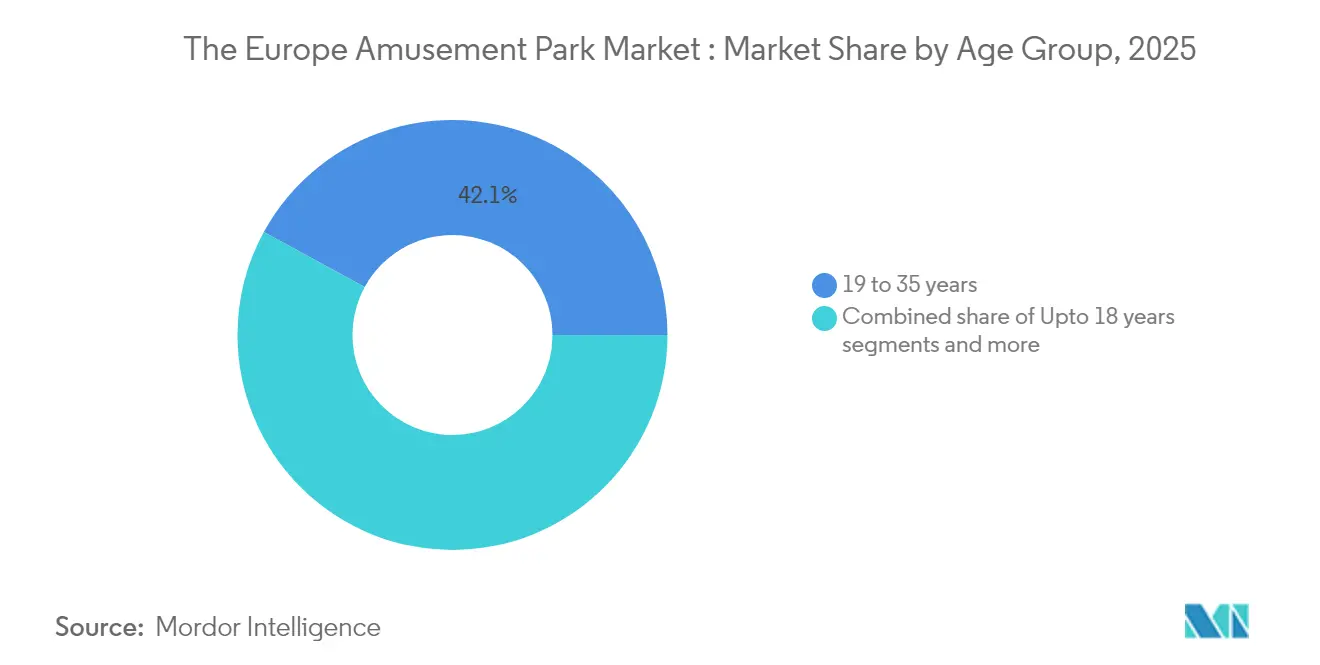

- By age group, visitors aged 19-35 years held 42.05% of Europe amusement park market size in 2025 and the up-to-18 segment is forecast to grow at a 6.74% CAGR to 2031.

- By revenue source, tickets captured 54.85% of Europe amusement park market share in 2025 and hotels and resorts are poised to post a 9.98% CAGR over the same period.

- By country, Germany accounted for 17.29% of Europe amusement park market share; Spain is expected to expand at a 6.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe contributes to a system defined not by any single geography but by the interaction of many. The global amusement parks market data by Mordor Intelligence represents that combined structure.

Europe Amusement Park Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in experiential tourism | +1.2% | Western Europe core, Mediterranean spillover | Medium term (2–4 years) |

| Increasing integration of IP-based attractions | +0.9% | United Kingdom, France, Germany | Long term (≥ 4 years) |

| Advancements in ride-safety technology | +0.6% | EU-wide, Nordic leadership | Short term (≤ 2 years) |

| Growing adoption of dynamic pricing systems | +0.8% | Western Europe, selective Eastern Europe | Medium term (2–4 years) |

| Rise of hybrid retail-tainment park formats | +0.4% | Urban centers, mall-integrated venues | Long term (≥ 4 years) |

| Deployment of 5G/edge-enabled experiences | +0.3% | Nordic and DACH early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Experiential Tourism

A sharp consumer pivot toward experience-over-possession spending has lifted attendance, with guests paying higher prices for immersive storytelling and shareable attractions. Operators report per-capita spend rising faster than footfall as upgraded food, merchandising, and premium queue-skipping packages gain traction. Social-media reach amplifies word-of-mouth, particularly among 19–35-year-old visitors who generate viral content that markets parks at minimal cost. IP-driven expansions, such as Universal’s planned Bedford resort, underscore how the Europe amusement park market leverages experiential pull rather than ride count alone to attract travelers. The trend extends to older demographics, as baby boomers seek quality service and accessibility that make multigenerational trips appealing. Experiential differentiation is now central to pricing power, shielding operators from inflationary input costs. The driver is expected to sustain medium-term growth by reinforcing destination appeal and boosting average length of stay.

Increasing Integration of IP-Based Attractions

Licensing blockbuster franchises has moved from ornamentation to core strategy: Merlin Entertainments’ 2024 acquisition of global Minecraft rights illustrates how IP secures younger audiences and drives merchandise sales. Parques Reunidos’ Paramount partnerships demonstrate similar economics: branded universes yield higher ticket prices, longer dwell times, and cross-channel marketing efficiencies. Multi-year contracts also create content refresh cycles that maintain repeat visitation without full-scale ride replacements. As intellectual-property owners demand premium fees, only well-capitalized groups can compete, reinforcing moderate concentration within the Europe amusement park market. The long-term payoff includes lower promotional spend because brand equity comes built-in. IP theming also unlocks film-studio collaborations on seasonal events and streaming tie-ins that extend visitor engagement beyond park gates. Over the forecast period, IP integration will continue to widen the performance gap between tier-one parks and regional independents.

Growing Adoption of Dynamic Pricing & Revenue-Management Systems

Algorithmic pricing tools have matured into mission-critical infrastructure, as seen at Europa-Park, which blends weather, hotel occupancy, and historical booking data to calibrate ticket prices hourly [2]International Association of Amusement Parks and Attractions, “Leveraging Artificial Intelligence for Attractions,” iaapa.org. . Yield management raises weekday utilization while capping holiday crowding, improving both revenue and guest satisfaction. Parks gain visibility into demand elasticities that inform marketing spend and add-on bundling. Sustained adoption should lift the Europe amusement park market CAGR by 0.8 percentage points, primarily through higher average transaction values. The systems also support personalized offers that deepen loyalty-program engagement and spur incremental visitation. Revenue managers increasingly integrate ancillary streams such as parking, dining, and VR experiences into a single yield platform.

Deployment of 5G/Edge-Enabled Immersive Experiences

EU funding worth EUR 142 million (USD 152.65 million) is accelerating 5G and edge-cloud infrastructure, permitting real-time augmented-reality games and personalized ride content [3]Health and Digital Executive Agency, “5G and Edge Cloud for Smart Communities,” hadea.ec.europa.eu. . Early adopters can monetize premium AR overlays, in-app micro-transactions, and location-based storytelling that adapts to guest profiles. Low-latency networks enable synchronized group experiences, raising satisfaction scores and social-media exposure. Investment costs are falling as telcos co-finance deployments in return for data traffic and branding rights. The technology also supports advanced crowd analytics that optimize staffing and concession placement. Although network rollout is uneven, Nordic and DACH parks are positioned to set consumer expectations that ripple across the Europe amusement park market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX & long ROI cycles | -1.8% | EU-wide, acute in Eastern Europe | Long term (≥ 4 years) |

| Escalating liability-insurance premiums | -0.7% | Western Europe entertainment sector | Medium term (2–4 years) |

| Tightening environmental-impact regulations | -0.9% | EU Green Deal compliance regions | Long term (≥ 4 years) |

| Aging demographic in Western Europe | -0.5% | Western Europe, Nordic concentration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX & Long ROI Cycles

New gate parks require EUR 100–200 million (USD 107.5–215 million) and can take 7–10 years to recoup cash outlays, discouraging entrants and slowing expansion in Central and Eastern Europe where financing costs are higher. Even evergreen brands like Euro Disneyland originally struggled to meet debt covenants, illustrating structural capital risk. Large parks must fund infrastructure, utilities, and road connections that magnify payback horizons. Government incentives mitigate risk but add political complexity. Existing groups with diversified lodging and IP licensing revenues enjoy lower cost of capital, widening the gap with local independents. This barrier reinforces the moderate concentration already characterizing the Europe amusement park market. Over the long term, only projects backed by multinational operators or public-private partnerships are likely to break ground.

Escalating Liability-Insurance Premiums

The post-pandemic insurance market remains tight: entertainment premium rates rose 7.5–10% in early 2025, and umbrella coverage for high-intensity rides attracts high deductibles. Casualty lines have stabilized, yet specialized leisure policies lag, raising operating costs by up to 5% of revenue, with liability components consuming the bulk. Underwriters demand granular safety data, incentivizing adoption of predictive maintenance but also increasing compliance workloads. Smaller parks lacking robust incident logs pay disproportionate surcharges or face reduced coverage limits. Medium-term financial strain could accelerate M&A as independents seek economies of scale in insurance purchasing. Operators offset cost pressure through dynamic pricing, but margin compression remains a headwind for growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rides: Water Attractions Gain Momentum

Water attractions generated a 7.12% CAGR forecast well above the Europe amusement park industry average by leveraging climate-controlled facilities that extend seasonal windows and tap wellness tourism demand. Mechanical rides still accounted for 48.05% of Europe amusement park market share in 2025, anchoring park identities with signature coasters and drop towers. Yet indoor water complexes such as Therme Erding are demonstrating how spa-entertainment hybrids can boost dwell time and daily spend, yielding superior revenue per square meter. Mechanical ride designers now weave interactive elements and IP theming to maintain relevance against water-based competition. Specialty attractions, including VR-driven experiences, fill niche positioning but face frequent content-refresh costs. The expanding water segment diversifies guest profiles, drawing multigenerational families and wellness seekers who historically bypassed thrill-centric parks. Operators that bundle mechanical icons with indoor water offerings are positioned to capture a wider visitor mix and smooth revenue seasonality.

Guest surveys reveal that water attractions also achieve higher repeat visitation, aided by lower height restrictions that include younger children and older adults. Developers integrate surf lagoons and thermal pools into resort hotels, cross-selling spa treatments and night tickets. This bundling pushes average length of stay beyond two nights, further lifting Europe amusement park market size for resorts with water features. Mechanical rides will retain marketing spotlight, but their absolute share is expected to erode marginally as capital shifts toward versatile hybrid facilities. Investors now evaluate projects on resilience to weather volatility and demographic breadth, metrics where water parks score strongly. Strategic focus is therefore tilting toward experiential zones that combine slides, wave pools, and relaxation areas coupled with dining and retail micro-districts.

By Age Group: Under-18 Visits Accelerate

Visitors aged 19-35 captured 42.05% of 2025 spending, solidifying their status as the Europe amusement park market’s core group. However, the up-to-18 cohort is on track for a 6.74% CAGR through 2031, powered by parental preference for experiential gifts and rising school-trip demand. Millennial parents, now in their mid-30s, allocate leisure budgets to family travel that bonds generations and yields social-media content. Parks tailored with edutainment zones and age-specific IP from Peppa Pig to Minecraft are outperforming broad-brush attractions. Operators also introduce flexible ticket bundles that let caregivers combine toddler playlands with thrill-ride access for older siblings, creating holistic family value propositions.

Demography poses both opportunities and limits: Europe’s fertility rate fell to 1.38 births per woman in 2023, yet later parenthood means households possess higher discretionary funds once children reach park-going age . Parks respond by integrating stroller-friendly paths, sensory-sensitive experiences, and upgraded childcare facilities, enabling longer stays. Cross-generational design also appeals to grandparents who join family trips, subtly offsetting the aging-population restraint. Youth-centric digital engagement via gaming IP and AR scavenger hunts deepens loyalty that can last decades. Although 36-65 year-old segments deliver steady volumes, the fastest-growing under-18 visitor base anchors future demand curves and shapes ride investment pipelines toward gentle thrills and interactive play.

By Revenue Source: Lodging Lifts Margins

Tickets contributed 54.85% of 2025 revenue, underscoring their historical primacy, but hotels and resorts are forecast for a 9.98% CAGR the highest among all streams. Multi-day visitors typically spend 3–4 times more than day guests, making lodging expansion a key profit lever. Europa-Park’s six-hotel campus and PortAventura’s integrated resort model illustrate how on-site rooms can double average guest outlays while capturing in-park food, beverage, and merchandise sales. Dynamic packaging bundles tickets, meals, and themed events, boosting yield and smoothing occupancy across weekdays.

Food-and-beverage programs are evolving into immersive culinary shows aligned with park IP, commanding premium pricing. Merchandise revenue faces e-commerce competition, but exclusive park-only products and personalization technologies extend spending. Hotels also provide hedges against weather disruptions: visitors with prepaid packages are less likely to cancel. Operators channel profits into new attractions, reinforcing the Europe amusement park market growth loop. Over the forecast horizon, resort development will remain the strategic priority for groups seeking to diversify revenue beyond gate receipts and increase share-of-wallet.

Geography Analysis

Germany retained 17.29% of 2025 revenue, buoyed by central geography, robust domestic tourism, and flagship parks such as Europa-Park that pull cross-border visitors. Its regulatory stability and transport infrastructure further cement leadership. Spain, however, is the growth champion, projected at a 6.98% CAGR to 2031 as Mediterranean climate and aggressive resort investments transform it into a year-round destination. PortAventura’s three-park complex and forthcoming indoor water expansion exemplify Spain’s push toward multi-day stays that appeal to Northern Europeans craving winter sunshine.

France and the United Kingdom represent mature markets. France benefits from Disney’s EUR 2 billion (USD 2.15 billion) park overhaul that adds Frozen and Lion King lands, reinforcing Paris’s stature as Europe’s most visited tourist city. The United Kingdom anticipates Universal’s Bedford resort, which could recalibrate domestic tourism flows once operational. Italy maintains consistent performance via Gardaland and regional independents, while BENELUX and Nordic regions excel in per-capita spending thanks to high household incomes and premium pricing acceptance. Central and Eastern Europe remain under-penetrated; however, rising disposable income and EU funds for infrastructure hint at long-term upside if financing barriers ease.

The amusement parks market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for North America, Asia, and Middle East.

Competitive Landscape

The market shows moderate concentration, with Merlin Entertainments holding the leading position, followed by Parques Reunidos. Other key players include Compagnie des Alpes, along with the Disney and Universal divisions that each operate single-brand resorts. Consolidation trends favor companies with access to intellectual property, data analytics, and diversified lodging portfolios, as rising guest expectations for seamless, omnichannel experiences increase capital expenditure requirements. Recent investments, such as Universal’s planned resort in Bedford and Disney’s reinvestment in Paris, reflect growing competition for the international tourist’s share-of-wallet. Meanwhile, Compagnie des Alpes has strengthened its position in Germany with the acquisition of Belantis, while Parques Reunidos is shifting capital toward IP-rich attractions.

Merlin’s licensing of the Minecraft brand highlights a broader strategy to attract younger, digitally native audiences through globally recognized gaming franchises. Technology has become a key differentiator for market leaders, with tools like AI-driven queue management, cashless ecosystems, and augmented reality experiences improving guest satisfaction and enabling personalized upselling. Additionally, rising insurance costs highlight the value of scale, as larger operators secure better group policies and more favorable premiums. In contrast, start-ups are carving out niches with urban micro-parks like UNO Parks’ indoor adventure centers, which require less capital and allow for rapid content rotation. These developments suggest a diverse range of growth strategies across the competitive landscape.

Despite these shifts, competitive barriers remain moderate, allowing regional independents to maintain strong local followings through culturally relevant themes and deep community ties. However, from 2025 to 2030, mergers and acquisitions are expected to accelerate as fragmented players seek strategic partnerships. These collaborations will likely be aimed at financing technological upgrades and mitigating the rising costs associated with regulatory compliance. As the market evolves, access to IP, technological capabilities, and operational scale will increasingly determine competitive advantage. Overall, the sector is poised for dynamic transformation driven by both innovation and consolidation.

Europe Amusement Park Industry Leaders

Merlin Entertainments

Parques Reunidos

Compagnie des Alpes

Europa-Park GmbH & Co Mack KG

Looping Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Universal Destinations & Experiences confirmed a multi-billion-pound resort near Bedford, UK, slated to open in 2031.

- April 2025: Compagnie des Alpes acquired Germany’s Belantis theme park for EUR 22 million (USD 23.65 million), bolstering its DACH presence.

- April 2025: Imagi Park inaugurated a 13,400 m² indoor complex at Val d’Europe, projecting 800,000 annual visitors.

- April 2025: Walibi Holland debuted YOY, Europe’s tallest duelling single-rail coasters, reinforcing its thrill-ride credentials.

Europe Amusement Park Market Report Scope

An amusement park is a place that has many games and rides (such as roller coasters and merry-go-rounds) for entertainment. This report aims to provide a detailed analysis of the European amusement park market. It focuses on the market dynamics, emerging trends in the segments and regional markets, and insights into the various product and application types. Also, it analyzes the key players and the competitive landscape.

The European amusement parks market is segmented by rides, age, revenue source, and country. By rides, the market is sub-segmented by mechanical rides, water rides, and other rides. By age, the market is sub-segmented by up to 18 years, 19 to 35 years, 36 to 50 years, 51 to 65 years, and more than 65 years. By revenue source, the market is sub-segmented by tickets, food & beverages, merchandise, hotels/resorts, and others, and by the country, the market is sub-segmented by the United Kingdom, Germany, France, and the rest of Europe. The report offers market size and forecasts in value (USD) for all the above segments.

| Mechanical Rides |

| Water Rides |

| Other Rides |

| Upto 18 years |

| 19 to 35 years |

| 36 to 50 years |

| 51 to 65 years |

| More than 65 years |

| Tickets |

| Food & Beverages |

| Merchandise |

| Hotels/Resorts |

| Others |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Rides | Mechanical Rides |

| Water Rides | |

| Other Rides | |

| By Age | Upto 18 years |

| 19 to 35 years | |

| 36 to 50 years | |

| 51 to 65 years | |

| More than 65 years | |

| By Revenue Source | Tickets |

| Food & Beverages | |

| Merchandise | |

| Hotels/Resorts | |

| Others | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe amusement park market in 2026?

It stands at USD 28.33 billion, reflecting steady recovery after pandemic headwinds.

How fast will the market grow through 2031?

The forecast CAGR is 4.58%, taking revenue to USD 35.47 billion by 2031.

Which ride category is expanding the quickest?

Water attractions lead with a 7.12% CAGR thanks to climate-controlled indoor developments.

Why are hotels and resorts critical for operators?

Lodging lifts per-guest outlays as multi-day stays can generate three to four times the spend of day visits.

Which country offers the fastest growth outlook?

Spain is projected to advance at a 6.98% CAGR, underpinned by Mediterranean climate and integrated resorts.

Page last updated on: