United States Camping And Caravanning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

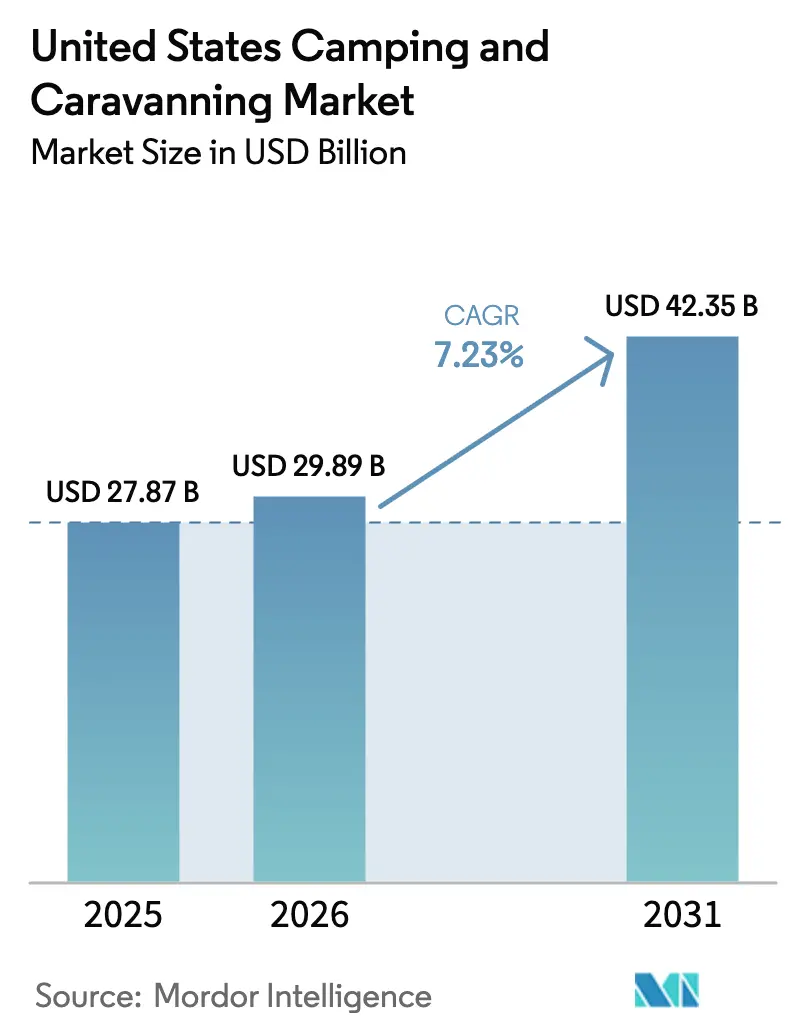

| Base Year Market Size (2025) | USD 27.87 Billion |

| Market Size (2026) | USD 29.89 Billion |

| Market Size (2031) | USD 42.35 Billion |

| Growth Rate (2026 - 2031) | 7.23% CAGR |

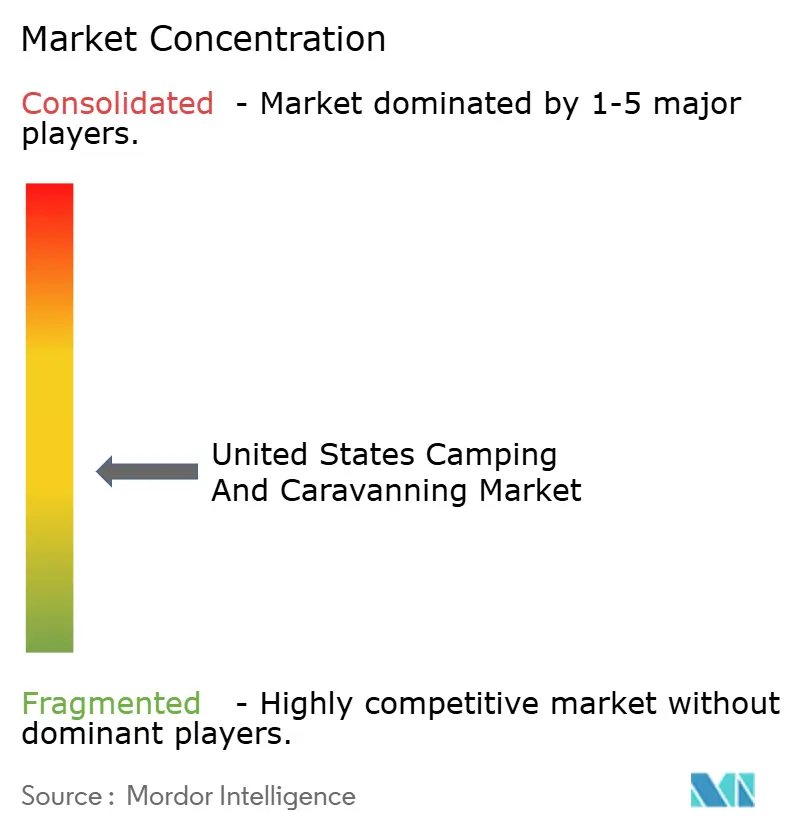

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Camping And Caravanning Market Analysis by Mordor Intelligence

The United States camping and caravanning market size is expected to grow from USD 27.87 billion in 2025 to USD 29.89 billion in 2026 and is forecast to reach USD 42.35 billion by 2031 at 7.23% CAGR over 2026-2031. The United States camping and caravanning market continues to benefit from a structural upturn in outdoor‐recreation demand, as 11 million additional households have adopted camping lifestyles compared with 2019 baselines [1]Kampgrounds of America, “Top Camping & Travel Trends for 2025,” koa.com . Public and private investments, such as Alabama's initiative to revamp state parks and KOA's deployment of EV-charging infrastructure across 28 properties, underscore a long-term strategic commitment to the U.S. camping and caravanning market. These investments highlight efforts to enhance infrastructure, expand capacity, and improve customer experiences, reflecting a positive growth outlook for the market. Furthermore, the integration of advanced technologies, including AI-powered revenue management systems and mobile self-check-in kiosks, is enabling businesses to optimize operational efficiency, reduce costs, and strengthen customer retention. These technological advancements are playing a critical role in driving profitability and fostering loyalty across the industry ecosystem.

Key Report Takeaways

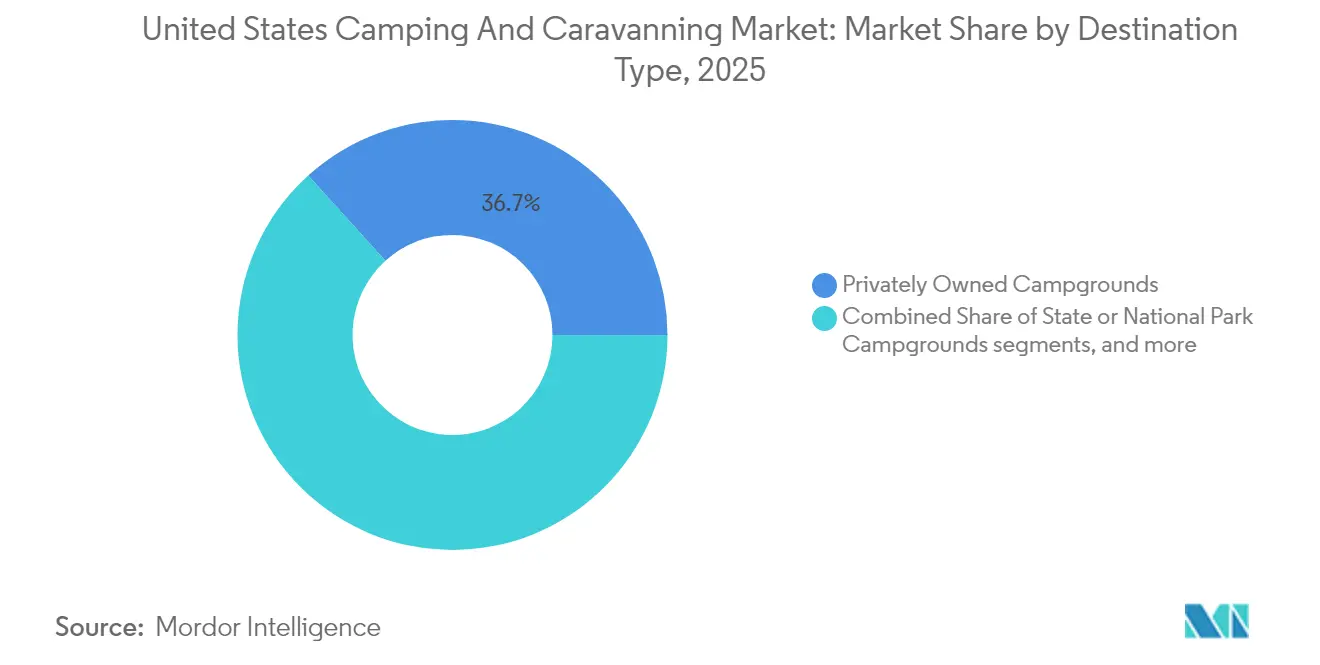

- By destination type, privately owned campgrounds held 36.71% of the United States camping and caravanning market share in 2025, whereas backcountry and wilderness areas are forecast to achieve a 9.21% CAGR to 2031.

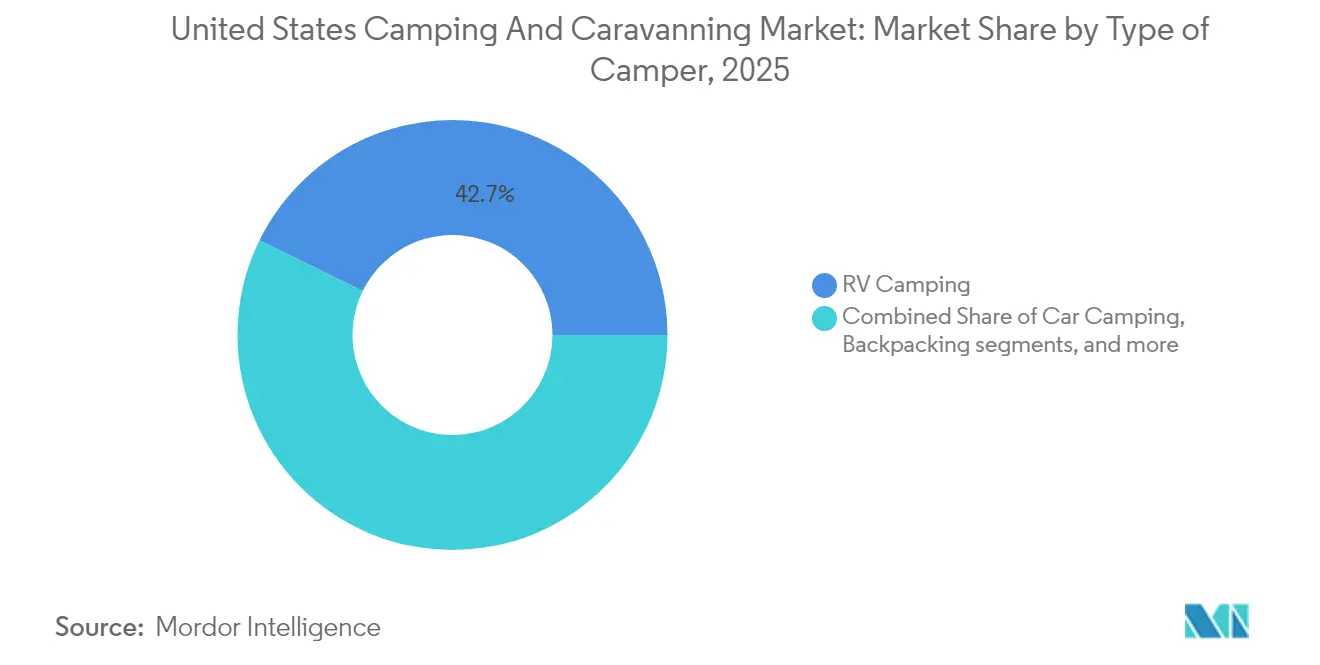

- By type of camper, RV camping contributed 42.74% of the United States camping and caravanning market in 2025 revenue, while backpacking is positioned for an 8.62% CAGR through 2031.

- By distribution channel, direct sales captured 55.62% of the United States camping and caravanning market in 2025 bookings, yet online travel agencies are projected to deliver a 11.58% CAGR during the forecast horizon.

- The South generated 33.84% of the United States camping and caravanning market of the 2025 revenue, but the West is slated for the fastest 7.84% CAGR owing to national park proximity and adventure tourism depth.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Americas representing one of the more structurally developed among them. The global report on camping and caravanning market by Mordor Intelligence reflects how these regional layers combine into a single system.

United States Camping And Caravanning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic outdoor recreation boom | +1.2% | National; gains largest in South and West | Medium term (2-4 years) |

| Surging RV ownership among millennials & Gen Z | +1.8% | Nationwide, concentrated in suburban metros | Long term (≥ 4 years) |

| Infrastructure upgrades in state-park campgrounds | +1.5% | Kentucky, Alabama, Oregon, Texas | Medium term (2-4 years) |

| Work-from-anywhere lifestyle fuelling van-life stays | +0.9% | National; early adoption across Western corridors | Short term (≤ 2 years) |

| Private-equity roll-ups are professionalizing campground chains | +1.1% | Destination hot spots, including coastal Florida and mountain Utah | Long term (≥ 4 years) |

| AI-powered dynamic pricing tools are boosting site utilization | +0.8% | Large multistate operators and franchise systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Post-Pandemic Outdoor Recreation Boom Drives Mainstream Adoption

Outdoor recreation added USD 639.5 billion to the U.S. gross domestic product in 2024, with RV-related activities alone delivering USD 26.3 billion in direct value [3]Go RVing, “Outdoor Recreation Economic Impact,” gorving.com . The United States reported 175.8 million participants in camping and caravanning activities, underscoring the market's role as a vital and growing segment within the nation's leisure spending landscape. This participation level reflects the increasing consumer preference for outdoor recreational activities, driven by factors such as rising disposable incomes, a growing emphasis on wellness, and the appeal of nature-based experiences. This surge transcends income brackets because state parks, gear-rental programs, and discounted public-land passes have lowered access barriers. Annual direct spending tied to camping now totals USD 61 billion and cycles through fuel stations, convenience stores, outfitting shops, and guide services, reinforcing community economic resilience.

Millennial and Generation Z RV Ownership Transforms Market Demographics

First-time RV buyers represent 36% of sales as rental trials via peer-to-peer platforms convert renters into owners [2]RV Industry Association, “2025 Ownership and Demographic Study,” rvia.org . Younger buyers prefer nimble campervans, hybrid pop-ups, and Class B rigs that fit into urban parking dimensions and plug into standard household outlets, redefining product portfolios among leading manufacturers. Social-connectivity requirements push campground operators to upgrade to fibre internet, individual Wi-Fi mesh nodes, and smart-lock shower facilities that guests can reserve in-app. Visual storytelling on Instagram and TikTok elevates the demand for photogenic communal spaces, mural walls, and star-gazing decks, an evolution that keeps the United States camping and caravanning market aligned with broader experience-economy trends. Additionally, the incorporation of remote-work amenities, covered cowork patios, ergonomic seating, and multi-device charging stations converts transient stays into week-long residencies that smooth mid-week demand volatility.

State-Park Infrastructure Modernization Catalyzes Capacity Expansion

The state of Alabama allocated USD 150 million through a bond issuance to enhance infrastructure within its parks. This funding was directed toward upgrading electrical systems to 50-amp capacity, modernizing bathhouse facilities, and constructing ADA-compliant ramps. These improvements have significantly increased the availability of reservable pads, thereby enhancing accessibility and user experience across the park system. Kentucky has allocated USD 40 million to expand sites designed to accommodate fifth wheels, reflecting a strategic investment in outdoor tourism. This decision highlights a bipartisan understanding of the sector's economic impact, particularly its ability to drive growth in local retail and dining industries through increased visitor spending and related activities. Such investments shrink peak-season waitlists, raise visitor satisfaction, and elevate occupancy ceilings. These capital flows hardwire scalability into the United States camping and caravanning market.

Work-From-Anywhere Culture Enables Extended-Stay Demand

The digital-nomad population swelled to 17 million in 2024, a 131% gain since 2019, driving month-long stay requests that conventional hotels rarely satisfy. Operators that integrated advanced features such as gigabit-speed internet, shaded desk pods, and privacy-screen-equipped meeting rooms demonstrated a notable increase in shoulder-season occupancy rates. This performance highlights the competitive advantage provided by enhanced amenities in attracting and retaining clients during off-peak periods, compared to operators that do not offer similar facilities. Longer stays translate into recurring ancillary purchases, propane refills, kayak rentals, pet daycare, and reduce guest acquisition cost because fewer check-ins are required to fill calendars. Rigs outfitted with solar arrays and lithium batteries dovetail with campground microgrids, slicing generator noise pollution and aligning with Leave-No-Trace ethics that younger travellers champion. Municipalities recognizing this economic upside are carving out extended-stay zoning overlays, thereby directly shaping the growth arcs inside the United States camping and caravanning market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising land and insurance costs | -1.4% | Coastal Carolinas, Sierra Nevada, Rockies | Long term (≥ 4 years) |

| Stringent zoning regulations | -0.7% | Suburban fringes of Atlanta, Denver, and Austin | Long term (≥ 4 years) |

| Growing wildfire frequency | -0.5% | California, Oregon, Washington | Medium term (2-4 years) |

| Short-term rental legislation spills over to RV sites | -0.3% | Resort towns such as Sedona and Asheville | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Operational Costs Pressure Campground Margins

Property-insurance premiums rose at double-digit clips through 2024 as carriers recalibrated actuarial models to inflation, supply-chain volatility, and weather extremes. Premium escalation squeezes small-park operators lacking multi-property risk pools, driving some to divest at valuations favourable to larger chains. Land values in coastal and mountain corridors have climbed faster than national farmland averages, lifting carrying costs and lengthening payback periods. Tight labour markets compel operators to offer on-site staff housing, tuition subsidies, or retention bonuses, inflating payroll expense structures. These cost vectors collectively erode margins, tempering the expansion pace within the United States camping and caravanning market.

Wildfire Frequency Restricts Access to Premium Destinations

The 2024 fire season forced full or partial shutdowns at Mount Rainier, Death Valley, and Sequoia & Kings Canyon national parks. Even unaffected private parks experienced cancellations due to poor air quality or travel advisories. State-mandated defensible-space clearances require costly tree thinning and brush removal, straining capital budgets. Rising deductibles and exclusions for fire peril drive insurance underwriters to demand higher premium deposits or impose acreage caps, pushing some operators to self-insure portions of risk. The geographic concentration of wildfires in high-value scenic corridors amplifies revenue volatility across the United States camping and caravanning market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Destination Type: Private Operators Dominate While Wilderness Segments Accelerate

Privately owned campgrounds generated 36.71% of 2025 revenue, underscoring the United States camping and caravanning market size advantage enjoyed by agile operators capable of rapid amenity refreshes and dynamic pricing pivots. Their independence from legislative budget cycles enables quicker adoption of resort-style upgrades such as lazy-river pools, dog parks, and rentable Airstreams. Data-driven membership programs nurture loyalty and fill mid-week gaps, supporting year-round labour retention.

Backcountry and wilderness areas are slated for a 9.21% CAGR through 2031, propelled by experiential travel motivations and widespread social-media amplification. Public-land agencies monetize demand via campsite fees funnelled into trail maintenance, while outfitters provide gear rentals and guided treks to newcomers seeking safety in remote terrains. Limited overnight capacity safeguards ecological integrity, unintentionally preserving premium pricing leverage within this niche of the United States camping and caravanning market. Other destination categories, parking-lot boondocking, private-land marketplaces like Hipcamp, and harvest-host farm stays, fit overflow demand scenarios and specialized tastes. Their permissive cost structures foster entrepreneurial experimentation, from pop-up movie nights to gourmet-food-truck rallies, adding cultural diversity to supply options.

By Type of Camper: RV Dominance Persists Despite Backpacking Acceleration

RV camping captured 42.74% of 2025 spend, a testament to mature service infrastructure that includes 24/7 roadside assistance, abundant waste-dump stations, and parts inventories. Electrified models such as Winnebago’s eRV2 prototype promise near-silent campsite operation and reduced carbon footprints, satisfying eco-conscious families eager for comfort and sustainability parity. High residual values reinforce buyer confidence and bolster financing availability, further entrenching RV leadership inside the United States camping and caravanning market.

Backpacking’s projected 8.62% CAGR aligns with younger consumers’ minimalism and quest for authenticity. Ultralight tents, subscription gear boxes, and GPS-enabled safety beacons lower entry barriers, while digital route-planning tools demystify multi-day itineraries. Retailers organize intro workshops that channel new participants into guided tours, cultivating a pipeline of repeat customers. Car camping and glamping formats occupy the middle ground; they lure style-seeking travellers who want real mattresses and climate control but eschew towing responsibilities. Marriott’s 2024 acquisition of Postcard Cabins validates mainstream appetite for hybrid outdoor accommodations.

By Distribution Channel: Digital Transformation Accelerates Despite Direct Sales Dominance

Direct reservations retained 55.62% of 2025 bookings, highlighting the enduring magnetism of brand websites that cater to loyalists through tiered reward points and site-preference memory. Operators exploit owned channels to bundle firewood delivery, linen rental, and late checkout, raising per-booking revenue. APIs integrate real-time availability with corporate travel systems, enabling companies to stage off-site retreats in nature yet preserve compliance audit trails.

Online travel agencies are forecast to post a 11.58% CAGR as generation-native app users prize frictionless booking. Aggregators rank sites by verified guest reviews, photo quality, and amenity filters, speeding decision cycles for novice campers uncomfortable navigating disparate owner websites. Some campgrounds deploy differential pricing, advertised rate parity during low seasons, and premium markup during holidays, to balance OTA visibility and commission costs. By 2030, predictive meta-search engines could auto-assemble full itineraries combining RV rentals, campground stays, and activity tickets, expanding transactional scope across the United States camping and caravanning market.

Geography Analysis

The South contributed 33.84% of 2025 revenue on the back of mild winters, extensive interstate networks, and a tradition of snowbird migration. States like Florida and Texas layer campground amenities onto broader tourism draws, encouraging dual-purpose trips that mix beach leisure with inland nature stays. Competitive dynamics revolve around upselling boat slips, fishing charters, and coastal ecotour packages, weaving multi-day itineraries that prolong visitor spend.

The West is set for an 7.84% CAGR through 2031, leveraging unparalleled national-park clusters and a deep-rooted adventure ethos. Yet volatility is baked in: wildfire smoke, mudslide-triggered road closures, and drought-driven water restrictions all loom as operational contingencies. Infrastructure projects like Love’s Travel Stops’ NEVI-funded charging corridors are mitigating range anxiety for electric RV travelers, broadening demand channels. The Northeast and Midwest wield dense resident populations within a day’s drive, enabling weekend getaways that fill Friday-to-Sunday septets. Fall foliage, maple-syrup festivals, and lake-focused recreation anchor seasonal peaks. Operators test insulated safari tents and geothermal bathhouses to lengthen usage windows into late November. While capital intensity is higher due to heating and snow-load engineering, revenue diversification through winterized cabins buffers off-season drop-offs.

Mordor Intelligence provides coverage of the camping and caravanning market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The camping and caravanning market in the United States is characterized by moderate fragmentation, with the top five operators collectively contributing one-fourth of the total revenue. Kampgrounds of America (KOA) operates a portfolio comprising 432 franchise parks and 51 corporate-owned parks. The corporate-owned parks generate an average revenue of USD 14,200 per pad, significantly outperforming the franchise units, which average USD 6,600 per pad. This disparity underscores the financial advantages and growth potential associated with direct ownership within the market. Sun Outdoors leverages multi-season resorts featuring water parks and pickleball stadiums, while Thousand Trails employs an annual pass model granting access to more than 80 resorts, securing recurring cash flow.

Private-equity firms, such as DLP Capital, are strategically consolidating parks into geographically diversified portfolios to achieve operational efficiencies. By streamlining procurement processes and deploying centralized reservation systems, these firms are leveraging economies of scale to enhance profitability. Concurrently, technology vendors are introducing turnkey solutions that integrate advanced features, including dynamic pricing mechanisms, gate security systems, and guest-experience applications, to modernize operations and improve customer satisfaction. Operators lacking the resources to adopt such modernization strategies face the risk of being relegated to lower-tier market segments, which could result in compressed pricing power and diminished occupancy rates.

Hipcamp, recognized for its platform that consolidates private-land campsites, and Outdoorsy, which has significantly enhanced its lifetime transaction value by integrating offerings such as insurance, trip-planning content, and campground booking widgets, are emerging as prominent disruptors in the market. These companies are strategically leveraging digital platforms to engage with tech-savvy consumers while fostering the development of untapped demand segments. Additionally, substantial growth opportunities exist in underexplored areas, including EV-charging services, premium glamping accommodations featuring en-suite bathrooms, and extended-stay coworking villages. These niches provide viable entry points for new players, even as established competitors continue to expand their market presence.

United States Camping And Caravanning Industry Leaders

Kampgrounds of America (KOA)

Thousand Trails (Equity LifeStyle Properties)

Sun Outdoors (Sun Communities)

Hipcamp

Jellystone Park

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Highway West Vacations, a leading operator in the hospitality sector, has acquired three California properties: Avila Pismo RV Resort & Campground, Costanoa, and Lake Siskiyou Camp Resort. This acquisition strengthens its presence in Northern California and expands its footprint in Central California.

- January 2025: Kampgrounds of America (KOA) plans to expand its Nashville KOA Resort through a merger with the Nashville RV Resort and Cabins. Set for completion by early 2025, the expansion will add 200 RV sites, 16 Deluxe Cabins, four rustic cabins, and 18 tent sites, increasing capacity to 536 sites to meet growing visitor demand.

- December 2024: Marriott International detailed plans for a nature-focused hotel collection targeting 2026 openings across U.S. gateway regions. Marriott International detailed plans for a nature-focused hotel collection targeting 2026 openings across U.S. gateway regions.

- December 2024: Marriott International, Inc. acquired Postcard Cabins, formerly Getaway, adding 1,200 cabins across 29 locations to its Bonvoy redemption catalog, enhancing its portfolio and redefining outdoor experiences by fostering meaningful connections with nature.

United States Camping And Caravanning Market Report Scope

Camping and caravanning are outdoor recreational activities that involve traveling and staying in tents or recreational vehicles (RVs) or caravans. These activities allow people to explore and experience the great outdoors, often in natural settings such as national parks, forests, beaches, and mountains. Both camping and caravanning offer a range of benefits, including the opportunity to connect with nature, escape from the stresses of daily life, and spend quality time with family and friends. They also provide a flexible and cost-effective travel method, with many camping and RV parks offering affordable accommodations and amenities.

The US Camping and Caravanning Market is segmented by destination type (state or national park campgrounds, privately owned campgrounds, public or privately owned land other than a campground, backcountry, national forest or wilderness areas, parking lots, and others), type of camper (car camping, RV camping, backpacking, and others), and distribution channel (direct sales, online travel agencies, and traditional travel agencies). The report offers Market size and forecasts for US Camping And Caravanning Market in value (USD) for all the above segments.

| State or National Park Campgrounds |

| Privately Owned Campgrounds |

| Public or Privately Owned Land Other Than a Campground |

| Backcountry, National Forest or Wilderness Areas |

| Parking Lots |

| Others |

| Car Camping |

| RV Camping |

| Backpacking |

| Others |

| Direct Sales |

| Online Travel Agencies |

| Traditional Travel Agencies |

| Northeast |

| Midwest |

| South |

| West |

| By Destination Type | State or National Park Campgrounds |

| Privately Owned Campgrounds | |

| Public or Privately Owned Land Other Than a Campground | |

| Backcountry, National Forest or Wilderness Areas | |

| Parking Lots | |

| Others | |

| By Type of Camper | Car Camping |

| RV Camping | |

| Backpacking | |

| Others | |

| By Distribution Channel | Direct Sales |

| Online Travel Agencies | |

| Traditional Travel Agencies | |

| By Geography | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

How big is the United States camping and caravanning market in 2026?

The United States camping and caravanning market size stands at USD 29.89 billion in 2026.

What growth rate is forecast through 2031?

The market is set to post a 7.23% CAGR from 2026 to 2031.

Which destination type commands the largest share?

Privately owned campgrounds led with 36.71% of 2025 revenue.

Which camper segment will expand fastest?

Backpacking is projected for an 8.62% CAGR to 2031.

Which U.S. region will grow quickest?

The Western region is projected to experience the highest compound annual growth rate (CAGR) through 2031.

How concentrated is competition among campground operators?

The top five players hold about one-fourth of revenue, reflecting moderate fragmentation.

Page last updated on: