Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

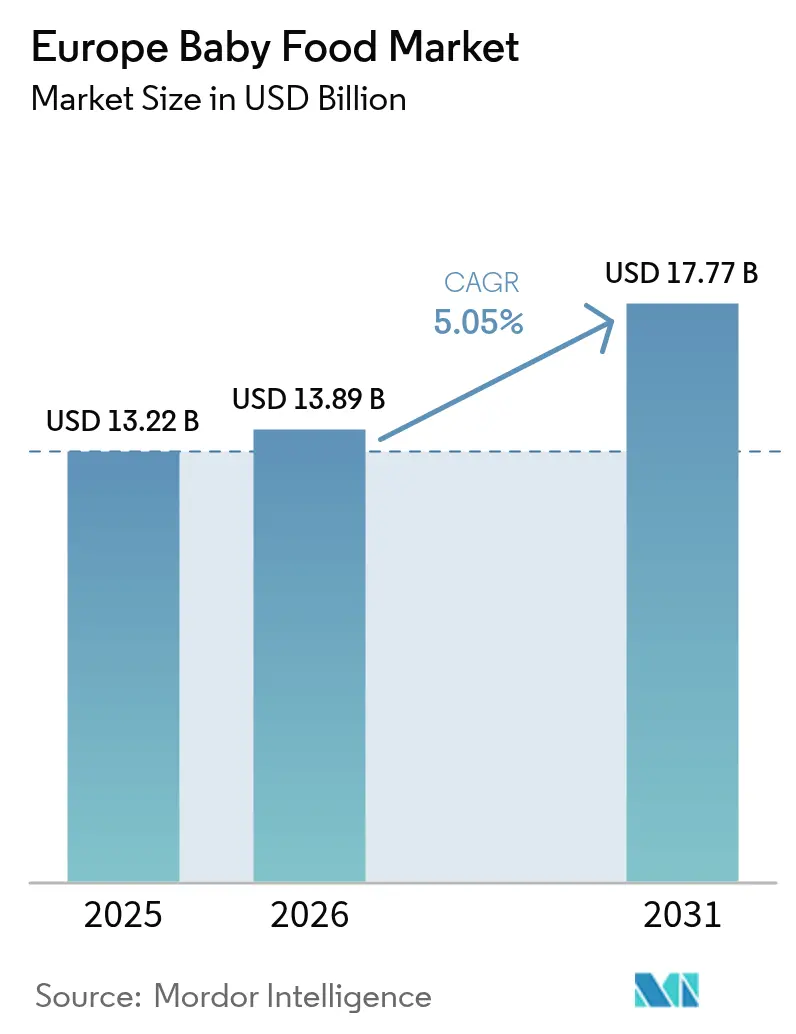

| Base Year Market Size (2025) | USD 13.22 Billion |

| Market Size (2026) | USD 13.89 Billion |

| Market Size (2031) | USD 17.77 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

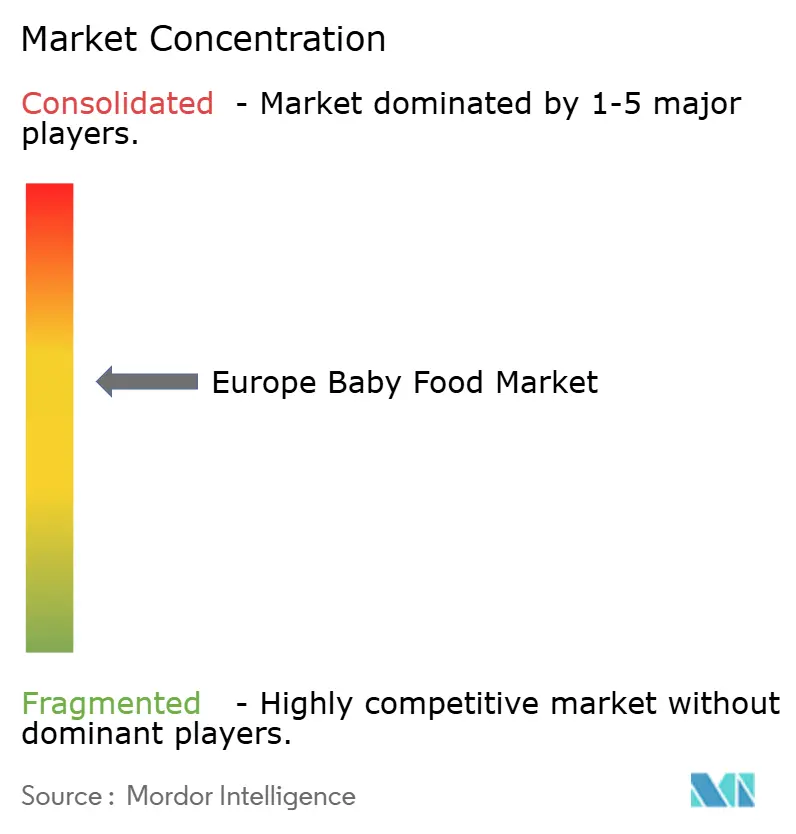

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Baby Food Market Analysis by Mordor Intelligence

The Europe baby food market size is expected to grow from USD 13.22 billion in 2025 to USD 13.89 billion in 2026 and is forecast to reach USD 17.77 billion by 2031 at 5.05% CAGR over 2026-2031. This growth trajectory reflects the market's resilience despite demographic headwinds, with strategic shifts toward premium nutrition and functional ingredients offsetting volume pressures from declining birth rates across the region. In 2023, 3.67 million babies were born in the European Union[1]Source: Eurostat, “Record drop in children being born in the EU in 2023,” ec.europa.eu. The market continues to expand through value-driven premiumization and innovation in specialized nutrition segments.

Key Report Takeaways

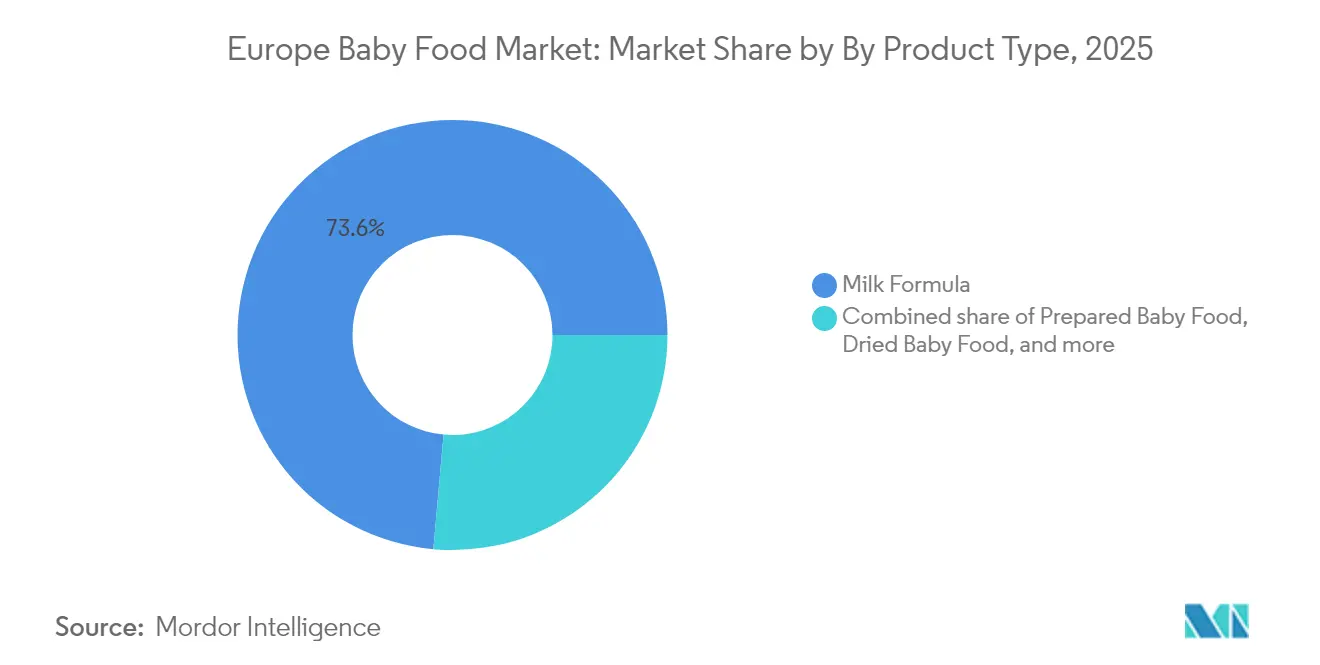

- By product type, milk formula captured 73.58% of the Europe baby food market share in 2025, while prepared baby food is projected to advance at a 7.02% CAGR from 2026-2031.

- By category, conventional products accounted for 71.64% of 2025 revenue, whereas organic alternatives are poised to grow at 7.41% CAGR through 2031.

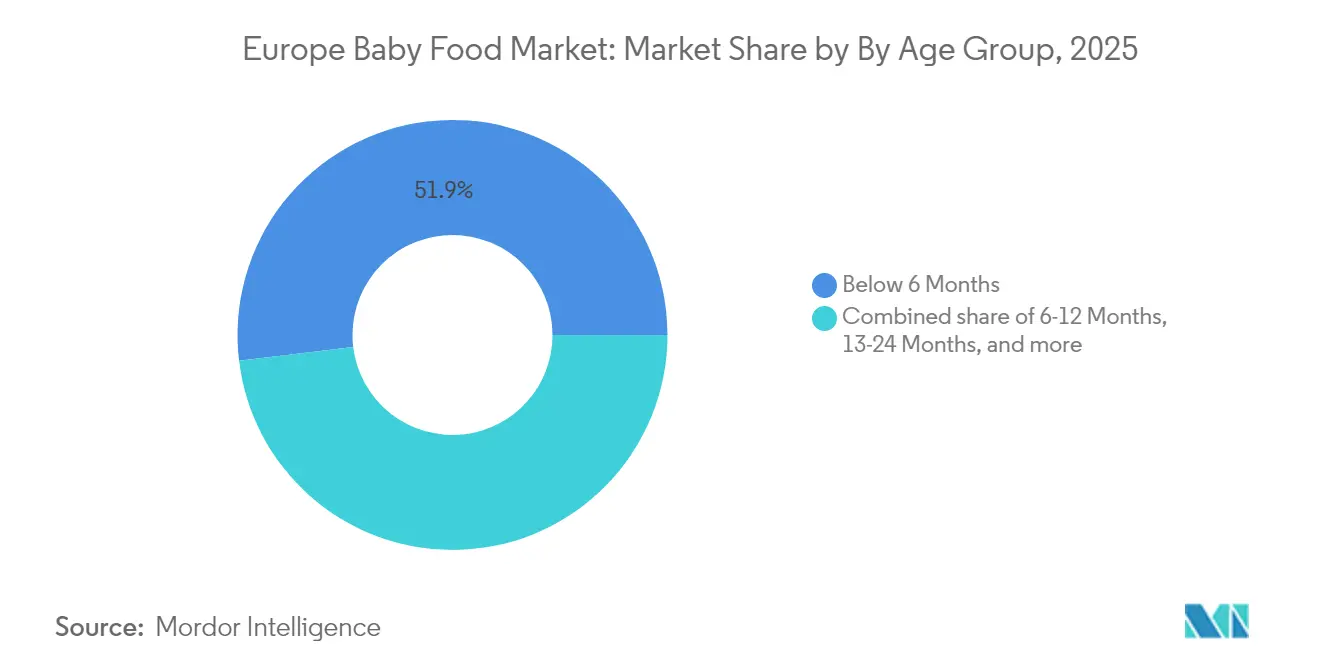

- By age group, products for infants below 6 months generated 51.92% of 2025 sales, and the 13-24 months cohort is expected to log a 6.87% CAGR in the forecast window.

- By distribution channel, supermarkets/hypermarkets led with 38.67% value in 2025, yet online retail is set for the fastest expansion at 7.22% CAGR to 2031.

- By geography, Germany held the largest 18.11% share of 2025 revenue, while Poland is forecast to register the highest 7.34% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Baby Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising number of working mothers and dual-income households | +1.2% | Germany, France, Netherlands, Sweden | Medium term (2-4 years) |

| Growing demand for organic and clean-label baby food | +1.8% | Germany, Netherlands, France, United Kingdom | Long term (≥ 4 years) |

| Functional ingredient innovation (DHA, probiotics, hypo-allergenic) | +1.5% | Global, with early adoption in Germany, Netherlands | Long term (≥ 4 years) |

| Influence of pediatric and medical guidance | +0.9% | Global, strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| Rising parental health consciousness | +1.1% | Germany, Netherlands, Sweden, France | Medium term (2-4 years) |

| EU Green Deal incentives for eco-packaging and sustainable sourcing | +0.7% | EU-wide, strongest in Germany, Netherlands, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Number of Working Mothers and Dual-Income Households

The transformation of European family structures drives sustained demand for convenient, nutritionally complete baby food solutions as maternal employment rates continue climbing across key markets. The EU Work-Life Balance Directive implementation has strengthened parental leave policies, yet the economic necessity for dual incomes persists, particularly in high-cost urban centers where housing expenses consume larger household budget shares. This demographic shift favors prepared baby food formats and premium convenience products that allow working parents to provide specialized nutrition without extensive meal preparation time. The trend accelerates in Nordic countries, where gender equality initiatives have normalized dual-career families, creating sustained market expansion opportunities for brands positioning around convenience without compromising nutritional integrity.

Growing Demand for Organic and Clean-Label Baby Food

European parents increasingly prioritize organic and clean-label formulations, driven by heightened awareness of agricultural practices and ingredient transparency following recent food safety incidents and environmental concerns. The EU's target of achieving 25% organic farmland by 2030, currently at approximately 11%, creates supply chain momentum supporting organic baby food expansion[2]Source: IFOAM Organics Europe, “Environmental impacts of achieving the EU’s 25% organic land by 2030 target,” organicseurope.bio. Clean-label positioning resonates particularly strongly in Germany and Netherlands, where consumer research indicates parents scrutinize ingredient lists more intensively for baby products than any other food category. This trend intersects with regulatory developments, as EFSA continues updating guidelines on acceptable additives and processing aids in infant nutrition, creating competitive advantages for manufacturers investing early in clean-label reformulations. The organic premium pricing model remains viable despite inflationary pressures, as parents demonstrate willingness to prioritize perceived safety and environmental benefits for infant nutrition over cost considerations.

Functional Ingredient Innovation (DHA, Probiotics, Hypo-allergenic)

Advanced nutritional science drives market premiumization through functional ingredients that address specific developmental needs, with human milk oligosaccharides (HMOs) and targeted probiotic strains leading innovation cycles. Nestlé's NAN Sinergity formula incorporates 6 different HMOs, while dsm-firmenich partnerships with Lallemand Health Solutions focus on early-life synbiotics combining probiotics with prebiotic HMOs. Clinical evidence supporting specific probiotic strains like Bifidobacterium longum subsp. infantis M-63 for HMO utilization and infant gut health development provides manufacturers with substantiated health claims for premium positioning. The regulatory pathway for novel functional ingredients remains rigorous under EFSA evaluation protocols, creating barriers to entry that favor established players with robust R&D capabilities and clinical trial infrastructure. Innovation focus shifts toward personalized nutrition approaches, with emerging research on genetic variations affecting nutrient metabolism potentially enabling customized formulation strategies for different infant populations.

Influence of Pediatric and Medical Guidance

Healthcare professional recommendations significantly shape parent purchasing decisions, with ESPGHAN, EFSA, and WHO Europe guidelines establishing evidence-based frameworks that influence product development and marketing strategies. Recent ESPGHAN recommendations emphasize complementary feeding timing between 4-6 months, iron-rich food introduction, and systematic allergen exposure protocols, creating market opportunities for products aligned with these clinical guidelines. Pediatric guidance increasingly emphasizes texture progression and self-feeding development, supporting growth in finger foods and age-appropriate consistency variations that traditional pureed formats cannot address. The medical community's growing recognition of early nutrition's impact on long-term health outcomes strengthens the scientific foundation for premium pricing and specialized formulations targeting specific developmental windows. Healthcare professional education programs by manufacturers create indirect marketing channels while building clinical credibility for evidence-based product positioning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining birth rates across Europe | -2.1% | EU-wide, strongest impact in Germany, Italy, Spain | Short term (≤ 2 years) |

| Stringent EU regulation and marketing code for infant formula | -0.8% | EU-wide, particularly affecting new market entrants | Medium term (2-4 years) |

| Climate-driven raw-material volatility for organic inputs | -0.6% | EU-wide, strongest in organic segment | Medium term (2-4 years) |

| Rise of home-made baby-led-weaning solutions | -0.4% | United Kingdom, Germany, Netherlands, Poland | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining Birth Rates Across Europe

European fertility rates reached historic lows in 2023, with total births declining 5.4% to 3.67 million across EU member states, creating structural headwinds for volume-based growth strategies in infant nutrition categories[3]Source: Eurostat, “Record drop in children being born in the EU in 2023,” ec.europa.eu. The fertility rate dropped to 1.38 children per woman, well below the 2.1 replacement level, with particularly steep declines in traditional high-birth-rate countries like Poland and Czech Republic. This demographic transition forces manufacturers to pursue value-over-volume strategies, emphasizing premium positioning and extended usage periods rather than market share expansion through broader consumer base growth. Economic uncertainty, housing affordability crises, and career prioritization among millennials compound the fertility decline, creating long-term structural challenges that require strategic pivots toward premiumization and international expansion to maintain revenue growth trajectories.

Stringent EU Regulation and Marketing Code for Infant Formula

Comprehensive regulatory frameworks governing infant formula composition, labeling, and marketing create significant compliance costs and market entry barriers, particularly affecting smaller manufacturers and new product categories. EU Regulation 609/2013 and Delegated Regulation 2016/127 establish detailed compositional requirements for infant formula, while marketing restrictions limit promotional activities for products intended for children under 12 months. Recent EFSA evaluations of novel ingredients like HMOs require extensive clinical documentation and safety assessments, creating regulatory lag times that can exceed 24 months for innovative formulations. The regulatory complexity favors established multinational companies with dedicated regulatory affairs capabilities while constraining innovation speed and market responsiveness for emerging players seeking to introduce differentiated products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Formula Dominance Drives Premiumization

Milk formula maintains commanding market leadership with 73.58% share in 2025, yet prepared baby food emerges as the fastest-growing segment with 7.02% CAGR from 2026-2031, reflecting shifting consumer preferences toward convenience and variety in infant nutrition. The prepared baby food segment capitalizes on dual-income household time constraints and premiumization trends, with organic and clean-label variants commanding premium pricing despite inflationary pressures across European markets.

Dried baby food maintains a steady market presence through cost-effectiveness and extended shelf life advantages, particularly appealing to price-conscious consumers and bulk purchasing patterns. Innovation within the milk formula category focuses on functional ingredients like HMOs and targeted probiotic strains, with clinical evidence supporting cognitive development and immune system benefits driving premium positioning strategies. The segment's evolution toward personalized nutrition approaches reflects broader healthcare trends emphasizing individualized dietary interventions based on genetic and developmental factors.

By Category: Organic Acceleration Outpaces Conventional Growth

The conventional baby food category holds 71.64% market share in 2025, yet organic alternatives demonstrate superior growth momentum with 7.41% CAGR from 2026-2031, indicating accelerating consumer preference shifts toward perceived cleaner and more sustainable nutrition options. Organic positioning benefits from EU agricultural policy support targeting 25% organic farmland by 2030, creating supply chain infrastructure that supports ingredient availability and cost competitiveness over time. Premium pricing strategies for organic products remain viable despite economic pressures, as parents demonstrate willingness to prioritize perceived safety and environmental benefits for infant nutrition over cost considerations.

Conventional products maintain market leadership through established distribution relationships and price accessibility, yet face increasing pressure to adopt clean-label formulations and sustainable packaging to compete with organic alternatives. The category boundary blurs as conventional manufacturers incorporate organic ingredients selectively while maintaining cost-competitive positioning through hybrid approaches. Regulatory frameworks under EU organic certification standards create quality differentiation opportunities while establishing consumer trust through third-party verification systems that support premium pricing strategies.

By Age Group: Extended Nutrition Windows Drive Growth

Products for infants below 6 months represent 51.92% of market share in 2025, reflecting the critical importance of early nutrition during exclusive milk feeding periods, while the 13-24 months category demonstrates the highest growth potential with 6.87% CAGR from 2026-2031. This growth pattern indicates parents increasingly extend specialized nutrition beyond traditional weaning timelines, creating opportunities for age-specific formulations targeting developmental milestones. The 6-12 months segment benefits from complementary feeding introduction guidelines established by ESPGHAN and WHO Europe, emphasizing iron-rich foods and systematic allergen exposure protocols that support specialized product development.

The 25+ months category captures parents seeking continued nutritional insurance as toddlers transition to family foods, with growing-up milks and fortified snacks addressing perceived nutritional gaps in diverse diets. Age-based segmentation strategies enable targeted marketing approaches addressing specific developmental concerns, from cognitive development support in early months to independence-building finger foods for older toddlers. Clinical research supporting age-specific nutritional requirements provides a scientific foundation for premium positioning and specialized formulation strategies that justify higher price points across extended feeding periods.

By Distribution Channel: Digital Transformation Accelerates

Supermarkets/hypermarkets maintain distribution leadership with 38.67% market share in 2025, leveraging established consumer shopping patterns and product visibility advantages, while online retail stores demonstrate the fastest growth at 7.22% CAGR from 2026-2031. Supermarkets/hypermarkets' leadership position stems from well-established consumer shopping patterns, extensive product assortments, and strategic in-store product placement that maximizes visibility. These traditional retail formats continue to benefit from their ability to offer immediate product availability and tactile shopping experiences. Moreover, online channels enable subscription models and personalized product recommendations that increase customer lifetime value while reducing acquisition costs for specialized brands.

Pharmacies and drugstores maintain important roles in premium and specialty product distribution, particularly for hypoallergenic and medical nutrition categories where healthcare professional recommendations influence purchasing decisions. Convenience stores capture impulse purchases and emergency restocking needs, though limited shelf space constrains assortment breadth compared to larger format retailers. The distribution landscape evolves toward omnichannel integration, with successful brands developing coherent strategies across physical and digital touchpoints while leveraging retail media opportunities for targeted consumer engagement.

Geography Analysis

Germany's market leadership position with 18.11% share in 2025 reflects the country's robust economic fundamentals and deeply embedded organic food culture that extends naturally to infant nutrition categories. German consumers demonstrate exceptional willingness to pay premium prices for perceived quality and safety benefits, with organic baby food penetration rates significantly exceeding European averages. The regulatory environment supports innovation through efficient EFSA coordination and an established clinical research infrastructure that enables rapid product development cycles.

Poland's exceptional 7.34% CAGR growth from 2026-2031 represents the most dynamic expansion opportunity within European markets, driven by unique demographic factors and accelerating premiumization trends among rising middle-class consumers. Polish consumers increasingly embrace Western European feeding practices and premium nutrition concepts, creating market expansion opportunities for established brands seeking growth beyond mature home markets. The retail infrastructure rapidly modernizes, with international hypermarket chains and emerging e-commerce platforms providing distribution access for specialized baby food categories previously unavailable in the market.

The United Kingdom, Italy, France, Spain, and Netherlands collectively represent mature markets requiring innovation-driven differentiation strategies to capture incremental growth beyond demographic constraints. These markets demonstrate established brand loyalties and sophisticated distribution networks that create barriers to entry for new players while rewarding sustained investment in product development and consumer education. Regional preferences vary significantly, with Mediterranean markets showing stronger retention of traditional feeding practices that affect prepared food acceptance rates, while Nordic countries demonstrate higher organic adoption and functional ingredient appreciation.

Competitive Landscape

The European baby food market exhibits moderate concentration, indicating balanced competitive dynamics where established multinational players compete alongside regional specialists and emerging premium brands. Strategic patterns emphasize innovation in functional ingredients, with major players investing heavily in HMO technology, targeted probiotic strains, and clean-label formulations to justify premium positioning despite demographic headwinds. Nestlé's introduction of NAN Sinergity with 6 different HMOs exemplifies the science-driven differentiation approach.

Technology adoption focuses on personalized nutrition platforms and direct-to-consumer subscription models that increase customer lifetime value while reducing traditional retail dependencies. White-space opportunities emerge in specialized nutrition categories targeting specific dietary needs, environmental sustainability positioning, and digital-native brand development that bypasses traditional distribution constraints.

Emerging disruptors leverage e-commerce platforms and social media marketing to build direct relationships with millennial parents seeking transparency and ingredient education beyond traditional marketing approaches. The regulatory environment under EFSA guidelines creates both barriers and opportunities, favoring companies with robust clinical research capabilities while constraining rapid market entry for innovative formulations requiring extensive safety documentation.

Europe Baby Food Industry Leaders

Nestlé SA

Danone SA

Reckitt

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Ella's Kitchen has expanded its product line for children aged 12 months and older with Oaty Smooshies, a range of dairy-free fruit and oat snacks. The products come in Berry and Peach + Banana flavors, packaged in recyclable pouches in a multipack format. Each serving contains real fruit and oats, providing fiber and counting as one portion of the recommended five daily fruit and vegetable servings. The products contain no added sugar or salt.

- November 2024: Bonya Formula introduced a lower-cost version of its baby formula. This new product, developed by the company behind Kendamil, is priced at nearly half the cost of the Kendamil Organic range and approximately one-third less expensive than most other leading brands in the market. Bonya will be available for purchase at Tesco and Sainsbury's.

- November 2023: Else Nutrition launched its Plant-Based Complete Nutrition Toddler Drink in the United Kingdom, marking its entry into the European market. The product, formulated for toddlers aged 12 months and older, is free from soy, dairy, corn syrup, and genetically modified organisms (GMO).

Europe Baby Food Market Report Scope

Baby food can be described as soft and easily consumed food manufactured from natural or organic ingredients or formula.

The market is segmented by type, distribution channel, and country. Based on type, the market is segmented into milk formula, dried baby food, prepared baby food, and other types. Based on the distribution channel, the market is segmented into hypermarkets/supermarkets, drugstores/pharmacies, and convenience stores. The study also covers the European market analysis of the major regions, including Spain, the United Kingdom, Germany, France, Italy, Russia, and the Rest of Europe.

For each segment, the market sizing and forecasts have been done based on value (in USD Million).

By Product Type

| Milk Formula | Standard Formula |

| Follow-on Formula | |

| Growing-Up Formula | |

| Specialty Formula | |

| Prepared Baby Food | |

| Dried Baby Food | |

| Other Baby Food |

By Category

| Conventional |

| Organic |

BY Age Group

| Below 6 Months |

| 6–12 Months |

| 13–24 Months |

| 25 Months + |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Pharmacies and Drugstores |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Milk Formula | Standard Formula |

| Follow-on Formula | ||

| Growing-Up Formula | ||

| Specialty Formula | ||

| Prepared Baby Food | ||

| Dried Baby Food | ||

| Other Baby Food | ||

| By Category | Conventional | |

| Organic | ||

| BY Age Group | Below 6 Months | |

| 6–12 Months | ||

| 13–24 Months | ||

| 25 Months + | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Pharmacies and Drugstores | ||

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe baby food market?

It is valued at USD 13.89 billion in 2026 and is projected to reach USD 17.77 billion by 2031.

Which product type holds the biggest share across Europe?

Milk formula commands 73.58% of 2025 sales, led by specialty and follow-on variants.

What is driving the shift toward organic baby food?

EU policy support for organic agriculture and parental concern over pesticide exposure are propelling organic SKUs at a 7.41% CAGR.

Which distribution channel is expanding quickest?

Online retail is growing 7.22% per year due to subscription models and doorstep convenience.

Page last updated on: