Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

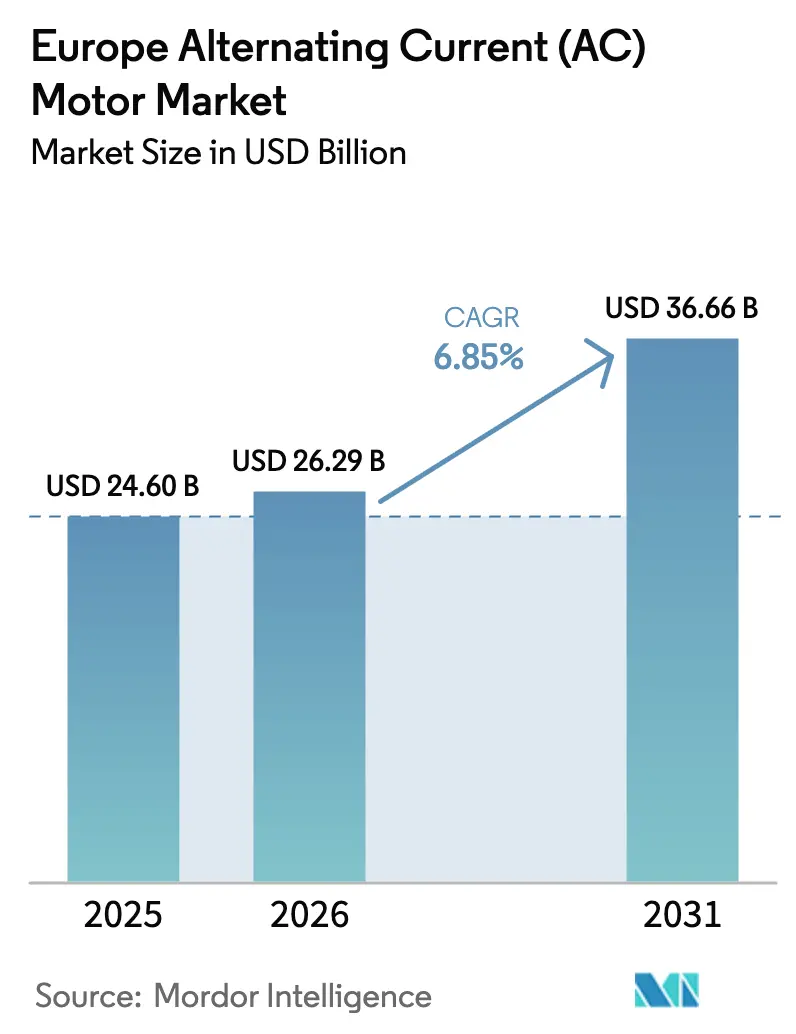

| Base Year Market Size (2025) | USD 24.6 Billion |

| Market Size (2026) | USD 26.29 Billion |

| Market Size (2031) | USD 36.66 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

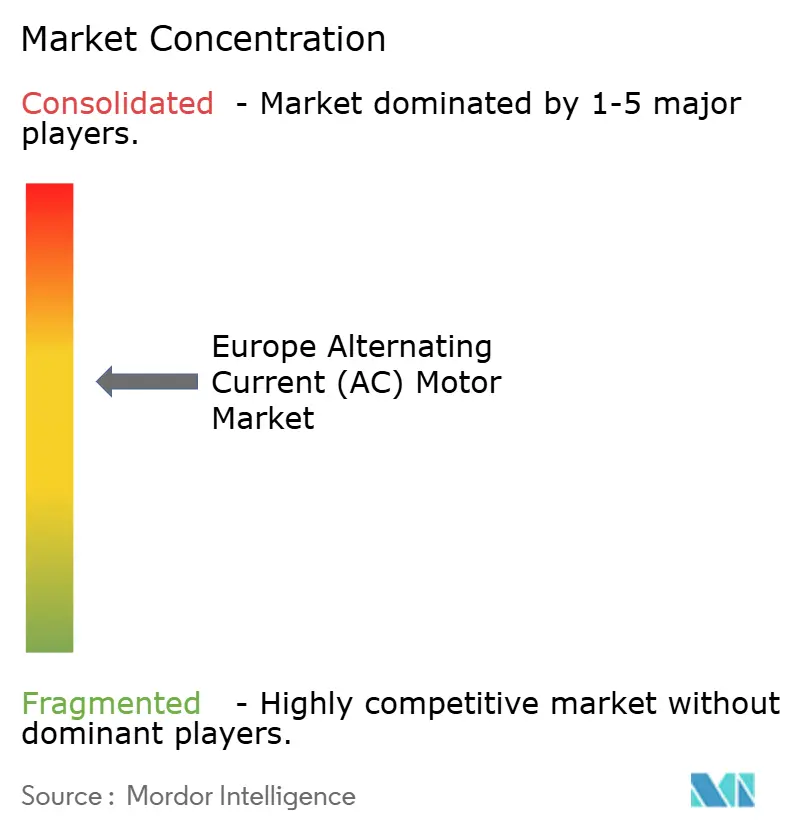

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Alternating Current (AC) Motor Market Analysis by Mordor Intelligence

The Europe alternating current motor market size is expected to grow from USD 24.6 billion in 2025 to USD 26.29 billion in 2026 and is forecast to reach USD 36.66 billion by 2031 at 6.85% CAGR over 2026-2031. This trajectory reflects the convergence of stringent EU energy-efficiency mandates, the reshoring of sophisticated manufacturing, and capital spending on hydrogen and renewable infrastructure. Manufacturers are prioritizing IE3-plus efficiency classes, integrating sensors that feed plant-wide IoT platforms, and redesigning drive packages to lower installation complexity amid tight labor markets. At the same time, large electrolyzer projects, district energy schemes, and medium-voltage retrofits are broadening demand beyond the traditional pump-fan-compressor core of the Europe alternating current motor market. Competitive dynamics remain moderate as global majors leverage integrated motor-drive offerings while regional specialists exploit application depth to defend share against price-led imports.

Key Report Takeaways

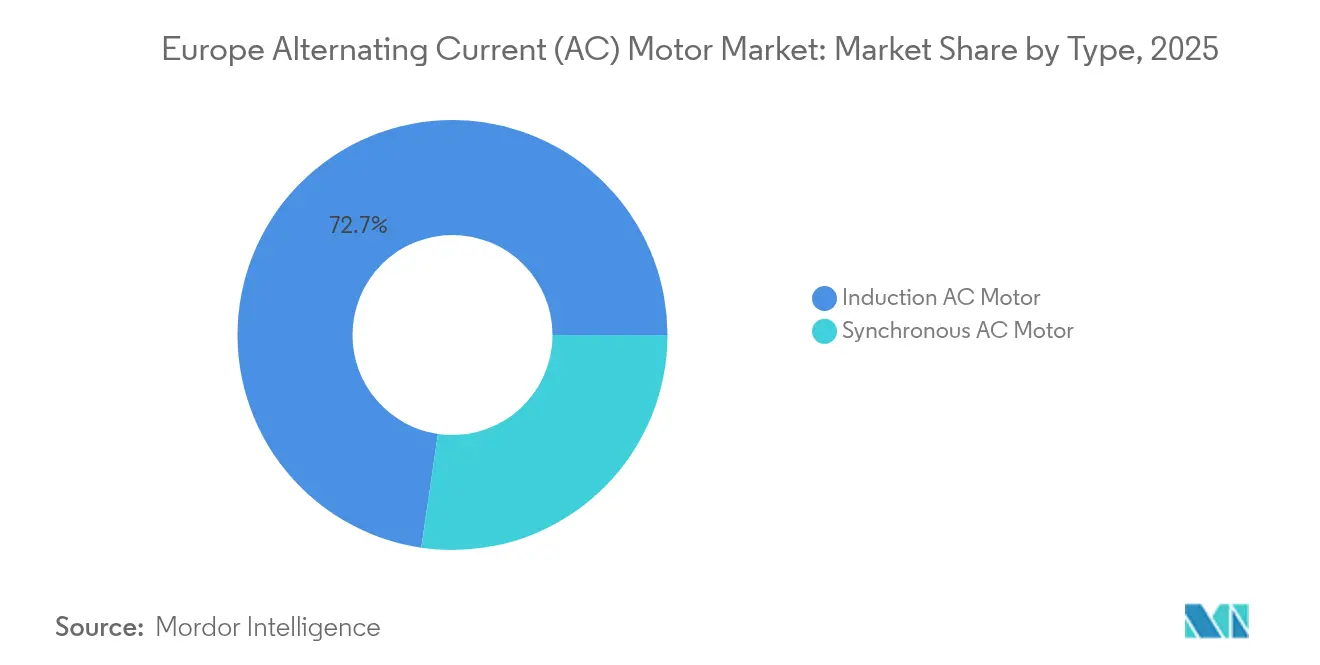

- By type, induction designs led with a 72.68% share of the European alternating current motor market in 2025, whereas synchronous designs are advancing at a 8.67% CAGR through 2031.

- By power rating, sub-1 kW units accounted for 37.02% of the Europe alternating current motor market size in 2025, while the 101-500 kW band is forecast to grow at an 8.29% CAGR.

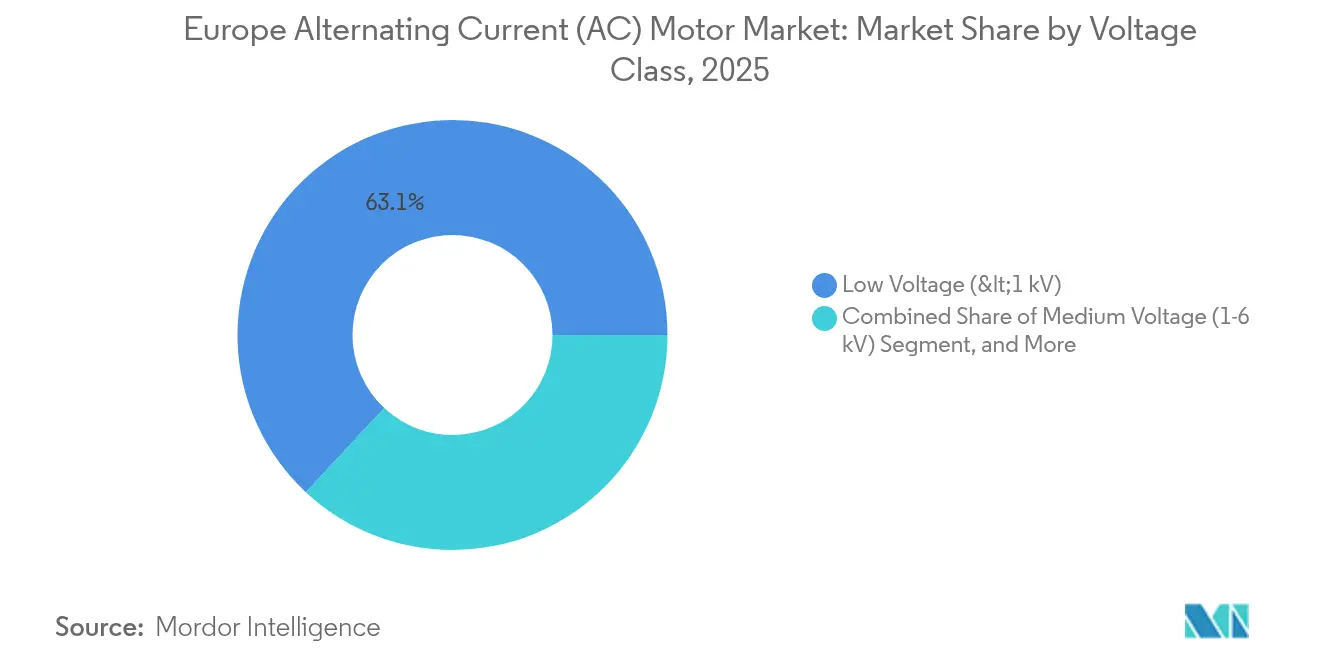

- By voltage class, low-voltage units below 1 kV held 63.05% revenue share in 2025, and medium-voltage units between 1-6 kV are on track for an 8.44% CAGR.

- By end-user industry, discrete manufacturing captured 23.35% revenue share in 2025, while water and wastewater applications are projected to expand at a 7.12% CAGR.

- By geography, Germany accounted for 26.10% of 2025 revenues, whereas Italy is projected to have the fastest growth rate of 7.42% from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Alternating Current (AC) Motor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating industrial automation and IoT adoption | +1.5% | Germany, Netherlands, Nordic countries | Medium term (2-4 years) |

| Stringent energy-efficiency regulations for electric motors | +1.2% | EU-wide, United Kingdom alignment | Short term (≤ 2 years) |

| Expansion of HVAC and refrigeration infrastructure | +0.9% | Southern Europe urban centers | Medium term (2-4 years) |

| Revival of automotive manufacturing and EV powertrain demand | +0.8% | Germany, France, Eastern Europe | Long term (≥ 4 years) |

| Growing adoption of high-frequency spindle motors in machine-tool re-shoring | +0.6% | Germany, Italy, Switzerland | Medium term (2-4 years) |

| Emergence of hydrogen electrolyzer projects needing large synchronous motors | +0.4% | Netherlands, Germany, Scandinavia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Industrial Automation and IoT Adoption

European factories are incorporating smart drives that collect data on vibration, temperature, and load to enable predictive maintenance and optimize line changeovers. Early projects report double-digit energy savings and sub-four-year paybacks as asset performance systems shift from fixed-speed to variable-speed regimes supported by edge computing nodes. German automotive suppliers have led pilot deployments, specifying Ethernet-ready IE5 platforms that publish diagnostic tags directly to manufacturing execution systems for real-time quality loops. The Europe alternating current motor market benefits from the resulting replacement cycle for legacy induction units with sensor-rich, firmware-upgradable models. Tier-one vendors are responding with subscription-based analytics modules that bundle hardware, firmware, and artificial-intelligence monitoring in a single service contract.[1]ABB Ltd., “ABB Drives Highlights and References,” abb.com

Stringent Energy-Efficiency Regulations for Electric Motors

EU Regulation 2019/1781 elevated the minimum requirement for three-phase motors above 0.75 kW to IE3 and extended coverage to submersible and close-coupled configurations. Penalties for non-compliance, enforced through national surveillance authorities, have accelerated retrofit programs across chemical, food, and building services sites. Suppliers now differentiate on IE4 and IE5 lines marketed as “future-proof,” while installers promote pay-per-savings contracting that sidesteps upfront capital hurdles. Certification-ready testing labs offer fast-track conformity assessments, giving domestically rooted brands an edge in the Europe alternating current motor market.[2]European Commission, “Commission Regulation (EU) 2019/1781 of 1 October 2019 laying down ecodesign requirements for electric motors and variable speed drives,” eur-lex.europa.eu

Expansion of HVAC and Refrigeration Infrastructure

Heat-pump sales surged after national decarbonization incentives tied to the REPowerEU plan, lifting demand for electronically commutated motors that maintain a high coefficient of performance across variable ambient temperatures. Supermarkets replacing hydrofluorocarbon systems with transcritical CO₂ racks deploy permanent-magnet drive compressors, each requiring precise speed modulation to meet food safety regulations while trimming electricity bills. Urban district-cooling schemes in southern capitals are specifying multi-megawatt synchronous machines paired with harmonic-free medium-voltage drives to compress chilled water at scale. These trends collectively reinforce mid-range growth in the Europe alternating current motor market.[3]Danfoss A/S, “How a new water pumping station keeps supply flowing in Bern,” danfoss.com

Revival of Automotive Manufacturing and EV Powertrain Demand

Battery-cell, module, and drivetrain plants reshored from Asia are equipping robotic stations with low-inertia motors that achieve micron-level positioning repeatability. Clean-room protocols demand sealed housings and integrated encoders, nudging customers toward premium synchronous architectures. Assembly lines for next-generation electric vehicles require high-torque servo packages to manage heavier battery packs without sacrificing takt time, stimulating value-added sales above conventional induction offerings. Charging-infrastructure OEMs simultaneously source forced-cooling motors for 350 kW DC fast-charge cabinets, thereby expanding the total addressable market for suppliers that can certify to both ATEX and automotive functional safety standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial procurement and installation costs | -0.7% | Price-sensitive markets, SME segment | Short term (≤ 2 years) |

| Rising raw-material price volatility (copper, rare earths) | -0.5% | EU-wide, import-dependent regions | Medium term (2-4 years) |

| Competitive pressure from permanent-magnet DC and servo drives | -0.4% | Precision applications, robotics | Medium term (2-4 years) |

| Supply chain tightness in insulated lamination steel | -0.3% | Manufacturing hubs, OEM suppliers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Initial Procurement and Installation Costs

Premium IE4-plus motors cost 20-40% more than standard units, and the prerequisite variable-frequency drives can double a project’s hardware bill. Retrofitting drives often necessitate switchboard upgrades, harmonic filters, and mechanical realignment, which can stretch payback models for small enterprises operating on tight margins. Energy-performance contracting mitigates sticker shock by spreading payments across multiple savings streams, but adoption remains uneven outside blue-chip industries. Until financing models mature, upfront economics will temper the pace at which the Europe alternating current motor market converts its installed base.

Rising Raw-Material Price Volatility (Copper, Rare Earths)

Windings account for a sizable share of motor manufacturing cost, leaving producers exposed to swings in copper prices exacerbated by global electrification programs. Permanent-magnet synchronous designs enhance sensitivity to the supply of neodymium and dysprosium, which is dominated by a narrow set of producers. Design engineers are trialing ferrite hybrid topologies and copper-alloy substitutes, but performance or tooling trade-offs persist. Periods of raw-material inflation therefore compress margins, elevate selling prices, and prompt some buyers to delay procurement cycles, suppressing near-term shipments in the Europe alternating current motor market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Synchronous Motors, Advance Premium Applications

Synchronous units controlled 27.32% of 2025 revenue yet are forecast for the highest 8.67% CAGR because precise torque response, low acoustic signature, and rising spindle-speed requirements outweigh higher capital costs in machine-tool, hydrogen, and HVAC drives. Integrated motor-drive packages that auto-tune power factors boost line-level efficiency and enable full-torque zero-speed starts that induction machines cannot match.

Induction units defend baseline duties such as fans, pumps, and conveyors thanks to their ruggedness and commoditized repair ecosystem. However, regulatory tightening, combined with predictive-maintenance preferences, is steadily redirecting orders to synchronous alternatives in the Europe alternating current motor market. ABB’s MV Titanium concept, which embeds a medium-voltage inverter within the motor frame, illustrates how synchronous architectures are converging mechanical and electronic components to lower total ownership cost.

By Power Rating: Industrial Electrification Drives Higher Power Demand

Sub-1 kW models dominate the volumes, accounting for 37.02% of the Europe alternating current motor market size in 2025. Yet the 101-500 kW slice is the fastest climber, expanding at 8.29% CAGR as cement, steel, and chemical sites electrify mechanical drives formerly powered by steam or hydraulics. Operators appreciate the ability to curtail idle loads through variable-torque algorithms and to synchronize multi-megawatt compressors directly with plant-wide energy-management systems.

In parallel, packages exceeding 500 kW win replacement business in legacy cogeneration plants and pumped-storage facilities, although growth is steadier due to longer project cycles. The power-rating spectrum, therefore, mirrors Europe’s industrial makeup, with mid-sized sites modernizing toward net-zero objectives.

By Voltage Class: Medium Voltage Gains Industrial Traction

Low-voltage frameworks remain the workhorse, accounting for 63.05% of the revenue share, making them ideal for quick-connect installation on standard plant distribution networks. Medium-voltage units are gaining ground with an 8.44% CAGR because they enable loads of 101-500 kW to operate at lower currents, smaller cable cross-sections, and reduced heat losses.

Advances in silicon-carbide switching have reduced the footprint of MV inverters, eliminating bulky step-down transformers. Utilities and water authorities in Italy and Spain have consequently specified 3.3 kV pump trains that halve total harmonic distortion and qualify for grid-service incentives, reinforcing the migration up the voltage curve within the Europe alternating current motor market.

By End-User Industry: Water Treatment Accelerates Modernization

Discrete manufacturing held 23.35% of 2025 turnover, but municipal water and wastewater plants are forecast to deliver the fastest 7.12% CAGR. Regulators cap specific energy consumption per cubic meter pumped, spurring tenders for premium IE4 motors coupled to real-time SCADA analytics. Retrofit awards across Northern Europe mandate variable-torque profiles that throttle pumps during low-demand windows, cutting both kilowatt-hours and pipe bursts.

Metal, mining, and food processors maintain steady order books with specialized requirements, including washdown ingress protection and explosion-proof housings. Oil and gas capex stays muted pending clarity on carbon-capture economics, yet operators continue to order hazardous-area induction machines for mid-life asset refreshes.

Geography Analysis

Germany anchored 26.10% of 2025 sales on the strength of its automotive, machinery, and chemical sectors that embed motors deep into digitized production cells. Federal support for hydrogen clusters is driving large synchronous-drive orders for electrolyzers, while offshore wind OEMs source pitch-control servos from domestic suppliers. Italian revenues are rising at a 7.42% CAGR as water-infrastructure concessions and renewable-heat incentives accelerate pump and compressor upgrades. Lombardy food processors further bolster demand by transitioning to variable-speed synchronous ammonia-based refrigeration packages to meet F-gas quotas. France, the United Kingdom, and the Benelux region each exhibit mid-single-digit growth trajectories tied to pharmaceutical, data center, and maritime electrification projects. Eastern European countries are attracting relocated assembly lines, thereby creating greenfield opportunities for low-voltage IE3 induction fleets and a nascent layer of premium synchronous retrofits. Nordic markets, although smaller, specify ruggedized IP66 housings and wide-temperature bearings for hydropower and district heating duties, keeping average selling prices above the continental mean. Collectively, these geographic subtleties ensure healthy, albeit varied, expansion across the Europe alternating current motor market.

Competitive Landscape

The market exhibits moderate concentration, with the top five brands holding roughly 55% of shipments, leaving a meaningful share for mid-tier regional specialists. ABB, Siemens, and Nidec defend their installed bases with lifecycle-service packages that integrate cloud analytics with drive firmware updates, while Regal Rexnord and WEG accelerate speed-to-market through modular assembly centers.

Private-equity-backed carve-outs underscore the consolidation appetite; the EUR 3.5 billion purchase of Siemens' Innomatics by KPS Capital Partners creates a stand-alone champion committed to deeper vertical integration and faster decision-making cycles. Portfolio gaps are being filled through M&A focused on embedded software, power electronics, and condition monitoring assets that shorten the time to compliance under EU eco-design rules.

Product differentiation leans on permanent-magnet designs, medium-voltage packages, and cybersecurity-hardened connectivity stacks. Suppliers are also localizing their copper and steel sourcing to hedge against raw-material swings, a capability that small importers struggle to replicate. As tender criteria prioritize lifecycle cost and service responsiveness, vendors equipped with pan-European field engineering teams are best placed to secure repeat business in the Europe alternating current motor market.

Europe Alternating Current (AC) Motor Industry Leaders

ABB Ltd.

Siemens AG

Nidec Corporation

Regal Rexnord Corporation

Toshiba Mitsubishi-Electric Industrial Systems Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: ABB extended its MV Titanium portfolio to serve hydrogen electrolyzers, rolling out integrated medium-voltage motor-drive packages that achieve up to 98% efficiency and align with REPowerEU production goals across Germany, the Netherlands, and Scandinavia.

- September 2025: Siemens finished folding the ebm-papst Industrial Drive Technology unit into its Digital Industries arm and introduced upgraded mechatronic systems for European autonomous transport and high-frequency spindle applications.

- August 2025: Nidec opened a European technical center in Munich staffed by 150 engineers to design next-generation permanent-magnet synchronous motors tailored to regional energy-efficiency rules and Industry 4.0 needs.

- July 2025: WEG committed EUR 50 million to expand its Portuguese plant, adding lines for IE4 and IE5 motors destined for water treatment, renewable energy, and automation customers, with production slated to start in Q2 2026.

Europe Alternating Current (AC) Motor Market Report Scope

AC motor converts electric energy into mechanical energy using electromagnetic induction. These motors are different from DC motors in their use and find applications in home appliances, water pumps, machine tools, Compressors, etc.

The Europe Alternating Current Motor Market Report is Segmented by Type (Induction AC Motors, and Synchronous AC Motors), Power Rating (less than 1 kW, 1–100 kW, and More), Voltage Class (Low Voltage, Medium Voltage, High Voltage), End-user Industry (Oil and Gas, Chemical and Petrochemical, Power Generation, Water and Wastewater, Metal and Mining, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Type

| Induction AC Motors | Single Phase |

| Poly Phase | |

| Synchronous AC Motors | DC Excited Rotor |

| Permanent Magnet | |

| Hysteresis Motor | |

| Reluctance Motor |

By Power Rating

| less than 1 kW |

| 1-100 kW |

| 101-500 kW |

| above 500 kW |

By Voltage Class

| Low Voltage (<1 kV) |

| Medium Voltage (1–6 kV) |

| High Voltage (>6 kV) |

By End-user Industry

| Oil and Gas |

| Chemical and Petrochemical |

| Power Generation |

| Water and Wastewater |

| Metal and Mining |

| Food and Beverage |

| Discrete Industries |

| Other End-user Industries |

By Country

| United Kingdom |

| Germany |

| Italy |

| France |

| Russia |

| Rest of Europe |

| By Type | Induction AC Motors | Single Phase |

| Poly Phase | ||

| Synchronous AC Motors | DC Excited Rotor | |

| Permanent Magnet | ||

| Hysteresis Motor | ||

| Reluctance Motor | ||

| By Power Rating | less than 1 kW | |

| 1-100 kW | ||

| 101-500 kW | ||

| above 500 kW | ||

| By Voltage Class | Low Voltage (<1 kV) | |

| Medium Voltage (1–6 kV) | ||

| High Voltage (>6 kV) | ||

| By End-user Industry | Oil and Gas | |

| Chemical and Petrochemical | ||

| Power Generation | ||

| Water and Wastewater | ||

| Metal and Mining | ||

| Food and Beverage | ||

| Discrete Industries | ||

| Other End-user Industries | ||

| By Country | United Kingdom | |

| Germany | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe alternating current motor market in 2026?

The market is valued at USD 26.29 billion in 2026 and is expected to grow at a 6.85% CAGR to USD 36.66 billion by 2031.

Which motor type is growing fastest across European industries?

Synchronous designs, particularly permanent-magnet models, are expanding at a 8.67% CAGR thanks to efficiency gains and precise speed control advantages.

Why are medium-voltage motors gaining share?

Medium-voltage units lower current draw for 101-500 kW loads, cut cabling costs, and now benefit from compact silicon-carbide drives that simplify installation.

Which end-user segment shows the highest growth?

Water and wastewater facilities are projected to post a 7.12% CAGR as utilities retrofit pumps to meet strict energy and circular-economy targets.

What is the main barrier to faster adoption of IE4 and IE5 motors?

High upfront costs for the motors and necessary variable-frequency drives make payback challenging for small and medium enterprises without performance-contract financing.

How concentrated is the supplier landscape?

The top five players control roughly 55% of shipments, indicating a moderately concentrated market with room for regional specialists to thrive.

Page last updated on: