Market Overview

| Study Period | 2020 - 2031 |

|---|---|

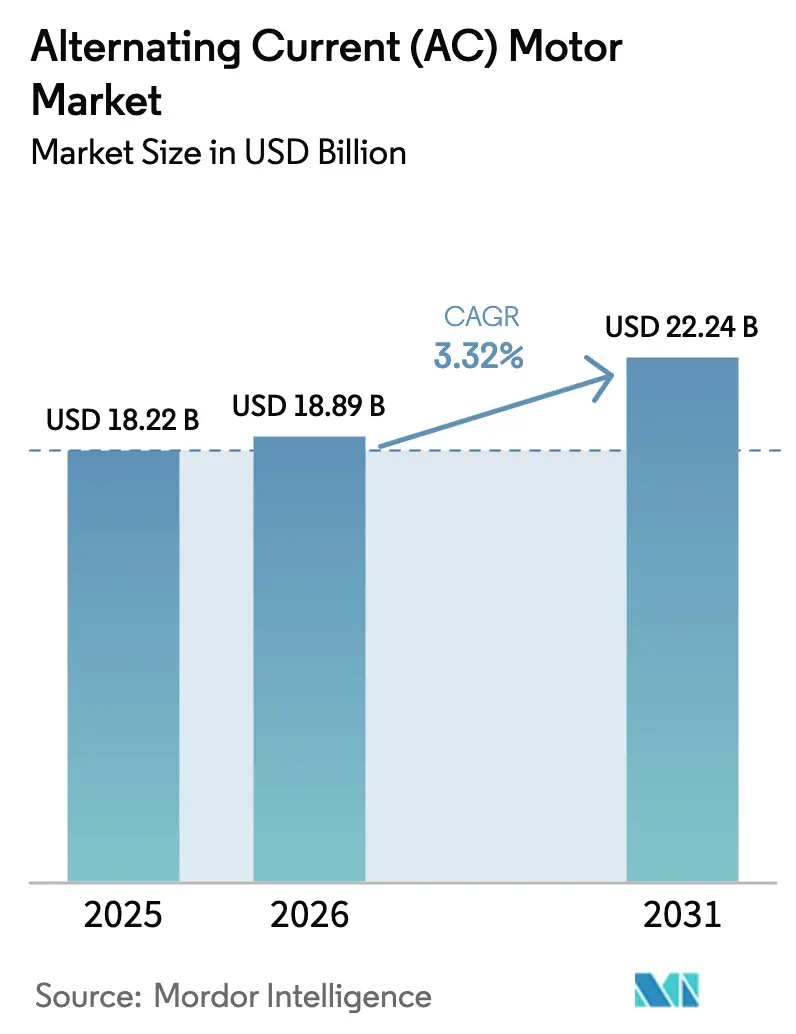

| Market Size (2026) | USD 18.89 Billion |

| Market Size (2031) | USD 22.24 Billion |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Africa |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alternating Current (AC) Motor Market Analysis by Mordor Intelligence

The Alternating Current Motor Market size is projected to expand from USD 18.23 billion in 2025 and USD 18.89 billion in 2026 to USD 22.24 billion by 2031, registering a CAGR of 3.32% between 2026 to 2031.

Mandatory IE3-IE4 efficiency rules now in force across major economies are shortening replacement cycles and pushing premium-efficiency adoption. Early movers among industrial buyers are capturing sub-three-year payback periods in high-utilization processes, while edge-analytics platforms bundled with drives are further improving uptime and trimming maintenance budgets. In parallel, the alternating current (AC) motor market is benefiting from a USD 50 billion wave of United States water-infrastructure grants and multibillion-dollar electrification programs in Africa that are unlocking latent demand for medium-voltage platforms. Competitive intensity remains moderate, yet vendors that combine IE4-ready portfolios with digital-service contracts are widening their lead. Synchronous permanent-magnet designs, axial-flux topologies for e-mobility, and silicon-carbide power electronics together outline the next frontier of differentiation in the alternating current (AC) motor market.

Key Report Takeaways

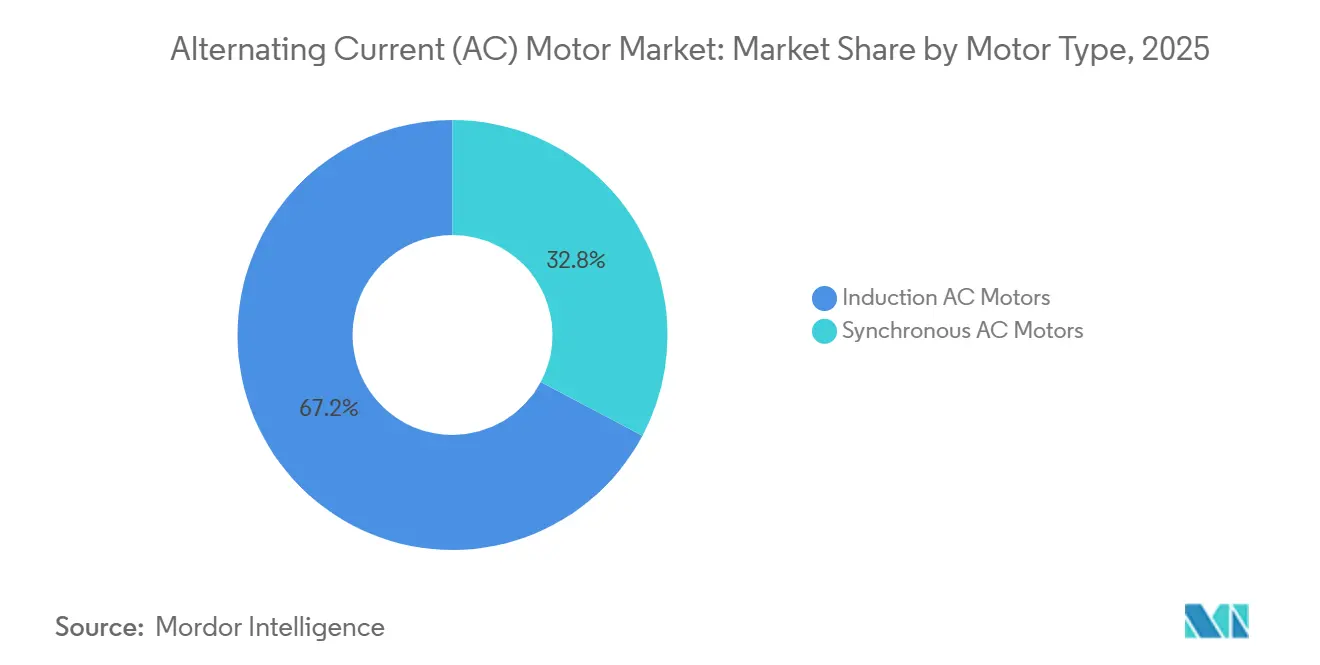

- By motor type, induction AC motors held 67.23% of the alternating current (AC) motor market share in 2025, while synchronous AC motors are projected to expand at a 3.68% CAGR through 2031.

- By voltage class, low-voltage machines accounted for 84.23% of 2025 revenue, whereas medium-voltage units are forecast to grow at a 3.89% CAGR during 2026-2031.

- By power rating, the 1-100 kW bracket accounted for 43.12% of sales in 2025, while motors above 500 kW are set to grow at a 4.09% CAGR over the same period.

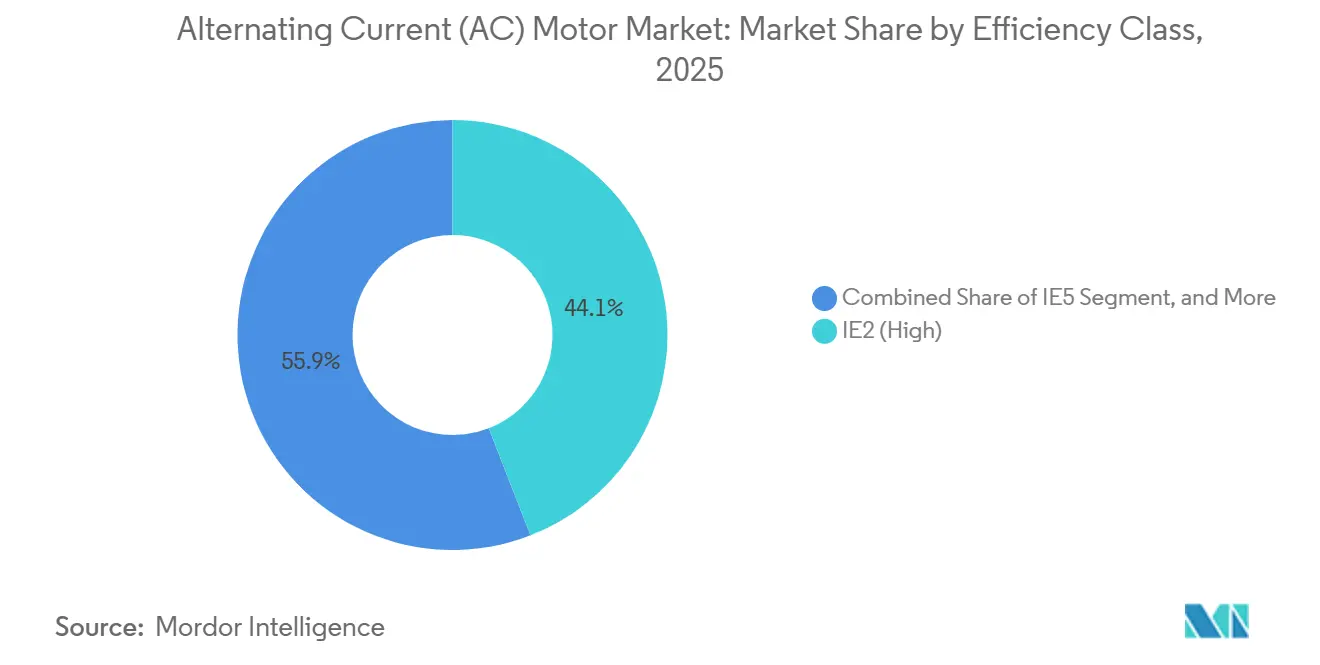

- By efficiency class, IE2 high-efficiency units represented 44.09% of the 2025 value, whereas IE4 super-premium motors should expand at a 4.28% CAGR through 2031.

- By end-user industry, discrete manufacturing accounted for 29.51% of 2025 revenue, yet water and wastewater treatment is predicted to grow at a 4.89% CAGR through 2031.

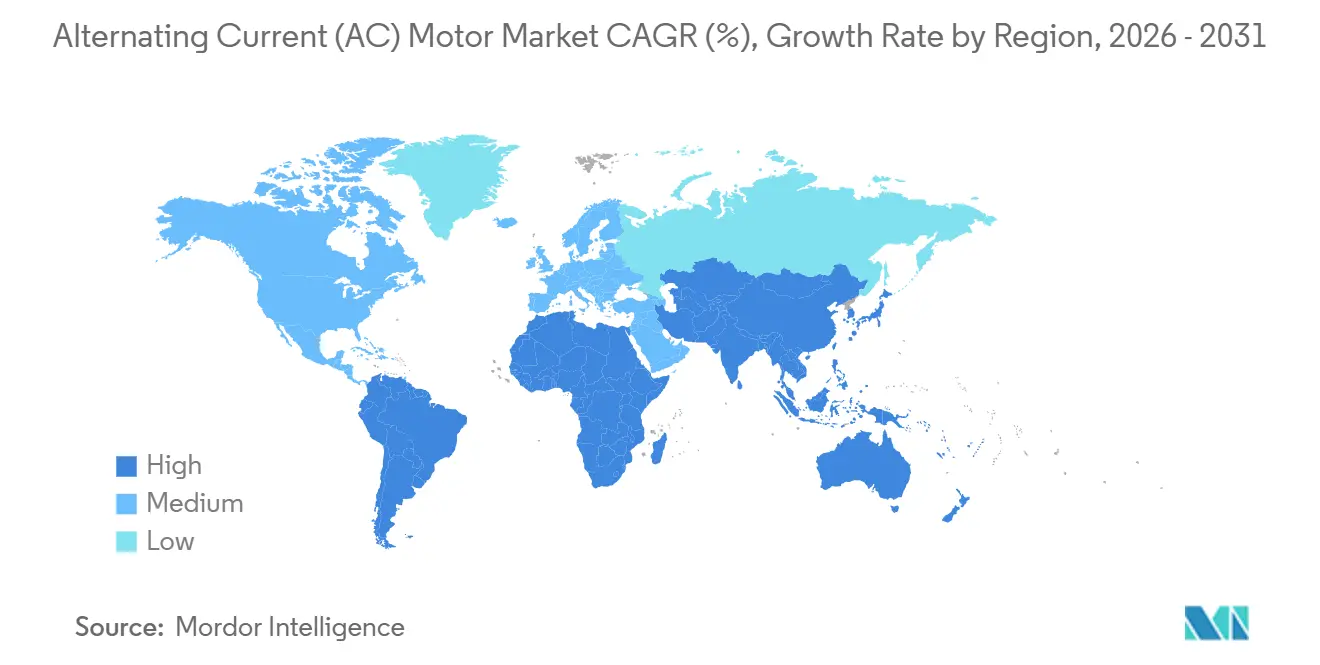

- By geography, Asia-Pacific delivered 56.41% of global turnover in 2025, while Africa is on track for the fastest growth at a 4.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Alternating Current (AC) Motor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory Energy-Efficiency Regulations | +1.2% | European Union, United States, China, India, global spillover | Medium term (2-4 years) |

| Rapid Industrial Automation and Robotics | +0.9% | Asia-Pacific core, North America and Europe spillover | Short term (≤ 2 years) |

| Expansion of Renewable-Energy Assets | +0.6% | China, United States, Germany, India | Long term (≥ 4 years) |

| HVAC/R Build-Out in Commercial Real Estate | +0.4% | North America, Europe, growing presence in Middle East | Medium term (2-4 years) |

| Rise of Axial-Flux PM Motors in E-Mobility | +0.3% | Europe and China EV hubs, early adoption in North America | Long term (≥ 4 years) |

| AI-Enabled Predictive-Maintenance Ecosystems | +0.5% | Global, led by discrete manufacturing in developed economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mandatory Energy-Efficiency Regulations Drive Accelerated Replacement Cycles

IE4 rules are now obligatory for motors above 0.75 kilowatts in the European Union, and IE3 minimums in China, the United States, and India are triggering early retirement of legacy IE1-IE2 fleets.[1] European Commission, “Ecodesign Regulation 2019/1781,” ec.europa.eu Compliance converges global product lines on super-premium platforms, favoring suppliers with scale manufacturing and harmonized certifications. For end users, a 75-kilowatt IE4 motor running 7,000 hours per year saves close to USD 1,200 in electricity costs, recovering the upfront price delta in under 3 years. Utilities and process industries that spend 60% or more of their operating budgets on motor power are therefore locking in multi-year procurement pipelines. As a result, the alternating current (AC) motor market is witnessing a structural pivot toward higher-efficiency design as the regulatory floor continues to rise.

Rapid Industrial Automation and Robotics Uptake Reshapes Motor Demand

Global robot installations topped 540,000 units in 2024, embedding millions of permanent-magnet servo motors with sub-millisecond positional accuracy.[2]International Federation of Robotics, “World Robotics 2025,” ifr.org Automotive and electronics assembly lines are shifting from pneumatic cylinders to servo actuation, cutting cycle times by more than 15% and energy draw by up to 50%. Collaborative-robot deployments are scaling fastest, requiring low-inertia frameless motors capable of a 10-millisecond safe-stop response. Warehouse automation adds further pull, with each autonomous mobile robot containing multiple small AC drives. Concentrated adoption in China, South Korea, and Japan ensures that Asia-Pacific remains the volume anchor of the alternating current (AC) motor market.

Expansion of Renewable-Energy Assets Multiplies Auxiliary-Motor Demand

Wind-turbine nameplate ratings are rising above 10 megawatts, and direct-drive permanent-magnet generators are displacing gearbox-based architectures to slash mechanical loss and maintenance. Each offshore turbine still needs dozens of auxiliary yaw, pitch, and cooling motors, creating a multiplier effect. On the solar side, single-axis trackers deploy thousands of sub-2-kilowatt motors per utility-scale plant; China’s 2024 installations alone implied more than 1.7 million units. Battery energy-storage co-locations add HVAC loads that lean on IE4-class compressor drives. The renewable build-out is therefore extending the alternating current (AC) motor market beyond traditional industrial confines.

HVAC/R Build-Out in Commercial Real Estate Sustains Baseline Growth

Commercial buildings are retrofitting variable-speed drive packages into chillers, air handlers, and cooling towers to meet tightening building-energy codes. In North America, heat-pump incentives are spurring replacement of gas furnaces with electrically driven compressors, each containing high-efficiency scroll or screw motors. Europe’s push toward near-zero-energy buildings mirrors the trend. Even in the Middle East, growth in district-cooling infrastructure is lifting demand for medium-voltage centrifugal chiller motors. Collectively, HVAC upgrades provide a dependable volume floor for the alternating current (AC) motor market across economic cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Copper and Rare-Earth Metal Prices | -0.8% | Global, acute across permanent-magnet supply chains | Short term (≤ 2 years) |

| High Upfront Cost of Premium-Efficiency Motors | -0.5% | South America, Africa, Southeast Asia | Medium term (2-4 years) |

| Power-Electronics Supply-Chain Bottlenecks | -0.4% | Global, most visible in automotive and renewable segments | Short term (≤ 2 years) |

| End-of-Life Recycling and Take-Back Compliance | -0.2% | European Union, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Copper and Rare-Earth Volatility Compresses Margins and Delays Orders

Copper traded between USD 8,000 and USD 10,500 per metric ton during 2024-2025, eroding the profitability of fixed-price contracts and prompting vendors to shorten quote validity to less than 30 days.[3]London Metal Exchange, “Copper Futures Historical Data 2024-2025,” lme.com Neodymium-iron-boron magnet prices rose 12-18% on tighter Chinese export quotas, raising material cost in permanent-magnet motors by up to USD 120 for a 20-kilowatt unit. In price-sensitive markets, buyers are back-specifying IE3 induction motors to sidestep rare-earth exposure, slowing the premium-efficiency trajectory of the alternating current (AC) motor market. Manufacturers are exploring ferrite-magnet or copper-rotor alternatives, but these options sacrifice torque density and complicate thermal design.

High Upfront Cost of Premium-Efficiency Motors Limits Penetration in Capital-Constrained Segments

IE4 motors command 40-60% price premiums over IE2 units, and the delta widens when variable-frequency drives and harmonic filters are added.[4]ABB Ltd., “Motion Division Annual Report 2024,” abb.com For small manufacturers in South America or Africa, an incremental USD 6,000 outlay for a 50-kilowatt motor exceeds annual maintenance budgets, extending payback periods beyond five years when electricity tariffs are below USD 0.08 per kilowatt-hour. Extended producer responsibility rules in the European Union and parts of Asia add an additional 2-4% to equipment costs. These economics temper the speed at which the alternating current (AC) motor market can transition to super-premium classes in emerging economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: Synchronous Designs Narrow the Gap

Induction AC motors led the alternating current (AC) motor market in 2025 with a 67.23% revenue share, underpinned by their rugged construction and low maintenance needs. They dominate pumps, fans, and conveyors that run across every industrial floor. Synchronous technology, although smaller in volume, is advancing at a 3.68% CAGR because permanent-magnet rotors add up to four percentage points of efficiency at full load. Robot builders, machine-tool makers, and electric-vehicle OEMs now specify synchronous drives for the tight torque response and compact frames that magnets enable.

Policy pressure is amplifying the shift. IE4 rules in the European Union and proposed U.S. mandates for IE4 reward synchronous adopters, prompting global OEMs to harmonize product lines and streamline inventory. Minerals processors are pairing megawatt-class synchronous motors with medium-voltage silicon-carbide drives, trimming electrical losses and switchgear footprints IEC.CH. As life-cycle analyses place a premium on kilowatt-hour savings, the alternating current (AC) motor market size is likely to tilt further toward synchronous formats through the decade.

By Voltage Class: Medium Voltage Gains Strategic Favor

Low-voltage motors below 1 kV captured 84.23% of 2025 revenue, reflecting their ubiquity in HVAC, food processing, and packaging. Variable-frequency drives coupled to these units allow soft starts and energy-saving speed control. Medium-voltage platforms between 1 kV and 11 kV are, however, the fastest risers at a 3.89% CAGR, as oil, gas, and metals operators consolidate several low-voltage feeders into single high-horsepower shafts, slicing copper mass by as much as 30% per installation.

Efficiency mandates currently stop at 1 kV, giving project owners latitude to negotiate bespoke performance benchmarks that favor vendors able to verify field efficiency through digital twins. Silicon-carbide power devices now featured in 6.6 kV and 11 kV drives cut switching losses by half, enabling smaller heat sinks and cabinets. These space and energy benefits dovetail with refinery, LNG, and desalination megaprojects in the Middle East and Asia, cementing medium-voltage as a strategic growth segment of the alternating current (AC) motor market.

By Power Rating: Volume at the Low End, Margin at the High End

Motors rated 1-100 kW delivered 43.12% of 2025 sales as universal workhorses across discrete factories and municipal water systems. Appliance makers are now installing IE3 or better induction frames even in fractional-horsepower sizes to meet Energy Star targets. Units above 500 kW, while smaller in count, are advancing at a 4.09% CAGR because LNG trains, mine ventilators, and desalination pumps require multi-megawatt drives that cost well into six figures each.

Edge analytics sensors costing less than 5% of asset value unlock predictive maintenance for these big machines, preventing bearing or insulation failures that can idle continuous-process sites for days. Data-center builders are also adopting 250-500 kW permanent-magnet fans to push power-usage effectiveness toward 1.2. The resulting barbell profile keeps entry-level segments dominant in unit count while positioning megawatt-scale equipment as the margin engine of the alternating current (AC) motor market.

By Efficiency Class: IE4 Emerges as the New Baseline

IE2 high-efficiency motors led with 44.09% of the 2025 value because they remain legal in several emerging markets and cost less up front. IE4 super-premium models are rising fastest at a 4.28% CAGR as utilities, data centers, and water utilities migrate to super-premium frames that pay back in under three years at industrial electricity tariffs. IE5 ultra-premium offerings, although scarce, serve semiconductor production and other around-the-clock loads willing to pay for every extra efficiency point.

IE1 designs are already banned in the European Union, China, and the United States, shrinking their addressable niche to legacy spares. Corporate ISO 50001 rollouts and green-building credits are also nudging buyers toward IE4 or better, accelerating the retreat of IE2 models from new-build specifications. Taken together, these forces make IE4 the de facto floor for new tenders by the late 2020s, reshaping the alternating current (AC) motor market toward higher-tier technology.

By End-User Industry: Water Infrastructure Surges, Discrete Manufacturing Holds Volume

Discrete manufacturing commanded 29.51% of 2025 revenue, with automotive and electronics plants operating thousands of induction and servo motors each. Production throughput and robotic penetration keep the segment firmly ahead in unit volume. Water and wastewater treatment, buoyed by USD 50 billion in U.S. infrastructure grants, is clocking the fastest expansion at a 4.89% CAGR as municipalities upgrade aging constant-speed pumps to IE4 variable-speed packages.

Oil and gas demand centers on explosion-proof, medium-voltage equipment able to withstand hydrogen sulfide atmospheres and 60 °C ambient temperatures. Chemicals and petrochemicals pay premiums for corrosion-resistant stainless housings, while mining specifies IP66 ingress protection for dusty sub-surface workings. Food and beverage processors round out the profile with stainless-steel wash-down motors certified to NSF hygiene codes. Collectively, these tailored specifications create a diverse yet resilient revenue blend for the alternating current (AC) motor market.

Geography Analysis

Asia-Pacific produced 56.41% of global revenue in 2025, headlined by China’s domestic output of more than 300 million units. Robot deployment density, 3.8 units per 1,000 workers in South Korea, locks in servo demand, while India’s IE3 mandate for motors above 0.75 kW is driving an early replacement wave across textiles and steel. Japan commands premium pricing thanks to the rapid uptake of IE5 frames in precision equipment, and Australia’s mining sector relies on >500 kW drives for haulage and crushing, boosting regional value intensity.

North America and Europe together delivered about 35% of 2025 revenue. The United States is mid-cycle on USD 50 billion in water-sector grants, with procurements peaking in 2025-2026, advancing the adoption of IE4 in municipal treatment works. Europe’s Ecodesign Regulation 2019/1781 already requires IE4 to be down to 0.12 kW by mid-2025, tightening upgrade timetables for building services and light manufacturing. Germany alone accounted for 28% of European sales as its machinery exporters modernize servo footprints, while the United Kingdom is pivoting toward heat-pump compressors to decarbonize building heating.

Africa is the fastest-growing region, charting a 4.22% CAGR to 2031 on the back of USD 25 billion in African Development Bank electrification projects targeting Egypt, South Africa, and Nigeria. South African mines are retrofitting IE3-IE4 ventilators to curb power costs that exceed 40% of operating expense, and Egypt’s planned industrial cities will need tens of thousands of motors for water and HVAC loads. Nigeria’s new rail corridor is stimulating cement, food-processing, and textiles clusters. The Middle East adds steady volume from desalination and district-cooling, while South America’s growth is anchored by Brazil, where local producer WEG leverages five-week lead times to outsell imports.

Competitive Landscape

The alternating current (AC) motor market shows moderate consolidation: ABB, Siemens, WEG, Nidec, and Regal Rexnord together earned 38% of 2025 revenue. Strategic focus aligns on efficiency leadership, digital-service bundling, and power-electronics integration. ABB’s 2025 launch of an IE5 synchronous-reluctance line with snap-fit construction halves disassembly time, boosting copper recovery to 91%. Siemens committed EUR 200 million (USD 220 million) to expand Bad Neustadt output for IE5 motors, raising capacity by 150,000 units by 2027.

Nidec’s motors-as-a-service model bundles hardware, analytics, and uptime guarantees into per-hour fees, shifting capital burden off balance sheets. WEG invested USD 120 million in a greenfield Indian plant that will produce 500,000 low-voltage units annually, sidestepping 18% import duties. Axial-flux innovators such as YASA, now owned by Mercedes-Benz, showcase 3 kW/kg power density, challenging radial-flux incumbents in e-mobility. Air-core stator newcomer Infinitum Electric halves unit weight, eliminates electrical steel, and targets HVAC fans and conveyors. Digital differentiation is rising: Rockwell Automation’s FactoryTalk controller reaches 94% bearing-failure prediction accuracy, eclipsing threshold-based alarms by 26 points.

Barriers to entry tighten in oil and gas, where IECEx and ATEX hazardous-area certifications demand costly testing. Patent filings concentrate on rare-earth-free rotor topologies and direct-oil cooling for thermal limits above 10 kW/kg, with ABB registering 47 such patents in 2024. Regional specialists, Kirloskar Electric in India and TECO in Taiwan, exploit localized service to win short-lead contracts, yet rising efficiency rules could tilt share toward scale brands that amortize R&D across global volumes.

Alternating Current (AC) Motor Industry Leaders

ABB Ltd.

Siemens AG

WEG Equipamentos Elétricos S.A.

Nidec Corporation

Regal Rexnord Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Siemens announced a EUR 200 million (USD 220 million) expansion of its Bad Neustadt motor factory, adding 80,000 m² of floor space for IE5 production and creating 450 jobs.

- December 2025: Nidec completed its USD 1.8 billion acquisition of Kollmorgen, strengthening motion-control reach in semiconductors, medical robotics, and aerospace.

- November 2025: WEG committed USD 120 million to build a Nashik, India, plant capable of 500,000 low-voltage motors yearly by 2027.

- October 2025: ABB introduced the M3BP IE5 synchronous-reluctance series, 0.75-355 kW, achieving >96% full-load efficiency without rare-earth magnets.

Global Alternating Current (AC) Motor Market Report Scope

The Alternating Current (AC) Motor Report is Segmented by Motor Type (Induction AC Motors, Synchronous AC Motors), Voltage Class (Low Voltage, Medium Voltage, High Voltage), Power Rating (Less Than 1 kW, 1 to 100 kW, 100 to 500 kW, Greater Than 500 kW), Efficiency Class (IE1, IE2, IE3, IE4, IE5), End-User Industry (Oil and Gas, Chemicals and Petrochemicals, Power Generation, Water and Wastewater, Metals and Mining, Food and Beverage, Discrete Manufacturing, Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Motor Type

| Induction AC Motors | Single-Phase |

| Poly-Phase | |

| Synchronous AC Motors | DC-Excited Rotor |

| Permanent-Magnet | |

| Hysteresis | |

| Reluctance |

By Voltage Class

| Low Voltage (Less Than 1 kV) |

| Medium Voltage (1 to 11 kV) |

| High Voltage (More Than 11 kV) |

By Power Rating

| Less Than 1 kW |

| 1 to 100 kW |

| 100 to 500 kW |

| Greater Than 500 kW |

By Efficiency Class

| IE1 (Standard) |

| IE2 (High) |

| IE3 (Premium) |

| IE4 (Super-Premium) |

| IE5 (Ultra-Premium) |

By End-User Industry

| Oil and Gas |

| Chemicals and Petrochemicals |

| Power Generation |

| Water and Wastewater |

| Metals and Mining |

| Food and Beverage |

| Discrete Manufacturing |

| Other End-User Industries |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Motor Type | Induction AC Motors | Single-Phase |

| Poly-Phase | ||

| Synchronous AC Motors | DC-Excited Rotor | |

| Permanent-Magnet | ||

| Hysteresis | ||

| Reluctance | ||

| By Voltage Class | Low Voltage (Less Than 1 kV) | |

| Medium Voltage (1 to 11 kV) | ||

| High Voltage (More Than 11 kV) | ||

| By Power Rating | Less Than 1 kW | |

| 1 to 100 kW | ||

| 100 to 500 kW | ||

| Greater Than 500 kW | ||

| By Efficiency Class | IE1 (Standard) | |

| IE2 (High) | ||

| IE3 (Premium) | ||

| IE4 (Super-Premium) | ||

| IE5 (Ultra-Premium) | ||

| By End-User Industry | Oil and Gas | |

| Chemicals and Petrochemicals | ||

| Power Generation | ||

| Water and Wastewater | ||

| Metals and Mining | ||

| Food and Beverage | ||

| Discrete Manufacturing | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What CAGR is forecast for global AC motors between 2026-2031?

The alternating current (AC) motor market is projected to grow at a 3.32% CAGR over 2026-2031.

Which efficiency class is expanding fastest?

IE4 super-premium motors are advancing at a 4.28% CAGR, the quickest among all efficiency tiers.

Why are medium-voltage motors gaining favor in heavy industry?

They cut copper usage and switchgear footprint, lowering both capex and lifetime energy losses.

How large is Asia-Pacific’s share of worldwide AC-motor revenue?

The region generated 56.41% of global sales in 2025, anchored by China’s massive production base.

Which end-user will grow most quickly through 2031?

Water and wastewater treatment is expected to rise at a 4.89% CAGR, driven by infrastructure grants.

What factors limit premium-efficiency uptake in emerging markets?

High upfront costs and volatile copper and rare-earth prices extend payback periods beyond five years.

Page last updated on: