Market Overview

| Study Period | 2025 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

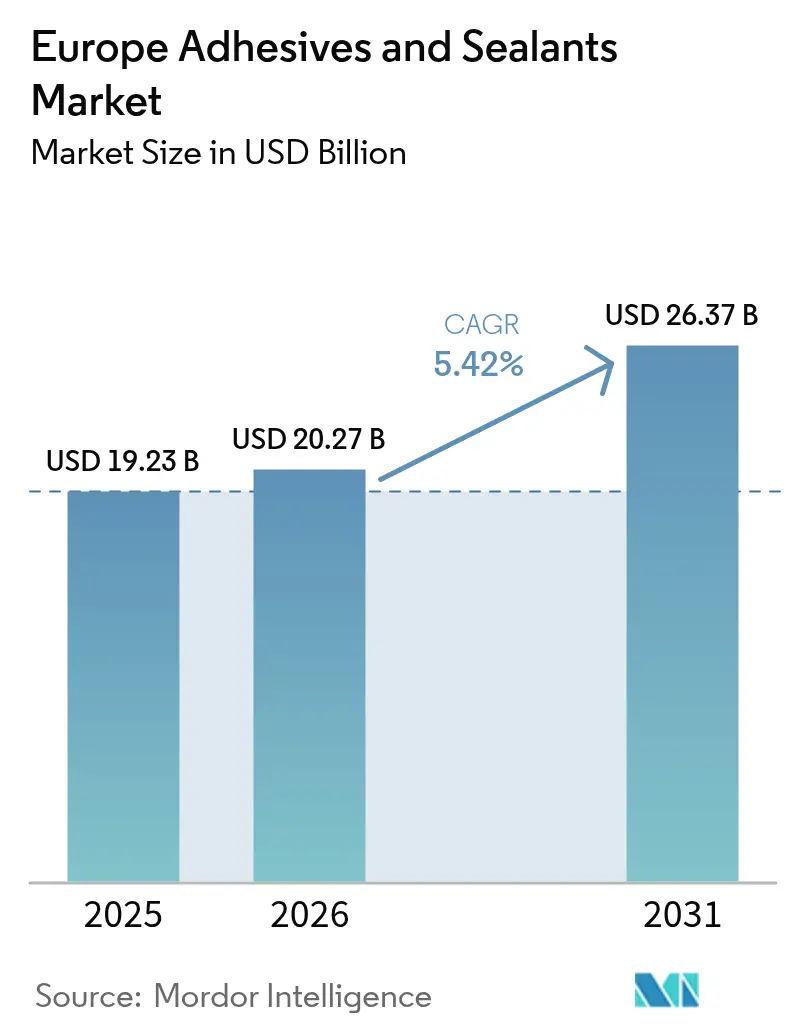

| Base Year Market Size (2025) | USD 19.23 Billion |

| Market Size (2026) | USD 20.27 Billion |

| Market Size (2031) | USD 26.37 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

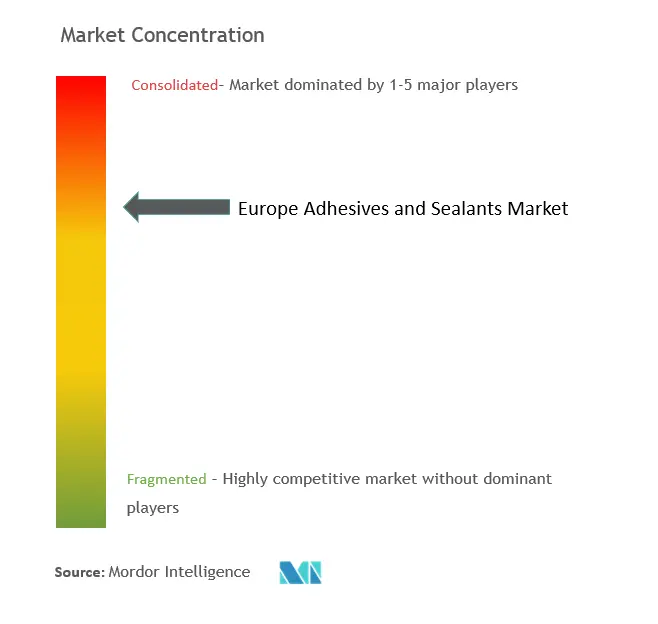

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Adhesives And Sealants Market Analysis by Mordor Intelligence

The Europe Adhesives And Sealants Market size in 2026 is estimated at USD 20.27 billion, growing from 2025 value of USD 19.23 billion with 2031 projections showing USD 26.37 billion, growing at 5.42% CAGR over 2026-2031. This trajectory reflects the sector’s ability to navigate stringent EU Green Deal regulations while capitalizing on construction recovery, automotive lightweighting mandates, and renewable-energy expansion. Water-borne systems gain traction as VOC limits tighten, and UV-cured chemistries accelerate line speeds in electronics and automotive plants. German infrastructure outlays underpin steady demand, while Spain’s renewable build-out positions it as the region’s quickest-growing buyer of structural bonding solutions. Competitive intensity remains moderate, with large incumbents refocusing portfolios on bio-based resins and acquisition-driven capability expansion to safeguard margins against feedstock price volatility and carbon-reduction costs.

Key Report Takeaways

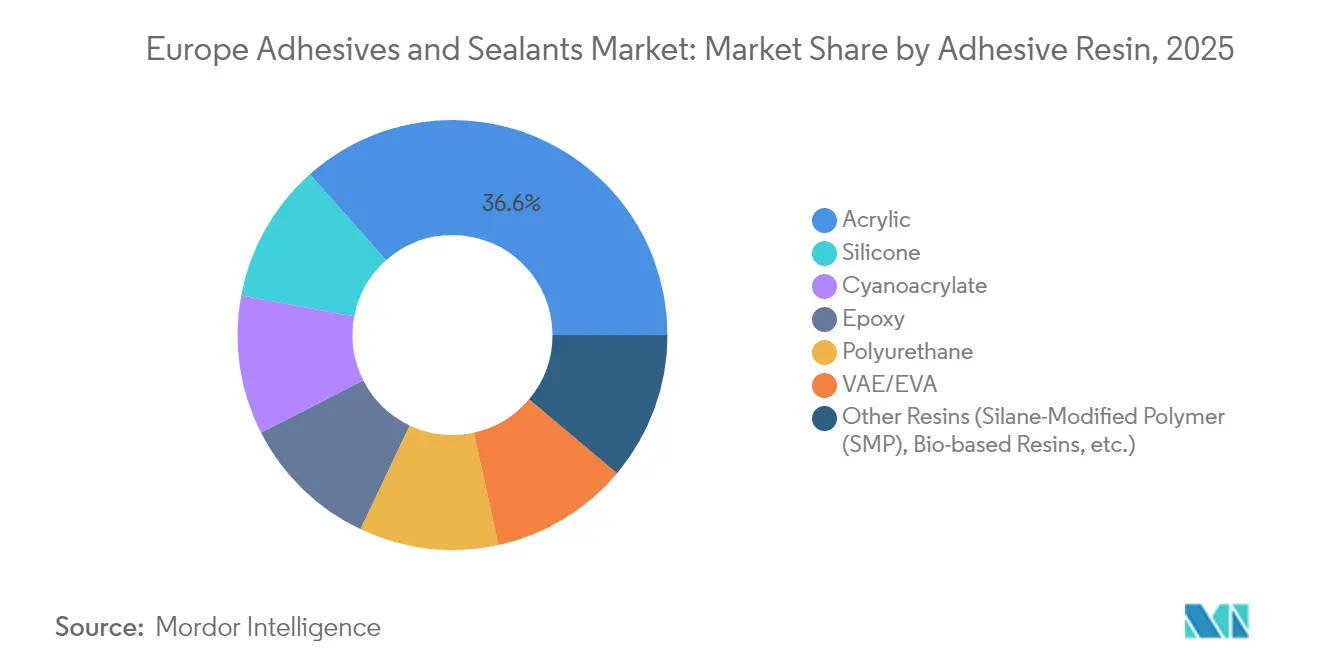

- By adhesive resin, acrylics captured 36.55% of the European adhesives and sealants market share in 2025; other resins will expand at 6.58% CAGR over 2026-2031.

- By technology, waterborne platforms commanded 42.70% share of the European adhesives and sealants market size in 2025, while UV-cured systems are projected to grow 6.21% CAGR through 2031.

- By sealant resin, silicone products led with 32.10% revenue in 2025, whereas hybrid and other chemistries are forecast to rise 5.63% CAGR.

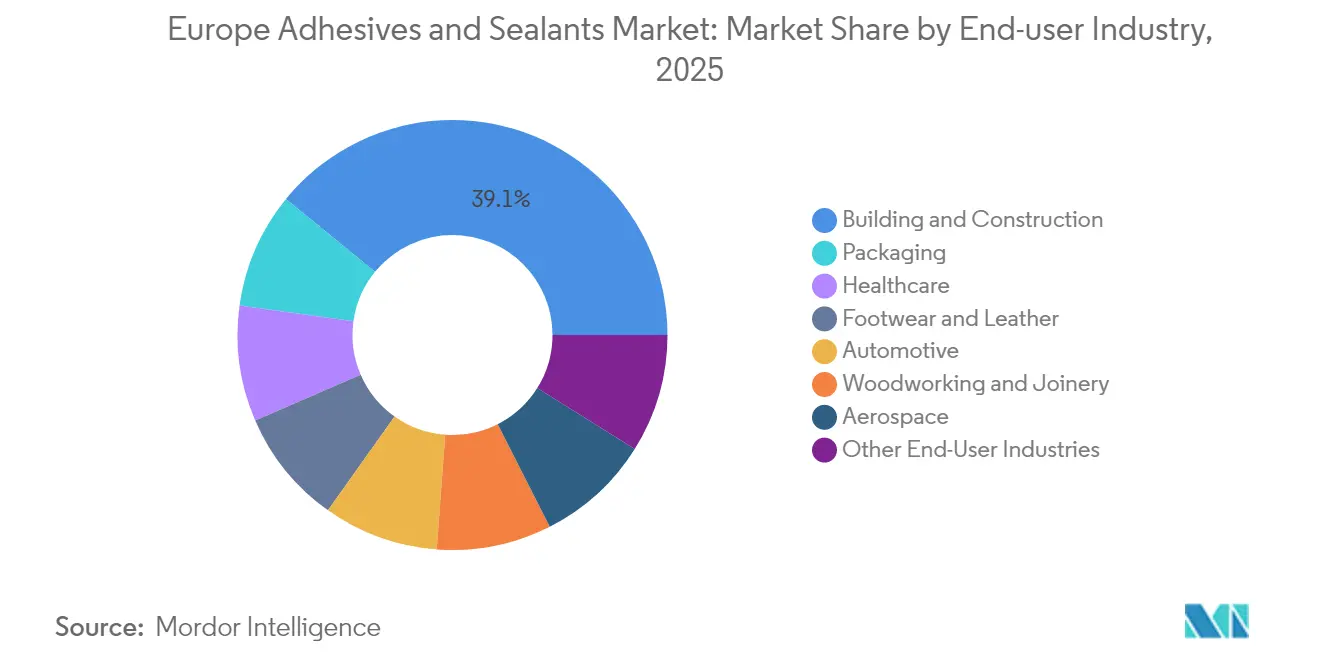

- By end-user industry, building and construction held 39.10% of Europe's adhesives and sealants market share in 2025; other industries are set to record the fastest 5.96% CAGR to 2031.

- By geography, Germany represented 21.95% of 2025 revenue; Spain is expected to deliver a 5.58% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Adhesives And Sealants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from residential renovation | +1.2% | Germany, France, Nordic countries | Medium term (2-4 years) |

| Surge in e-commerce packaging volumes | +0.8% | Germany, UK, Netherlands | Short term (≤ 2 years) |

| Accelerating lightweighting in the auto industry | +1.0% | Germany, France, Italy | Medium term (2-4 years) |

| Fast-growing wind-turbine blade bonding | +0.7% | Nordic countries, Germany, and Spain | Long term (≥ 4 years) |

| Prefab modular construction uptake | +0.6% | Nordic countries, Germany, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Residential Renovation

European renovation activity is gathering momentum as energy-efficiency mandates and post-pandemic lifestyle shifts lift spending on insulation, flooring, and window upgrades. The EU Renovation Wave aims to double building refurbishment rates by 2030, bolstering demand for continuous-bonding systems that eliminate thermal bridging. Germany’s EUR 50 billion (~USD 58.45 billion) annual renovation market increasingly specifies bio-based products such as Henkel’s LOCTITE HB S ECO, which cuts embodied CO₂ by more than 60% compared with fossil-based counterparts. Nordic suppliers pioneer factory-applied adhesives for prefabricated façade panels, allowing rapid site assembly while meeting stringent indoor-air-quality norms. This renovation push is set to sustain volume growth for the European adhesives and sealants market through 2028[1]Fraunhofer WKI, “Adhesives in Energy-Efficient Building Renovation,” wki.fraunhofer.de.

Surge in E-Commerce Packaging Volumes

Rising parcel shipments prompt converters to adopt high-speed, solvent-free bonding solutions compatible with paper-recycling guidelines published by FEICA. Flexible-packaging adhesives must balance bond strength and de-inkability while supporting mono-material designs that simplify recycling under the EU Plastics Strategy. Germany and the Netherlands are upgrading automated lines that require tight viscosity control and quick setting. These trends underpin incremental gains for the European adhesives and sealants market, especially in hot-melt and waterborne grades engineered for rapid throughput[2]FEICA, “Guidelines for Paper Recycling Adhesives,” feica.eu.

Accelerating Lightweighting in European Auto Industry

Modern vehicles incorporate more than 400 linear feet of adhesive, up from 30 feet in 2001, to bond steel-aluminum structures and reinforce battery enclosures. DuPont BETAMATE enabled a 30% weight reduction in the TX5 electric taxi, while Sika’s thermally conductive lines address battery thermal management. German OEMs deploy precision-dispensing robots to meet 2030 emissions targets, propelling structural adhesive volumes in the European adhesives and sealants market.

Fast-Growing Wind-Turbine Blade Bonding Market

Larger composite blades rely on epoxy and polyurethane systems providing fatigue resistance under cyclic loads. Research into acrylic-matrix composites promises recyclability advantages, and debondable chemistries are being developed for end-of-life blade disassembly. Sweden’s green-industrial program and Spanish coastal wind farms amplify structural-bonding consumption over the long term.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Environmental Concerns | -0.9% | EU-wide, particularly Germany and Nordic countries | Medium term (2-4 years) |

| Volatile Feedstock Prices | -1.1% | Germany, France, Netherlands | Short term (≤ 2 years) |

| Skill Gap in Robotic Adhesive-Dispensing Workforce | -0.8% | Germany, Italy, Nordic countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Environmental Concerns

REACH diisocyanate restrictions effective August 2023 force reformulation of polyurethane systems or mandatory worker training, while formaldehyde emission ceilings effective August 2026 drive shifts to ultra-low-emission grades. The addition of 247 SVHCs, including octamethyltrisiloxane, extends regulatory uncertainty. Sustainability investment needs 70% higher annual capital outlays across Europe’s chemical sector, compressing margins yet spurring long-run innovation in bio-based feedstocks.

Volatile Feedstock Prices

Natural-gas-driven electricity spikes since the Russia-Ukraine conflict, alongside supply disruptions, have cut European chemical output volumes. BASF’s switch to bio-based ethyl acrylate carries a price premium that customers must absorb. Producers now prioritize cost discipline and capacity rationalization, potentially crimping near-term expansion prospects for the European adhesives and sealants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Adhesive Resin: Bio-Based Alternatives Challenge Acrylic Dominance

Acrylics retained 36.55% revenue share of the European adhesives and sealants market in 2025, thanks to versatility and adhesion to diverse substrates. Other resins, including bio-based innovations, are forecast to expand 6.58% CAGR to 2031 as carbon-reduction mandates intensify. Europe adhesives and sealants market size for bio-based grades is projected to widen as BASF’s renewable ethyl acrylate rolls out and xylan hot-melts demonstrate 30 MPa lap-shear while remaining reusable. Cyanoacrylates gain traction in electronics miniaturization, and polyurethane formulators pursue moisture-curing systems that bypass diisocyanate training. Silicone chemistries grow in high-temperature segments, whereas VAE/EVA retains cost-driven niches.

By Adhesive Technology: UV-Cured Innovation Outpaces Water-Borne Leadership

Waterborne platforms accounted for 42.70% of the 2025 revenue base, reflecting entrenched production lines and alignment with VOC caps. UV-cured systems, however, will post a 6.21% CAGR through 2031 as assembly plants seek instant-bond processing. Panacol’s black UV epoxies cure in thicker layers, eliminating shadow areas, and are now specified in EV motor wire stress-relief joints.

Reactive hot melts combine rapid set with strong final bonds, serving high-speed packaging lines. Solvent-borne demand persists in aerospace, where long open time is critical, but higher-solids versions help meet tightening emission norms. Equipment upgrades toward LED-UV lamps cut energy use and further incentivize technology switching in the European adhesives and sealants market.

By Sealant Resin: Silicone Versatility Drives Market Leadership

Silicone grades delivered 32.10% of 2025 turnover owing to durability in façade joints and automotive glazing. Hybrid silane-modified-polymer sealants are predicted to log a 5.63% CAGR, merging silicone weathering with polyurethane adhesion. Medical care adopts Wacker’s SILPURAN tapes for atraumatic removal, while construction sites demand low-modulus SMP products compatible with damp substrates. Polyurethane sealants tweak isocyanate levels to meet training thresholds, and epoxies satisfy chemical-resistant flooring. Ongoing research and development into renewable polyols and fume-free curing aids the transition to lower-carbon offerings within the European adhesives and sealants market.

By End-User Industry: Renewable Energy Diversification Challenges Construction Dominance

Building and construction supplied 39.10% of revenue in 2025 as renovation incentives and energy-efficiency codes sustained adhesive uptake in insulation and flooring. Renewable energy and electronics will outpace at 5.96% CAGR, enlarging the Europe adhesives and sealants market size for specialty structural adhesives in turbine blades and thermally conductive pastes for EV batteries. Automotive lightweighting continues, with structural bonding replacing spot welds, and aerospace recovers as fleet renewals progress. Packaging formulators build solvent-free laminating capability, while healthcare acquisitions by H.B. Fuller expand wound-closure solutions in a bid to offset cyclical construction exposure.

Geography Analysis

Germany’s 21.95% revenue weight in 2025 stems from EUR 500 billion infrastructure plans that maintain a baseline of construction sealant demand. The country’s auto sector, though confronted by EV transition headwinds, keeps investing in bonding robots that enhance precision and reduce weld spatter. The Europe adhesives and sealants market size is attached to Germany is supported by deep supplier networks and research and development clusters around Cologne and Düsseldorf.

Spain is forecast to log a 5.58% CAGR as wind-turbine component plants in Galicia and Valencia expand capacity to meet EU renewable targets. Construction modernization programs integrating modular timber frames also boost the consumption of moisture-curing polyurethane adhesives.

The United Kingdom maintains resilient niches in roofing and specialty composites, aided by Sika’s acquisition of Cromar Building Products. France leans on renovation subsidies and industrial policy backing for sustainable chemistry, but high electricity tariffs temper growth. Italy progresses on bonus-driven façade upgrades.

Eastern European cohesion-fund projects strengthen demand in Poland and Romania, while the Russia market remains constrained by sanctions that limit feedstock flows and technology transfer, thereby reshaping trade routes within the broader Europe adhesives and sealants market.

Competitive Landscape

The European adhesives and sealants market is consolidated in nature. Strategic moves focus on vertical integration and specialty niches. Automation investments proliferate, with in-line quality monitoring and robotic dispensing reducing scrap rates and meeting OEM audit requirements. Feedstock volatility drives interest in local sourcing agreements, though production scale keeps petrochemical majors central to supply. Technology leadership and sustainability credentials underpin pricing power in the European adhesives and sealants market.

Europe Adhesives And Sealants Industry Leaders

Sika AG

H.B. Fuller Company

3M

Arkema

Henkel AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Henkel and Nordmeccanica elevated their three-decade collaboration to a strategic partnership, co-developing low-VOC adhesive-laminating technology for European converters.

- December 2024: H.B. Fuller acquired Medifill Ltd. and signed a provisional agreement for GEM S.r.l., reinforcing its European wound-closure platform

- May 2024: Dow expanded capacity at SAS Chemicals GmbH in Böhlen, Germany to boost organic, hybrid, and silicone sealant output for insulating-glass assemblies.

Europe Adhesives And Sealants Market Report Scope

Adhesives are made from a combination of resins, additives, and solvents. The composition of the resins and additives entirely depends on the end-user industry in which they are used. The market is segmented by resin type, technology, end-user industry, and geography. By Adhesive resin type, the market is segmented into acrylic, cyanoacrylate, epoxy, polyurethane, silicone, VAE/EVA, and other resins. Concerned about technology, the market is segmented into the hot melt, reactive, solvent-borne, UV-cured, and waterborne. By sealant resin type, the market is segmented into polyurethane, epoxy, acrylic, silicone, and other resin types. By end-user industry, the market is segmented into aerospace, automotive, building and construction, footwear and leather, healthcare, packaging, woodworking and joinery, and other end-user industries. By geography, the market is distributed among the following countries: France, Germany, Italy, Russia, Spain, the United Kingdom, and the rest of Europe. The report offers market size and forecasts in terms of both revenue (USD million) and volume (kilotons) for all the above segments.

By Adhesive Resin

| Acrylic |

| Cyanoacrylate |

| Epoxy |

| Polyurethane |

| Silicone |

| VAE / EVA |

| Other Resins (Silane-Modified Polymer (SMP), Bio-based Resins, etc.) |

By Adhesive Technology

| Hot-Melt |

| Reactive |

| Solvent-Borne |

| UV-Cured |

| Water-Borne |

By Sealant Resin

| Polyurethane |

| Epoxy |

| Acrylic |

| Silicone |

| Other Resins (Polysulfide, SMP Hybrid, etc.) |

By End-User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Woodworking and Joinery |

| Other End-User Industries (Renewable Energy,Electronics and Appliances, etc.) |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| NORDIC Countries |

| Rest of Europe |

| By Adhesive Resin | Acrylic |

| Cyanoacrylate | |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| VAE / EVA | |

| Other Resins (Silane-Modified Polymer (SMP), Bio-based Resins, etc.) | |

| By Adhesive Technology | Hot-Melt |

| Reactive | |

| Solvent-Borne | |

| UV-Cured | |

| Water-Borne | |

| By Sealant Resin | Polyurethane |

| Epoxy | |

| Acrylic | |

| Silicone | |

| Other Resins (Polysulfide, SMP Hybrid, etc.) | |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Woodworking and Joinery | |

| Other End-User Industries (Renewable Energy,Electronics and Appliances, etc.) | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe adhesives and sealants market?

The market is worth USD 20.27 billion in 2026 and is projected to grow to USD 26.37 billion by 2031.

Which end-user industry holds the largest share?

Building and construction leads with 39.10% share in 2025, driven by renovation and energy-efficiency mandates.

Which adhesive technology is growing fastest?

UV-cured systems are expected to expand at a 6.21% CAGR through 2031 owing to instant-bond processing benefits.

Why is Spain the fastest-growing geography?

Spain’s 5.58% CAGR outlook stems from robust wind-energy investments and construction-modernization programs.

How are regulations influencing product development?

REACH restrictions on diisocyanates and formaldehyde, plus VOC limits, accelerate shifts to water-borne, UV-cured, and bio-based chemistries.

Page last updated on: