Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

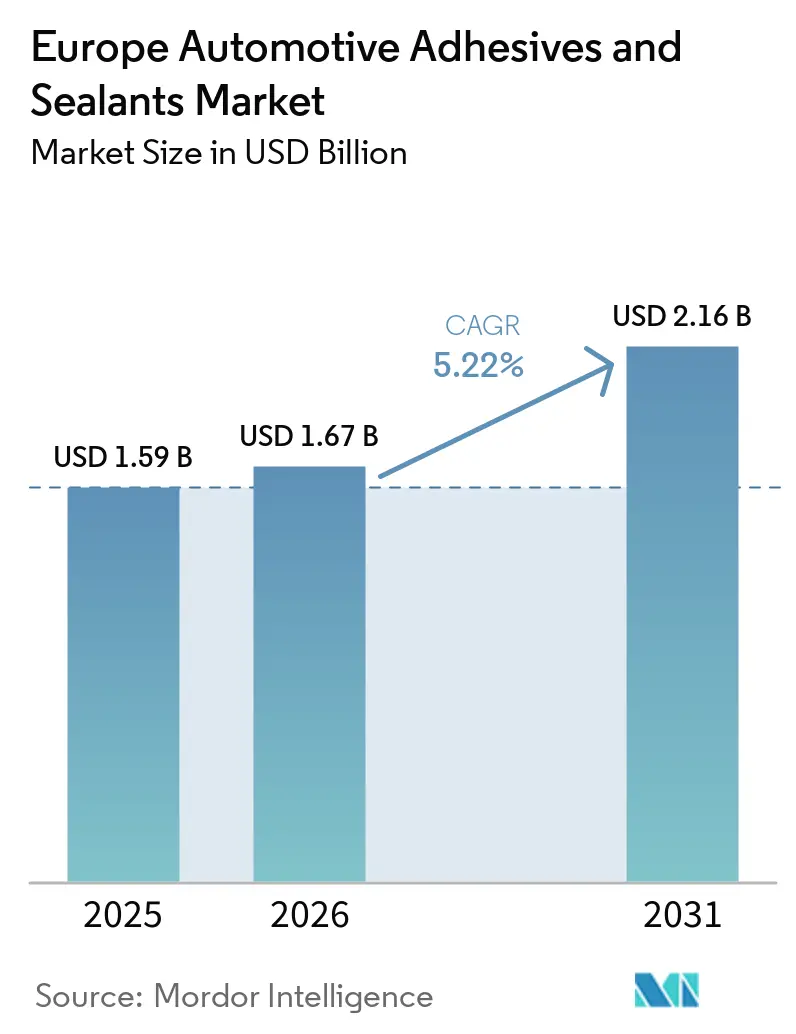

| Base Year Market Size (2025) | USD 1.59 Billion |

| Market Size (2026) | USD 1.67 Billion |

| Market Size (2031) | USD 2.16 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automotive Adhesives And Sealants Market Analysis by Mordor Intelligence

The Europe Automotive Adhesives And Sealants Market size was valued at USD 1.59 billion in 2025 and is estimated to grow from USD 1.67 billion in 2026 to reach USD 2.16 billion by 2031, at a CAGR of 5.22% during the forecast period (2026-2031). EV (electric vehicle)-led power-train redesigns, stringent European Union (EU) volatile organic compound (VOC) regulations, and the adoption of inline robotic dispensing are influencing material selection. The industry is transitioning from solvent-borne chemistries to water-borne and reactive hot-melts. Polyurethane systems remain the primary choice for most structural joints, while vinyl acetate ethylene (VAE)/ethylene vinyl acetate (EVA) water-borne chemistries are increasingly used in roof-liner and interior lamination. This shift supports original equipment manufacturers (OEMs) in producing lighter, lower-emission vehicles that comply with Directive 2004/42/EC. Demand for thermally conductive adhesives is rising, driven by specifications for 60 gigawatt-hours (GWh) or more gigafactories in Germany and Spain. Meanwhile, supply chain constraints in dosing equipment are maintaining stable margins for formulators capable of ensuring timely delivery. Competition is intensifying as companies such as Henkel AG & Co. KGaA, Sika AG, 3M, Dow, and Arkema utilize integrated urethane chains to achieve 10-15% cost advantages over regional competitors.

Key Report Takeaways

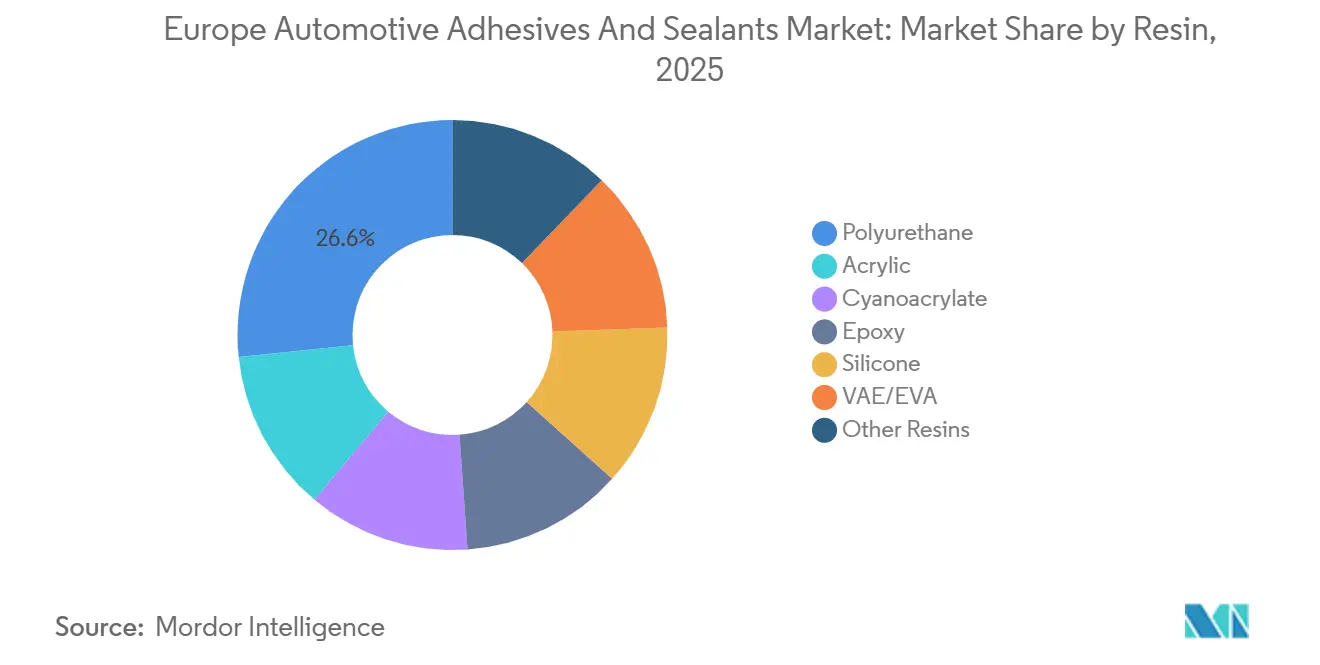

- By resin, polyurethane led with 26.63% of the Europe automotive adhesives & sealants market share in 2025, while VAE/EVA formulations are forecast to expand at a 5.88% CAGR through 2031.

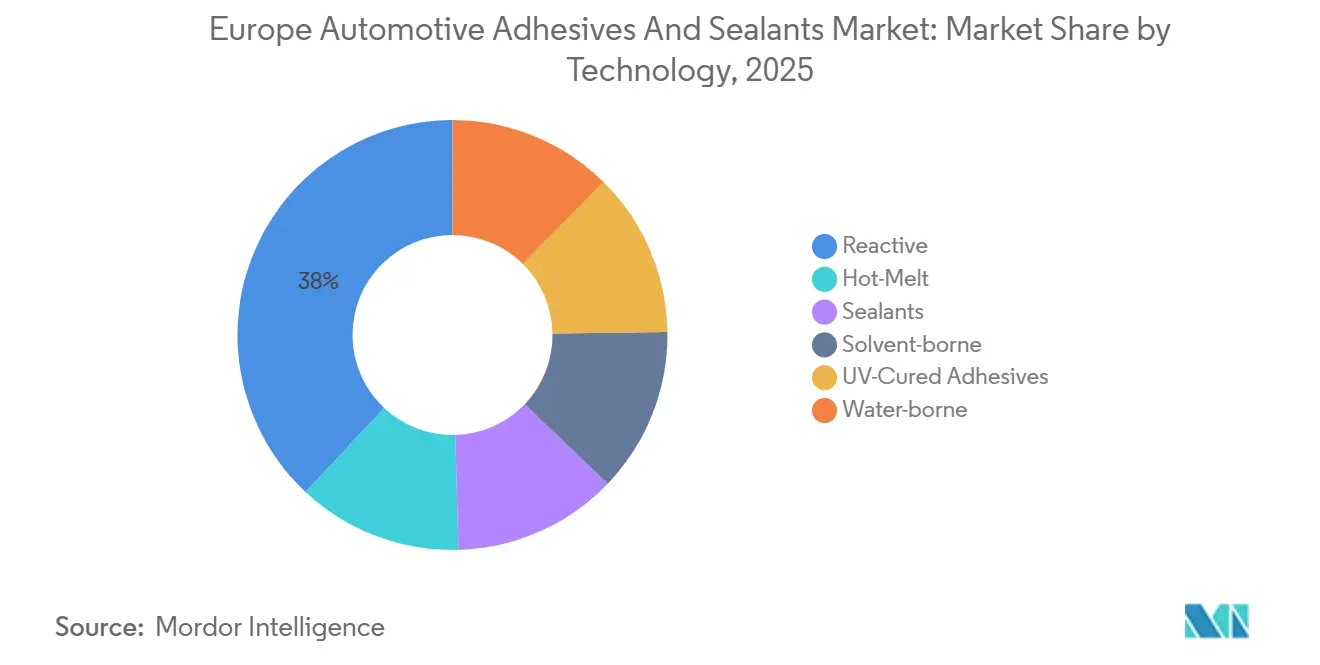

- By technology, reactive systems captured 38.02% revenue in 2025, whereas hot-melt adhesives are projected to advance at a 5.63% CAGR over 2026-2031.

- By geography, Germany accounted for 18.56% of 2025 revenue, but France is set to grow the fastest at a 6.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Automotive Adhesives And Sealants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweighting drive for EV and ICE vehicles | +1.2% | Germany, France, Spain, Italy, UK | Medium term (2-4 years) |

| EU VOC-reduction regulations accelerate low-VOC chemistries | +0.8% | EU-wide (Germany, France, Italy, Spain, UK primary) | Short term (≤ 2 years) |

| Surge in European EV battery-pack production | +1.0% | Germany, Spain, France, Hungary | Medium term (2-4 years) |

| In-line robotic dispensing boosts OEM throughput | +0.6% | Germany, Spain, the Czech Republic, and Slovakia | Short term (≤ 2 years) |

| Sensor-embedded "smart" structural adhesives emerge | +0.4% | Germany, UK, France (pilot deployments) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lightweighting Drive for EV and ICE Vehicles

Aluminum, composites, and mixed-material architectures are replacing traditional spot-welds with high-peel polyurethane and epoxy bonds. These bonding methods distribute loads effectively and reduce stress concentrations. Hydro achieved a 30% reduction in mass by replacing steel closures with aluminum, maintaining the material's 90% recyclability[1]Hydro, “Aluminum Lightweighting Solutions for Automotive,” hydro.com. BMW’s i-Series used elastomer-toughened epoxies to bond carbon fiber to aluminum, addressing thermal-expansion mismatches and protecting the fibers. Audi has improved its formulation cycles by utilizing artificial intelligence (AI)-driven finite-element simulations to evaluate potential chemistries, reducing qualification lead times. The European Union (EU) Automotive Package, which includes a EUR 1.8 billion (USD 2.10 billion) battery incentive, is encouraging original equipment manufacturers (OEMs) to reduce vehicle weight by 100-150 kilograms. This trend is driving the shift from traditional bolts to modern adhesive solutions.

EU VOC-Reduction Regulations Accelerate Low-VOC Chemistries

Directive 2004/42/EC has set a cap of 420 grams per liter (g/l) for volatile organic compounds (VOCs) in topcoats. This regulation is nudging formulators towards more eco-friendly routes, specifically water-borne and ultraviolet (UV)-cure methods. Henkel AG & Co. KGaA’s AQUENCE PL 5101, a one-component water-borne adhesive, eliminates the typical four-hour pot-life waste associated with two-part mixes. It also allows line flushes using soapy water. Tesa’s 52215 Ultra-Low-VOC tape is making progress in the heating, ventilation, and air conditioning (HVAC) sector, bonding recycled polypropylene seals while adhering to VDA 278 cabin-air standards. However, this tape has a drawback: its lower initial tack extends fixture times. Toyochem’s UV-curable TOYOMELT P-201 series addresses this challenge, offering instant curing and 100°C heat resistance, all without the use of solvents.

Surge in European EV Battery-Pack Production

New gigafactories are reshaping consumption patterns. Starting late 2026, Stellantis and Contemporary Amperex Technology Co., Limited (CATL)'s joint venture in Zaragoza, with a capacity of 50 gigawatt-hours (GWh), will utilize 2-3 kilograms of thermally conductive adhesive and 1-2 kilograms of structural adhesive for each battery pack[2]Stellantis, “Zaragoza Gigafactory Announcement,” stellantis.com. Northvolt Drei's 60 GWh facility in Germany is setting stringent specifications: a conductivity of over 2 watts per meter-kelvin (W/mK) and a dielectric strength exceeding 20 kilovolts per millimeter (kV/mm) to effectively manage thermal runaway. Dow’s VORATRON MA 8200 and Collano’s two-component polyurea systems are designed to meet these demanding thresholds. However, a bottleneck arises with high-viscosity dosing equipment, which is currently facing a 16-week lead time, hindering production ramp-ups. A 2025 technical review by Springer highlights the growing trend: battery modules are now consuming 40-50% more adhesive volume compared to traditional internal combustion engine (ICE) powertrains.

In-Line Robotic Dispensing Boosts OEM Throughput

Assembling EV platforms takes 20-30% more time, prompting a shift towards automation to counterbalance these cycle penalties. Henkel’s TECHNOMELT PUR 6221, a UV-curable adhesive, boasts a rapid curing time of seconds under UV light. It also features a fluorescent tracer for machine-vision quality control, enabling a throughput of over 60 jobs per hour on door-panel assembly lines. In 2025, Germany's production of 1.67 million EVs constituted 40% of the nation's total output, supported by the integration of robotic adhesive cells. Spain maintained a steady production of 2.25 million units, despite a 12.5% mix of electrified vehicles, due to robotic systems that kept takt times consistent. Eastern European plants, exporting 90% of their output, have embedded robots in 70-80% of their new production lines. In contrast, Italy's base, characterized by a significant presence of small and medium-sized enterprises (SMEs), lags behind with only 45% robot integration, primarily due to capital expenditure constraints.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Isocyanate price volatility | -0.7% | EU-wide, acute in Germany, Italy, and France | Short term (≤ 2 years) |

| REACH chemical-compliance costs | -0.5% | EU-wide (Germany, France, Netherlands primary) | Medium term (2-4 years) |

| Shortage of high-viscosity dosing equipment for battery lines | -0.3% | Germany, Spain, Hungary (gigafactory hubs) | Short term (≤ 2 years) |

| OEM certification delays for novel bio-based systems | -0.2% | Germany, France, Sweden (early-adopter OEMs) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Isocyanate Price Volatility

In early 2026, prices for Methylene Diphenyl Diisocyanate (MDI) and Toluene Diisocyanate (TDI) increased significantly due to Middle-East tensions disrupting feedstock supply routes. ICIS reported a polyol midpoint price increase of USD 450 per ton within a week. Producers such as BASF and Huntsman implemented price increases ranging from EUR 100 to 300 (USD 117.16 to 351.48) per ton, creating challenges for Tier-2 formulators without long-term contracts. Utilization rates remain around 82%, providing limited relief until new Chinese production capacity transitions to export-grade materials. Original Equipment Manufacturers (OEMs), already under pressure from electric vehicle (EV) margin constraints, are resisting cost pass-throughs, further compressing formulation EBITDA.

REACH Chemical-Compliance Costs

In April 2025, the European Chemicals Agency (ECHA) increased registration fees by 19.5%, impacting companies handling volumes of greater than or equal to 1,000 tons. The Annex XIV sunset for triphenyl phosphate necessitates expensive reformulation processes, expected to be completed between 2030 and 2032. Henkel introduced Technomelt PUR 6260 ECO, which contains greater than or equal to 60% renewable carbon, at a 20% price premium. Meanwhile, Bostik's hybrid sealant required 18 months of OEM testing, diverting Research and Development (R&D) resources that could have been allocated to performance enhancements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Polyurethane Holds Ground While Water-Borne Gains

Polyurethane accounted for 26.63% of the projected 2025 revenue, driven by its high peel strength (greater than 20 MPa) and impact resilience, which are critical for battery enclosures and body-in-white assemblies. Companies such as Henkel and Dow have invested USD 20 million in expanding a German reactive hot-melt production line to ensure supply. Meanwhile, vinyl acetate ethylene/ethylene vinyl acetate (VAE/EVA) water-borne chemistries are expected to grow at a compound annual growth rate (CAGR) of 5.88% through 2031, as original equipment manufacturers (OEMs) increasingly adopt low-volatile organic compound (VOC) solutions for dashboards and roof-liners. Epoxies continue to dominate module potting applications, with innovations such as Nagoya University’s epoxy-thermoplastic elastomer (TPE) hybrid demonstrating 22× impact strength, indicating long-term durability. Silicones, including WEVO-CHEMIE’s WEVOSIL 28015 FL, are gaining traction in high-temperature battery seals, meeting the demands of -40°C to +85°C cycling with elastic recovery.

The growth of VAE/EVA does not signal the decline of polyurethanes; instead, both chemistries are expected to coexist, addressing varying requirements for operating temperature and modulus across vehicle zones. For instance, Evonik’s VPS SIVO 260 silane promoters enhance polycarbonate adhesion by 27%, ensuring polyurethane remains relevant for transparent roof architectures. Additionally, circular-economy regulations are driving research into beta-amino-ester debondable epoxies, signaling a potential shift toward easier end-of-life disassembly in the coming decade.

By Technology: Reactive Systems Lead, Hot-Melts Accelerate

Reactive chemistries accounted for 38.02% of the projected 2025 revenue, with one-component epoxies, moisture-cure polyurethanes, and silane-terminated polymers providing cure-on-demand strength for mixed-material joints. SikaPower and Sikaflex product lines are integral to body-shop robotic cells, while Arkema’s Bostik division supplies modified silane (MS) polymer sealants that resist ultraviolet (UV)-induced chalking. Hot-melt adhesives are growing at a CAGR of 5.63%, with UV-curable polyurethane grades combining rapid curing times with automated quality control processes.

Solvent-borne systems are primarily used in aftermarket refinishing due to their 10-minute tack time and ambient curing capabilities, despite concerns regarding volatile organic compound (VOC) emissions. Ultraviolet (UV)-cure acrylates are utilized in specialized applications such as camera and sensor mounting, supported by the growth of advanced driver-assistance systems (ADAS). Water-borne dispersions are applied in instrument panels and noise, vibration, and harshness (NVH) laminates, although their slower setting times present a challenge. Overall, hybrid curing technologies are expected to redefine traditional boundaries, with polyurethane hot-melts incorporating UV triggers and epoxy systems using latent amine catalysts to enable faster snap-curing processes.

Geography Analysis

Germany is projected to remain a significant revenue contributor, accounting for 18.56% in 2025, driven by the production of 1.67 million electric vehicles (EVs), representing 40% of the country's total vehicle output. Battery-focused plants in Lower Saxony and Saxony utilize 2-3 kilograms of thermally conductive adhesive per vehicle, increasing the average material expenditure despite a 1% decline in total vehicle production anticipated in 2026. Northvolt’s Drei gigafactory is expected to consume 1,200-1,500 tons of adhesive annually at full capacity, boosting demand for fillers and dosing robots.

France is forecasted to grow at a compound annual growth rate (CAGR) of 6.34%, supported by the Stellantis/Contemporary Amperex Technology Co. Limited (CATL) investment in Zaragoza and the scaling of Renault’s E-Tech platform. This initiative will add 500,000 battery packs annually, requiring up to 2,000 tons of cell-to-plate adhesives. Domestic tier-one suppliers are adapting to low-volatile organic compound (VOC) regulations by retooling for water-borne interior bonding solutions. In contrast, Italy is expected to experience a decline in production, exposing its fragmented small and medium-sized enterprise (SME) supplier network to margin pressures. However, the country’s EUR 55.9 billion (USD 65.49 billion) components sector continues to invest in formulation kits for aftermarket collision repair, partially offsetting the volume decline.

Spain maintained stable vehicle production at 2.25 million units in 2025 while increasing the share of electrified vehicles, driven by Sagunto’s 50 gigawatt-hour (GWh) battery plant, which requires 1.5-2.0 kilograms of structural adhesive per battery pack. The United Kingdom’s 11% decline in manufacturing output is counterbalanced by a large vehicle parc of 40.2 million units, generating EUR 1.5-2.0 billion (USD 1.75-2.34 billion) in annual demand for body repair adhesives. In Eastern Europe, Czech and Slovak manufacturing plants have integrated robots into 80% of new production lines, utilizing fast-cure polyurethane (PUR) hot-melts to meet export delivery schedules. Meanwhile, Russia’s vehicle output remains 40-50% below pre-2022 levels, but demand for polyurethane sealants is supported by commercial vehicle production and aftermarket repainting activities.

Competitive Landscape

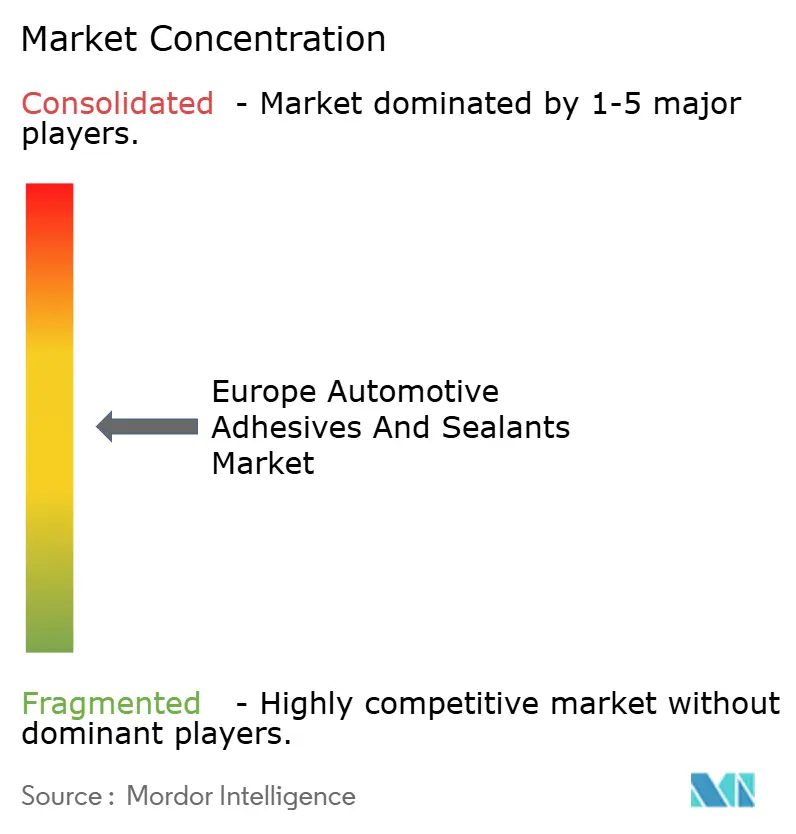

The Europe automotive adhesives & sealants market is moderately fragmented. Henkel AG & Co. KGaA, Sika AG, 3M, Dow, and Arkema are supported by captive methylene diphenyl diisocyanate (MDI), toluene diisocyanate (TDI), and epoxy production pathways. Henkel’s planned acquisition of ATP Adhesive Systems in January 2026 will integrate EUR 270 million (USD 316.34 million) in reactive hot-melt sales into its portfolio, enhancing its coverage of battery modules. Similarly, Sika’s acquisition of Akkim in February 2026 for CHF 220 million (USD 278.57 million) will expand its presence into Eastern Europe and Central Asia, leveraging Gestamp’s stamping plants, which are projected to achieve an electric vehicle (EV) mix exceeding 50% by 2027.

Dow, BASF, and Arkema continue to introduce high-conductivity urethanes, often collaborating with dosing-equipment specialists to establish closed supply chains. BASF’s strategy to spin off its coatings unit into a joint venture with Carlyle, valued at EUR 7.7 billion (USD 9.02 billion), is expected to redirect funds toward adhesion promoters that overlap with adhesive applications. Meanwhile, H.B. Fuller is diversifying its portfolio through acquisitions, including Medifill/GEM and ND Industries in 2024, securing positions in the medical-device and thread-locker segments, which adhere to automotive quality standards.

Opportunities exist in the development of smart and debondable joints. Parker Hannifin’s CoolTherm TC-850, launched in May 2025, offers room-temperature curing, eliminating oven bottlenecks and providing 2 W/mK thermal conductivity for battery pack cooling. University-industry collaborations are exploring sensor-embedded epoxies with fiber-optic strain measurement capabilities; however, cost premiums of 40-60% limit their application to premium battery electric vehicles (BEVs). Patent filings, such as US 20250206940, which details one-component epoxies with -40°C impact tolerance, indicate that original equipment manufacturers (OEMs) are bypassing tier-one suppliers to develop proprietary bonding solutions.

Europe Automotive Adhesives And Sealants Industry Leaders

3M

Henkel AG & Co. KGaA

Sika AG

Dow

Arkema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Sika acquired Turkey-based Akkim for CHF 220 million (USD 278.57 million), adding production facilities in Turkey and Romania. This acquisition strengthens Sika's position in the European automotive adhesives and sealants market, particularly in Eastern Europe.

- January 2026: Henkel AG & Co. KGaA finalized the acquisition of ATP Adhesive Systems, adding EUR 270 million (USD 316.34 million) in annual sales. This acquisition strengthens Henkel's reactive hot-melt capabilities, particularly for battery modules, aligning with the growing demand for automotive adhesives and sealants in Europe.

Europe Automotive Adhesives And Sealants Market Report Scope

Automotive adhesives and sealants are chemical compounds used in vehicle manufacturing, assembly, and repair to bond components and seal gaps against environmental factors. These materials provide a lightweight alternative to mechanical fasteners, supporting structural integrity, aesthetics, and fuel efficiency.

The Europe automotive adhesives and sealants market is segmented by resin, technology, and geography. By resin, the market is segmented into acrylic, cyanoacrylate, epoxy, polyurethane, silicone, VAE/EVA, and other resins. By technology, the market is segmented into hot-melt, reactive, sealants, solvent-borne, UV-cured adhesives, and water-borne. The report also covers the market size and forecasts for automotive adhesives and sealants in 6 countries across the region. The market sizes and forecasts are provided in terms of value (USD).

By Resin

| Acrylic |

| Cyanoacrylate |

| Epoxy |

| Polyurethane |

| Silicone |

| VAE/EVA |

| Other Resins |

By Technology

| Hot-Melt |

| Reactive |

| Sealants |

| Solvent-borne |

| UV-Cured Adhesives |

| Water-borne |

By Geography

| France |

| Germany |

| Italy |

| Russia |

| Spain |

| United Kingdom |

| Rest of Europe |

| By Resin | Acrylic |

| Cyanoacrylate | |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| VAE/EVA | |

| Other Resins | |

| By Technology | Hot-Melt |

| Reactive | |

| Sealants | |

| Solvent-borne | |

| UV-Cured Adhesives | |

| Water-borne | |

| By Geography | France |

| Germany | |

| Italy | |

| Russia | |

| Spain | |

| United Kingdom | |

| Rest of Europe |

Market Definition

- End-user Industry - In the automotive industry, both the OEM and after market adhesive and sealants applications are considered under the scope.

- Product - All adhesive and sealant products used in automotive industry are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, UV Cured Adhesives, and Sealants technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms