Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.55 Billion |

| Market Size (2026) | USD 1.64 Billion |

| Market Size (2031) | USD 2.21 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Epoxy Adhesive Market Analysis by Mordor Intelligence

The Europe epoxy adhesives market size is projected to be USD 1.55 billion in 2025, USD 1.64 billion in 2026, and reach USD 2.21 billion by 2031, growing at a CAGR of 6.12% from 2026 to 2031. Consistent vehicle electrification, Green-Deal renovation mandates, and technology shifts toward low-VOC chemistries are widening the application envelope and lifting the average price-per-kilogram of high-performance grades. The surge in electric vehicle battery assembly favors thermally conductive epoxies that combine mechanical strength with heat-dissipation capacity. Regional suppliers are also accelerating water-borne launches as end-users tighten sustainability scorecards and prepare for tougher REACH authorizations. Germany’s dual role as Europe’s largest adhesive manufacturing base and fastest-expanding demand center reinforces its bellwether status for the Europe epoxy adhesives market.

Key Report Takeaways

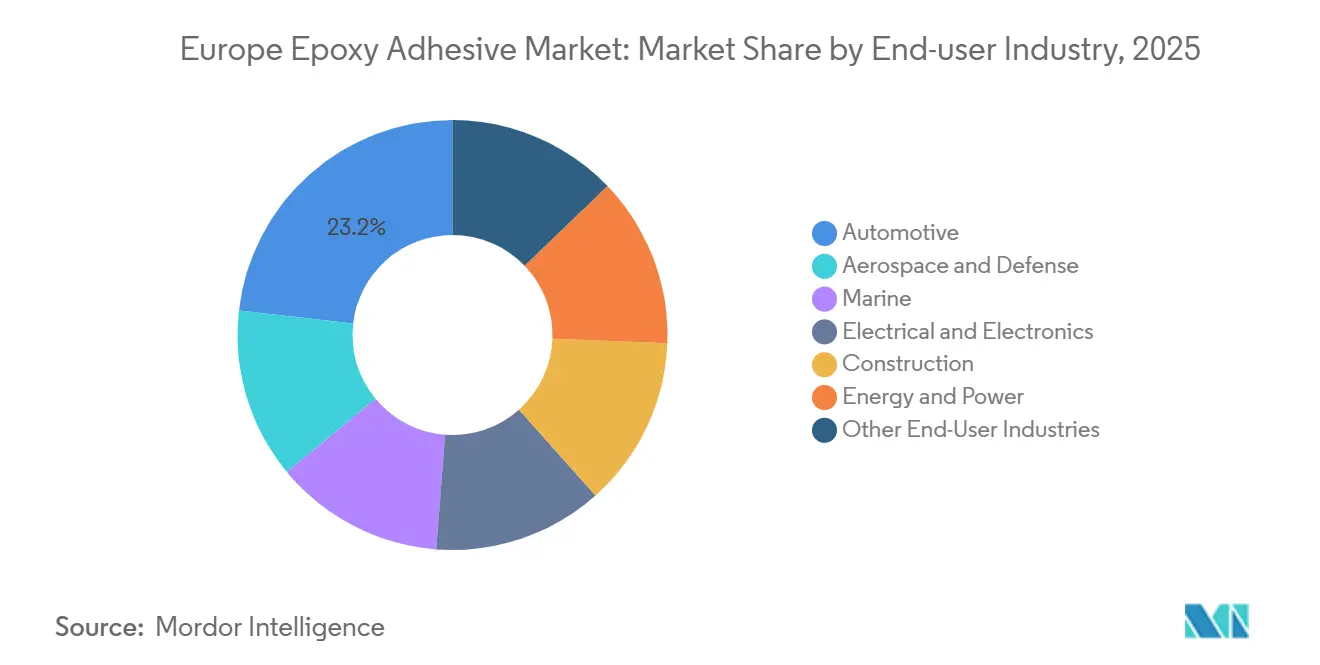

- By end-user industry, automotive applications held 23.18% of the Europe epoxy adhesives market share in 2025, while electrical and electronics is forecast to expand at a 6.58% CAGR during the forecast period (2026-2031).

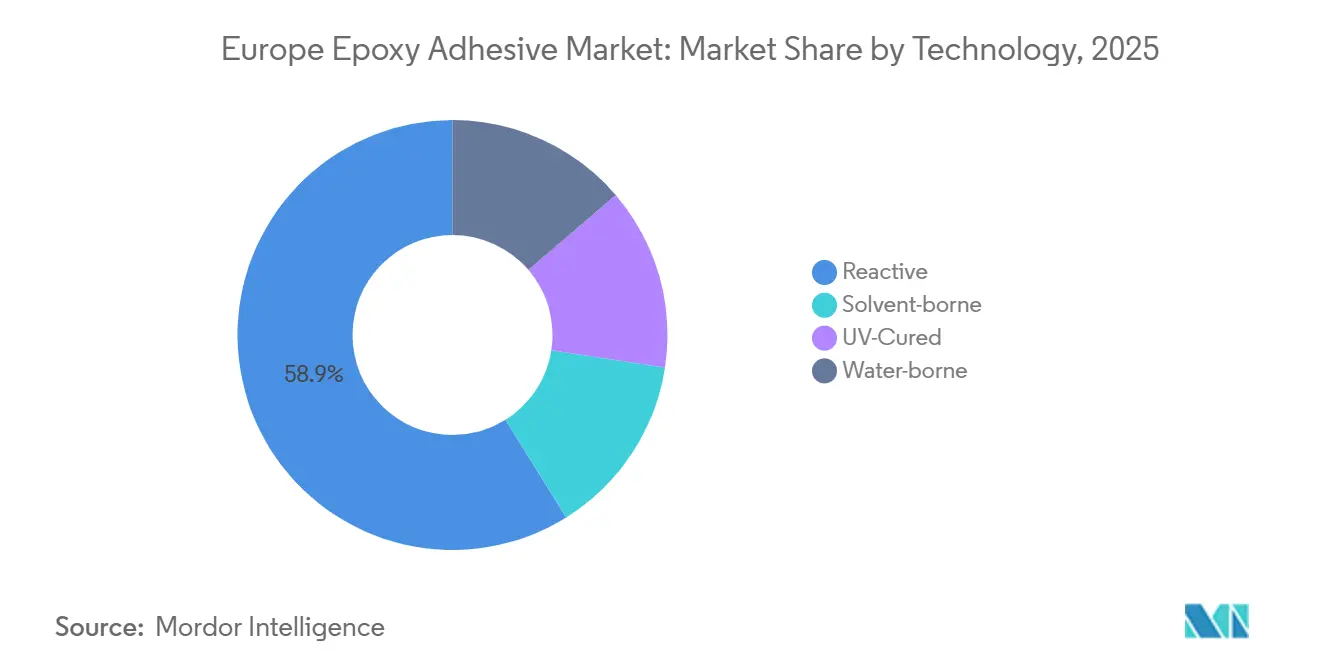

- By technology, reactive systems accounted for 58.87% share of the Europe epoxy adhesives market size in 2025, whereas water-borne systems are projected to post a 6.47% CAGR during 2026-2031.

- By country, Germany commanded 23.12% share of the Europe epoxy adhesives market in 2025 and is anticipated to rise at a 6.35% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Epoxy Adhesive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electric Vehicle and Lightweight-Vehicle Structural Bonding Boom | + 1.8% | Germany, France, UK, Nordic countries | Medium term (2-4 years) |

| Construction Renovation Surge (EU Green Deal) | + 1.5% | Germany, France, Italy, Spain, Nordic countries | Long term (≥ 4 years) |

| VOC/REACH-Driven Shift to High-Performance Systems | + 1.2% | Global (EU-wide enforcement) | Short term (≤ 2 years) |

| Offshore Wind Blade Upsizing | + 0.9% | Germany, UK, Nordic countries, Spain | Long term (≥ 4 years) |

| Robotic Dispensing Adoption in Assembly Lines | + 0.7% | Germany, France, Italy, UK | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electric Vehicle and Lightweight-Vehicle Structural Bonding Boom

In battery housings, crash structures, and mixed-material body components, epoxy adhesives are increasingly supplanting traditional methods like welds, rivets, and mechanical fasteners. Modified with ceramic fillers, thermally conductive epoxies achieve a thermal conductivity of ≥2 W/m·K and lap-shear strengths of up to 30 MPa. This capability facilitates module-to-cooling-plate interfaces that effectively manage heat and endure crash loads. The diversity in cell formats, such as cylindrical, pouch, and blade, drives a distinct demand for epoxies, pressure-sensitive tapes, and gap-fillers. This collective demand is expanding the footprint of the European structural adhesives market in vehicle platforms. As lightweighting trends push OEMs towards aluminum and fiber-reinforced polymer parts, the need arises for chemically compatible adhesives. These adhesives must withstand thermal cycling from −40 °C to 80 °C without delaminating. Supplier portfolios, including SikaForce and WEVO-CHEMIE, now highlight silicone grades with initial adhesion exceeding 2 MPa and thermal conductivities approaching 1.5 W/m·K, specifically for EV modules[1]WEVO-CHEMIE, “High-Thermal-Conductivity Silicone Adhesives for EV Batteries,” wevo-chemie.com. Furthermore, pilot lines that incorporate robotic metering and in-line infrared curing are not only reducing takt times but also enhancing adoption rates in German and French gigafactories. Given these trends, the European epoxy adhesives market for battery applications is poised for double-digit volume growth from 2026 to 2028.

VOC/REACH-Driven Shift to High-Performance Systems

In April 2025, the European Commission proposed capping authorizations at 10 years and implementing an "essential use" filter, tightening the compliance window for legacy solvent-borne systems. BASF-Sika's Baxxodur EC 151an, an amine-based epoxy hardener, boasts 90% lower VOC emissions compared to traditional amine systems and reduces cure time by two-thirds, showcasing how regulation drives innovation. As OEMs chase ISO 14001 certifications, water-borne and UV-cured chemistries are winning more designs in appliances, engineered wood, and electronics. Henkel's acquisition of ATP Adhesive Systems, with a portfolio over 90% water-based, strategically boosts Henkel's foothold in Europe's epoxy adhesives market, targeting the automotive, electronics, and construction sectors. This regulatory trend suggests a sustained CAGR premium for sustainable grades throughout the forecast period.

Offshore Wind Blade Upsizing

As rotor diameters exceed 220 m, they exert heightened peel and shear stresses on spar-cap and shell bonds. Researchers at the University of Oulu have developed bio-based epoxies from forest residue, boasting tensile strengths up to 76% greater than their fossil-based polyester counterparts. These innovations not only enhance strength but also facilitate chemical recycling, addressing challenges related to the end-of-life of blades. The IMPACT project at DTU Wind has introduced advanced fatigue prediction models[2]DTU Wind, “IMPACT Project Final Report 2025,” dtu.dk . These models enable tighter adhesive design parameters, translating to significant operational cost savings. Manufacturers in Germany and the UK are experimenting with two-component toughened epoxies. These epoxies, with critical strain-energy release rates of ≥30 kJ/m², aim to curb crack propagation over a projected 30-year service life. Such advancements are driving a surge in demand within the European epoxy adhesives market, especially as offshore wind capacities expand to align with the Fit-for-55 targets.

Robotic Dispensing Adoption in Assembly Lines

Automated bead applications enhance throughput and ensure consistent quality, particularly in gluing EV battery cells and potting electronics. Sika's "Curing-by-Design" technology, which allows for an adjustable pot life followed by a rapid snap cure, has achieved a remarkable 40% reduction in cycle times on pilot battery lines. A 2026 study on radical-induced cationic frontal polymerization demonstrated that epoxy joints could be fully cured in just 10 seconds at 80 °C. This aligns adhesive chemistry with the demands of high-speed robotics. Henkel's AI-powered digital twin technology predicts thermal runaway scenarios and enables the selection of the best gap-filler viscosity and bead shape. This reduces scrap rates and warranty claims. The resilience of automation drives specification adherence and ensures consistent demand for epoxy adhesives in automotive and appliance manufacturing across Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BPA and Epichlorohydrin Feedstock Price Volatility | -0.8% | Global (EU production hubs: Germany, Netherlands) | Short term (≤ 2 years) |

| Toxicological/Regulatory Re-classification of BPA | -0.5% | Global (EU-wide enforcement, spillover to UK) | Medium term (2-4 years) |

| Rise of Bio-based and Hybrid Alternatives | -0.4% | Germany, France, Nordic countries, Rest of Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

BPA and Epichlorohydrin Feedstock Price Volatility

In 2025, European epoxy resin prices fell by 12% due to market oversupply, leading to tighter margins and heightened procurement uncertainties. Westlake shut down its Pernis facility, which produced epoxy resins, BPA, and epichlorohydrin, in June 2025. This was soon followed by Ineos's announcement in October 2025 to close its Rheinberg units for epichlorohydrin and chlorine. Meanwhile, India's imposition of anti-dumping duties shifted Asian epoxy flows towards Europe, exacerbating price fluctuations. To navigate this volatility, adhesive formulators are turning to multi-vendor contracts and are even delving into bio-based feedstocks. Despite these measures, the unpredictability of near-term costs continues to impact working-capital decisions in the European epoxy adhesives market.

Toxicological/Regulatory Re-classification of BPA

Concerns over endocrine disruption could lead to potential restrictions on BPA, unless essential-use exemptions apply. The REACH revision hastens substitution timelines, echoing the phase-downs of formaldehyde in wood bonding. While hybrid epoxidized plant-oil systems achieve lap-shear strengths exceeding 20 MPa, challenges like feedstock variability and moisture sensitivity hinder scaling. Consequently, adhesive suppliers allocate up to 5% of their R&D budgets for reformulation and collaborate with sector associations to obtain transitional derogations. Without these adaptations, they risk losing ground in the European epoxy adhesives market by the late 2020s.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Automotive Dominance and Electronics Upswing

In 2025, the automotive sector accounted for 23.18% of Europe's epoxy adhesives market, highlighting a consistent preference for epoxies in enhancing body stiffness and crash absorption. As the industry electrifies, there's a growing demand for thermally conductive gap-fillers, flame-retardant potting resins, and debond-on-demand solutions, all pivotal for battery recycling. With lap-shear strength requirements set between 15-23 MPa and service temperatures reaching up to 80 °C, the average value per vehicle sees a boost, allowing the European epoxy adhesives market to maintain its premium pricing. The electronics sector is on a 6.58% CAGR trajectory, driven by 5G rollouts and the miniaturization of power modules. These advancements necessitate adhesives boasting thermal conductivity of ≥3 W/m·K and high elongation to counter thermal mismatches. In Germany and Poland, assembly lines for Mini-LEDs are now opting for low-viscosity silicone gels that cure at room temperature, a move that slashes energy consumption. A diverse demand spanning consumer devices, industrial automation, and photovoltaic inverters ensures steady volume growth, even amidst potential softening in consumer electronics cycles.

Construction, ranking third in volume, is buoyed by EU renovation subsidies. These subsidies promote the use of low-VOC, high-grab polyurethanes, especially for bonding façades and insulation panels. The marine, aerospace, and renewable-energy sectors each have their unique demands. For instance, they seek niche high-performance grades, such as moisture-tolerant methacrylate adhesives for composite hulls and flame-retardant epoxies. The latter must adhere to FAR 25.853 standards concerning fire, smoke, and toxicity in aircraft interiors. Energy applications, particularly in offshore wind, prioritize crack-resistant epoxies, ensuring they maintain a fracture toughness of ≥25 kJ/m² over a 30-year lifecycle. Together, these diverse segments bolster end-market resilience, shielding the European epoxy adhesives market from the cyclical fluctuations of any single sector.

By Technology: Reactive Systems Lead, Water-Borne Gains Momentum

In 2025, reactive systems accounted for 58.87% of the European epoxy adhesives market. This segment delivers moduli exceeding 2,000 MPa and elongations ranging from 2% to 300% for various joints. Within this segment, two-component epoxies dominate automotive structural bonding. Water-borne systems represent the fastest-growing segment, with a robust 6.47% CAGR projected through 2031. Their zero-solvent carrier and seamless processability make them highly suitable for hygiene-sensitive applications such as medical tapes and flexible electronics. For instance, ATP’s water-based acrylics have already surpassed a 1.5 MPa peel strength on low-surface-energy substrates. Solvent-borne adhesives, while facing challenges from VOC regulations, continue to hold niche applications that require quick evaporation and deep substrate wetting. However, they are gradually losing market share to water-borne and reactive alternatives. UV-cured adhesives form another segment offering rapid processing and energy efficiency. Despite these advantages, adoption is limited by substrate opacity, shadow-cure issues, and the high capital investment required for UV equipment. A 2021 study on radical-induced cationic frontal polymerization demonstrated that epoxy adhesives, when UV-activated and used with substrates heated to 80°C, can achieve full cure in under 10 seconds for aluminum joints. These adhesives deliver lap-shear strengths of up to 20 MPa, comparable to traditional thermal cures that require minutes to hours.

Geography Analysis

In 2025, Germany commanded a 23.12% share of Europe's epoxy adhesives market. By 2031, this share is projected to grow at a 6.35% CAGR, driven by electric vehicle (EV) assembly activities in Bavaria and Baden-Württemberg, alongside substantial renovation budgets allocated for public buildings. Despite a 2.8% dip in domestic sales volume, German adhesive manufacturers, as reported by Industrieverband Klebstoffe, achieved sales of EUR 13.6 billion in 2024. This figure highlights the industry's heavy reliance on exports and its production efficiency. Federal incentives for battery gigafactories in Brandenburg and Lower Saxony bolster domestic demand, particularly for thermally conductive and flame-retardant epoxy gap-fillers. Additionally, BASF's expansion of dispersion capacities in Ludwigshafen solidifies Germany's position as a primary supply hub for low-VOC grades, which are in high demand across Europe.

In France, Airbus facilities in Toulouse and Nantes emphasize the importance of epoxy adhesives in aerospace composite bonding. These epoxies must meet rigorous standards, including flame-smoke-toxicity and lightning-strike resistance. The UK, a frontrunner in offshore wind energy, requires crack-resistant epoxies for blades exceeding 100 meters, produced near the Humber estuary. Concurrently, London's push for retrofitting buildings amplifies the demand for low-emission construction adhesives. In Italy, the furniture and appliance sectors in Lombardy lean towards moisture-curing polyurethanes for wood paneling. Meanwhile, Spain's revitalized residential market boosts the demand for polyurethanes, especially for bonding insulation panels.

The Nordic countries are witnessing growth above the European average, largely due to strict environmental regulations that favor bio-based chemical solutions. Both Denmark and Sweden are expanding their offshore wind capabilities, sourcing high-toughness epoxies predominantly from suppliers in Germany and Switzerland. Eastern Europe, spearheaded by nations like Poland, Czechia, and Romania, is seeing significant investments in automotive parts and electronics assembly. This surge is further bolstered by Sika's acquisition of Akkim, which is set to enhance production capabilities with new assets in Turkey and Romania. However, Russia's market is hampered by international sanctions and disruptions in the supply chain, curtailing its impact on the overall trajectory of Europe's epoxy adhesives market.

Competitive Landscape

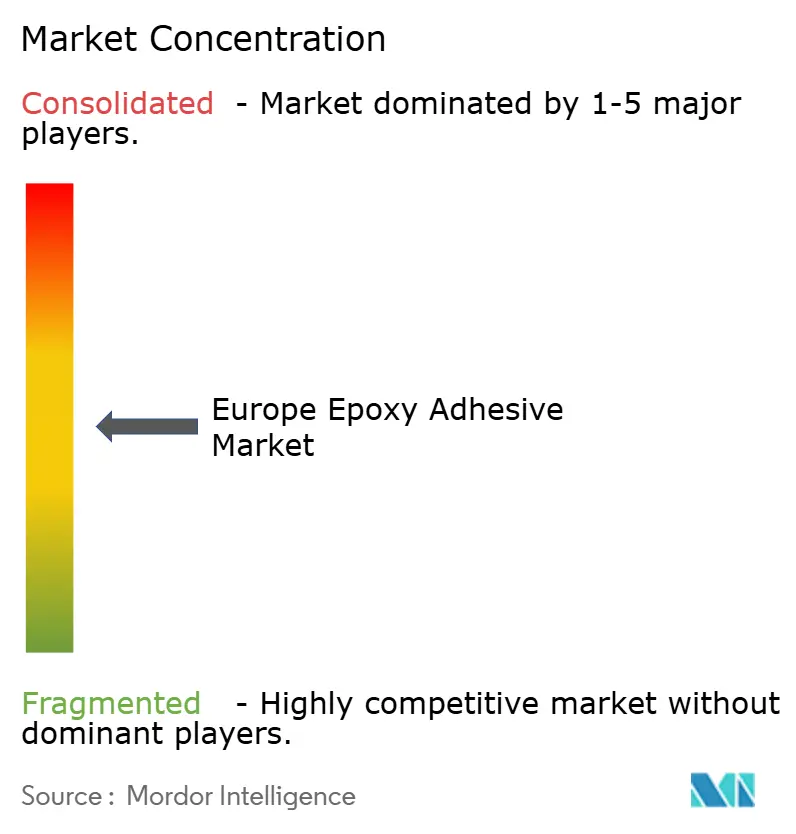

Major players like Henkel, Sika, BASF, 3M, Dow, and H.B. Fuller dominate the European epoxy adhesives market, which exhibits moderate fragmentation. Portfolio decarbonization is crucial; for instance, BASF and Sika's co-development of Baxxodur EC 151 reduces VOC content by 90% and cuts cure time in half, meeting REACH and Green Deal standards. Suppliers are leveraging AI and digital twins in formulation labs, shortening product-development cycles by as much as 30%. Meanwhile, Henkel's investments are enabling battery gap-filler prototyping in just 48 hours, thanks to machine-learning predictive tools.

Emerging opportunities lie in debond-on-demand adhesives, which aid in EV battery recycling and ensure DIN/TS 54405-compliant separability in appliances. Patent filings from 2025 to 2026 highlight a focus on thermally conductive silicone hybrids exceeding 2 W/m·K and bio-based polyurethane dispersions, underscoring a robust R&D push. Niche players like WEVO-CHEMIE are establishing a foothold with ultra-high-thermal-conductivity grades, while regional specialists leverage their closeness to clients for customized formulations in engineered wood and marine composites. While price competition is subdued in premium segments, fluctuations in raw material prices and energy costs necessitate vigilant margin management across the value chain, influencing strategic choices in the European epoxy adhesives landscape.

Europe Epoxy Adhesive Industry Leaders

Arkema Group

H.B. Fuller Company

Henkel AG & Co. KGaA

Sika AG

Dow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Sika agreed to acquire Turkish adhesive producer Akkim, adding CHF 220 million in 2025 sales and two manufacturing hubs in Turkey and Romania to boost Eastern-European distribution.

- January 2026: Henkel signed a deal to acquire Switzerland-based ATP Adhesive Systems, a specialist in water-based high-performance tapes with EUR 270 million 2025 sales and 700 employees.

Europe Epoxy Adhesive Market Report Scope

Epoxy glue is a high-strength, two-part adhesive consisting of a resin and a hardener that, when mixed, cures into a rigid, durable, and waterproof polymer. It excels at bonding, sealing, and filling gaps between diverse materials like metal, wood, and glass. Epoxy is renowned for its superior resistance to chemicals, moisture, and extreme temperatures.

The Europe Epoxy Adhesives market report is segmented by technology, end-user industry, and geography. By end-user industry, the market is segmented into aerospace and defense, automotive, marine, electrical and electronics, construction, energy and power, and other end-user industries. By technology, the market is segmented into reactive, solvent-borne, uv-cured, and water-borne. The report also covers the market size and forecasts for epoxy adhesives in 7 countries across the Europe region. For each segemnt market sizing and forecasts are provided in terms of value (USD).

By End-User Industry

| Aerospace and Defense |

| Automotive |

| Marine |

| Electrical and Electronics |

| Construction |

| Energy and Power |

| Other End-User Industries |

By Technology

| Reactive |

| Solvent-borne |

| UV-Cured |

| Water-borne |

By Country

| France |

| Germany |

| Italy |

| Russia |

| Spain |

| United Kingdom |

| NORDIC Countries |

| Rest of Europe |

| By End-User Industry | Aerospace and Defense |

| Automotive | |

| Marine | |

| Electrical and Electronics | |

| Construction | |

| Energy and Power | |

| Other End-User Industries | |

| By Technology | Reactive |

| Solvent-borne | |

| UV-Cured | |

| Water-borne | |

| By Country | France |

| Germany | |

| Italy | |

| Russia | |

| Spain | |

| United Kingdom | |

| NORDIC Countries | |

| Rest of Europe |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the epoxy adhesives market.

- Product - All epoxy adhesive products are considered in the market studied

- Resin - Under the scope of the study, one component and two component based epoxies are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms