Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

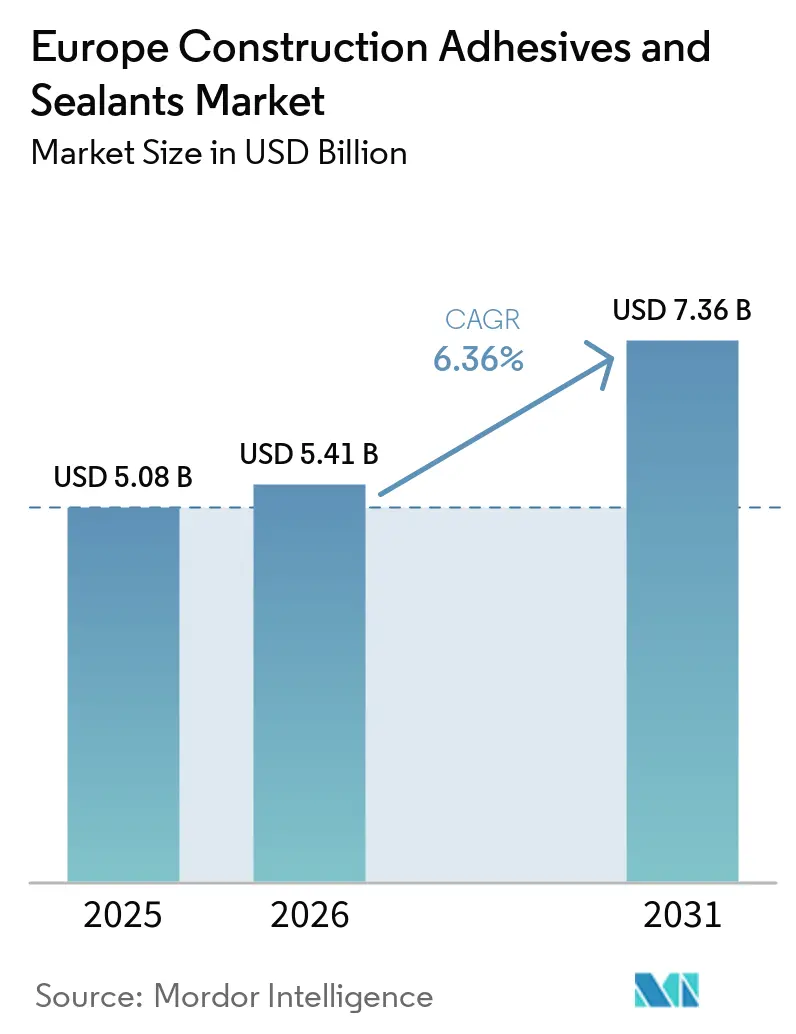

| Base Year Market Size (2025) | USD 5.08 Billion |

| Market Size (2026) | USD 5.41 Billion |

| Market Size (2031) | USD 7.36 Billion |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Construction Adhesives And Sealants Market Analysis by Mordor Intelligence

The Europe Construction Adhesives And Sealants Market size was valued at USD 5.08 billion in 2025 and is estimated to grow from USD 5.41 billion in 2026 to reach USD 7.36 billion by 2031, at a CAGR of 6.36% during the forecast period (2026-2031). The escalation reflects synchronized public-sector funding, faster retrofits, and accelerated adoption of low-VOC chemistries. Germany anchors regional demand with the EUR 500 billion infrastructure program, while Italy and Austria supply a growing pipeline of bridge and tunnel refurbishments. Revised EU regulations, Construction Products Regulation (CPR), Classification-Labeling-Packaging (CLP), and new VOC limits, push converters toward water-borne platforms verified to EMICODE EC1 Plus. Concurrently, platinum-linked silicone costs and isocyanate volatility narrow margins for solvent-borne and reactive systems, increasing the strategic importance of backward integration and long-term feedstock contracts. Competitive activity centers on Digital Product Passports (DPP), Environmental Product Declarations (EPD), and the acquisition of regional specialists with strong installer networks.

Key Report Takeaways

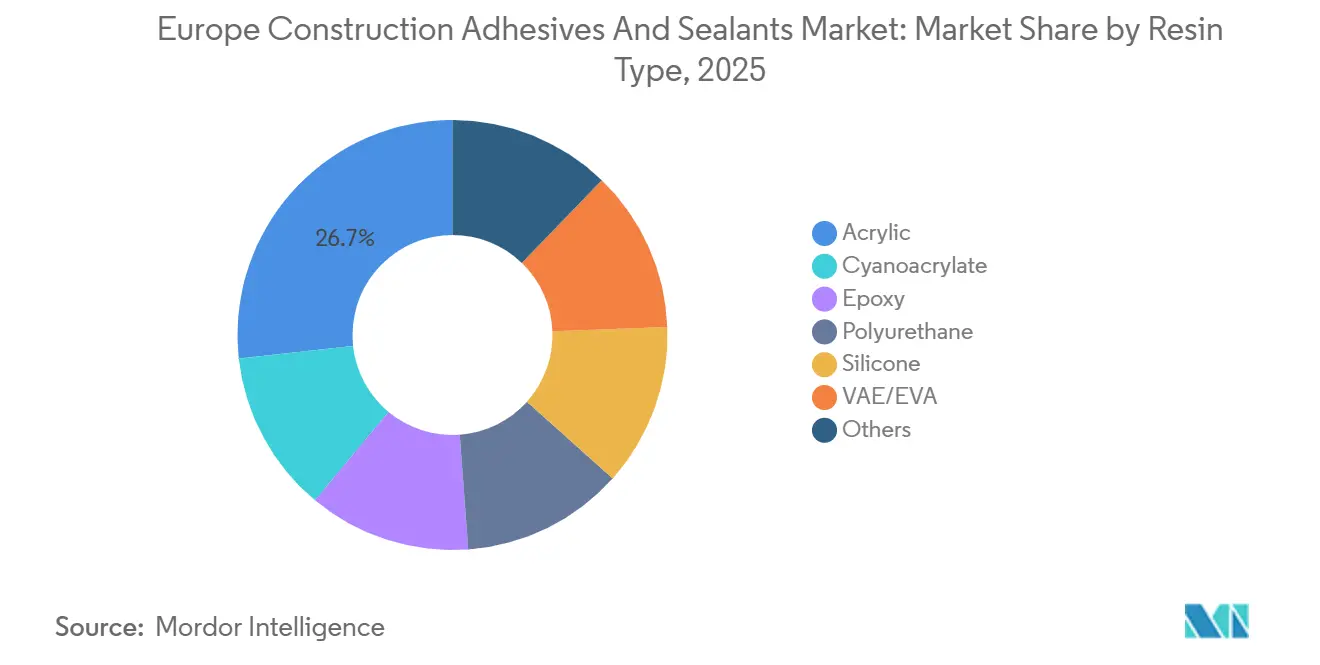

- By resin type, acrylic held the largest share of 26.75% in 2025, and silicone's market share is expected to grow with a CAGR of 6.28% during the forecast period (2026-2031).

- By technology, sealants had a share of 42.37% in 2025, and the share of water-borne products is expected to grow with a CAGR of 6.57% during the forecast period (2026-2031).

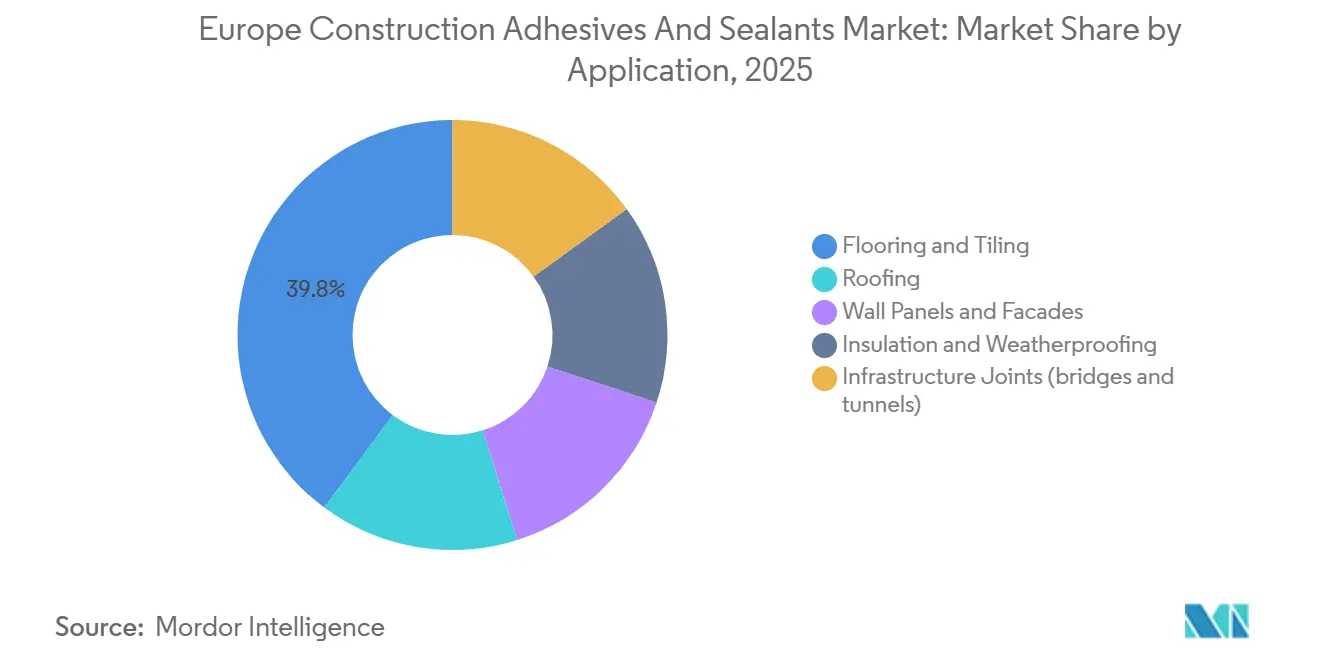

- By application, the market share of flooring and tiling was 39.83% in 2025, and the share of infrastructure joints (bridges and tunnels) is expected to grow with a CAGR of 6.54% during the forecast period (2026-2031).

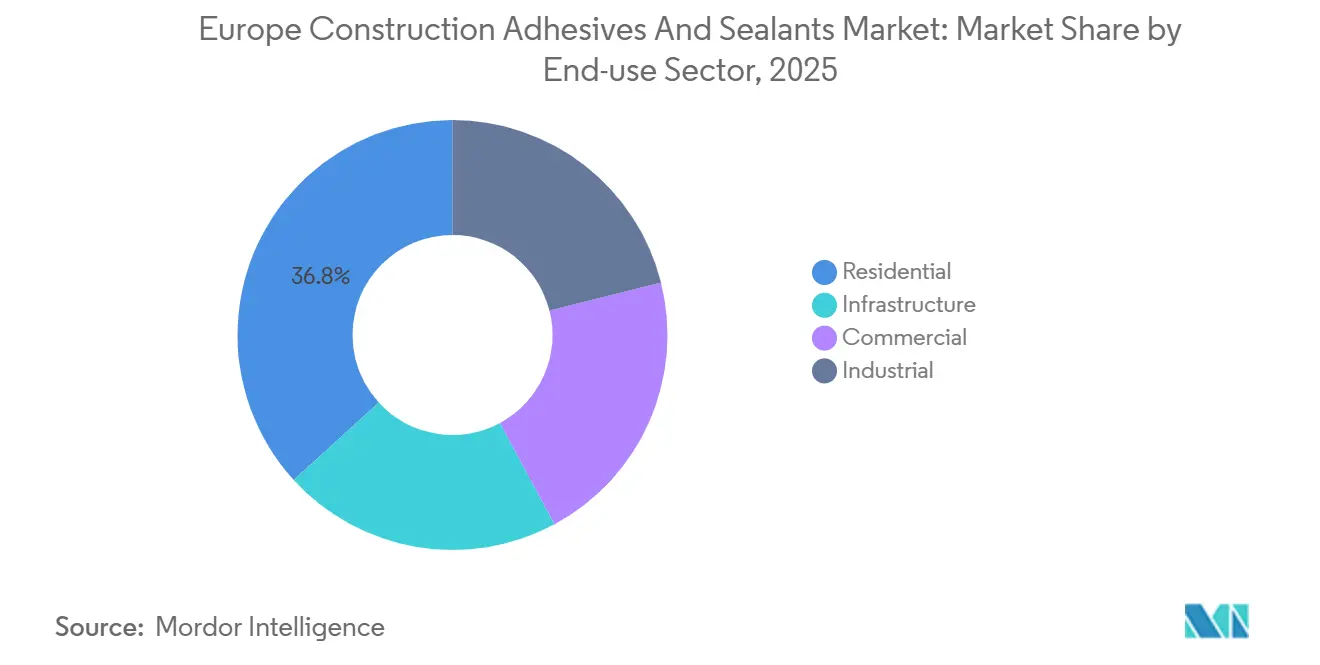

- By end-use sector, the residential sector had a market share of 36.78% in 2025, and the infrastructure sector's market share is poised to grow with a CAGR of 6.23% during the forecast period (2026-2031).

- By geography, Germany held a market share of 24.48% in 2025, and Italy's share is expected to grow with a 5.46% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Construction Adhesives And Sealants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift to low-VOC, REACH-compliant formulations | +1.2% | EU-wide, with early adoption in Germany, Netherlands, Nordics | Medium term (2-4 years) |

| Post-pandemic EU renovation wave (Renovation Wave Initiative) | +1.5% | EU-wide, concentrated in France, Germany, Italy, Spain | Long term (≥ 4 years) |

| Growth of off-site and modular construction | +0.9% | Sweden, Germany, Ireland, UK; spillover to Central Europe | Medium term (2-4 years) |

| Rising demand for high-performance façade systems | +0.8% | Germany, France, UK, Benelux; commercial and infrastructure sectors | Medium term (2-4 years) |

| Carbon-reduction mandates accelerating structural glazing | +0.7% | Denmark, Germany, Netherlands; public buildings and ZEB projects | Long term (≥ 4 years) |

| 3D-printed concrete's adhesive and sealant demand | +0.4% | Germany, Netherlands, Belgium; pilot projects and research consortia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to Low-VOC, REACH-Compliant Formulations

The revised CLP entered force on 10 December 2024 and applies from 1 July 2026, adding new hazard classes and digital label rules that compress reformulation windows for D4, D5, and D6 siloxanes. MAPEI’s solvent-free silylated polymer, ULTRABOND ECO S955 1K, already meets EMICODE EC1 Plus with TVOC below 60 µg/m³ after 28 days, demonstrating market readiness for low-VOC flooring jobs. The Construction Products Regulation (CPR) revision, effective 8 January 2026, embeds the Digital Product Passport (DPP) and whole-life carbon accounting into CE marking, rewarding early movers who complete third-party verification ahead of public-tender deadlines. National embodied-carbon caps, such as Denmark’s 7.1 kg CO₂e/m²/year in 2025, tightening to 5.8 kg in 2029, are spreading to Germany and the Netherlands, accelerating the displacement of solvent-borne sealants[1]“Guidance on CLP hazard classes,” European Chemicals Agency, echa.europa.eu.

Post-Pandemic EU Renovation Wave (Renovation Wave Initiative)

The European Union (EU) targets energy upgrades for 35 million buildings by 2030, channeling EUR 66 billion in public funding through 2029. The Energy Performance of Buildings Directive (EPBD) recast requires whole-life carbon assessments for new buildings above 1,000 m² from 2028 and for all new construction from 2030. Germany’s Climate & Transformation Fund allocates EUR 12.5 billion (USD 14.59 billion) to rail infrastructure and prioritizes residential retrofits, pushing construction output from a 4.9% contraction in 2024 to 2.5% growth in 2026, the region’s fastest rebound. Uptake in France and Spain trails due to fragmented contractor networks, yet improved financing tools are lifting quarter-on-quarter retrofit volumes. Labor remains the choke point because only 25% of construction workers hold at least one green skill, prompting formulators to emphasize error-tolerant, primer-less products that reduce installer training time[2]“Renovation Wave Initiative,” European Commission, ec.europa.eu.

Growth of Off-Site and Modular Construction

An Ecorys study measured 20-60% schedule savings, 20% cost reduction, and up to 90% on-site waste reduction for volumetric systems. Sweden already prefabricates 90% of single-family homes, while Germany directs EUR 2 billion (USD 2.26 billion) to climate-neutral social housing that mandates modern methods of construction. Ireland’s Housing for All plan backs modular builds with a EUR 100 million (USD 113.08 billion) fund, stimulating demand for fast-curing polyurethane and hot-melt adhesives robust enough to withstand transport vibration and temperature swings. Sika’s Purform primer-less polyurethane cuts surface-prep steps, and Sikafloor-3000 Snapbooster reduces cure time from 24-48 hours to six, directly addressing labor shortages projected to reach a four-million-person gap by 2035.

Rising Demand for High-Performance Façade Systems

Dow introduced PAS 2060-certified carbon-neutral silicones that enable structural glazing with 15% less aluminum framing and 10-25% better thermal performance, trimming façade embodied carbon by up to 40%. Sika’s high-strength adhesives permit 55% SG and 25% IG joint reduction, saving more than 100 tons of CO₂-equivalent per large commercial façade. Timber–aluminium hybrids, such as Staticus Hybrid Unitized Façade and Hydro’s CIRCAL recycled profiles, further lower embodied carbon, meeting Denmark’s 5.8 kg CO₂e/m²/year trajectory by 2029. Developers in Germany, France, and the UK adopt life-cycle rather than upfront cost metrics, pushing suppliers to document EPDs and DPPs earlier in design phases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in isocyanate and silicone feedstock prices | -0.9% | EU-wide, acute in Germany, Italy, Spain due to energy-intensive production | Short term (≤ 2 years) |

| Russia-Ukraine war driven logistics disruptions | -0.6% | Central and Eastern Europe, Balkans; spillover to Western EU via freight costs | Short term (≤ 2 years) |

| Skill shortages in advanced application techniques | -0.5% | EU-wide, concentrated in Germany, France, UK, Netherlands | Medium term (2-4 years) |

| Lengthy EU chemical approval timelines (CLP/GHS) | -0.3% | EU-wide, affecting all formulators introducing new chemistries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Isocyanate and Silicone Feedstock Prices

Wacker Chemie flagged an additional 25% price rise effective 1 February 2026, while silicone DMC (Dimethyl Carbonate) and EVA (Ethylene-Vinyl Acetate) indices rose 28% and 22%, respectively. Converters scramble for eight-to-twelve-week delivery slots versus four-to-six in 2024, carrying extra inventory that absorbs working capital. Isocyanate plants averaged 75-80% utilization through 2025 on weak demand and high energy costs, leaving 2026 stabilization dependent on curtailing Chinese exports. Persistently higher European electricity prices, two to three times U.S. Gulf Coast benchmarks, erode competitiveness and push formulators toward long-term supply contracts.

Russia-Ukraine War Driven Logistics Disruptions

EU sanctions blocked epoxy and polyurethane exports to Russia, yet trade trackers uncovered circumvention via Polish and Italian intermediaries, muddying chain-of-custody transparency and inflating compliance costs. Freight detours add five to ten days on Black Sea routes and raise landed costs by an average 4%. A durable cease-fire would normalize freight rates and lower propylene and acrylic acid raw-material inputs, but persistent hostilities keep a 3-5% risk premium baked into Central and Eastern European costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Dominance Meets Silicone’s Compliance Edge

Acrylic resins maintained 26.75% Europe Construction Adhesives and Sealants market share in 2025, led by flooring and tiling, where open time and water cleanup offset lower bond strength. Silicone’s 6.28% CAGR through 2031 stems from mandatory structural glazing in embodied-carbon-capped projects and the phase-out of D4-D6 siloxanes from mid-2026. Polyurethanes remain indispensable for bridge-joint movement capability above ±25% and UV-exposed roofing membranes. Epoxies govern industrial flooring but lose momentum because of long cure cycles and VOC (Volatile Organic Compound) levels incompatible with EMICODE EC1 Plus. Niche streams such as bio-based polyurethanes, backed by BASF’s SUSBOARD, and alkali-activated blends trialed in 3D-printed concrete, remain under a very low share of Europe Construction Adhesives and Sealants market size through 2031. Early silicon reformulators gain specification lock-in with façade engineers seeking carbon-neutral EPDs.

Acrylic’s installed volume base ensures slow erosion even as water-borne modifiers prune VOC content. Silicone suppliers hedge platinum exposure through recycling catalysts and long-term supply deals. Polyurethane innovators exploit primer-less tech to cut installer hours in labor-scarce regions, boosting uptake in modular factories. Epoxy vendors re-position high-solids, fast-cure grades for extreme-wear logistics floors, while cyanoacrylates persevere in repair kits.

By Technology: Sealants Lead, Water-Borne Gains Regulatory Tailwind

Sealants covered 42.37% of 2025 revenue, ranging from 1K hybrids for façade mullions to 2K polysulfides for runway joints. Water-borne adhesives are expected to expand at a 6.57% CAGR during the forecast period (2026-2031), propelled by Q4 2025 EU VOC ceilings and EMICODE EC1 Plus labeling that caps TVOC at 60 µg/m³ after 28 days. Solvent-borne grades stay relevant in cold-weather jobs where rapid set outweighs emissions penalties, though margins narrow on costlier acetates and glycols. Reactive 2K systems address structural floors and bridges requiring greater than 2 MPa adhesion and 25-year durability, but feedstock turbulence adds price volatility.

Hot-melts thrive in prefab lines, delivering 60-second set times that mirror assembly-line takt yet struggle above 80°C façade service. CPR’s 2026 DPP trigger rewards water-borne products with lower embodied carbon, lifting their Europe Construction Adhesives and Sealants market size share by 2031. Formulators cross-license humectants and freeze-thaw stabilizers to ensure pan-European shelf life.

By Application: Infrastructure Joints Outpace Flooring’s Volume Base

Flooring and tiling retained 39.83% demand in 2025 under the Renovation Wave. Nevertheless, infrastructure joints forecast a 6.54% CAGR during the forecast period (2026-2031) as Austria’s Semmering Tunnel Chain, the Brenner Base Tunnel, and Italy’s ASPI upgrades require long-life sealants designed for 100-year bridges. Roofing applications add steady demand from Germany’s Deutsche Bahn station modernization, where single-ply membranes rely on UV-resistant polyurethanes. Façade and wall panels move toward structural glazing that cuts aluminium 15% and improves U-values, satisfying whole-life carbon assessment criteria.

Insulation adhesives align with Minimum Energy Performance Standards rolling out from 2030, leading to a higher Europe Construction Adhesives and Sealants market size for water-borne grades. The UK’s GBP 718 billion (USD 946.90 billion) infrastructure pipeline, including the Lower Thames Crossing, sustains bridge-deck adhesive demand into the next decade.

By End-use Sector: Residential Volume Versus Infrastructure Growth

Residential held 36.78% of 2025 revenue due to mass retrofits financed by recovery funds, but infrastructure is expected to grow at 6.23% CAGR during the forecast period (2026-2031) as governments channel stimulus into rail, highways, and tunnels. Commercial segments revive as office retrofits return, yet remain below 2019 occupancy. Industrial uptake waits on energy-price relief before large logistics hubs proceed.

Infrastructure bids favor suppliers ready with DPP, EPD, and low-embodied-carbon proofs, lifting average selling prices despite material inflation. Residential renovators choose water-borne systems to speed interior re-occupancy, and SME installers prefer one-component, primer-less offerings to manage scarce labor.

Geography Analysis

Germany’s market share in 2025 was 24.48%, and this size gain from Deutsche Bahn’s EUR 12.5 billion (USD 14.59 billion) station, track, and roofing upgrades lifts sealant consumption for expansion gaps and platform waterproofing. Public tenders now rate bids on DPP completeness and EPD carbon factors, elevating compliant suppliers. Skilled-labor shortages remain acute, so primer-less and fast-cure products gain traction across Länder.

In Italy, the EUR 2.9 billion (USD 3.27 billion) ASPI overhaul touches 2,855 km of highways, 40 bridges, and 87 tunnel tubes. Polyurethane sealants formulated for ±25% movement and 25-year durability command premiums on viaduct joints, while high-viscosity epoxy adhesives secure crash-barrier anchors. Water-borne tile adhesives enjoy pull-through in residential refurbishments financed by the Superbonus 110% scheme that extends to 2027.

Rest-of-Europe consolidates niche strengths: Sweden’s 90% prefab ratio drives hot-melt lines; Austria’s Semmering and Brenner tunnels consume spray-applied waterproofing membranes; the Netherlands mandates whole-life carbon calculations in municipal projects, converting façade contractors en masse to carbon-neutral silicones. Eastern Europe’s lagging adoption gap narrows as TEN-T corridors unlock EU grants tied to low-carbon materials, incrementally raising Europe construction adhesives & sealants market share for vetted suppliers.

Competitive Landscape

The Europe Construction Adhesives & Sealants market is moderately concentrated. Strategic moves in 2025 included Sika’s Fast Forward efficiency program targeting CHF 150-200 million (USD 181.1-241.4 million) annual savings by 2028; Dow’s rollout of PAS 2060-verified silicones; and Hydro’s scaling of 75R recycled aluminum façade profiles. Competition intensifies as the 1 July 2026 CLP deadline narrows reformulation windows, likely nudging SME exits or acquisitions by capital-rich multinationals.

Europe Construction Adhesives And Sealants Industry Leaders

Henkel AG & Co. KGaA

MAPEI S.p.A.

Sika AG

Arkema

H.B. Fuller Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Bolton Group laid the foundation stone for a sustainable adhesive product plant in Rheinmünster, Germany. This plant is expected to be ready by 2027 and will grant a production capacity of 170 million products annually.

- October 2025: Henkel Adhesive Technologies` construction adhesives business started offering an increasing number of Environmental Product Declarations (EPDs) in Germany and other countries. These declarations provide detailed insights into the environmental footprint of individual products.

Europe Construction Adhesives And Sealants Market Report Scope

Adhesives are substances that join or bond two or more surfaces together by sticking to them. They are a type of material that provides cohesion between different substrates, creating a durable and often permanent bond. Adhesives are used in various applications, from everyday household use to industrial and technological processes.

Sealants are materials used to fill, seal, or close gaps and joints to prevent the passage of liquids or gases. They are designed to provide a barrier against moisture, air, dust, and other environmental elements. Sealants are commonly used in construction, automotive, aerospace, and other industries to create airtight and watertight seals and provide insulation and protection.

The Europe Construction Adhesives and Sealants market is segmented by resin type, technology, application, end-use sector, and geography. By resin type, the market is segmented into acrylic, cyanoacrylate, epoxy, polyurethane, silicone, VAE/EVA, and other resins. By technology, the market is segmented into water-borne, solvent-borne, reactive, hot-melt, and sealants (1K and 2K). By application, the market is segmented into flooring and tiling, roofing, wall panels and facades, insulation and weatherproofing, and infrastructure joints (bridges and tunnels). By end-use sector, the market is segmented into residential, commercial, industrial, and infrastructure. The report also covers the market size and forecasts for construction adhesives and sealants in 6 countries across the region. The market sizes and forecasts are provided in terms of value (USD).

By Resin

| Acrylic |

| Cyanoacrylate |

| Epoxy |

| Polyurethane |

| Silicone |

| VAE/EVA |

| Others |

By Technology

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot-melt |

| Sealants (1K and 2K) |

By Application

| Flooring and Tiling |

| Roofing |

| Wall Panels and Facades |

| Insulation and Weatherproofing |

| Infrastructure Joints (bridges and tunnels) |

By End-use Sector

| Residential |

| Commercial |

| Industrial |

| Infrastructure |

By Country

| France |

| Germany |

| Italy |

| Russia |

| Spain |

| United Kingdom |

| Rest of Europe |

| By Resin | Acrylic |

| Cyanoacrylate | |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| VAE/EVA | |

| Others | |

| By Technology | Water-borne |

| Solvent-borne | |

| Reactive | |

| Hot-melt | |

| Sealants (1K and 2K) | |

| By Application | Flooring and Tiling |

| Roofing | |

| Wall Panels and Facades | |

| Insulation and Weatherproofing | |

| Infrastructure Joints (bridges and tunnels) | |

| By End-use Sector | Residential |

| Commercial | |

| Industrial | |

| Infrastructure | |

| By Country | France |

| Germany | |

| Italy | |

| Russia | |

| Spain | |

| United Kingdom | |

| Rest of Europe |

Market Definition

- End-user Industry - Residential construction, commercial construction, public buildings, industrial buildings and infrastructure projects are considered under the construction industry.

- Product - All adhesive and sealant products used in construction industry are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and Sealants technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms