Enterprise Manufacturing Intelligence Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.03 Billion |

| Market Size (2031) | USD 13.92 Billion |

| Growth Rate (2026 - 2031) | 22.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Manufacturing Intelligence Market Analysis by Mordor Intelligence

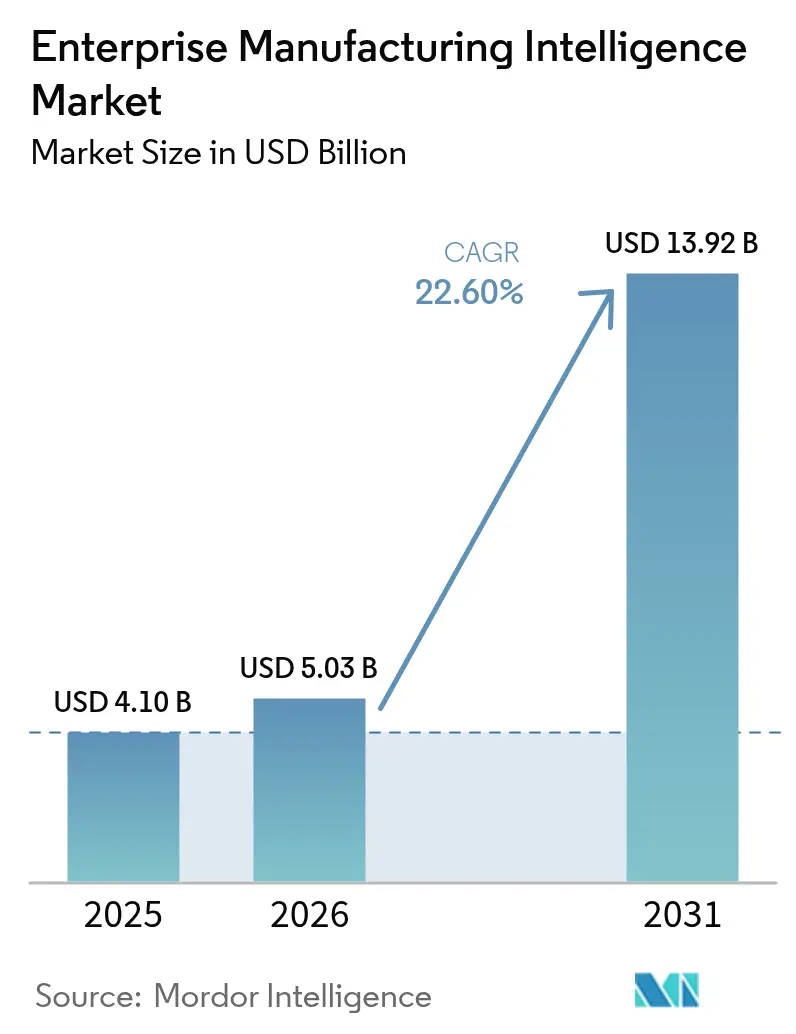

The Enterprise Manufacturing Intelligence market size was valued at USD 4.1 billion in 2025 and estimated to grow from USD 5.03 billion in 2026 to reach USD 13.92 billion by 2031, at a CAGR of 22.6% during the forecast period (2026-2031). Robust demand stems from manufacturers replacing stand-alone automation with predictive systems that blend operational technology and artificial intelligence. Continuous investments in private 5G networks, edge computing, and digital twins shorten decision cycles, while policy incentives link overall equipment effectiveness (OEE) to green financing. Moderate competitive intensity lets incumbents monetize installed bases even as cloud-native specialists court fast adopters. Heightened cyber-security risks, talent gaps in IT-OT integration, and macro-economic uncertainty remain headwinds, but documented returns such as 10-15% OEE gains and up to 60% lower quality-control costs sustain capital allocation.[1]European Commission, “Clean Industrial Deal Factsheet,” europa.eu

Key Report Takeaways

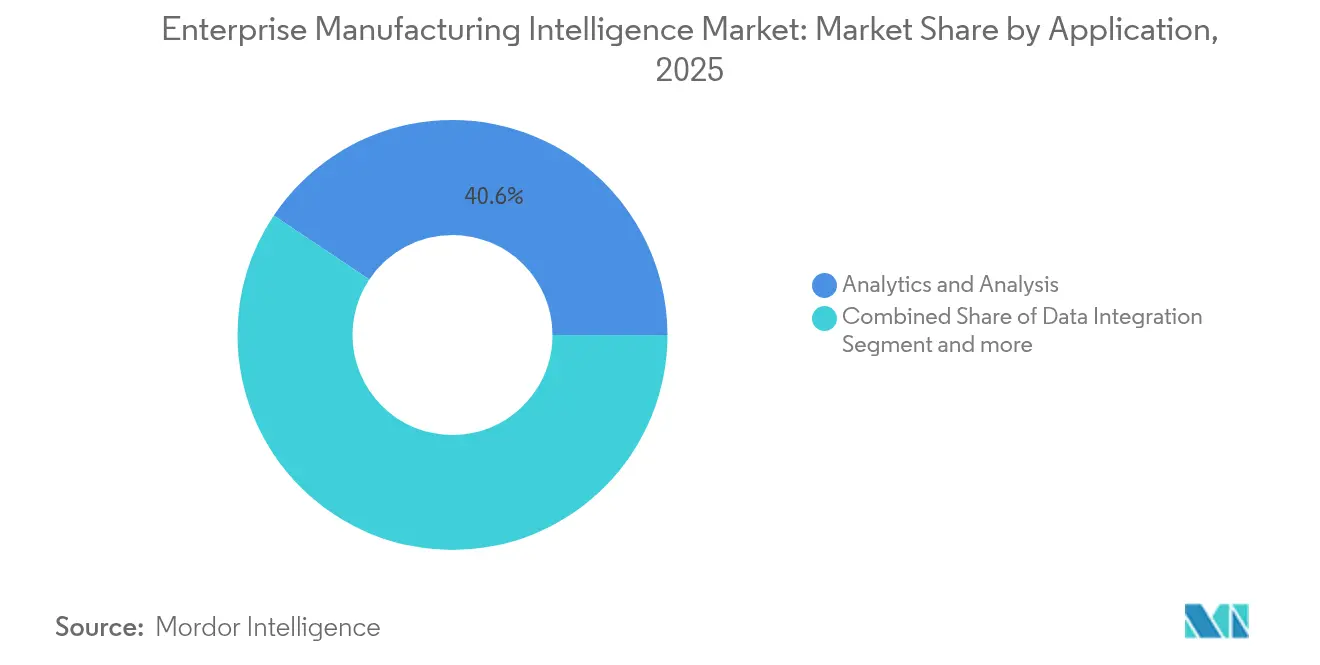

- By application, Analytics and Analysis led with 40.62% revenue share in 2025; Workflow and KPI Management is forecast to advance at a 27.09% CAGR through 2031.

- By end-user industry, automotive held 23.52% of the Enterprise Manufacturing Intelligence market share in 2025, while pharmaceuticals and biotechnology are set to expand at a 25.54% CAGR to 2031.

- By deployment mode, on-premises accounted for 54.22% of the Enterprise Manufacturing Intelligence market size in 2025; cloud-native deployments will grow at a 27.68% CAGR through 2031.

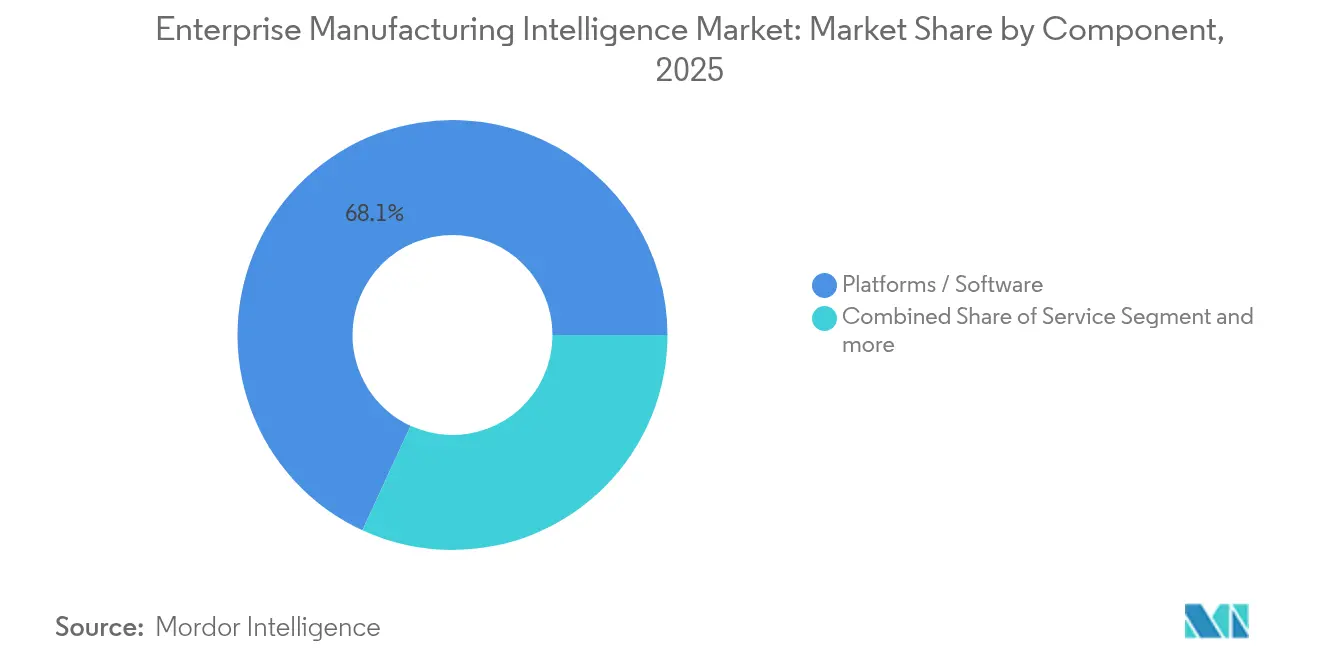

- By component, platforms/software captured 68.12% revenue share in 2025; services record the highest projected CAGR at 27.63% to 2031. North America commanded 37.71% of global revenue in 2025; Asia-Pacific is the fastest-growing region at a 26.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enterprise Manufacturing Intelligence Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift-left analytics enables real-time quality-by-design | 4.20% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Digital thread requirements in smart factories | 3.80% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Integration of industrial 5G & edge AI | 3.50% | Global, led by APAC and North America | Medium term (2-4 years) |

| Economies' green-deal subsidies linked to OEE KPIs | 2.90% | Europe primary, expanding to North America | Long term (≥ 4 years) |

| Rising use of low-code composable apps by operators | 2.10% | Global, with faster adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift-left Analytics Enables Real-time Quality-by-design

Real-time analytics embedded into production detect deviations at origin and have lowered scrap by as much as 30% at facilities such as Samsung Biologics, where computational fluid-dynamics models run inline to adjust biopharma parameters instantly. Machine-learning algorithms now forecast quality outcomes from upstream signals, closing the gap between design intent and manufacturing reality. Regulated industries gain added value because early defect detection prevents recalls and regulatory penalties. When integrated with execution platforms, AI-powered control loops keep processes within specification while maximizing throughput. These outcomes strengthen executive support for scaled deployments across multi-site networks. [2]Samsung Biologics, “Digital Bioprocessing for Real-time Quality Control,” samsungbiologics.com

Digital Thread Requirements in Smart Factories

End-to-end digital threads connect design, production, and service data, letting manufacturers trace issues back to specific process settings and material lots. Aerospace supplier Safran Aero Boosters uses PTC ThingWorx to link engineering models with shop-floor execution, enabling predictive maintenance and continuous improvement. The concept is expanding to suppliers through blockchain-backed traceability that ensures data integrity for audit readiness. Seamless connectivity also lets global plants adopt best practices in real time, accelerating product launches and shortening change-management cycles.

Integration of Industrial 5G and Edge AI

Private 5G networks eliminate latency barriers and support millisecond-level control required for autonomous mobile robots and vision inspection. Hyundai Motor and Samsung demonstrated RedCap 5G that delivers dedicated wireless capacity for mission-critical tasks in smart factories. Edge AI processes video and sensor data locally, addressing sovereignty concerns and improving resilience when cloud links falter. Combined, these technologies enable adaptive cells that self-optimize workflow orchestration without human intervention.

Economies’ Green-deal Subsidies Linked to OEE KPIs

European Clean Industrial Deal programs reward measurable efficiency, prompting factories to install intelligence platforms that track energy use and waste against real-time OEE dashboards. Subsidy eligibility hinges on continuous monitoring, accelerating platform demand among producers seeking preferential financing. Solutions that integrate sustainability metrics with production analytics now form a core requirement in supplier RFPs across automotive and food processing plants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pay-back hesitation in brown-field retrofits | -2.80% | Global, particularly in mature industrial regions | Medium term (2-4 years) |

| Persistent data ownership uncertainty in multi-tier supply chains | -1.90% | Global, with higher impact in regulated industries | Long term (≥ 4 years) |

| Talent shortage in IT-OT data engineering | -1.50% | Global, acute in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pay-back Hesitation in Brown-field Retrofits

Legacy plants struggle to justify sensor retrofits and integration work that interrupt production and stretch pay-back periods. Managers favour projects with immediate savings, delaying holistic intelligence rollouts. The risk of disrupting long-lifecycle assets, alongside capex freezes in cyclical sectors, pushes many firms to pilot limited scopes rather than commit to enterprise-wide deployments.

Persistent Data Ownership Uncertainty in Multi-tier Supply Chains

Multi-stakeholder networks face conflicting expectations over who controls granular production data. OEMs demand transparency for quality assurance, while suppliers fear IP exposure. Absent clear legal frameworks for liability, parties hesitate to share data across cloud platforms, slowing adoption of cross-enterprise analytics—especially in pharmaceuticals, where strict validation rules raise additional compliance costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Analytics and KPI Platforms Anchor Adoption

Analytics and Analysis held a 40.62% slice of 2025 revenue, confirming that insight generation underpins every deployment of the Enterprise Manufacturing Intelligence market. Workflow and KPI Management, forecast at a 27.09% CAGR, reflects the pivot from static reports to real-time, closed-loop performance control. Visualization tools and data-integration layers round out typical stacks but spend concentrates where algorithms deliver measurable throughput gains.

Enterprises now tie operator workflows to machine learning outputs that guide decision steps, creating self-adjusting lines. Honeywell’s explainable-AI modules exemplify how contextual guidance slashes downtime and training overhead. As generative interfaces mature, query-by-voice dashboards let frontline staff interrogate live plant metrics, shrinking the barrier between domain experts and shop-floor data.

By End-user Industry: Automotive Dominance, Pharma Momentum

Automotive producers accounted for 23.52% revenue in 2025 through extensive platform rollouts for body-shop robotics and final-assembly sequencing. Pharmaceuticals and biotechnology will post the fastest 25.54% CAGR as regulators mandate continuous process verification and digital twins. The Enterprise Manufacturing Intelligence market size for drug makers is forecast to expand fastest because batch genealogy and sterile conditions require granular, time-stamped datasets.

GlaxoSmithKline’s digital twin vaccines project reports tangible yield increases after virtual validation of recipe changes. Aerospace and defense firms concentrate on digital-thread traceability to meet export-control audits, while semiconductor fabs exploit inline analytics for sub-micron defect detection. Food processors also climb the adoption curve due to stringent safety protocols.

By Component: Platforms Dominate, Services Accelerate

Software platforms captured 68.12% share in 2025 as buyers prioritize configurable suites over point solutions. Yet services will outpace at 27.63% CAGR because multi-disciplinary expertise is needed to harmonize legacy devices, retrain staff, and iterate models. Siemens’ AI consulting practice addresses this gap, packaging change management with turnkey deployments. Embedded hardware evolves towards AI-on-chip gateways that run inference locally, shrinking data transfer and enabling lights-out cells in clean-room environments. Vendors co-design reference architectures to guarantee deterministic behaviour from sensor to dashboard, further lowering integration risk.

By Deployment Mode: Cloud-native Surges Past Early Security Doubts

On-premises installations represented 54.22% of the Enterprise Manufacturing Intelligence market size in 2025 because operators favoured local control over latency-sensitive assets. Cloud-native offerings, projected at a 27.68% CAGR, now integrate zero-trust architectures and region-restricted storage to alleviate sovereignty fears. Hybrid edge-cloud models provide deterministic response on-site while routing heavy analytics to the cloud.

Microsoft’s industry-specific data services grant manufacturers managed Kubernetes clusters that host real-time models adjacent to ERP data, reducing integration complexity. The resulting elasticity helps seasonal producers flex capacity without stranded hardware costs, accelerating budget approvals for cloud expansions.

Geography Analysis

North America controlled 37.71% of 2025 global revenue as early adopters such as Procter and Gamble embedded hybrid cloud execution systems that unify more than 100 plants. Federal reshoring incentives and partnerships with hyperscalers reinforce momentum by funding lighthouse sites that showcase OEE boosts. An extensive ecosystem of system integrators supplies talent pipelines that de-risk rollouts for mid-sized manufacturers.

Asia-Pacific will post the fastest 26.41% CAGR through 2031. China, Japan, and South Korea funnel state grants into Industry 4.0 pilots, while Singapore’s nation-wide digital-factory roadmap prescribes baseline connectivity standards. Electronics and battery producers lead adoption to offset tight labour markets and meet export quality thresholds. Regional cloud providers now operate local availability zones to satisfy data-residency regulations, widening access for tier-2 suppliers. Europe leverages regulatory levers such as the Clean Industrial Deal, steering capital towards platforms that document emissions alongside OEE. German automotive clusters pilot blockchain provenance to certify recycled steel, and Italian food-processing lines deploy AI to cut energy use. Brexit-triggered supply-chain shocks elevate the need for inventory visibility from Midlands aerospace plants to mainland tier-1 suppliers, cementing Enterprise Manufacturing Intelligence adoption as a resilience strategy.

Competitive Landscape

Industry incumbents including Siemens, ABB, and Honeywell bundle software upgrades with their automation footprints, offering seamless migration paths for existing PLC and DCS estates. Siemens’ USD 10 billion acquisition of Altair Engineering in 2025 augments the portfolio with CAE and AI-driven simulation, reinforcing its digital-thread narrative. These firms exploit lifetime service contracts to cross-sell cloud analytics modules and sustain revenue beyond hardware.

Mid-market challengers such as Sight Machine focus on rapid ROI via pre-built data models for discrete manufacturing, while Tulip’s low-code apps empower operators to digitize forms without coding. Partnerships, not zero-sum rivalry, shape go-to-market strategies: cloud hyperscalers integrate OT connectors, and MES vendors white-label analytics engines to extend reach. Co-innovation labs involving suppliers and OEMs streamline validation cycles in regulated contexts like pharma.

Start-ups secure funding by specializing in niche pain points such as serialization compliance or AI vision kits. Venture arms of OEMs scout these innovators to plug feature gaps; Mitsubishi Electric’s stake in Formic Technologies exemplifies such moves to deliver robot-as-a-service for SMEs. Despite deal activity, no single vendor controls a dominant share, preserving customer leverage in procurement negotiations. [4]Siemens AG, “Siemens to Acquire Altair Engineering to Strengthen Simulation and AI Portfolio,” press.siemens.com

Enterprise Manufacturing Intelligence Industry Leaders

Siemens AG

Rockwell Automation Inc.

Honeywell International Inc.

Emerson Electric Co.

AVEVA Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Siemens invested CAD 150 million in a Global AI Manufacturing Technologies RandD Center for battery production in Canada.

- February 2025: Hyundai Motor and Samsung unveiled private 5G RedCap technology to improve mission-critical factory connectivity.

- January 2025: L2L Inc. acquired Accumine Technologies to enhance connected-workforce solutions, releasing L2L Connect for simplified machine data collection.

Global Enterprise Manufacturing Intelligence Market Report Scope

The enterprise manufacturing intelligence is basically a software solution that can collect and present all the manufacturing-related data from multiple sources primarily to provide the decision-makers with information about the organization's performance. Moreover, by centralizing all the manufacturing data, the software allows the users to easily find the information needed, regardless of the source, and can easily perform analysis on any characteristics of manufacturing, related to production costs, capacity, quality, resources available, among others.

| Data Integration |

| Analytics & Analysis |

| Visualization / Dashboards |

| Workflow & KPI management |

| Automotive |

| Aerospace & Defense |

| Electronics & Semiconductors |

| Food & Beverage |

| Chemicals & Materials |

| Pharmaceuticals & Biotech |

| On-premise |

| Hybrid (Edge + Cloud) |

| Cloud-native |

| Platforms / Software |

| Services |

| Embedded Analytics Hardware |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Europe | Italy |

| France | |

| United Kingdom | |

| Germany | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Africa | Nigeria |

| South Africa | |

| Kenya |

| By Application | Data Integration | |

| Analytics & Analysis | ||

| Visualization / Dashboards | ||

| Workflow & KPI management | ||

| By End-user Industry | Automotive | |

| Aerospace & Defense | ||

| Electronics & Semiconductors | ||

| Food & Beverage | ||

| Chemicals & Materials | ||

| Pharmaceuticals & Biotech | ||

| By Deployment Mode | On-premise | |

| Hybrid (Edge + Cloud) | ||

| Cloud-native | ||

| By Component | Platforms / Software | |

| Services | ||

| Embedded Analytics Hardware | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Europe | Italy | |

| France | ||

| United Kingdom | ||

| Germany | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Africa | Nigeria | |

| South Africa | ||

| Kenya | ||

Key Questions Answered in the Report

What is the current value of the Enterprise Manufacturing Intelligence market?

The market stands at USD 5.03 billion in 2026 and is forecast to reach USD 13.92 billion by 2031, reflecting a 22.6% CAGR.

Which region holds the largest Enterprise Manufacturing Intelligence market share today?

North America leads with 37.71% of global revenue in 2025 due to early AI-driven smart-factory investments.

Which application segment is growing the fastest?

Workflow and KPI Management applications are projected to expand at a 27.09% CAGR between 2026 and 2031.

Why are pharmaceuticals adopting Enterprise Manufacturing Intelligence platforms rapidly?

Strict regulatory demands for real-time batch tracking and digital twins push pharmaceutical companies toward 25.54% CAGR adoption.

How are private 5G networks influencing manufacturing intelligence deployments?

Dedicated 5G reduces latency to millisecond levels, enabling edge AI for autonomous robots and real-time quality inspection on the shop floor.

What limits Enterprise Manufacturing Intelligence uptake in legacy plants?

Brown-field retrofit projects often face extended pay-back periods, making executives cautious about full-scale platform installation.

Page last updated on: