Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Intelligent Process Automation Market is Segmented by Technology (Robotic Process Automation, Natural Language Processing, and More), Component (Platform / Software, and Services), Deployment (On-Premise, Cloud, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Vertical (Manufacturing, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

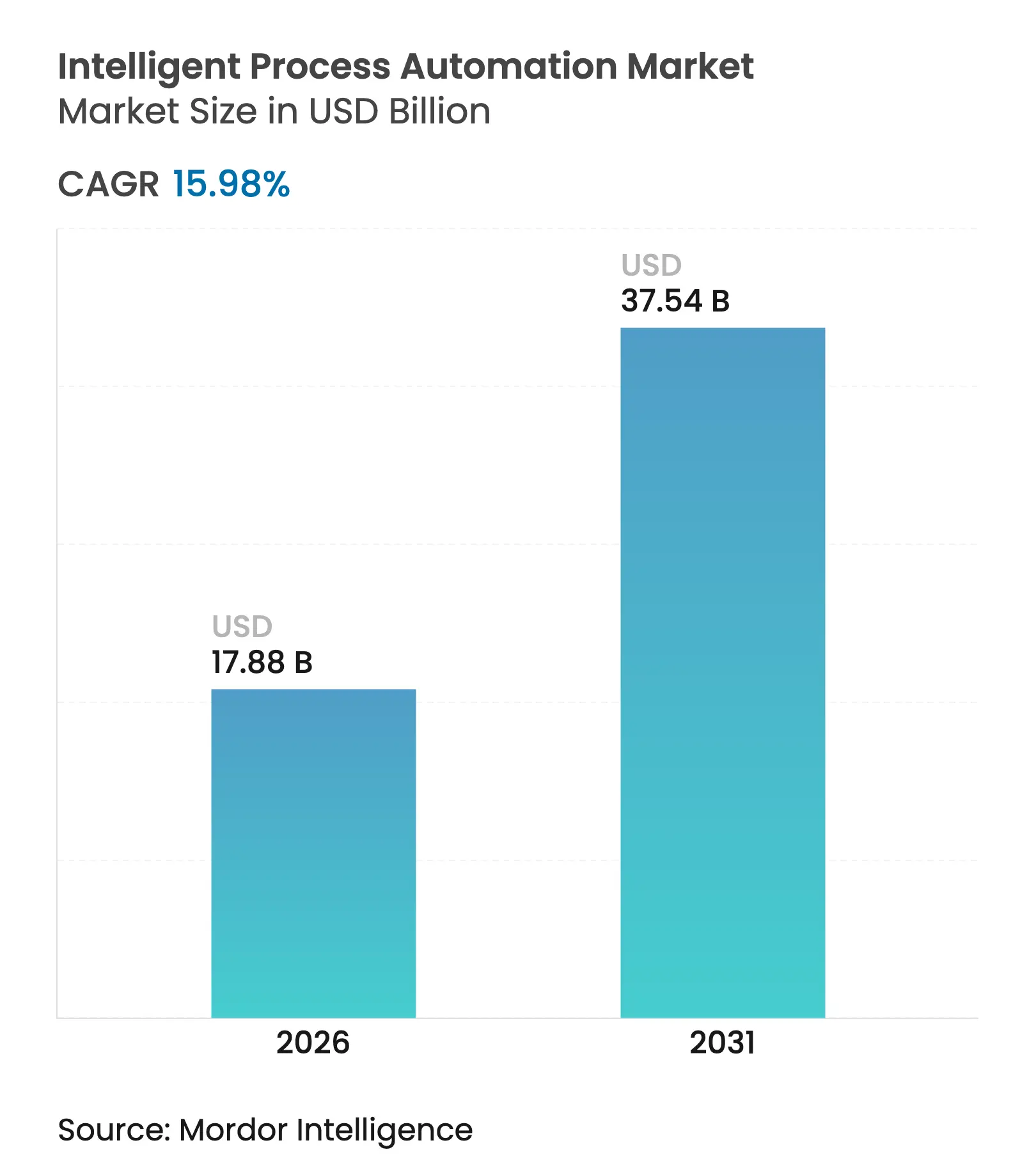

| Market Size (2026) | USD 17.88 Billion |

| Market Size (2031) | USD 37.54 Billion |

| Growth Rate (2026 - 2031) | 15.98 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The intelligent process automation market size is expected to grow from USD 15.42 billion in 2025 to USD 17.88 billion in 2026 and is forecast to reach USD 37.54 billion by 2031 at 15.98% CAGR over 2026-2031. Growth has been propelled by enterprises replacing rules-based bots with cognitive platforms that merge artificial intelligence, machine learning, and natural-language processing, allowing unstructured data handling and real-time decision making. Pandemic-era supply-chain shocks, emerging AI-governance mandates, and the maturation of cloud-native automation suites widened board-level attention on operational resilience. Early movers in banking, healthcare, and manufacturing reported 25-35% run-rate savings and 50-60% cycle-time cuts after full-scale deployments. Vendors responded with “agentic” capabilities that learn process context and orchestrate complex workflows autonomously, compressing time-to-value for both Fortune 500 and mid-market adopters.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Demand for operational efficiency and cost reduction

Demand for operational efficiency and cost reduction

| +3.2% | Global | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

+3.2%

|

Geographic Relevance

:

Global

|

Impact Timeline

:

Short term (≤ 2 years)

|

Advancements in AI and machine learning

Advancements in AI and machine learning

| +4.1% | North America and the EU, APAC core | Medium term (2-4 years) | |||

Growing adoption of cloud-based automation

Growing adoption of cloud-based automation

| +2.8% | Global, early gains in North America, Europe | Short term (≤ 2 years) | |||

Integration with low-code / no-code ecosystems

Integration with low-code / no-code ecosystems

| +2.3% | Global, SME-heavy regions | Medium term (2-4 years) | |||

Sustainability-linked automation for Scope-3 reporting

Sustainability-linked automation for Scope-3 reporting

| +1.7% | EU, North America, select APAC | Long term (≥ 4 years) | |||

Post-quantum cryptography compliance

Post-quantum cryptography compliance

| +1.4% | Government and regulated industries globally | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Demand for operational efficiency and cost reduction

Enterprise finance, HR, and supply-chain leaders deployed cognitive bots to blunt wage inflation and margin pressure. Post-deployment surveys showed 80% of finance chiefs planning new IPA rollouts and realizing 25-35% annual cost take-outs while halving process cycle times.[1]SolveXia, “32 Finance Automation Trends and Statistics for 2025,” solvexia.com These wins reframed automation from a tactical tool into a foundational element of digital operating models. As more workflows were digitalized, manual interventions created bottlenecks that threatened customer experience, accelerating board approvals for enterprise-wide IPA budgets.

Advancements in AI and machine learning

Generative large-language models let automation platforms interpret context, correct exceptions, and adjudicate decisions once reserved for human analysts. Automation Anywhere’s Process Reasoning Engine showed how AI agents capture enterprise intent and manage end-to-end workflows without rigid scripts. Document-heavy sectors such as legal and healthcare, automated contract review and patient-record coding, are expanding the intelligent process automation market's addressable workload.

Growing adoption of cloud-based automation platforms

Cloud deployments represented 67% of new customer projects by early 2024, up from single digits five years earlier. Subscription pricing aligned costs with realized value, speeding adoption among mid-market firms. Hyperscaler ecosystems bundle AI services, secure APIs, and compliance tooling, enabling global rollouts in days and shrinking infrastructure overheads for even the largest banks.

Integration with low-code / no-code ecosystems

Business users authored automations inside visual builders, reducing reliance on scarce developers. Public-sector agencies built citizen-service workflows in weeks, mitigating talent shortfalls and elevating service quality. Low-code platforms now embed pre-trained AI models, letting non-technical staff orchestrate invoice classification or customer emails without writing code, broadening the intelligent process automation market user base.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Complexity in implementation

Complexity in implementation

| -2.1% | Global, complex enterprise environments | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-2.1%

|

Geographic Relevance

:

Global, complex enterprise environments

|

Impact Timeline

:

Short term (≤ 2 years)

|

Data security and privacy concerns

Data security and privacy concerns

| -1.8% | EU (GDPR), North America, and regulated industries globally | Medium term (2-4 years) | |||

Rising costs of specialized AI talent

Rising costs of specialized AI talent

| -1.3% | Global, acute in North America and Western Europe | Medium term (2-4 years) | |||

Regulatory scrutiny under emerging AI laws

Regulatory scrutiny under emerging AI laws

| -1.1% | EU (AI Act), emerging in North America and APAC | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Complexity in implementation

Deploying AI-infused automation across legacy estates exposed integration gaps, data silos and change-management hurdles. Enterprises underestimated the effort to standardize workflows and tune machine-learning models, delaying go-live by quarters and depressing early ROI. Heterogeneous ERP landscapes lacking modern APIs forced expensive middleware workarounds, while immature best practices for agentic bots raised governance risks.

Data security and privacy concerns

Cloud IPA pipelines move sensitive records through external infrastructure, raising fears of breaches and non-compliance. The EU AI Act obliges explainability, algorithmic-bias audits, and data-lineage tracing, inflating deployment overheads. Post-quantum encryption upgrades loom, compelling vendors to harden cryptographic stacks and customers to reassess risk models before scaling cognitive automations.

By Technology: RPA Dominance Meets AI Enhancement

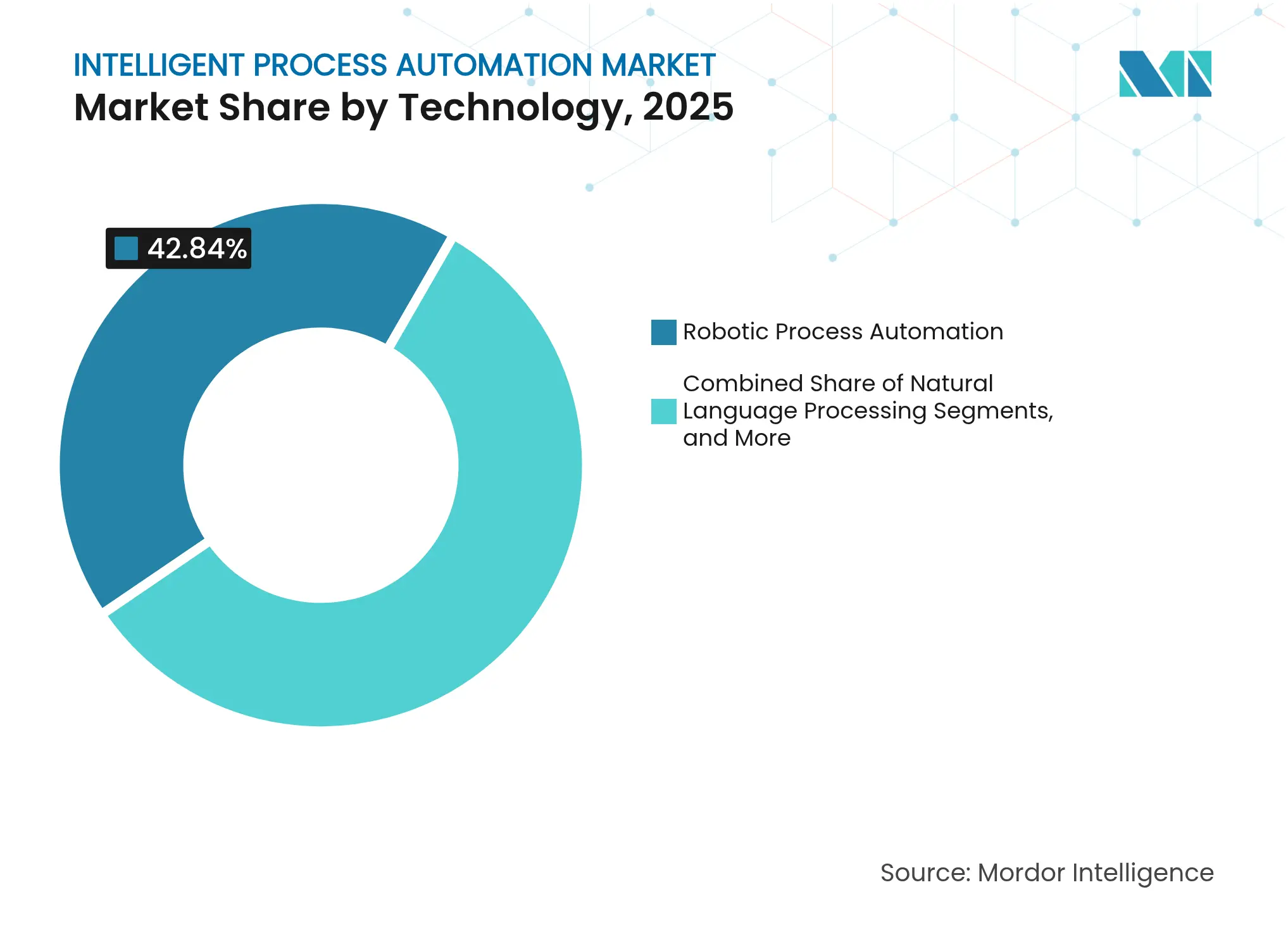

Robotic Process Automation accounted for 42.84% of the intelligent process automation market share in 2025, underscoring its entrenched role as the launchpad of digital workforce programs. Meanwhile, the intelligent process automation market size for Process Mining and Discovery is projected to compound at 26.4% CAGR to 2031 as firms map opaque workflows before injecting AI bots. Early RPA champions such as Arçelik automated 650,000 annual transactions, validating bot reliability in high-volume back offices. Cognitive add-ons—natural-language processing, computer vision, and conversational agents—have pushed automatable use cases into contract analysis, compliance monitoring, and front-office customer support.

The technology stack is now coalescing around agentic orchestration layers that learn context and self-correct. Vendors embed generative AI to summarise documents, extract entities and draft next-best actions, converting static bots into adaptive copilots. Process-mining engines surface bottlenecks and yield real-time heat maps that guide prioritisation. Integrated IPA suites bundle these capabilities, positioning vendors that own the full lifecycle—from discovery to deployment to optimisation—to capture a larger wallet share.

Note: Segment shares of all individual segments available upon report purchase

By Component: Platform Strength Drives Service Growth

Platform and Software offerings held 63.95% revenue in 2025 as buyers demanded unified environments integrating RPA, OCR, NLP, and analytics. Yet Services expanded 23.6% CAGR, signalling project complexity and skills gaps. Consulting units design target-operating models and centre-of-excellence frameworks, while implementation teams knit bots into ERP, CRM, and core-banking stacks. Managed-service providers run bot farms, monitor exceptions, and retrain models, converting IPA from a capital purchase into an outcome-based subscription.

The intelligent process automation market size for managed services will widen as enterprises confront talent scarcity and governance mandates. Vendors package pre-built industry accelerators—loan underwriting, claims adjudication, energy-plant maintenance—to shrink timelines and assure compliance. Citizen-developer enablement programs spur advisory engagements around guardrails, auditability, and lifecycle management.

By Deployment: Cloud Momentum Accelerated

Cloud deployments captured a 53.90% share in 2025, rising with a 22.7% CAGR as businesses shifted from capex to opex models. Intelligent process automation market adoption benefited from hyperscaler AI services—speech-to-text, form-recognition APIs, and large-language-model endpoints—accessible only in cloud regions. Automation Anywhere said 72% of new customers bought cloud subscriptions in 2025. On-premise remains for data-sovereign sectors, but hybrid architectures now dominate regulated industries seeking to isolate PII while tapping cloud elasticity.

Automatic platform updates deliver the latest security patches and model improvements without change-window bottlenecks. Cloud-native telemetry feeds usage analytics into vendor dashboards, enabling proactive support and consumption-based billing. These advantages entice mid-market firms previously priced out of enterprise-grade automation, widening the intelligent process automation market's total addressable base.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

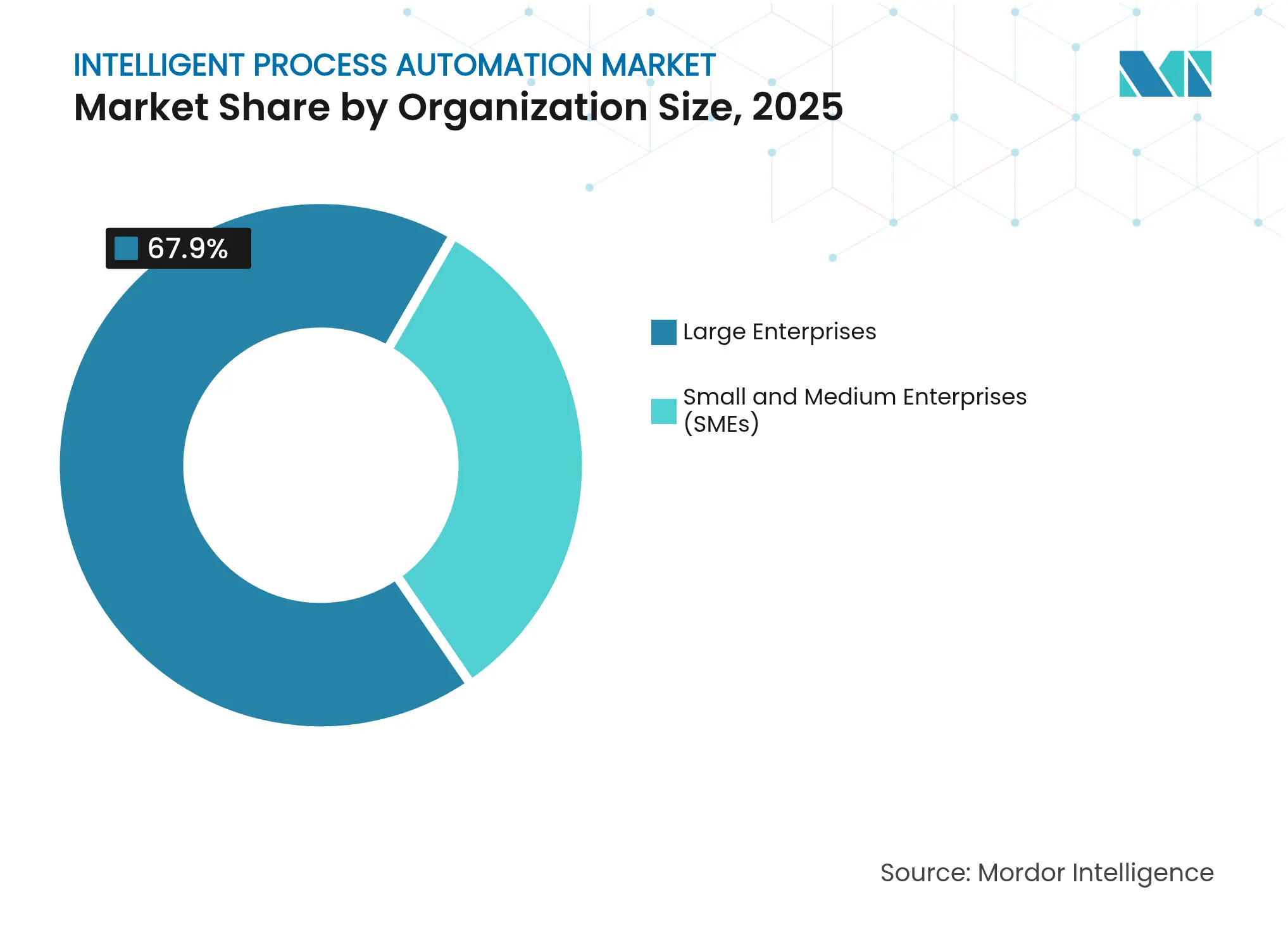

By Organization Size: SME Acceleration Transforms Market

Large Enterprises drove 67.90% revenue in 2025 through cross-functional deployments spanning finance, HR, and supply chain. However, SME adoption surged at 21.6% CAGR after low-code builders and industry templates slashed entry barriers. The intelligent process automation market now counts mid-cap retailers streamlining invoice capture and regional hospitals fast-tracking patient-record coding as mainstream buyers.

Cloud licensing aligns spend with business volume, while training-as-a-service programs upskill citizen developers in days. SMEs leverage vendor marketplaces offering plug-and-play connectors into Payables, Salesforce, or Shopify, bypassing bespoke integrations. As AI model-training costs fall, vertical-specific models reach price points affordable for small teams, further accelerating diffusion.

Note: Segment shares of all individual segments available upon report purchase

By End-User Vertical: BFSI Leadership Meets Healthcare Surge

BFSI retained 28.95% revenue in 2025, automating KYC, loan origination, and Basel reporting. NatWest cut project-approval lead times from 73 days to 73 minutes by embedding IPA in governance workflows. Meanwhile, the intelligent process automation market size tied to Healthcare and Life Sciences is forecast to swell at 24.6% CAGR as providers tackle claims backlogs and patient-record digitisation. UiPath showcases hospitals using bots to reconcile insurance codes and schedule surgeries, trimming administrative overhead.

Manufacturing reached 95% bot adoption or evaluation, leveraging computer-vision QA and predictive maintenance to avert downtime. Retailers automate inventory reconciliation and return management, while logistics players deploy AI-guided route planning to reduce fuel spend and emissions.

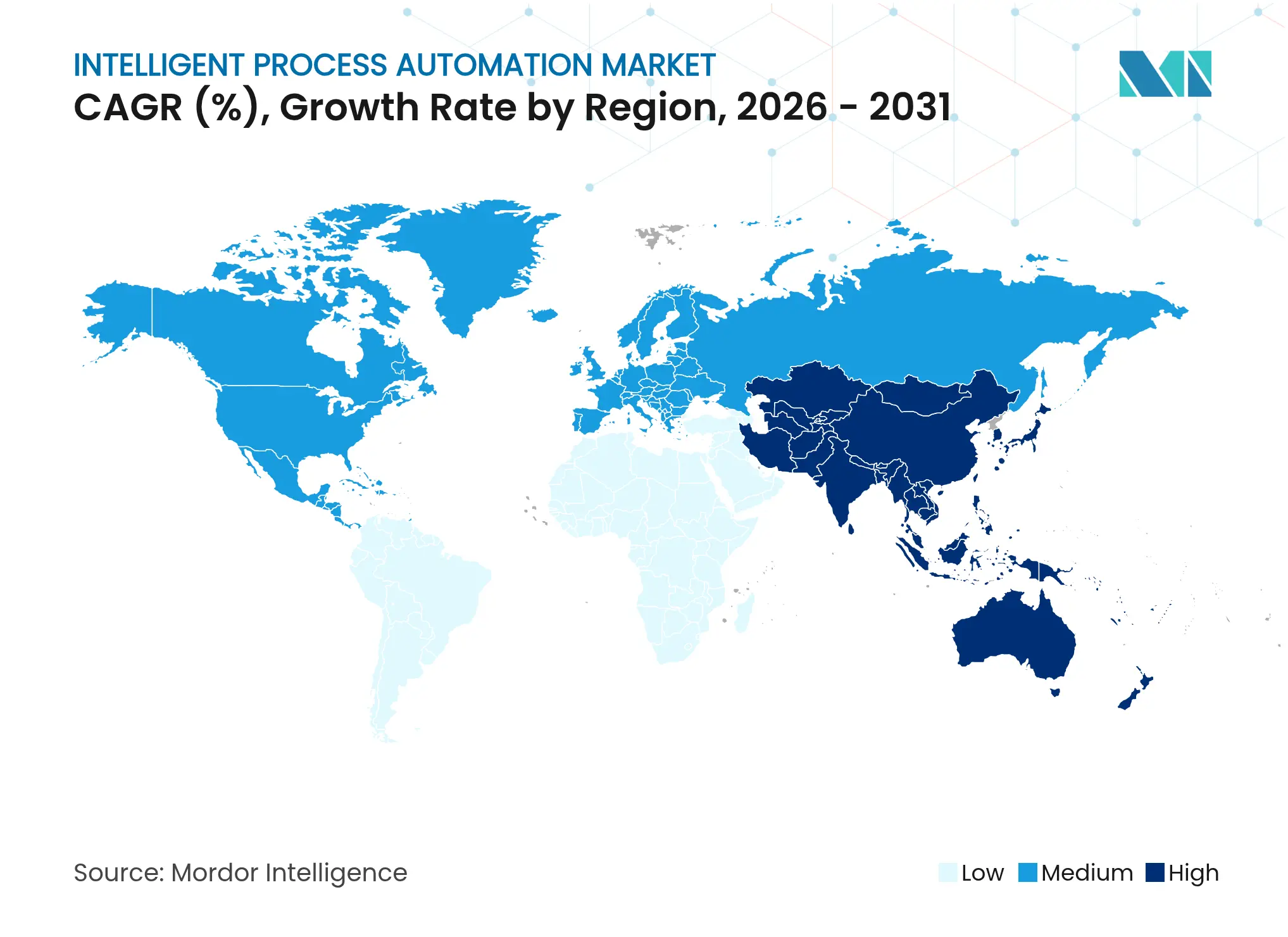

North America retained 36.92% revenue in 2025 after first-mover enterprises scaled cognitive automation across entire business-process stacks. Government agencies widened adoption for tax processing, benefits, and public health surveillance, further deepening market penetration. Mature compliance frameworks provided clarity for AI audits and model governance, encouraging aggressive rollouts inside health insurers and tier-1 banks.

Asia-Pacific ranked as the fastest-growing region, advancing 20.7% CAGR to 2031. Enterprises leapfrogged on-premise estates, subscribing directly to cloud IPA suites that bundle speech analytics and low-code orchestration. Governments in India and Southeast Asia promoted automation as part of national digital-economy blueprints, subsidising SME adoption and training programs. The young, tech-literate workforce shortened learning curves, enabling rapid citizen-developer uptake and fuelling the intelligent process automation market momentum.

Europe’s stringent GDPR and upcoming AI Act shaped platform requirements around explainability, bias mitigation, and data-sovereignty controls. Vendors added audit logs and algorithmic-risk dashboards to satisfy regulators. Sustainability-linked automations gained traction as firms used IPA to compute Scope-3 emissions and populate ESG disclosures, illustrated by Climatiq’s Autopilot launch that converts procurement spend into carbon metrics. Middle East and Africa and South America remained nascent but reported double-digit growth as manufacturers and banks pursued cost-out programs amid macro headwinds.

Market Concentration

The intelligent process automation market displayed moderate fragmentation in 2025. UiPath, Automation Anywhere, and Microsoft anchored platform ecosystems, while Celonis, SS&C Blue Prism, and industry-specific newcomers targeted process-mining, managed RPA, and vertical templates. Competitive intensity rose through alliances rather than consolidations; UiPath linked with Inflection AI to deliver private-cloud agentic bots for security-sensitive customers. Automation Anywhere embedded Azure OpenAI to let citizen developers build generative-AI agents without leaving its interface.

Specialists gained a share in document understanding and process discovery, exploiting gaps in incumbent portfolios. Low-code vendors bundled native RPA, eroding standalone bot license growth. Vendors now compete on successful time-to-value metrics, security posture, and pre-built domain accelerators rather than raw bot counts. Quantum-safe encryption roadmaps and zero-trust architectures emerged as differentiators for regulated buyers.[4]Lattice Semiconductor, “Cybersecurity Solutions for the AI and Quantum Era,” latticesemi.com

Managed-service integrators forged co-sell pacts with platform providers to deliver end-to-end automation-as-a-service. These alliances address the skills shortage, offering outcome-based SLAs that guarantee exception handling and model retraining. As a result, spend is consolidating with vendors able to orchestrate discovery, design, deployment, and ongoing optimisation under one commercial umbrella.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Our study, according to Mordor Intelligence, defines the intelligent process automation market as global revenue generated by software platforms, from stand-alone RPA bots to integrated cognitive suites, and the related implementation services that apply AI, machine learning, computer vision, natural language processing, and process-mining to automate repetitive as well as judgment-oriented business workflows.

Scope Exclusion: Pure industrial motion-control hardware and traditional business-process outsourcing fees are excluded.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

We interviewed automation architects, system integrators, and shared-service heads across North America, Europe, and Asia-Pacific to test license-fee ranges, average bot counts per process, and conversion rates from pilots to scaled programs, filling gaps spotted in desk work.

Desk Research

Analysts gathered public data from sources such as United States Bureau of Labor Statistics productivity files, Eurostat ICT surveys, OECD digital-economy indicators, Questel patent libraries, Volza shipment dashboards, and IEEE Intelligent Systems papers. Company filings, investor calls, and technology news streams on Dow Jones Factiva added adoption and pricing clues. The sources named here are only a subset of those consulted.

Market-Sizing & Forecasting

The 2025 baseline was built with a top-down reconstruction of enterprise IT spending that isolates automation budgets by industry, then checked against bottom-up supplier revenue samples and channel inquiries. Core drivers, bot price erosion, cloud-subscription mix, process-mining uptake, service-attach ratios, and generative AI premium uplift, feed a multivariate regression that projects demand to 2030. Missing figures are imputed by benchmarking peers of similar scale and geography.

Data Validation & Update Cycle

Results pass three-layer variance checks and senior review before sign-off. We refresh each model annually, and material market events trigger interim updates so clients receive the latest view.

Why Mordor's Intelligent Process Automation Baseline Commands Reliability

Benchmark comparison

Published numbers differ; one 2024 study quotes USD 14.55 billion, another places the 2025 value at USD 18.26 billion, while a further outlook cites USD 25.9 billion for 2027.

Estimates diverge because each publisher varies service inclusions, rollout assumptions, and currency handling. Mordor's scope stays fixed on platform and enablement revenue only; its exchange rates follow IMF averages, and its refresh cadence is annual, which reduces distortion.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 15.42 B (2025) | Mordor Intelligence | Anonymized source:Mordor Intelligence | Primary gap driver: | |

USD 14.55 B (2024) | Global Consultancy A | Counts services only, omits platform subscriptions | ||

USD 18.26 B (2025) | Analyst Firm B | Assumes very high enterprise rollout rates and bundles predictive analytics tools | ||

USD 25.90 B (2027) | Trade Journal C | Extends 2022 growth linearly and ignores price compression |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Opportunities in Singapore's Chemical Logistics Market

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.