Internet Of Things In Banking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 51.4 Billion |

| Market Size (2031) | USD 200.18 Billion |

| Growth Rate (2026 - 2031) | 31.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Internet Of Things In Banking Market Analysis by Mordor Intelligence

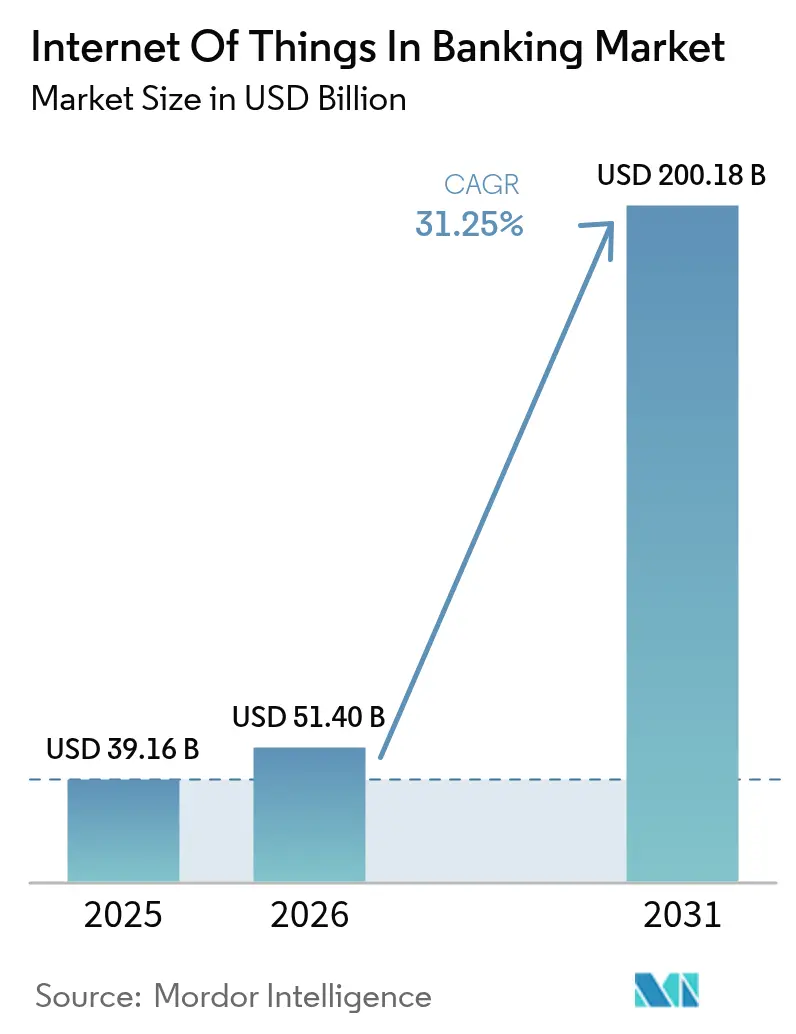

The Internet Of Things In Banking Market size was valued at USD 39.16 billion in 2025 and estimated to grow from USD 51.4 billion in 2026 to reach USD 200.18 billion by 2031, at a CAGR of 31.25% during the forecast period (2026-2031).

The growth pace mirrors banks’ shift toward sensor-rich operating models, real-time data flows, and embedded payments that link financial services to daily device usage. Institutions are layering connected sensors on ATMs, branches, and mobile endpoints to streamline cash operations, trigger context-aware offers, and automate payments initiated from vehicles and smart appliances. A regulatory push, notably the Consumer Financial Protection Bureau’s open-banking rule, effective April 2026, is accelerating API readiness that enables third-party developers to integrate IoT signals with banking data. Parallel mandates in Europe under PSD3 and the proposed Payment Services Regulation expand strong-authentication requirements and create secure rails for IoT-enabled transactions.[1]Payments Practice, “PSD3 and PSR: what to expect,” ACI Worldwide, aciworldwide.com Banks that orchestrate these capabilities report 30-40% efficiency gains and 20-30% uplifts in product-recommendation hit rates when omnichannel IoT programs mature.[2]Editorial staff, “Omnichannel efficiency with IoT,” World Wide Technology, wwt.comSupply-chain constraints surrounding semiconductors and uneven 5G rollout still temper device deployments; however, falling sensor costs and edge-compute advances point to sustained expansion of the Internet of Things in the Banking market throughout the decade.

Key Report Takeaways

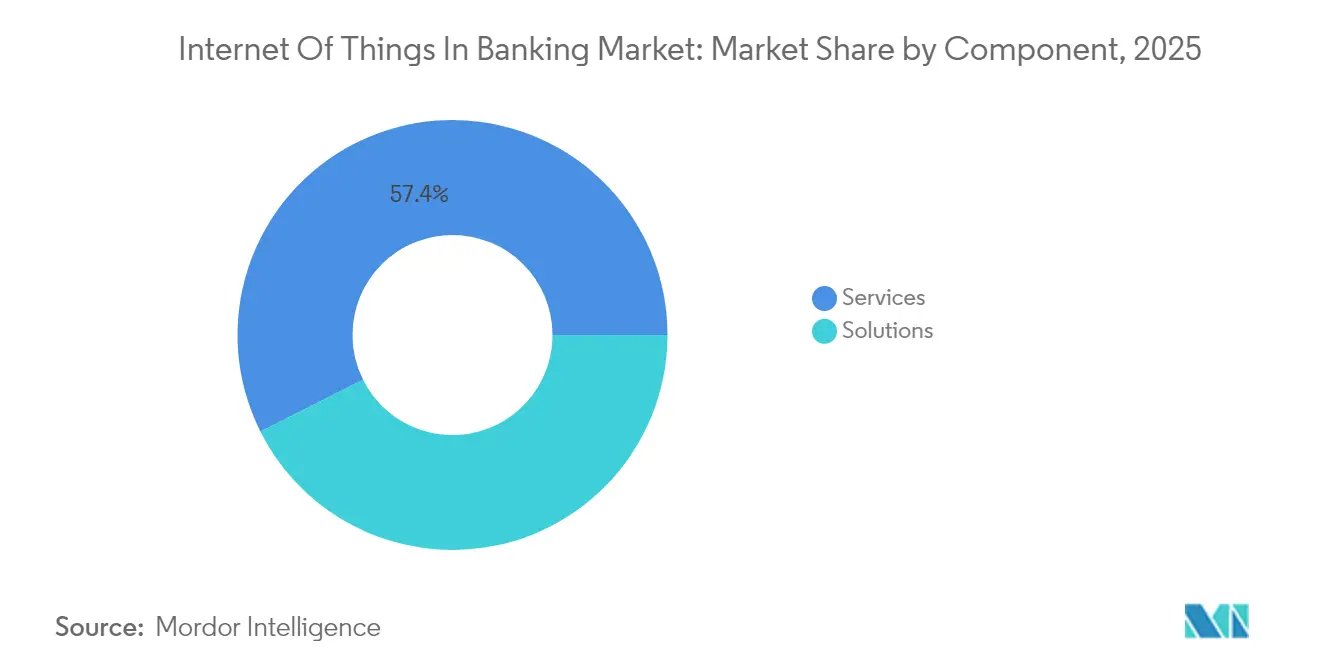

- By component, services commanded 57.40% of 2025 revenue, while solutions posted the fastest 32.60% CAGR outlook through 2031.

- By application, security led with 35.80% of the Internet of Things in the Banking market share in 2025 and is projected to grow at 33.80% CAGR to 2031.

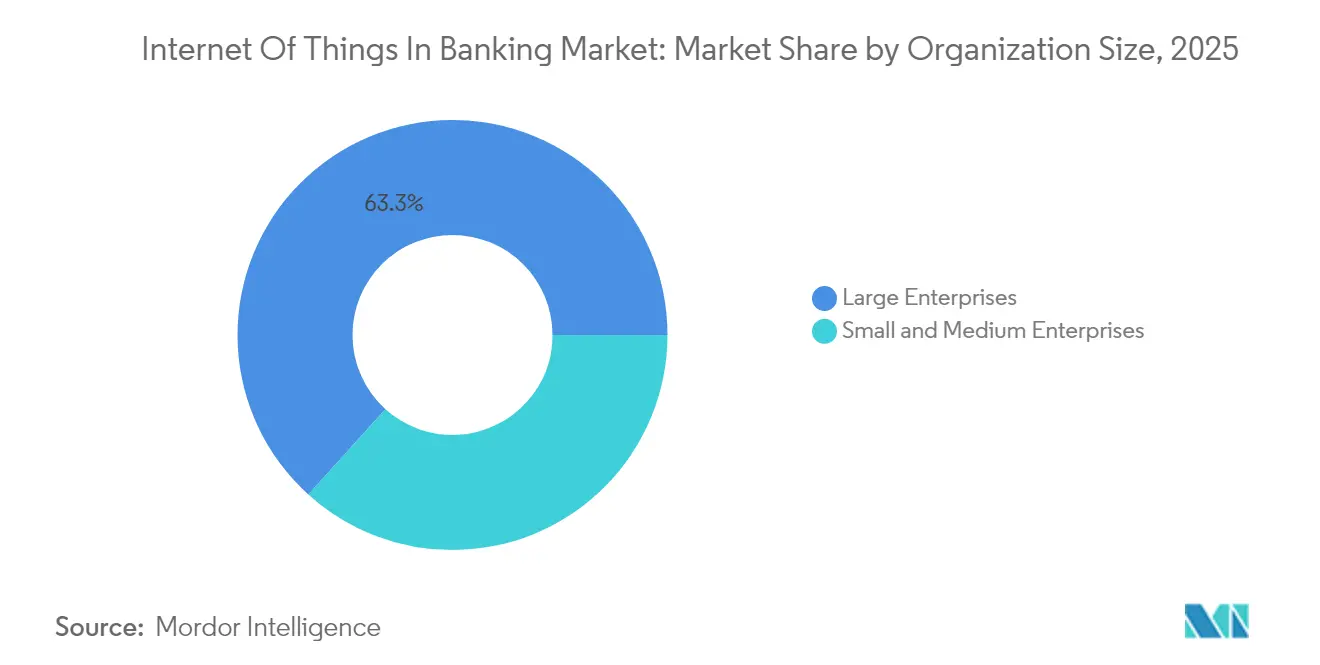

- By organization size, large enterprises held a 63.30% share in 2025, whereas SMEs are set to expand at a 32.45% CAGR during the same period.

- By end user, retail banking captured 42.10% revenue in 2025; insurance is the fastest-growing segment at 33.00% CAGR through 2031.

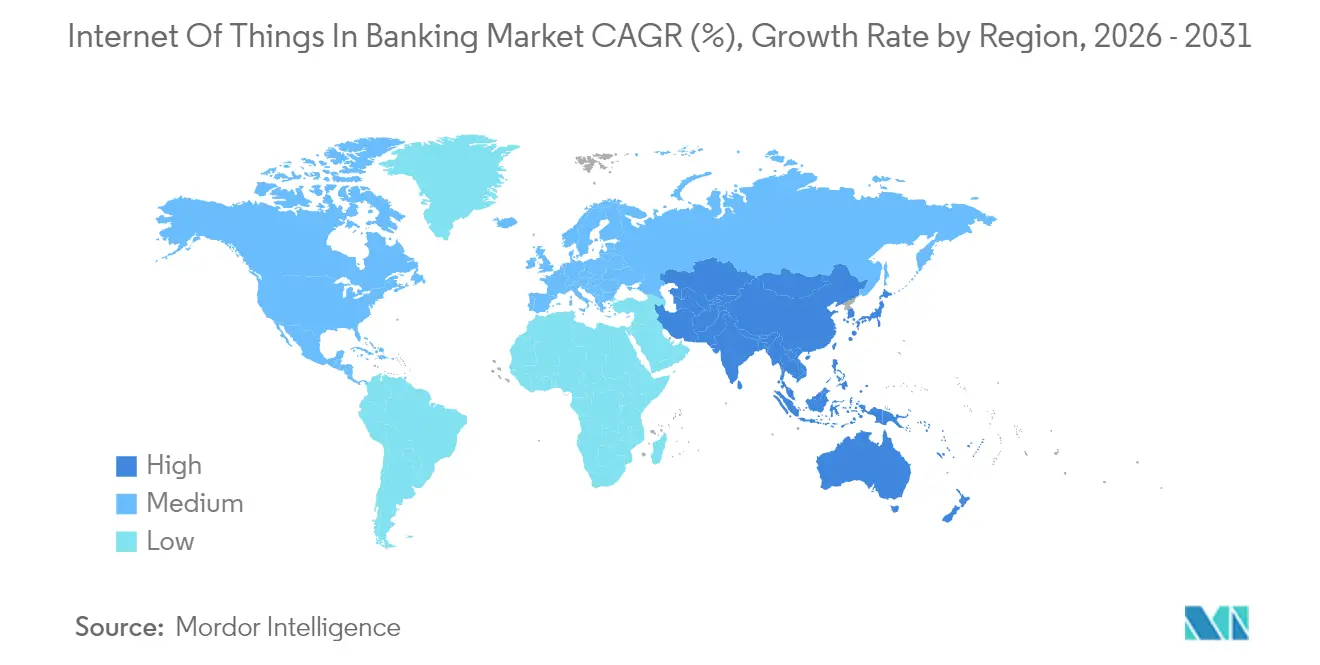

- By geography, North America retained 37.90% of 2025 revenue, but Asia-Pacific is forecast to advance at 32.70% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Internet Of Things In Banking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Omnichannel customer-experience push | +5.2% | Global; strongest in North America and EU | Medium term (2-4 years) |

| Real-time fraud detection and security | +6.8% | Global; critical in emerging APAC markets | Short term (≤ 2 years) |

| Regulatory open-banking mandates | +4.1% | North America and EU first; extending to APAC | Medium term (2-4 years) |

| Branch/ATM cost-optimization via sensors | +3.9% | Mature banking markets worldwide | Long term (≥ 4 years) |

| IoT-enabled embedded payments (cars and appliances) | +7.3% | North America and EU early; rapid APAC scaling | Long term (≥ 4 years) |

| Edge-analytics hyper-personalized microlending | +4.7% | APAC core; spill-over to Latin America and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Omnichannel Customer-Experience Push

Banks wire sensors into ATMs, mobile apps, and wearables to create journeys that pivot seamlessly across physical and digital environments. NatWest upgraded 5,500 ATMs with 19-inch touchscreens and live telemetry that flags downtime before it occurs. The bank also released a retail-banking app for Apple Vision Pro so clients can move funds using gaze and gesture. Such integrations let institutions blend geolocation, device health, and purchase patterns to anticipate needs, lifting cross-sell accuracy by one-third on mature rollouts. Sensor analytics enable pre-visit branch staffing, queue alerts, and dynamic personalized offers that raise customer satisfaction scores by double digits. The Internet of Things in Banking market, therefore, benefits from higher user stickiness and reduced operating costs.

Real-Time Fraud Detection and Security

Distributed sensors feed anomaly engines that flag suspicious patterns in milliseconds. A federated-learning model combining device telemetry with transaction streams now achieves 96.3% fraud-detection accuracy while keeping data local for privacy. Smart cameras and environmental sensors guard ATMs and cash machines, detecting skimming devices or abnormal temperature spikes that hint at tampering. Blockchain hashes applied at the edge create immutable logs for dispute resolution, and on-device AI reduces false positives that once annoyed customers. Early adopters report fraud-loss reductions of more than 20% in the first implementation year. Security urgency propels continual investment, fortifying the Internet of Things in the Banking market against cybercrime-related hesitancy.

Regulatory Open-Banking Mandates

The CFPB requires banks above USD 850 million in assets to provide standardized, permissioned access to customer data by April 2026. This mandate creates rails on which IoT manufacturers can embed payments, such as vehicles paying for charging or fridges reordering groceries. Europe’s PSD3 draft rules likewise oblige dedicated interfaces and strong customer authentication. Banks see compliance not as overhead but as a springboard to new fee streams through licensed IoT ecosystems. Standard APIs trim integration timelines by half, boosting ROI for pilot projects and sustaining growth in the Internet of Things in Banking market.

IoT-Enabled Embedded Payments (Cars and Appliances)

Visa and BMW have piloted connected-car wallets that settle fuel, tolls, and maintenance without driver input.[3]Editorial staff, “Connected car payments,” Cognizant, cognizant.com Smart homes now reorder detergent as soon as sensors record low levels, with payments cleared on background rails. Machine-to-machine transactions scale via 5G slices that guarantee latency below 10 milliseconds, supporting 75 billion devices forecast to be online in 2025. Usage-based insurance leverages telemetry to adjust premiums daily, and pay-per-use loans for appliances align repayments with actual utilization. These models reinforce customer loyalty and diversify revenue, lifting the Internet of Things in Banking market trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and cybersecurity concerns | –4.3% | Global; stricter enforcement in EU and California | Short term (≤ 2 years) |

| Device/platform interoperability gaps | –3.1% | Global; pronounced in fragmented APAC markets | Medium term (2-4 years) |

| Rural 5G latency bottlenecks | –2.8% | Rural areas worldwide; acute in developing markets | Long term (≥ 4 years) |

| ESG scrutiny on IoT energy consumption | –1.9% | EU and North America first; spreading globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cybersecurity Concerns

The EU Cyber Resilience Act obliges manufacturers to ship devices with automatic security updates, exposing vendors that cannot maintain over-the-air patching. Banks must track diverging rules from California’s Consumer Privacy Act to India’s Digital Personal Data Protection law, adding compliance overhead. Breaches at a single sensor can undermine banking cores if segmentation is weak. Federated-learning pilots show 99.94% model accuracy without exporting raw data, but most lenders still face skills gaps in securing device fleets.[4]Y. Zhou et al., “Privacy-preserving IoT models for banking,” MDPI Sensors, mdpi.com Rising insurance premiums for cyber coverage inflate project costs and can slow adoption within the Internet of Things in Banking market.

Device / Platform Interoperability Gaps

IoT uses dozens of protocols, from MQTT to Zigbee, that rarely interoperate natively. Nacha’s Afinis group is building common APIs for payment endpoints, yet many devices rely on proprietary formats. Banks wanting a pan-vendor network often insert middleware that adds latency and cost. Integration delays have reached nine months on multi-vendor pilots, prompting some institutions to restrict scope to single-supplier ecosystems. In emerging Asia, local manufacturers’ custom stacks deepen fragmentation, limiting the addressable slice of the Internet of Things in the Banking market until standardization crystallizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Drive Implementation Success

Services hold 57.40% of 2025 revenue, underscoring that domain expertise, regulatory insight, and 24-hour support tilt outcomes in complex rollouts. The Internet of Things in Banking market size for services is projected to expand at 30.40% CAGR, reflecting demand for integrators who stitch sensors into legacy cores and cloud fabrics. Banks often outsource threat modeling, compliance mapping, and device-life-cycle governance to reduce risk. Solutions cover hardware kits, software platforms, and connectivity bundles, and they benefit from cloud-native shifts that let lenders retire on-premises data centers. Joint offers, such as IBM-Wipro’s AI-enabled platform, bundle analytics and cyber hardening, amplifying competition among solution providers.

Second-generation deployments favor pay-as-you-grow managed services, pushing smaller banks to embrace turnkey bundles rather than capex-heavy in-house builds. Vendors are packaging edge-compute nodes with pre-certified connectors for open-banking APIs, trimming time to value. Hardware margins remain thin, so suppliers pivot to annuity models around device monitoring and predictive maintenance. As cloud vendors release financial-grade edge stacks, the Internet of Things in Banking market further tilts toward service-centric economics.

By Application: Security Leads Amid Rising Threats

Security applications captured 35.80% of 2025 revenue and expand at 33.80% CAGR, riding regulatory imperatives and growing attack vectors. The Internet of Things in Banking market size for security reached USD 18.76 billion in 2026 and is forecast to exceed USD 80.29 billion by 2031. Smart ATMs detect temperature anomalies, shock events, or tampering patterns and can lock dispensers automatically. Device-level encryption and root-of-trust chips now ship by default in premium terminals, reducing compliance audit time.

Monitoring, data management, and customer experience modules share infrastructure but vary in analytics heft. Banks leverage telemetry to optimize branch energy use, cutting power costs by up to 12% year over year. Customer-experience engines marry foot-traffic sensors with CRM histories to trigger in-branch personalized greetings. Integrated platforms that host multiple applications on the same sensor grid help reduce overall TCO, broadening appeal across the Internet of Things in the Banking market.

By Organization Size: SMEs Accelerate Adoption

Large institutions own 63.30% of current spending thanks to resources for multi-year programs, yet SMEs post the liveliest 32.45% CAGR. Subscription-based edge gateways and serverless analytic stacks let community banks bypass heavy lift. The Internet of Things in Banking market share held by SMEs is expected to breach 41.00% by 2031 as turnkey offerings close capability gaps. Smaller lenders prioritize branch automation and real-time alerts for cash-handling compliance, yielding tangible ROI within months.

Global tier-ones are experimenting with quantum-safe encryption and AI copilots that parse sensor data to advise frontline staff. They also pilot micro-branch formats featuring video kiosks and robot cash recyclers to cut real-estate costs. These innovations seed best practices that filter down to mid-tier banks once costs rationalize, nurturing inclusive growth across the Internet of Things in the Banking industry.

By End User: Insurance Emerges as Growth Leader

Retail banking continues to dominate with 42.10% of 2025 revenue, powered by consumer-facing ATMs, mobile wallets, and smart-home finance links. Yet insurance logs the quickest 33.00% CAGR as underwriters mine telemetry from cars, homes, and wearables to craft usage-based policies. The Internet of Things in Banking market size for insurance applications is projected to rise from USD 8.25 billion in 2026 to USD 34.35 billion in 2031. Corporate banking leans on IoT in trade-finance corridors where sensors verify shipment integrity and trigger automatic bill-of-lading payments.

Investment banks test smart-trading floors whose occupancy sensors regulate HVAC and lighting, paring energy bills while feeding ESG dashboards. Non-banking finance firms integrate IoT into peer-to-peer lending models, validating collateral conditions in real time. Cross-industry convergence blurs classical boundaries, underpinning diversified revenue streams within the Internet of Things in the Banking market.

Geography Analysis

North America retains leadership with 37.90% of 2025 revenue, buoyed by solid cyber legislation and early fintech-bank partnerships. Sensor-enabled branches post 30-40% productivity uplifts, and quantum-trial algorithms run 1,000 times faster than legacy optimizers. Canada advances cash-circle inclusion through connected community ATMs, while Mexico leverages IoT-based remittance kiosks that cut transaction fees. The Internet of Things in Banking market sees federal support for 5G expansion into underserved zones, flattening latency disparities across the continent.

Asia-Pacific is the growth engine, charging ahead at 32.70% CAGR. China’s AIBank serves more than 100 million customers on microservices cores that ingest IoT data to personalize lending. India deploys edge mini-data centers to extend mobile banking into rural districts where fiber remains sparse. Southeast Asian super-apps fuse ride-hailing, food delivery, and instant credit, with IoT sensors tracking driver performance for dynamic insurance pricing. Regional regulators fast-track sandbox approvals, ensuring the Internet of Things in Banking market captures rising smartphone penetration.

Europe predicates progress on privacy and ESG. PSD3 and the pending PSR impose mandatory authentication and harmonized APIs, fostering secure device onboarding. Institutions integrate energy-monitoring sensors to gauge carbon footprints, aligning with commitments to net-zero roadmaps. Device makers embed power-thrifty chips, addressing scrutiny over IoT electricity draw. In emerging regions of Latin America and the Middle East and Africa, payments modernization programs and mobile-money regimes create fertile ground for leapfrogging deployments. For instance, Brazil’s PIX and Nigeria’s eNaira rails allow IoT endpoints to initiate real-time payments, diversifying revenue sources within the Internet of Things in Banking market.

Regulatory Landscape

IoT deployments in banking are increasingly shaped by operational-resilience and data-access requirements that bring connected endpoints (ATMs, branch sensors, wearables, and embedded-payment devices) into regulated ICT scope. In the European Union, the Digital Operational Resilience Act (DORA, Regulation (EU) 2022/2554) has applied since 17 January 2025, requiring financial entities and critical third-party ICT providers to implement ICT risk management, incident reporting, resilience testing, and third-party oversight across digital supply chains that include IoT device fleets and edge platforms.

Supervisory expectations are further elaborated through technical standards and guidance, including Commission Delegated Regulation (EU) 2024/1774 on ICT risk management tools, methods, and policies, and the EBA Guidelines EBA/GL/2025/02 (applicable from 20 May 2025) aligning ICT and security risk expectations across institutions. For device-level security and privacy controls, banks and vendors cite IoT baselines such as ISO/IEC 27402:2023, while supervisors incorporate DORA-aligned ICT risk assessments into ongoing reviews. This affects governance and documentation, and it influences vendor selection for IoT-enabled banking programs.

Value Chain Analysis

The IoT in banking value chain covers device and sensor providers (ATM telemetry modules, cameras, environmental sensors, NFC wearables), connectivity and network operators (including 4G/5G and private networks), and edge gateways and device-management platforms (fleet provisioning, OTA updates, certificate and key management). From there, data streaming and integration layers connect to application stacks that deliver security, monitoring, data management, and customer experience management. Systems integrators and managed service providers span these layers to link IoT telemetry with core banking, fraud and AML systems, and open-banking APIs, while cloud and security vendors support compliance-grade infrastructure, encryption, and observability for uptime and audit expectations.

Downstream, banks convert IoT signals into automated workflows such as predictive maintenance for self-service channels, context-aware engagement, and machine-triggered payments routed across payment rails. Interoperability standards and industry groups, such as payment-endpoint API work, shape integration costs and time-to-value. At the regulatory level, EU DORA (effective January 2025) reinforces due diligence and continuous controls monitoring across third-party technology providers. Recent ecosystem activity also points to consolidation and new edge form factors, including CSI acquiring Qolo (July 2026) to strengthen embedded finance and orchestration capabilities, and Inter&Co launching NFC wearables in the United States (July 2026) to extend banking access beyond the phone to connected payment endpoints.

Competitive Landscape

The Internet of Things in Banking market is moderately fragmented, with cloud hyperscalers, financial-software incumbents, device makers, and pure-play IoT platforms contesting influence. IBM, Microsoft, and Oracle leverage expansive cloud zones and regulatory accreditations to win multi-country deals. Specialized suppliers such as NCR Atleos focus on smart-ATM fleets, while Diebold Nixdorf concentrates on cash recyclers equipped with predictive-maintenance AI. Partnerships trump zero-sum rivalry: IBM pairs with Wipro to blend systems integration and AI accelerators, and Temenos links SaaS core banking with Taurus to safeguard digital assets.

Patent-tracking services show spikes in filings around biometric gating, proximity payments, and distributed edge orchestration. Vendors collaborate with telcos to guarantee 5G quality-of-service slices for latency-critical financial events. White-space opportunities persist in agricultural lending, where IoT crop sensors inform weather-indexed payouts, and in cross-border SME corridors lacking resilient device coverage. Vendor differentiation hinges on compliance toolkits and pre-certified API stacks that hasten time to revenue for banks entering the Internet of Things in the Banking industry.

Pricing models tilt toward outcome-based fees tied to fraud-loss reduction or service-availability metrics. As device volumes climb, suppliers bundle lifecycle management with carbon-tracking dashboards to answer ESG audits. Alliance ecosystems encompassing chipset designers, security-certificate authorities, and managed-connectivity operators underpin holistic offerings. Customer surveys indicate that banks favor vendors able to furnish multiyear roadmaps with clear regulatory audit support, shaping procurement cycles across the Internet of Things in Banking market.

Internet Of Things In Banking Industry Leaders

IBM Corporation

Infosys Limited

Accenture PLC

Cisco Systems, Inc.

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity is scaling multi-vendor ATM and branch device modernization through standardized interfaces, which can reduce protocol fragmentation and integration delays that have limited larger deployments. The XFS4IoT specification preview released by CEN-CENELEC (May 2026) offers a concrete path away from legacy XFS 3.x approaches toward web/API-driven self-service device control, supporting banks and ATM operators that run heterogeneous fleets and want faster rollout cycles for telemetry, security controls, and new user experiences.

A second opportunity is operationalizing device-triggered payments and embedded finance with stronger governance, where IoT shifts from passive monitoring to transaction initiation that must be auditable end-to-end. Market signals include implementation of the National Financial Regulatory Administration guideline JR/T 0338-2025 in China (May 2025) for financial applications of IoT technology, alongside bank programs connecting IoT signals to modern rails, including Visa and BMW piloting connected-car wallets for payments. Together, these developments create whitespace for orchestration layers that unify consent, authentication, routing, and dispute evidence across device types (vehicles, appliances, wearables, ATMs) and across end users such as retail banking and insurance, where telemetry-driven pricing and underwriting depend on secure ingestion and policy-compliant data use.

Recent Industry Developments

- July 2026: Inter&Co launched Inter Ring and Inter Wristband in the United States, using passive NFC for contactless payments linked to credit card accounts. The launch extends banking interactions to wearable endpoints and reinforces the shift toward device-initiated commerce that banks must support with tokenization, risk controls, and lifecycle management across new form factors.

- June 2026: Bank of China expanded its relationship with IBM to establish a new innovation model leveraging IBM Garage, focusing on modernization with AI, blockchain, and IoT-related technologies. The expanded engagement highlights how large banks are bundling connected-channel telemetry with modern data and automation stacks to shorten deployment cycles and improve observability across digital services.

- March 2026: IBM completed the acquisition of Confluent, adding a data streaming platform that strengthens real-time data ingestion and event processing for enterprise clients, including financial services. Streaming infrastructure supports higher-frequency IoT telemetry and faster anomaly detection, improving how banks operationalize sensor signals for security monitoring, uptime management, and contextual customer journeys.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenue generated from IoT solutions and related services that banks use to connect devices, collect data, and run banking use cases such as branch and ATM monitoring, security, and customer experience improvement.

Scope exclusions: We exclude general IT outsourcing that is not tied to IoT deployments, and we also exclude pure telecom connectivity revenue when it is sold as a standalone service.

Segmentation Overview

- By Component

- Solutions

- Services

- By Application

- Security

- Monitoring

- Data Management

- Customer Experience Management

- Other Applications

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By End User

- Retail Banking

- Corporate Banking

- Investment Banking

- Non-Banking Financial Companies

- Insurance

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping what IoT means in a banking environment, and then listing the revenue pools that can be counted in a repeatable way. We refer to public materials such as central bank and financial regulator publications, the World Bank Global Financial Development indicators, the International Telecommunication Union (ITU) connectivity statistics, and NIST cybersecurity guidance, since these help anchor adoption conditions and baseline terminology.

To turn context into sizing inputs, we also review sources such as FFIEC and similar supervisory guidance for technology controls, bank annual reports and investor decks, and reputable press coverage of connected ATM fleets, branch modernization, and fraud prevention initiatives. Where available, a paid subscription for company financials and news is used to validate supplier exposure and investment direction, and a patent database helps us sanity check innovation intensity around sensors, identity, and secure device management in BFSI. These examples are not exhaustive, and many other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs come from interviews and structured surveys with a mix of banking technology leaders, IoT solution owners, and service teams supporting deployments, so the adoption path and spending cadence are understood in operational terms. Since this is a global market, coverage is balanced across major regions, and feedback is used to close gaps on typical implementation scope, renewal patterns, and what gets counted as IoT versus adjacent digital programs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 15% | APAC: 44% |

| Mid tier: 59% | Functional/Unit leaders: 34% | EMEA: 30% |

| Smaller Players: 15% | Managers: 51% | Americas: 26% |

Market-Sizing & Forecasting

The sizing model is built by using a top-down approach first, where banking IoT spend is reconstructed from the broader IoT stack and then narrowed using adoption and use case intensity indicators specific to banks. The totals are then corroborated through selective bottom-up checks, such as sampling typical solution pricing, validating service attach rates, and rolling up a limited set of supplier revenue exposures to make sure the final number does not drift from real buying behavior.

Key inputs used in the model include the installed base and upgrade cycle of connected endpoints in banking environments (such as ATMs and monitored branch assets), the mix of security and monitoring use cases versus customer experience programs, cloud versus on-premise preference for sensitive workloads, and the expected services share needed for integration and ongoing device management. We also track region-level digital banking activity and compliance-driven security spending as practical demand signals that influence adoption timing.

For forecasting, scenario analysis is used so base, conservative, and accelerated adoption paths can be tested against what interviewees expect for rollout speed, refresh cycles, and budget approvals. When bottom-up data is incomplete, gaps are handled through ratio-based assumptions tied back to primary feedback, then checked against the nearest observable indicators before finalizing the series.

Data Validation & Update Cycle

Numbers are cross-checked using multiple passes so unusual jumps are identified early and corrected with clear rationale. Analysts compare outputs against independent signals such as endpoint growth trends, banking IT and security spending direction, and the expected split between solutions and services. Assumptions are then reviewed by another analyst before sign-off.

If a variance looks material, we re-check definitions, re-contact a few respondents, and re-run sensitivity tests on the inputs that drive the change. Reports are refreshed annually, and interim updates are made when major events materially change adoption, regulation, or technology costs. Before delivery, a final review is done so clients receive the latest updated view.

Mordor Intelligence's Banking Internet of Things Market Estimate Compared With Other Published Estimates

Published market sizes for IoT in banking can look far apart because the boundary line is not consistent across studies, and because the banking-only view is sometimes mixed with wider financial services. Differences also show up when one source counts hardware and connectivity heavily, and another focuses more on software and managed services revenue.

Endpoint and deployment signals, such as connected ATM and branch modernization activity plus the typical services attach rate shared in interviews, are the checks that keep Mordor Intelligence's estimate tied to banking-specific IoT programs rather than the full BFSI technology spend. Gaps also come from the time window used for currency conversion, how fast pricing is assumed to change for platforms and managed services, and whether the forecast is built from a base case or an aggressive adoption curve.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 39.16 B (2025) | |

| Global Consultancy A | USD 68.15 B (2024) | Uses a broader banking and financial services definition, and its component scope emphasizes the full IoT stack across BFSI, which can pull in non-bank spend and inflate the total versus a banking-only cut. |

| Industry Advisory B | USD 58.56 B (2024) | Applies a wider end-use mix that includes insurance and other financial services, and its base-year framing can embed higher early adoption assumptions that push the 2024 value up. |

Overall, the spread is mostly explained by what is counted as banking IoT versus wider BFSI, plus how base-year assumptions are set when adoption is still uneven across regions. By keeping the scope tied to bank use cases and checking the model against practical deployment and services signals, the result stays traceable to a few clear inputs that can be revisited as conditions change.

Key Questions Answered in the Report

What is the growth outlook for the Internet of Things in Banking market between 2026 and 2031?

The market is projected to rise from USD 51.4 billion in 2026 to USD 200.18 billion by 2031 at a 31.25% CAGR.

Which component segment holds the largest share today?

Services lead with 57.40% of 2025 revenue because banks rely on external expertise for integration, security, and compliance.

Why are security applications expanding fastest?

Rising cyber threats and strict regulations push banks to embed tamper detection, biometric access, and encrypted communications, fueling a 33.80% CAGR for security solutions.

How does open banking regulation influence IoT adoption?

Mandated APIs allow approved third parties to access banking data, enabling connected cars, appliances, and wearables to initiate secure payments automatically.

Which region delivers the strongest growth momentum?

Asia-Pacific posts a 32.70% CAGR as digital-only banks in China and India scale IoT-centric services across mobile-first populations.

What key challenge hampers large-scale IoT rollouts in banking?

Platform interoperability gaps force banks to juggle multiple protocols, extending project timelines and raising integration costs.

Page last updated on: