Engineering Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

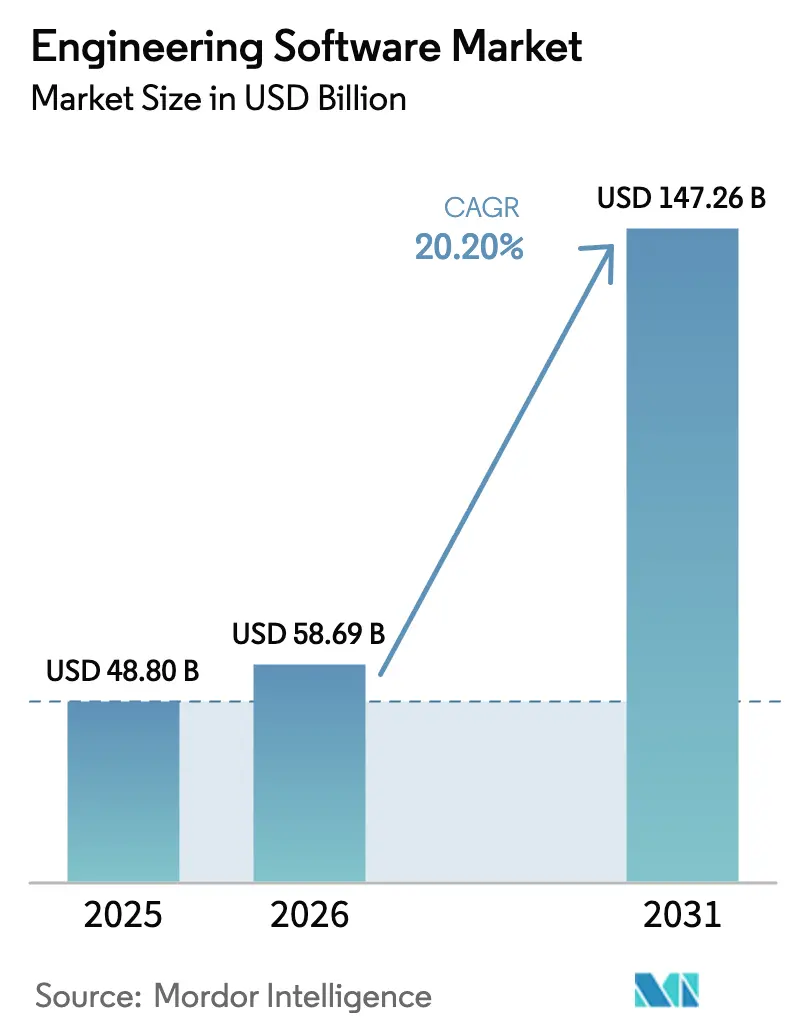

| Market Size (2026) | USD 58.69 Billion |

| Market Size (2031) | USD 147.26 Billion |

| Growth Rate (2026 - 2031) | 20.20% CAGR |

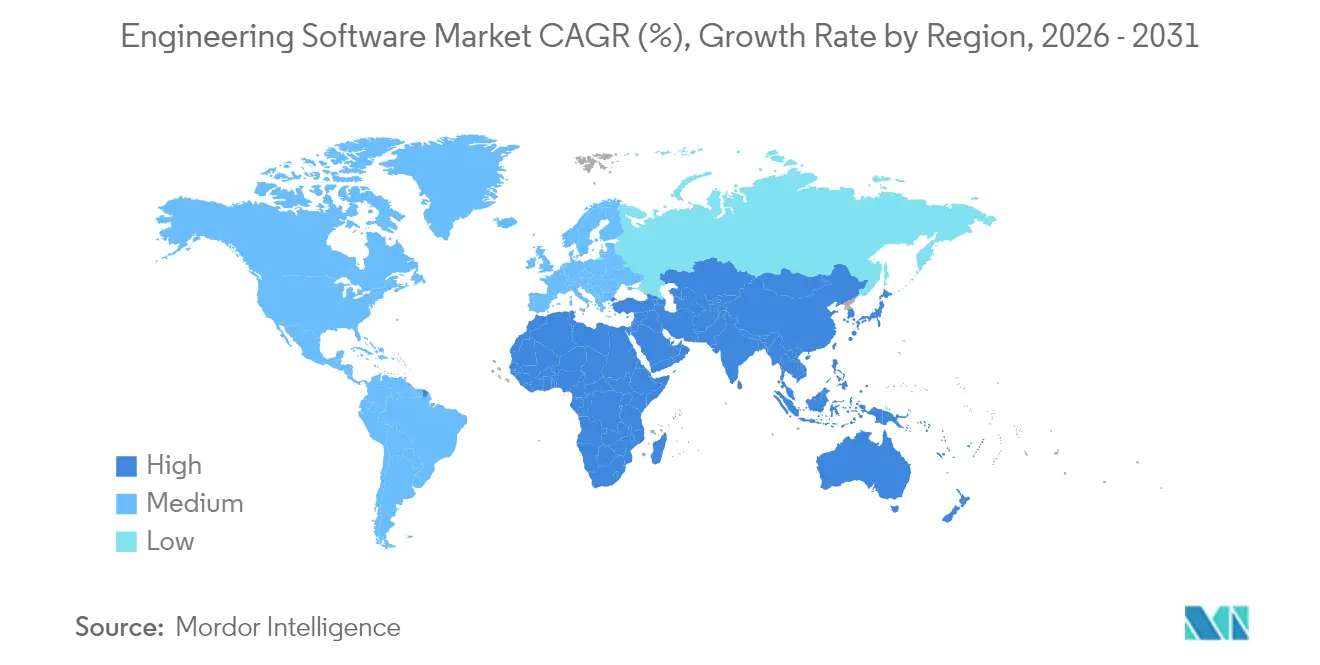

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Engineering Software Market Analysis by Mordor Intelligence

Engineering software market size in 2026 is estimated at USD 58.7 billion, growing from 2025 value of USD 48.8 billion with 2031 projections showing USD 147.3 billion, growing at 20.2% CAGR over 2026-2031. Intensifying generative-AI integration slashes iteration cycles from hours to seconds while preserving 90% validation accuracy, easing the talent crunch that will leave India short by up to 1.9 million engineers by 2026. Cloud deployment is widening access for small and medium enterprises, and the 37% jump in 2024 industrial-software M&A reveals vendors racing to assemble end-to-end digital-twin stacks. Regional momentum comes from North America’s aerospace and automotive digital-twin uptake, China’s double-digit software revenue growth, and EU sustainability mandates that embed life-cycle assessment in every design decision. Competitive dynamics feature heavyweight suites from Autodesk, Dassault Systèmes and Siemens pitched against AI-native upstarts and cloud-first specialists.

Key Report Takeaways

- By deployment, cloud-based solutions grew at 18.8% and now account for 45.70% of the engineering software market size, while on-premise still holds a 54.30% share in 2025.

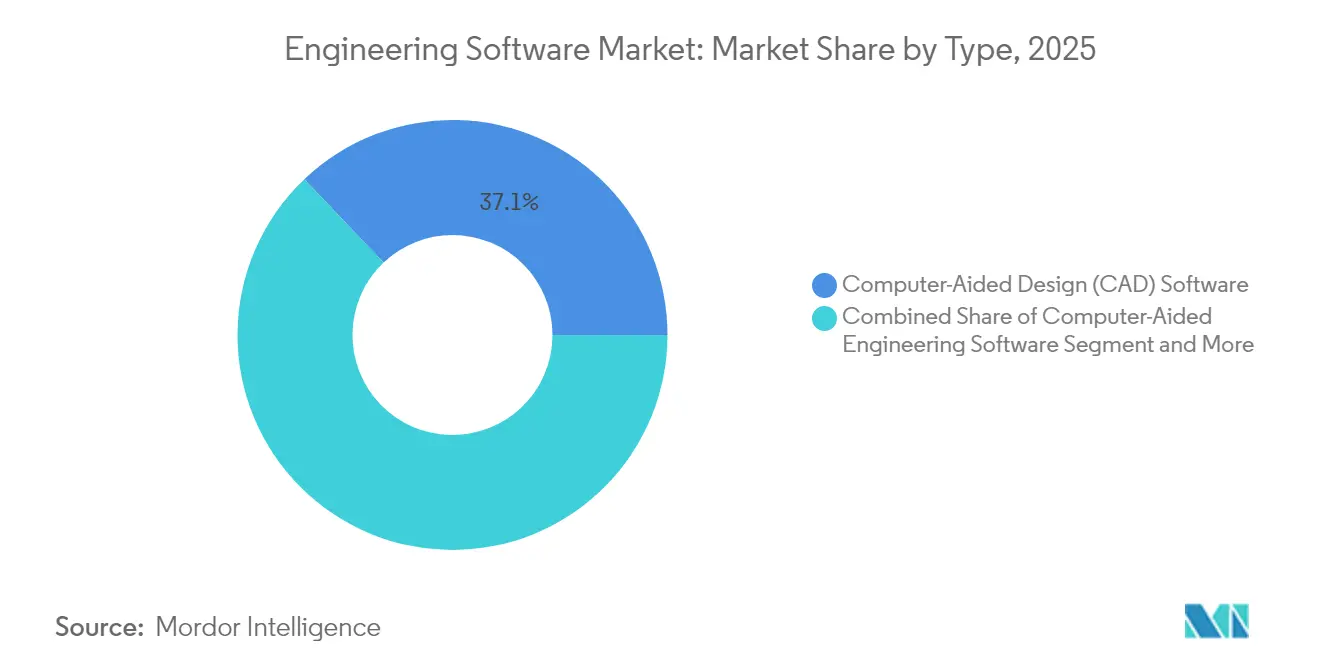

- By product type, CAD software commanded 37.10% engineering software market share in 2025; CAE tools are set to expand at a 13.3% CAGR through 2031.

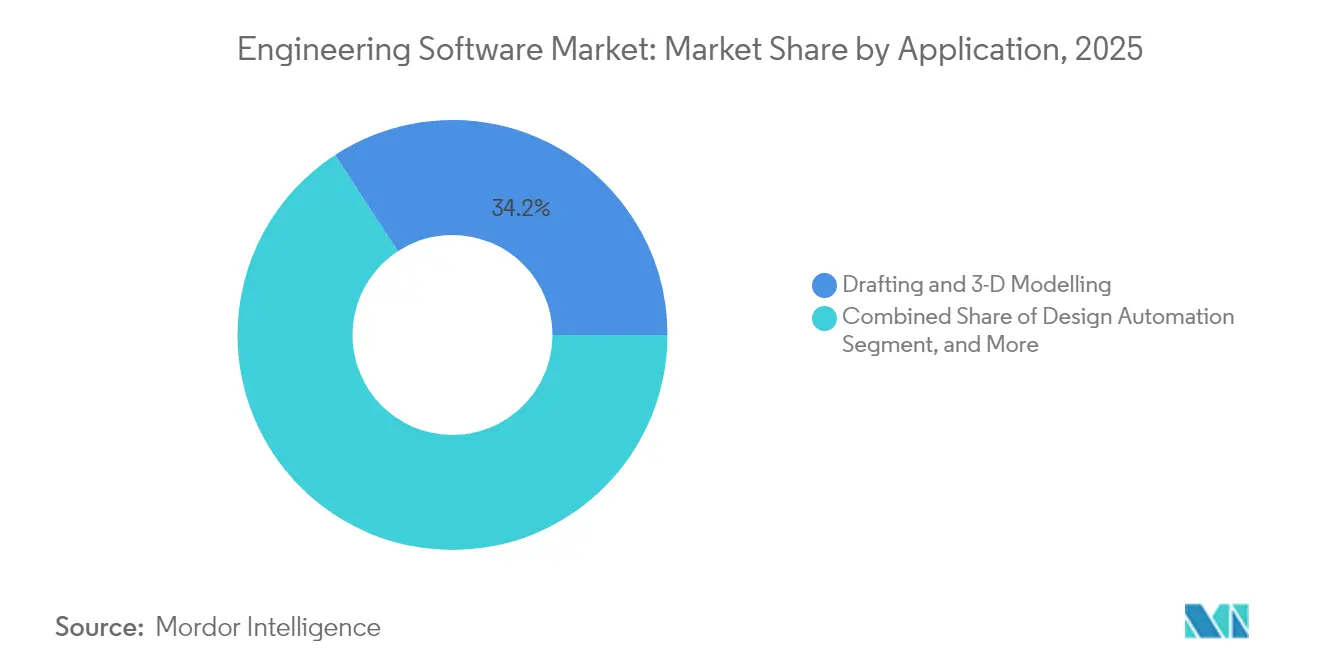

- By application, drafting and 3-D modelling captured 34.20% of the engineering software market size in 2025, whereas digital twin and simulation led growth at 14.0% CAGR.

- By end-user, automotive and transportation held 27.90% revenue share in 2025, but healthcare and medical devices is growing at 13.5% CAGR to 2031.

- Regionally, North America led with 32.10% engineering software market share in 2025 while APAC is advancing at 14.8% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Engineering Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-based deployment becomes default | +3.2% | Global, early North America and EU | Medium term (2-4 years) |

| Rising CAD and 3-D use among SMEs | +2.8% | APAC core, spill-over to LatAm and MEA | Long term (≥ 4 years) |

| Simulation-driven digital-twin workflows | +4.1% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Subscription SaaS pricing widens adoption | +2.5% | Global | Short term (≤ 2 years) |

| Generative-AI design automation | +3.7% | North America and EU initially, rapid APAC rise | Short term (≤ 2 years) |

| Mandatory sustainability LCA integration | +1.9% | EU and APAC chiefly, North America spill-over | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-based deployment becomes default licensing model

Enterprises are shifting budget from servers to subscriptions as Siemens’ cloud-native Designcenter and Autodesk’s Token Flex show how continuous updates and global collaboration offset capital budgets. Two-thirds of manufacturers are already reskilling staff for these platforms, yet multi-tenant architectures raise IP-security questions, spurring hybrid models that keep sensitive work on-premise while outsourcing compute spikes to the cloud. Vendors that deliver zero-trust encryption and sovereign-cloud options will capture the hesitant segments of the engineering software market.

Growing adoption of CAD and 3-D modelling across SMEs

Affordable SaaS tiers are opening the engineering software market to millions of small firms: Kenyan case studies show productivity jumps once manual drafting is replaced with digital files. Yet OECD data confirm that financial and skills gaps still obstruct uptake, highlighting a need for low-code design wizards and built-in training. Where vendors wrap onboarding, templates, and partner ecosystems into the license, they compress time-to-value and expand the engineering software market faster in price-sensitive economies.

Simulation-driven digital-twin engineering workflows

Aerospace programs now match physical and virtual twins with 99.99% fidelity, trimming inspection by 45% and lifting first-time-right builds by 60%. Healthcare twins deliver patient-specific treatment vectors, and additive-manufacturing twins help factories model spare-parts logistics. The cadence of real-world data into design means simulation modules must sit natively inside CAD suites, anchoring a rich seam of recurring revenue inside the engineering software market.

Subscription–SaaS price model expands addressable base

PTC’s move to subscriptions lifted ARR to USD 1.27 billion and grew recurring revenue 26%, validating pay-as-you-go licences that flex with project peaks. ANSYS’ Elastic Licensing bills hourly compute, letting startups spin up high-end solvers without cap-ex. As long-term total cost often exceeds perpetual models, vendors must prove a pipeline of features and cloud optimizations that justify renewal, a cornerstone in stabilizing the engineering software market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High licence & training costs | -2.1% | Global, acute for SMEs in emerging markets | Short term (≤ 2 years) |

| Shortage of specialised CAE/CAD talent | -1.8% | Global, most acute North America & EU | Long term (≥ 4 years) |

| IP-security concerns on cloud | -1.3% | Global, strong in defense & aerospace | Medium term (2-4 years) |

| Interoperability gaps across AI-native tools | -0.9% | Global, rising as AI adoption accelerates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High upfront licence and training costs for advanced suites

Enterprise-class simulation bundles from ANSYS push beyond USD 2.8 billion in annual sales, reflecting price points that few SMEs can absorb without staggered ROI. Training magnifies the hurdle because 65% of manufacturers are reskilling for new tools, inflating onboarding budgets. Although subscriptions spread expense, all-in ownership sometimes outstrips legacy perpetual licences, slowing the engineering software market in cost-sensitive regions.

Global shortage of specialised CAE/CAD talent

India alone needs up to 1.9 million extra engineers by 2026, while the US construction lists 382,000 monthly vacancies, illustrating a global supply lag. Without seasoned users, sophisticated suites lie underutilized, capping productivity gains. Automation raises baseline efficiency but cannot fully substitute domain insight, throttling the engineering software market where education pipelines trail demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: CAD Software Remains the Anchor While CAE Surges

The engineering software market size reached USD 18.11 billion for CAD tools in 2025, equal to 37.10% of total revenue, underscoring their role as the industry’s baseline workspace. Continuous usage-based upgrades keep these tools sticky across architecture, mechanical, and industrial design teams. Generative-AI sketching accelerates concept formation, yet downstream manufacturability remains contingent on precise parametric CAD, preserving its primacy in workflows.

Computer-Aided Engineering solutions are scaling at 13.3% CAGR to 2031 on the back of AI-powered solvers that slash compute time by blending physics-based simulation with surrogate models. As multidisciplinary optimisation embeds inside broader platforms, CAE’s share of the engineering software market revenue is projected to close the gap with CAD. CAM, PLM, and EDA suites provide essential continuity into production, yet their growth rates trail the flagship CAD and CAE categories because many customers already license basic modules and add incremental seats only as programmes scale.

By Deployment: Hybrid Models Bridge Security and Collaboration

On-premise installations still hold 54.30% engineering software market share as of 2025, supported by entrenched infrastructure in defence, heavy machinery, and aerospace firms guarding classified IP. Local compute clusters also ensure deterministic performance for dense, multi-physics simulations that can swamp bandwidth-limited locations.

Cloud deployments are expanding at 18.8% CAGR because subscription billing, instant scaling, and browser access appeal to SMEs and globally distributed teams. The engineering software market size for cloud seats is forecast to surpass USD 92.4 billion by 2031 as compliance-ready sovereign clouds and confidential computing mature. Hybrid architecture is becoming the default: design vaults reside on-premise while burst capacity routes to encrypted cloud nodes, satisfying IT policy without forfeiting elasticity. Vendors that provide transparent license roaming between environments will temper churn risk and capture longer lifetime value.

By Application: Digital Twins Shift Verification From Late-Stage to Continuous

Drafting and 3-D modelling delivered 34.20% revenue in 2025, yet their growth is plateauing as these capabilities saturate design functions. Value now concentrates on integrated simulation workflows where digital twins compare live sensor data with virtual models to predict field performance.

Digital twin and simulation platforms are advancing at a 14.0% CAGR, widening the engineering software market size for predictive analytics modules. As-built data syncs back into design intent, shrinking warranty costs and feeding circular-economy objectives. Design automation and plant-process modelling address sector-specific needs—process chemical plants, energy grids, or smart buildings—but the lines blur once unified data models underpin all assets in a single environment. Enterprises demanding closed-loop verification will prioritise vendors excelling in twin fidelity, real-time data ingestion, and cross-disciplinary interoperability.

By End-user Industry: Healthcare Climbs the Adoption Curve

Automotive and transportation cornered 27.90% of the engineering software market share in 2025, reflecting decades of embedded CAD and CAE practice. Electric-vehicle chassis, ADAS electronics, and lightweight composites keep seat counts high, yet growth moderates as tools already blanket most OEM tiers.

The healthcare and medical devices segment is scaling at 13.5% CAGR as FDA’s AI-SaMD guidelines clear pathways for software-based diagnostics that rely on heart-flow and organ-replica twins. Digital twins reduce clinical trial loops, pushing the engineering software market into regulated clinical workflows once viewed as outside core engineering. Aerospace and defence sustains premium licence density because programmes demand certified traceability and ITAR-aligned hosting. Construction and infrastructure depends on BIM coordination: studies show up to 40% clash reduction when 5-D BIM permeates contractors. Semiconductor, energy, and heavy equipment verticals likewise intensify simulation spending as component complexity and decarbonisation targets expand modelling scope.

Geography Analysis

North America generated 32.10% of the engineering software market revenue in 2025, buoyed by aerospace and automotive pioneers that embed twins across the product lifecycle and factory operations. The region’s policy leadership in AI-enabled medical devices creates spill-over demand from healthcare OEMs, while Canada’s clean-electricity roadmap triggers demand for renewable-energy design suites. Venture investment continues to seed AI-native startups, intensifying competition.

APAC records the fastest cadence at 14.8% CAGR, with China’s software revenue topping 98,281 billion yuan in the first nine months of 2024 and local champions increasing R&D budgets to close feature gaps with Western majors. India’s engineer shortfall stimulates demand for AI-assisted tools, while Japan and South Korea drive EDA innovation for advanced node semiconductors. As Southeast Asian governments court manufacturing shifts, SMEs there adopt cloud subscriptions, widening the engineering software market footprint. Europe maintains stringent sustainability laws that oblige every OEM to run embedded LCA before product release, converting compliance cost into software spend. Nordic harmonisation of building-lifecycle data amps BIM uptake, and German industrial exporters integrate digital twins for remote service optimisation. Data-sovereignty rules shape cautious cloud adoption, nudging vendors toward multi-tenant instances within EU borders to safeguard IP.

Competitive Landscape

The engineering software market features a moderate concentration anchored by three platform leaders—Autodesk, Dassault Systèmes, and Siemens—whose combined installed base locks in training ecosystems and data gravity. Siemens’ USD 10 billion Altair acquisition in 2024 deepened AI simulation breadth while creating the industry’s most expansive PLM-to-shop-floor stack. Autodesk sustains brand reach through AutoCAD ubiquity and accelerates cloud migration via Forge microservices.

Competitive tension rises from AI-native players offering text-to-CAD generation or browser-only BIM, often at sub-USD 100 monthly tiers. These specialists address narrow pain points, such as generative massing studies or PCB co-design, then expand horizontally. Switching costs remain high: model histories, libraries, and macros entrench incumbents, but SaaS free tiers encourage experimentation, especially in emerging markets where software piracy historically eroded revenues. M&A tallied 86 deals in 2024, showing incumbents prefer acquisition over internal build to plug portfolio gaps.

Strategic themes include embedding LCA and ESG analytics, zero-trust cloud architectures and low-code configurators that democratise design among non-engineers. Significant white space persists in SME enablement where complex UIs still intimidate first-time buyers. Vendors that balance simplicity, compliance and AI-augmented productivity will expand their slice of the engineering software market ahead of peers tethered to legacy desktop models.

Engineering Software Industry Leaders

Autodesk Inc.

Siemens Digital Industries Software

Synopsys Inc.

Dassault Systèmes SE

Bentley Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Siemens unveiled Industrial Copilot for Operations and partnered with JetZero on blended-wing aircraft using the Xcelerator platform.

- December 2024: Maguar Capital financed the acquisition of hsbCad, strengthening off-site wood construction design tied to Autodesk Revit.

- October 2024: Tech Soft 3D bought Actify and Theorem Solutions to extend multi-CAD viewing and translation tools.

- September 2024: CAI Software acquired Parsable to knit CAD with factory execution for Tier-1 manufacturers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the engineering software market as revenue generated from commercially licensed packages, such as CAD, CAE, CAM, AEC/BIM, EDA, PLM, and niche geotechnical tools, used to design, simulate, manufacture, or manage physical products and infrastructure. These suites span on-premise, cloud, and hybrid deployments and are tracked globally by end-user industries that include automotive, aerospace, industrial machinery, construction, electronics, energy, and healthcare.

Scope exclusion: bespoke, in-house utilities developed by individual firms strictly for internal use are not counted within Mordor's revenue pool.

Segmentation Overview

- By Type

- Computer-Aided Design (CAD) Software

- Computer-Aided Engineering (CAE) Software

- Computer-Aided Manufacturing (CAM) Software

- Architecture, Engineering and Construction (AEC/BIM) Software

- Electronic Design Automation (EDA) Software

- Product Lifecycle Management (PLM) Software

- Geotechnical/Infrastructure Engineering Software

- By Deployment

- On-premise

- Cloud

- Hybrid

- By Application

- Design Automation

- Plant and Process Design

- Product Design, Testing and Digital Twin

- Drafting and 3-D Modelling

- Other Specialised Applications

- By End-user Industry

- Automotive and Transportation

- Aerospace and Defence

- Industrial Machinery and Heavy Equipment

- Construction and Infrastructure

- Electronics and Semiconductor

- Energy and Utilities

- Healthcare and Medical Devices

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed software channel partners, design-house leads, plant digitalization managers, and civil-engineering consultants across North America, Europe, and fast-growing Asian economies. These conversations tested adoption hurdles, license mix shifts, and region-specific price corridors, allowing us to fine-tune assumptions and stress-test early model outputs.

Desk Research

We began with foundational statistics from sources such as the US Bureau of Labor Statistics, Eurostat, and UN Comtrade to size engineering labor pools, trade flows of machine tools, and capital-goods investment trends. Technology adoption signals were drawn from IEEE Xplore and arXiv citation counts on digital twin, generative design, and high-performance computing, while open-access construction-permit datasets helped indicate AEC software demand in growth corridors. Financial disclosures accessed through D&B Hoovers and news archives on Dow Jones Factiva supplied vendor revenue splits and average selling prices that underpin our price ladders.

Further granularity came from trade associations, such as the Society of Automotive Engineers, SEMI, and the Construction Industry Institute, which publish downloadable benchmarking surveys on simulation hours, chip tape-outs, and BIM penetration. The desk sources listed here are illustrative; several other public and paid references were consulted to validate figures and clarify gray areas.

Market-Sizing & Forecasting

A single top-down build, anchored on global engineering R&D spend and fixed-asset formation, was reconstructed into addressable software outlay using historic penetration ratios and price bands, then selectively cross-checked with bottom-up roll-ups of vendor revenues and sampled ASP × seat volumes. Key model drivers include engineering employment headcount, CAD seat density per engineer, cloud migration rates, subscription renewal cycles, and industry capital-expenditure forecasts. Multivariate regression combined with scenario analysis projects these variables to 2030, while gaps in vendor disclosures are bridged by normalized gross-margin benchmarks gleaned from earnings calls.

Data Validation & Update Cycle

Outputs pass an automated anomaly screen, peer review by a second analyst, and a supervisory sign-off. Figures are refreshed yearly, with interim updates triggered by events like major pricing shifts or blockbuster mergers, ensuring clients receive a current, balanced viewpoint.

Why Mordor's Engineering Software Baseline Earns Investor Confidence

Published estimates often diverge because firms pick different software buckets, pricing logics, and refresh cadences. For example, Global Consultancy A pegs 2025 revenue at USD 49.9 billion, Industry Research House B cites USD 64.7 billion for the same year, and Regional Publication C lists USD 48.4 billion for 2024.

Key gap drivers include whether PLM maintenance fees are counted, how aggressively cloud discounting is modeled, and the point in the fiscal year each provider freezes currency conversions. Mordor's page reports USD 48.83 billion for 2025, aligning software categories with IFRS revenue recognition rules and using quarterly FX averages, which competitors may overlook.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 48.83 bn (2025) | Mordor Intelligence | - |

| USD 49.9 bn (2025) | Global Consultancy A | Excludes EDA maintenance; uses list prices without regional discount factors |

| USD 64.7 bn (2025) | Industry Research House B | Bundles bespoke in-house tools and multi-year services into software revenue |

| USD 48.4 bn (2024) | Regional Publication C | Applies 2022 FX rates and partial coverage of hybrid deployments |

In sum, by aligning scope strictly to licensable products, applying audited price corridors, and revisiting inputs every year, Mordor Intelligence delivers a transparent, repeatable baseline that decision-makers can rely on with confidence.

Key Questions Answered in the Report

What is the current engineering software market size and growth outlook?

The market stands at USD 58.7 billion in 2026 and is forecast to reach USD 147.3 billion by 2031, advancing at a 20.2% CAGR.

Which deployment model is growing fastest?

Cloud-based deployment is scaling at 18.8% CAGR, rising from 45.70% of installations today as subscription billing and elastic compute drive adoption.

Which industry segment will grow quickest to 2031?

Healthcare and medical devices lead with a 13.5% CAGR as digital-twin diagnostics and AI-enabled devices win regulatory clearance.

How are sustainability regulations influencing CAD purchasing?

EU and APAC mandates require embedded life-cycle assessment in design tools, pushing vendors to integrate LCA dashboards and fueling new licence demand.

What is the biggest restraint facing wider market expansion?

High licence plus training costs hamper SME adoption, especially in emerging markets where upfront budgets are tight and skilled operators scarce.

Who are the leading vendors in the space?

Siemens, Autodesk and Dassault Systèmes currently anchor the market through broad portfolios and recent AI-focused acquisitions, but they face increasing pressure from cloud-native and AI-specialist entrants.

Page last updated on: