Oil Filter Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.94 Billion |

| Market Size (2030) | USD 5.01 Billion |

| Growth Rate (2025 - 2030) | 4.94% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oil Filter Market Analysis by Mordor Intelligence

The Oil Filter Market size is estimated at USD 3.94 billion in 2025, and is expected to reach USD 5.01 billion by 2030, at a CAGR of 4.94% during the forecast period (2025-2030). Steady demand from commercial vehicles in emerging economies and the premium pricing power of synthetic media solutions balance the long-term volume drag from electric‐vehicle adoption. Accelerating infrastructure projects across Asia and Latin America keep hydraulic and transmission filter sales buoyant, while Euro 7 and comparable emission frameworks mandate higher-performance filtration that supports value growth. Producers focus on nanofiber and multilayer synthetic media to meet extended-service requirements, and digital channels continue to reshape aftermarket sales patterns. Supply-side consolidation is underway as leading vendors scale up R&D and recycling capabilities to defend margins against raw-material volatility and rising competitive intensity.

Key Report Takeaways

- By type, engine oil filters led with a 41.28% of the oil filter market share in 2024; hydraulic filters are projected to expand at a 4.95% CAGR through 2030.

- By sales channel, the aftermarket held 65.47% of the oil filter market share in 2024 and is advancing at a 5.03% CAGR between 2025 and 2030.

- By vehicle type, passenger vehicles accounted for 53.72% of the oil filter market share in 2024, while medium and heavy commercial vehicles are tracking the fastest growth at a 5.07% CAGR to 2030.

- By distribution channel, traditional retail captured 47.81% of the oil filter market share in 2024, while online retail and e-commerce channels are projected to post the quickest 4.97% CAGR through 2030

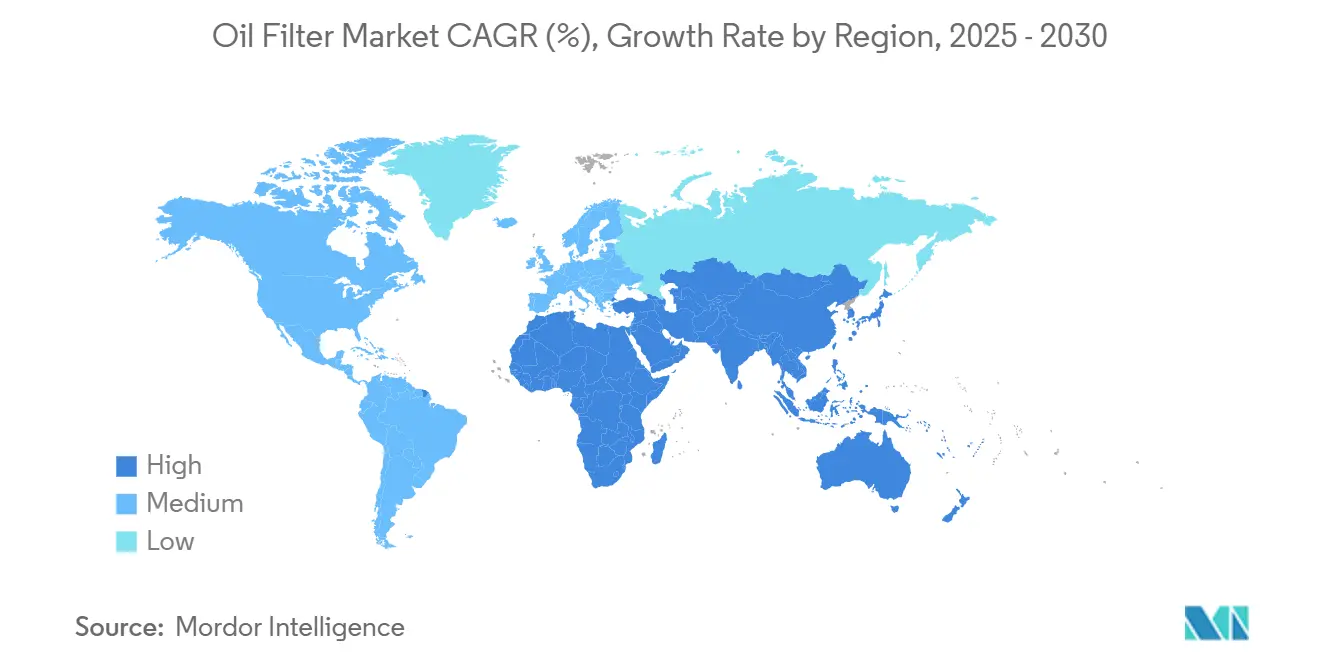

- By geography, Asia-Pacific commanded 38.93% of the oil filter market share in 2024 and is set to grow at a 4.99% CAGR, remaining the leading region through 2030.

Global Oil Filter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Vehicle-Parc Growth | +1.8% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Increasing OEM Adoption Of Extended-Life Synthetic Oil Filters | +1.2% | Global, with early gains in North America and EU | Long term (≥ 4 years) |

| Stringent Emission | +1.0% | Global, led by EU Euro 7 and US EPA standards | Short term (≤ 2 years) |

| Rising Aftermarket E-Commerce Penetration | +0.7% | North America and EU core, expanding to Asia Pacific | Medium term (2-4 years) |

| Thermal-Management Demand | +0.5% | Global, with concentration in developed markets | Medium term (2-4 years) |

| Circular-Economy Push Toward Recyclable Filter Housings & Media | +0.4% | Global, led by EU regulations and corporate sustainability | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Vehicle-Parc Growth in Emerging Asia

Sustained automotive production expansion in China and India underpins multi-year demand for original-equipment and replacement filters. India’s push to become an export manufacturing hub attracts fresh capacity from global automakers, while rising e-commerce logistics and infrastructure spending lift commercial-vehicle shipments. Hybrid powertrains help maintain internal-combustion predominance across commercial fleets, keeping routine lubrication and hydraulic filtration needs elevated. Construction booms across Southeast Asia further propel hydraulic filter uptake in excavators, loaders, and cranes. These factors lock in incremental volume for the oil filter market even as EV penetration gradually climbs.

Increasing OEM Adoption of Extended-Life Synthetic Oil Filters

Automakers now specify synthetic media capable of 15,000–20,000-mile drain intervals to cut servicing costs and meet warranty-extension targets. Solutions such as MANN+HUMMEL’s 20,000-mile filter series combine micro-glass fibers with polymeric layers to capture sub-5 µm particles while sustaining flow [1]“20,000-Mile Engine Oil Filter Product Sheet,” MANN+HUMMEL Group, mann-hummel.com . Fleet operators value the up to two-fifths longer life, accepting the higher unit price in exchange for reduced downtime and labor. Nanofiber advances also enable lighter, recyclable housing that aligns with circular-economy objectives. As a result, premium filters offset part of the lost unit volumes from electrification in the global oil filter market.

Stringent Emission & Fuel-Efficiency Regulations

Euro 7, effective from 2025, imposes tighter particle-number thresholds and durability validation up to two lakh kms, pushing OEMs toward higher-efficiency crankcase and engine filters [2]“Euro 7 Standards Explained,” European Commission, europa.eu. Parallel updates from the U.S. Environmental Protection Agency require comparable lifetime compliance, spurring global harmonization of filter specifications. These policies enlarge the addressable value pool for suppliers who can certify longer-lasting, low-pressure media, particularly in commercial vehicles where uptime and compliance penalties loom.

Rising Aftermarket E-Commerce Penetration

Online platforms now allow direct-to-installer and subscription sales, offering transparent pricing and real-time inventory. Fleet managers exploit digital procurement portals that integrate telematics data, auto-generating replenishment orders before mileage thresholds are reached. Smaller brands leverage marketplaces to bypass traditional wholesalers, intensifying price competition and broadening consumer choice. Authenticity verification technologies, such as QR-code serial tracking, help established manufacturers defend brand equity and limit counterfeit infiltration into the oil filter market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing EV Share Reducing Oil-Filter Replacement Volume | -1.5% | North America and EU core, expanding globally | Long term (≥ 4 years) |

| Volatility In Automotive Production Cycles | -1.1% | Global, with acute impact in developed markets | Short term (≤ 2 years) |

| Raw-Material Price Inflation | -0.8% | Global, with higher impact on premium filter segments | Short term (≤ 2 years) |

| Counterfeit & Low-Quality Filters | -0.6% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing EV Share Reducing Oil-Filter Replacement Volume

Battery-electric cars eliminate engine oil, and hybrids halve replacement frequency. Historically core to high-margin extended-life filters, premium passenger segments are leading in EV adoption across Europe and the United States. Suppliers respond by diversifying into battery-coolant and cabin particulate filtration, but these niches do not yet match the scale of lost engine oil applications. Strategic mergers, exemplified by Thermo Fisher’s USD 4.1 billion purchase of Solventum’s filtration assets, illustrate the quest for portfolio breadth and new revenue streams [3].

Volatility in Automotive Production Cycles

Since 2024, semiconductor shortages and shifting trade policies have triggered intermittent shutdowns, complicating capacity planning for filter suppliers. Short-notice schedule cuts from OEMs force producers to carry higher finished goods inventories, tying up working capital and pressing margins. Smaller regional manufacturers face heavier exposure, prompting some to channel surplus stock into aftermarket networks at discount levels, which weighs on overall pricing across the oil filter market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Engine Oil Filters Sustain Value While Hydraulics Outpace Growth

The engine oil sub-segment held 41.28% of the oil filter market share in 2024, underlining its centrality to internal-combustion maintenance. Extended-life synthetic designs stabilize value retention despite a gradual dip in change-out volumes. Diesel-engine fuel filters remain vital in trucks and off-highway machinery, even as gasoline direct-injection spreads in light vehicles. Hydraulic filters are on course for a 4.95% CAGR, benefiting from construction machinery growth in Asia and rising factory automation in North America. Other niche filters, including transmission and power-steering variants, gain relevance as power-train complexity intensifies. Manufacturers emphasize recyclable, polymer-based modules, positioning themselves to tap forthcoming circular-economy procurement mandates.

Demand dynamics within the oil filter market point to differentiated growth paths: engine units face electrification headwinds but preserve margins through premium media, whereas hydraulic lines enjoy volume upside linked to infrastructure and industrial expansion. Suppliers with cross-segment engineering capabilities can repurpose nano-fiber labs and automated pleating lines across both categories, lowering unit costs and enhancing strategic flexibility.

By Sales Channel: Aftermarket Still Dominant, Digital Shifts Accelerate

Aftermarket demand drives 65.47% of the oil filter market share in 2024, solidifying the aftermarket’s primacy within the oil filter market size. It also registered a robust CAGR of 5.03% through 2030. Vehicles remain in service for extended periods, and owner preference for quick lube outlets and independent workshops keeps replenishment cycles predictable. Larger fleets increasingly adopt predictive-maintenance dashboards that schedule filter swaps around utilization rather than fixed mileage, smoothing demand seasonality.

The pivot to e-commerce is reshaping behavior. Consumers appreciate shipping and fitment-compatibility tools, whereas small garages use online bulk orders to avoid stockouts. Brands investing in digital storefronts and interactive part-selection guides win share without undercutting brick-and-mortar partners. Nonetheless, the rise in counterfeit listings obliges premium suppliers to integrate blockchain or serialized hologram labels, an extra cost and a brand-differentiator in the global oil filter market.

By Vehicle Type: Commercial Fleets Lead Expansion Amid Passenger-Car Volume

Due to their population scale, passenger vehicles generated 53.72% of the oil filter market share in 2024, yet medium and heavy commercial trucks are registering the fastest 5.07% CAGR through 2030. Fleet uptime priorities and stricter emissions rules drive the adoption of high-capacity spin-on or cartridge filters with integrated bypass valves. Light commercial vans benefit from the surge in last-mile delivery, sustaining steady-state growth. Although premium passenger segments are shifting to battery power first, mass-market models in emerging economies remain combustion-engine dominated, ensuring a multiyear runway for engine-oil filter demand.

Commercial-vehicle resilience hinges on the slower electrification timeline for heavy-duty, where battery weight, charging infrastructure, and duty cycles remain barriers. Euro 7 extends tailpipe compliance verification to real-world conditions, pushing OEMs and fleet managers toward higher filtration efficiency and more extended durability. Suppliers that can document filtration performance across 100,000-mile oil-drain intervals position themselves favorably in the oil filter market.

By Distribution Channel: Traditional Retail Holds Ground as Online Gains Pace

Traditional Retail retains a 47.81% of the oil filter market share in 2024, fueled by professional installation preference and immediate part availability. National parts chains cooperate with quick-lube centers to hold core SKUs in local warehouses, ensuring same-day completion for walk-in customers. Authorized dealerships reinforce loyalty with bundled maintenance packages, though pricing transparency challenges margin sustainability.

Online retailers are expanding at a 4.97% CAGR, propelled by robust search-filtering tools, user reviews, and subscription offerings that deliver filters and gaskets ahead of mileage targets. Digital storefronts also level the playing field for niche producers specializing in racing or off-road applications. Yet, counterfeit risk remains acute: consumers increasingly rely on serialized QR verification apps supplied by original manufacturers. Effective authentication fosters customer trust and underwrites premium positioning for established brands in the evolving oil filter market.

Geography Analysis

Asia-Pacific captured 38.93% of the oil filter market share in 2024 and is pacing a 4.99% CAGR through 2030 on the back of sustained vehicle production and infrastructure investment. China’s status as the world’s largest auto producer secures hefty OEM volumes, while India’s manufacturing build-out and burgeoning vehicle parc underpin aftermarket consumption. Slower regional EV uptake relative to Europe and North America prolongs engine-oil filtration demand, and large-scale construction programs fuel hydraulic-filter sales.

North America represents a mature but innovative-forward arena, where synthetic media penetration exceeds two-thirds of passenger-car replacements. EV uptake is accelerating, yet the sizable legacy vehicle parc guarantees a stable baseline for the oil filter market. E-commerce already captures nearly 30% of filter revenue in the United States, encouraging brands to refine omni-channel fulfillment models. Europe faces dual pressures: rapid electrification and stringent Euro 7 standards that extend service intervals. Suppliers offset volume risk by marketing premium, recyclable cartridges engineered for 200,000 km durability. Government subsidies for zero-emission buses leave heavy-duty diesel fleets comparatively smaller, yet long-haul trucking still relies on high-performance multi-stage oil filtration.

South America, the Middle East, and Africa account for a modest but rising share. Brazil’s auto-production recovery and oil-and-gas field expansions stimulate engine and hydraulic filter replacements. Gulf region megaprojects create continuous demand for construction-equipment filtration, while sub-Saharan Africa’s mining trucks and agricultural machinery drive niche opportunities. Currency volatility constrains import affordability, pushing local assemblers to seek cost-optimized filters, yet the absence of tight emission rules keeps conventional media relevant beyond 2030.

Competitive Landscape

The oil filter market remains moderately fragmented, with the top five suppliers estimated to hold nominal combined share. MANN+HUMMEL, Donaldson, and Robert Bosch anchor the premium tier, promoting multilayer synthetic and nanofiber products capable of extended service intervals and low differential pressure. Donaldson leverages its industrial filtration know-how to cross-pollinate high dirt-holding capacities into off-road equipment. Bosch integrates smart sensors that signal remaining filter life to connected dashboards, aligning with OEM telematics ecosystems.

Consolidation momentum is growing as incumbents hedge against EV headwinds. Hengst SE has absorbed CSC Technologies and IFS to deepen specialty media portfolios and gain regional manufacturing bases. New entrants focusing on bio-based polymers or full aluminum housings position themselves around sustainability credentials, courting automakers that have pledged cradle-to-grave carbon reductions.

R&D priorities include reducing pressure drop, increasing dust-holding capacity, and ensuring recyclability. Vendors experiment with complete cellulose-free designs and solvent-free adhesive systems to improve environmental footprints. Intellectual-property litigation has intensified around nanofiber layering techniques, reflecting the premium commanded by high-efficiency media. Overall, competitive dynamics emphasize hybrid value propositions—performance, sustainability, and digital integration—rather than pure price leadership.

Oil Filter Industry Leaders

Mann+Hummel

Donaldson Company

Mahle GmbH

Robert Bosch GmbH

DENSO Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: MANN+HUMMEL, transitioned its MANN-FILTER brand of oil filters to use plant-based lignin in place of crude-oil-based resins. This move not only cuts down the filter's CO2 footprint but also diminishes its dependence on fossil fuels.

- March 2025: Purolator unveiled its latest innovation: the Purolator 20K Premium Oil Filter. Tailored for high-performance driving, the 20K Premium Oil Filter promises exceptional engine protection for up to 20,000 miles, catering to drivers prioritizing affordability, reliability, and durability.

- February 2025: Standard Motor Products, Inc. (SMP) expanded its line of Oil Filter Housing Kits and Assemblies. These kits, factory-assembled with pre-installed oil filters and sensors, are tailored for specific applications and feature updated components along with manifold gaskets.

Global Oil Filter Market Report Scope

| Fuel Filters |

| Engine Oil Filters |

| Hydraulic Filters |

| Other Filters (Transmission, etc.) |

| OEM |

| Aftermarket |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

| Traditional Retail |

| Online Retail / E-Commerce |

| Authorized Service Centers |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Fuel Filters | |

| Engine Oil Filters | ||

| Hydraulic Filters | ||

| Other Filters (Transmission, etc.) | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium & Heavy Commercial Vehicles | ||

| By Distribution Channel | Traditional Retail | |

| Online Retail / E-Commerce | ||

| Authorized Service Centers | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the oil filter market?

The oil filter market size is USD 3.94 billion in 2025.

How fast is the market expected to grow through 2030?

It is projected to expand at a 4.94% CAGR between 2025 and 2030.

Which region leads global demand?

Asia-Pacific holds 38.93% of 2024 revenue and is also the fastest-growing region.

Which product type is expanding the quickest?

Hydraulic filters are forecast to grow at a 4.95% CAGR through 2030.

How will electric-vehicle adoption influence filter sales?

Battery-electric cars remove engine oil filtration, and hybrids cut change-out frequency by up to 70%, reducing long-term volume but boosting demand for premium synthetic filters in remaining ICE fleets.

Which sales channel dominates today?

The aftermarket accounts for 65.47% of global filter revenue due to routine replacements over vehicle lifespans.

Page last updated on: