Electronically Scanned Array Radar Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

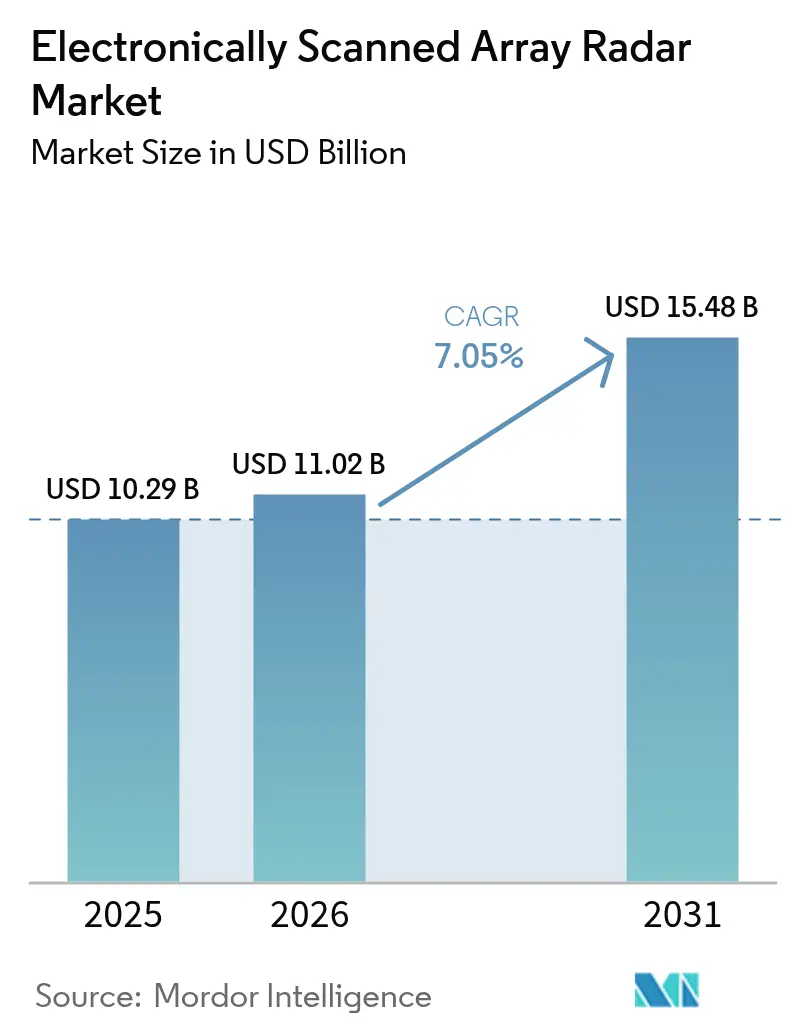

| Market Size (2026) | USD 11.02 Billion |

| Market Size (2031) | USD 15.48 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

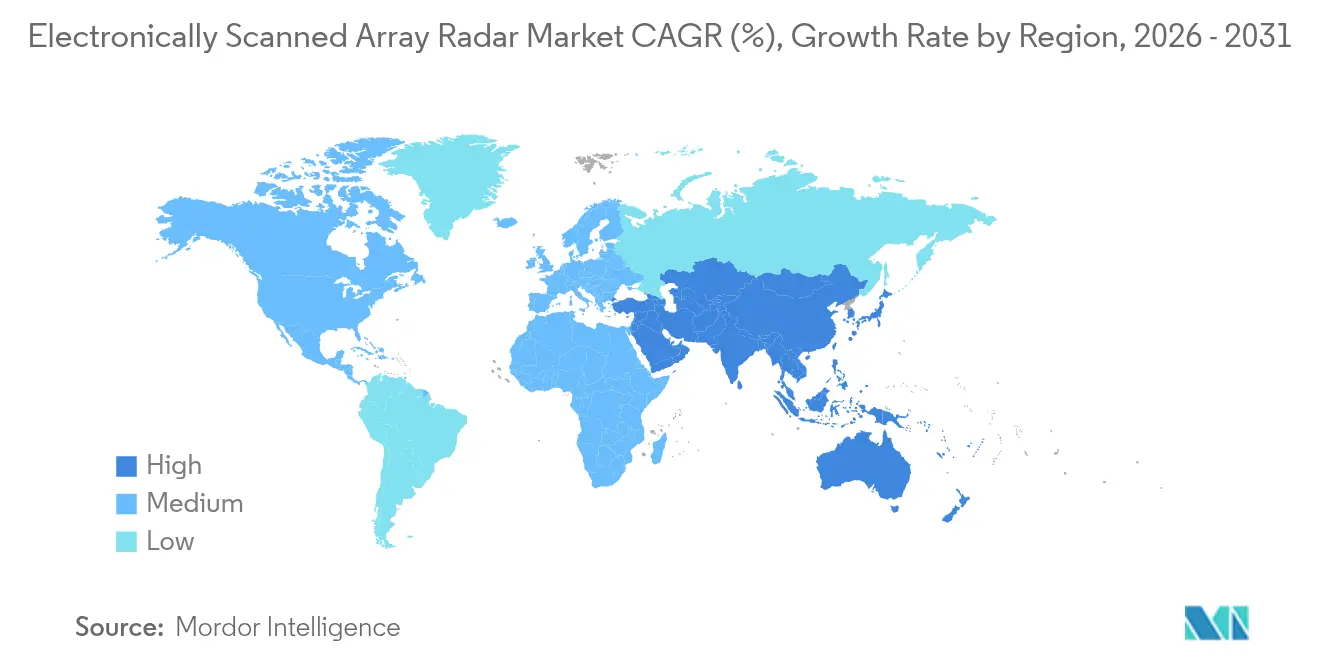

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

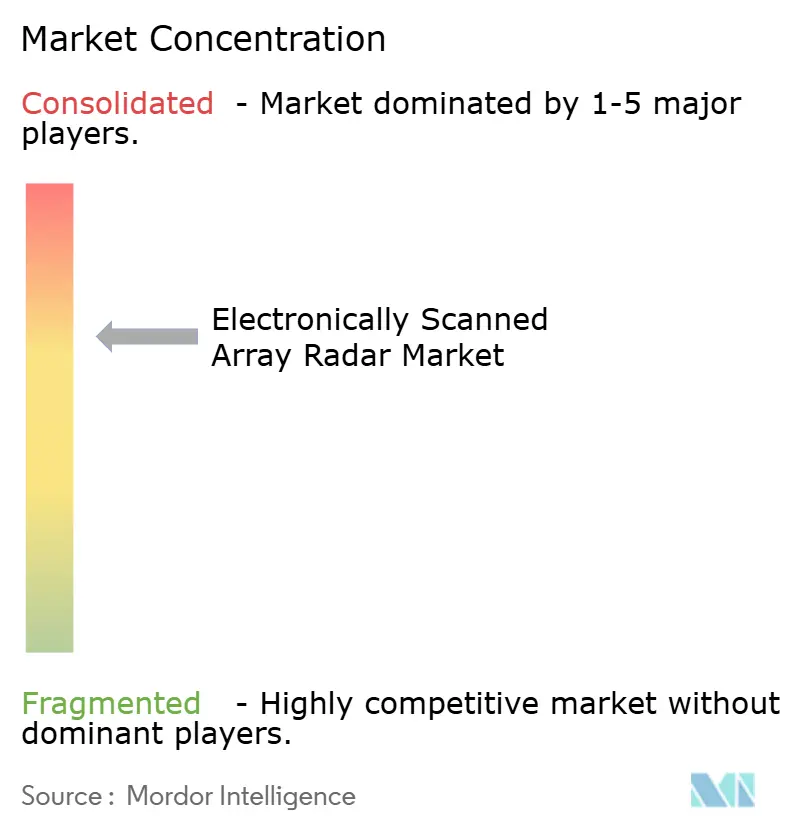

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronically Scanned Array Radar Market Analysis by Mordor Intelligence

The electronically scanned array (ESA) radar market size was valued at USD 10.29 billion in 2025 and estimated to grow from USD 11.02 billion in 2026 to reach USD 15.48 billion by 2031, at a CAGR of 7.05% during the forecast period (2026-2031). Robust defense spending, especially across the Indo-Pacific and Eastern Europe, is accelerating the shift from mechanically steered units to AESA architectures. Persistent demand for multi-function 4D situational-awareness radars, expanding adoption of gallium-nitride (GaN) transmit/receive modules, and rapid maturation of software-defined beam-forming are reshaping procurement priorities. The market also benefits from AI-enabled threat classification, while retrofit activity on legacy platforms keeps near-term volumes stable. Supply-chain exposure to critical minerals and stringent export-control frameworks temper growth momentum, yet platform diversification and international partnerships continue to broaden addressable demand.

Key Report Takeaways

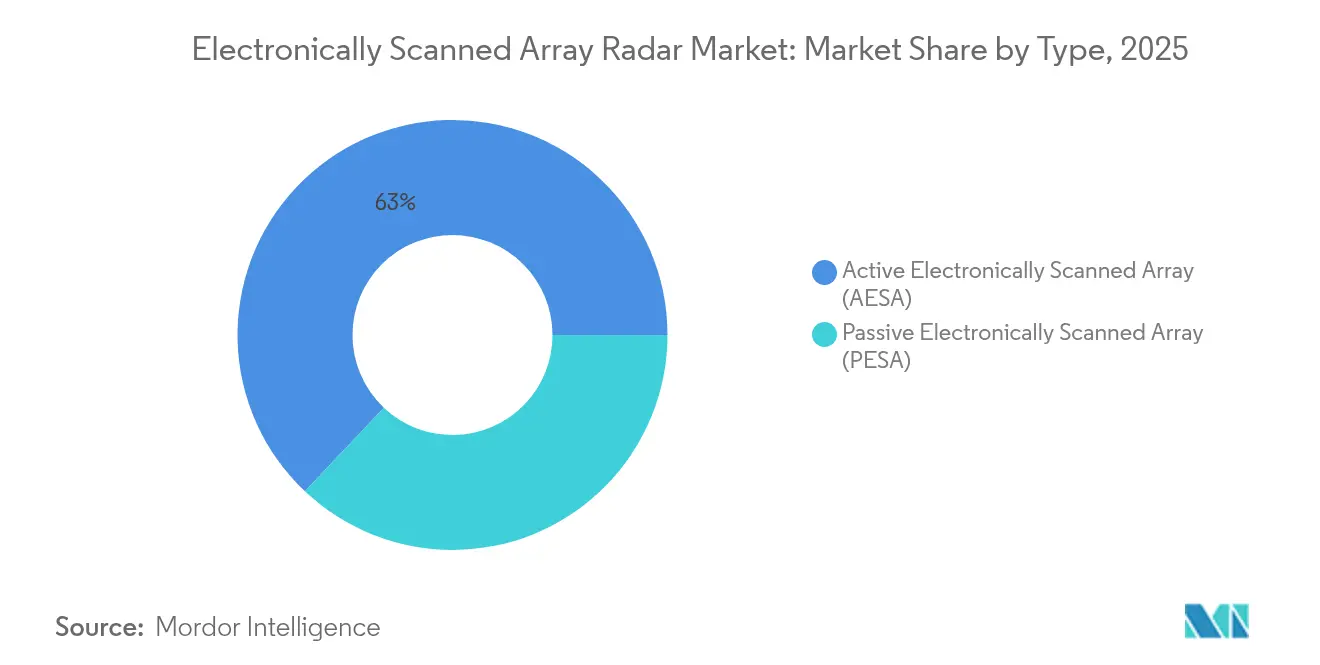

- By type, Active Electronically Scanned Array (AESA) systems led with 62.96% revenue share in 2025, while the segment is set to expand at a 9.32% CAGR to 2031.

- By platform, land-based deployments captured 45.12% of the electronically scanned array radar market share in 2025, while naval platforms recorded the fastest 10.62% CAGR through 2031.

- By fit, line-fit installations commanded 68.23% of the electronically scanned array radar market size in 2025, whereas retrofit solutions grew at a 10.21% CAGR from 2026 to 2031.

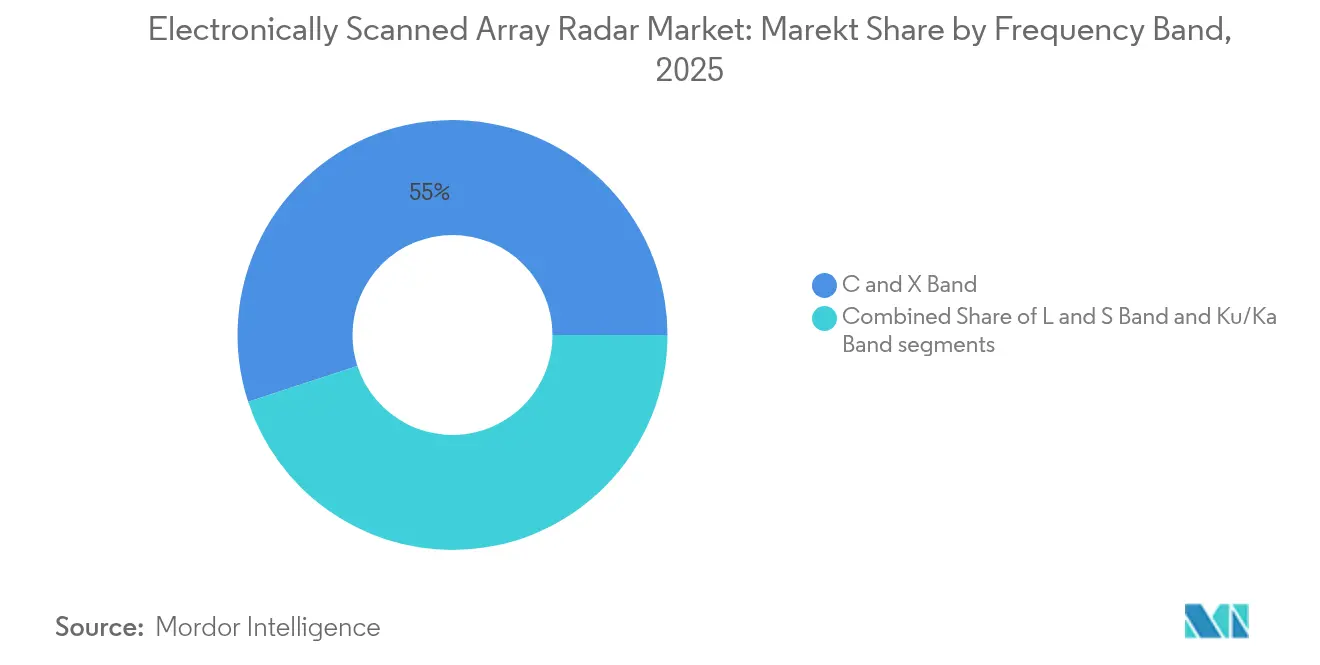

- By frequency band, the C and X band segment accounted for 55.02% share of the market in 2025, while Ku/Ka band products posted an 8.26% CAGR to 2031.

- By application, surveillance and early warning represented a 42.11% share in 2025, and electronic warfare use cases advance at a 10.02% CAGR over the forecast horizon.

- By end-user, defense forces held a 49.35% share in 2025, yet homeland security agencies registered a 9.05% CAGR through 2031.

- By component, antenna aperture and radome hardware contributed 38.41% of revenue in 2025; digital signal processors led growth at 8.14% CAGR.

- By geography, North America maintained a 35.12% share in 2025, whereas Asia-Pacific is projected to post a 9.61% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electronically Scanned Array Radar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Military modernization programs accelerating AESA procurement | +2.1% | Global; North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Demand for multi-function 4D situational-awareness radars | +1.8% | Global; contested regions | Long term (≥ 4 years) |

| Geopolitical tension–fueled defense budget expansion | +1.5% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Transition to GaN T/R modules lowering lifecycle cost | +1.2% | Advanced defense markets | Medium term (2-4 years) |

| AI-enabled software-defined beam-forming capabilities | +0.8% | North America, Europe, select Asia-Pacific | Long term (≥ 4 years) |

| Lightweight ESA retrofits for UAVs and attritable platforms | +0.6% | All regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Military Modernization Programs Accelerating AESA Procurement

AESA capability has shifted from desirable to mandatory for next-generation assets. The US Air Force fielded Northrop Grumman’s AN/TPS-80 G/ATOR, combining five legacy functions into one platform.[1]“AN/TPS-80 G/ATOR Programme,” armyrecognition.com European states follow, with the UK integrating an advanced Typhoon radar and Estonia procuring Thales GM400α systems. Procurement velocity reflects recognition that legacy mechanically scanned radars cannot support multi-domain operations. AI-enabled modes further magnify mission value. Consequently, defense agencies now treat AESA as foundational infrastructure for network-centric warfare.

Demand for Multi-Function 4D Situational-Awareness Radars

Operators require instantaneous azimuth, elevation, range, and Doppler data. Thales’ NS200 offers full digital beam-forming up to 400 km while supporting swarm defense and missile guidance.[2] “NS200 4D Radar,” thalesgroup.com Lockheed Martin’s Long-Range Discrimination Radar tracks targets beyond 2,000 km for ballistic-missile defense.[3]“Long Range Discrimination Radar,” lockheedmartin.com Civil aviation’s NextGen program similarly propels demand for advanced surveillance. Convergence of military and civilian needs lowers per-unit cost. The ability to cover multiple missions with one aperture transforms platform design economics.

Geopolitical Tension–Fueled Defense Budget Expansion

Regional flashpoints accelerate spending. Japan raised its defense allocation by 16%, Germany 28 28% in 2024, and Israel lifted outlays by 65% amid active conflict. China placed counter-stealth radar on South China Sea reefs, prompting allied investments. NATO interoperability requirements reinforce standardised AESA procurement. High outlays create virtuous volume effects, pushing system prices down and widening market access.

Transition to GaN T/R Modules Lowering Lifecycle Cost

GaN devices deliver double the power density of GaAs while tolerating higher operating temperatures. Raytheon supplied the first GaN-equipped AN/TPY-2 to the Missile Defense Agency in May 2025.[4]“AN/TPY-2 GaN Upgrade,” raytheon.com India’s Uttam radar boasts a 25% range uplift thanks to GaN modules. Improved thermal efficiency eases cooling and enables smaller form factors. Commercial automotive radar volumes further compress semiconductor costs, though gallium supply dependence on China remains a strategic concern.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High program CAPEX versus legacy systems | -1.8% | Emerging markets | Short term (≤ 2 years) |

| ITAR and export-control constraints | -1.2% | Technology-transfer markets | Long term (≥ 4 years) |

| Thermal-management limits of dense GaN arrays | -0.9% | High-power applications | Medium term (2-4 years) |

| Rare-earth supply-chain fragility for T/R modules | -0.7% | China-dependent markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Program CAPEX Versus Legacy Systems

AESA upgrades carry steep upfront costs. The B-52 radar replacement has surpassed initial estimates and slowed schedules. Northrop Grumman’s USD 121.5 million contract to refurbish B-1 antennas highlights the investment intensity. Complex integration work on power, cooling, and data buses inflates budgets. Smaller defense agencies defer adoption, sustaining a two-tier market.

ITAR and Export-Control Constraints

US export rules classify electronically scanned array radar as Category XI. Licences, technical-assistance agreements, and compliance audits extend project timelines and raise transaction costs. Allies often face delays in replenishing stocks during crises. Restrictions open doors for non-US suppliers, potentially fragmenting technology standards across theatres.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: AESA Dominance Drives Innovation

AESA technology accounted for 62.96% revenue in 2025 as distributed T/R modules eliminated single-point failure, while the segment promises a 9.32% CAGR through 2031. The electronically scanned array radar market benefits as each module scales independently, allowing graceful degradation under battle damage. Passive electronically scanned arrays (PESA) persist in cost-sensitive ground roles, yet falling GaN device pricing narrows the cost gap. AI-driven waveform agility further widens AESA’s performance edge.

Growing demand for resilience against sophisticated jamming favours AESA configurations that can hop frequency and steer beams within microseconds. As volumes rise, manufacturing economies drive unit pricing closer to PESA equivalents, reshaping procurement calculus. Software-defined updates lengthen service life and accelerate capability upgrades. Consequently, the electronically scanned array radar market size for AESA platforms is forecast to reach USD 9.75 billion by 2031, reinforcing its position as the baseline architecture across airborne, maritime, and ground systems.

By Platform: Naval Surge Outpaces Traditional Domains

Land-based systems held a 45.12% share in 2025, yet naval installations are tracking an 10.62% CAGR, the highest across platforms. New-build destroyers, frigates, and amphibious vessels integrate SPY-6, CERETRON, and GhostEye systems, replacing mechanically scanned arrays. Raytheon’s USD 1.18 billion SPY-6 series contract exemplifies volume potential.

The maritime up-cycle reflects Indo-Pacific fleet modernization and the need for distributed missile-defense coverage. Onshore, counter-UAS demand sustains ground segment sales, while airborne upgrades to F-15EX and Gripen E remain robust. Space and high-altitude pseudo-satellites add incremental demand, albeit from a small base. Altogether, the electronically scanned array radar market share for naval platforms is projected to rise four percentage points by 2031 as sea-based ballistic-missile defense becomes a top priority.

By Fit: Retrofit Market Accelerates Modernization

Line-fit deliveries represented 68.23% of 2025 revenue owing to F-35, Type 26, and Constellation-class procurement pipelines. Retrofit activity, however, grows faster at 10.21% CAGR as forces extend legacy fleet life. The APG-79 integration on F/A-18 and SPY-6 back-fit for Nimitz-class carriers illustrates scale.

Modular arrays and common back-end processors simplify insertion, curbing downtime. Digital-through-digital interfaces reduce cabling while embedded cooling plates lower structural modification needs. Retrofitting, therefore, offers near-new performance without the capital outlay of platform replacement, bolstering the electronically scanned array radar market through mid-decade.

By Frequency Band: C and X Band Versatility Prevails

C and X band units generated 55.02% of revenue in 2025. They are prized for their multi-mission flexibility and minimal rain fade. They enable single-aperture execution of air-to-air and surface-search tasks, streamlining topside real estate.

Ku/Ka band arrays expand at 8.26% CAGR on the back of high-resolution imaging and small-drone tracking. Higher frequencies shorten antenna length, allowing mast-mounted or podded solutions on space-constrained platforms. L and S bands remain relevant for long-range early warning. Collectively, the electronically scanned array radar market size for Ku/Ka variants should exceed USD 2.17 billion by 2031 as tactical-UAV proliferation continues.

By Application: Electronic Warfare Capabilities Surge

Surveillance and early warning contributed 42.11% of revenue in 2025, yet electronic warfare (EW) applications clock a 10.02% CAGR through 2031. AESA enables simultaneous radar and jamming, with each module addressing different frequencies. Jane's reports multi-role arrays disrupting adversary data links while retaining search capacity.

Fire-control systems adopt AESA for improved track-while-scan, supporting networked shooters. Civil air traffic control transitions to digitally networked systems under the FAA NextGen roadmap. Growing EW demand ensures the electronically scanned array radar market maintains double-digit growth despite cyclical defense budgets.

By End-User: Homeland Security Adoption Accelerates

Military organizations accounted for 49.35% of revenue in 2025, but homeland security stakeholders expanded fastest at 9.05% CAGR. Border agencies deploy gap-filling radars with unmanned integration to counter low-slow-small threats.

Dual-use procurement leverages common logistics between defense and civil authorities, aiding budget approval. As drone incursions intensify, coastal and critical-infrastructure operators procure cost-efficient AESA units, lifting the electronically scanned array radar industry’s non-military share yearly.

By Component: Digital Processing Drives Innovation

Antenna and radome elements generated 38.41% of the 2025 turnover. However, demand for high-throughput processors positions the DSP segment for an 8.14% CAGR, reflecting AI insertion.

GaN T/R modules remain a pivotal investment area. Supply-chain localization projects in the US, Japan, and India target resilience despite raw-material constraints. Improved thermal-interface materials and direct-to-liquid cooling are under development, ensuring the electronically scanned array radar market remains at the forefront of semiconductor innovation.

Geography Analysis

North America retained a 35.12% share in 2025, buoyed by the world’s largest defense budget and a mature industrial base. Multi-year production of SPY-6 and TPY-4 systems underpins regional demand, while artificial-intelligence upgrades to legacy radars lock in aftermarket revenue. Canadian NORAD modernization and Mexican border-security programs provide supplemental orders. Continuous investment in GaN fab capacity positions the region to secure export competitiveness despite rising global rivalry.

Asia-Pacific posts the strongest 9.61% CAGR to 2031. China’s KJ-3000 AEW platform and phased-array coverage on reclaimed South-China-Sea outposts spur neighbours to accelerate buys. Japan’s transfer of FPS-3ME radars to the Philippines and Mongolia demonstrates deepening defense cooperation. India’s indigenously developed Uttam radar showcases ambitions for sovereignty, while South Korea’s Hanwha Systems equips FFX-III frigates with domestic GaN arrays. These combined initiatives elevate the electronically scanned array radar market across the region.

Europe continues to grow steadily as NATO’s integrated-air-and-missile-defense strategy mandates the adoption of standardised AESA. HENSOLDT’s EUR 6.929 billion (USD 8.06 billion) backlog exemplifies continental scale. The EISNET consortium integrates multi-sensor data for real-time command, emphasising software-defined interoperability. Influenced by the Ukraine conflict, Eastern European states prioritise ground-based air-defense radar, while the UK’s Eurofighter upgrades anchor airborne spending. Collectively, European procurement sustains the electronically scanned array radar market share above 25% through the forecast window.

Competitive Landscape

The market exhibits moderate concentration. Lockheed Martin Corporation, Northrop Grumman Corporation, and RTX Corporation collectively account for a major share of global revenue through multi-decade portfolios and vertically integrated R&D pipelines. Raytheon’s real-time cognitive-radar algorithms and GaN manufacturing scale offer competitive moats. Northrop Grumman leverages ground-based multi-mission arrays such as G/ATOR, while Lockheed Martin fields long-range discrimination capability and maritime systems.

Regional champions mature rapidly. HENSOLDT sustains record order intake with TRML-4D and CERETRON software-defined architectures. Saab expands Giraffe production in the UK, while ASELSAN and Hanwha Systems capture domestic naval programs. Partnerships like Norway’s GhostEye collaboration with Raytheon and Kongsberg illustrate co-development as an export-control workaround.

Emerging entrants focus on software-first models, offering modular backends to host third-party waveforms. Such openness appeals to militaries seeking sovereign control over updates. Meanwhile, demand for counter-UAS radars invites smaller firms to use cost-effective digital beam-forming solutions, averting over-engineering. New procurement models, including capability-as-a-service subscriptions for surveillance hotspots, further diversify the electronically scanned array radar market.

Electronically Scanned Array Radar Industry Leaders

Northrop Grumman Corporation

Lockheed Martin Corporation

RTX Corporation

Thales Group

Leonardo S.p.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Raytheon secured a USD 647 million contract for SPY-6 production, broadening missile-defense coverage for US naval fleets.

- May 2025: Raytheon delivered the first GaN-based AN/TPY-2 radar to the Missile Defense Agency, enhancing ballistic-missile-defense reach.

- April 2025: Lockheed Martin handed the first TPY-4 radar to the US Air Force under the 3DELRR program.

- February 2025: L3Harris completed the first flight of Viper Shield EW on a Block 70 F-16 alongside APG-83 AESA radar.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the electronically scanned array (ESA) radar market as all new active or passive radars whose beams are steered electronically through phase-controlled antenna elements across airborne, land, naval, space, and high-altitude pseudo-satellite platforms. According to Mordor Intelligence, the baseline year 2025 market value stands at USD 10.29 billion.

Scope Exclusions: Mechanical-scan radars, passive RF sensors, and software-only upgrades that do not add new T/R modules remain outside this evaluation.

Segmentation Overview

- By Type

- Active Electronically Scanned Array (AESA)

- Passive electronically scanned array (PESA)

- By Platform

- Airborne

- Land

- Naval

- Space and High-Altitude Pseudo-Satellites (HAPS)

- By Fit

- Line-fit (new-build)

- Retrofit/Upgrade

- By Frequency Band

- L and S Band

- C and X Band

- Ku/Ka Band

- By Application

- Surveillance/Early-warning

- Fire-control and Weapon-Guidance

- Electronic Warfare and SIGINT

- Weather and Air-Traffic Control

- By End-User

- Defense Forces

- Homeland Security and Border Agencies

- Commercial Aviation and ATC

- By Component

- T/R Module

- Digital Signal Processor

- Antenna Aperture and Radome

- Other Components

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor's team interviewed procurement officers in North America, radar integrators in Europe, and component suppliers across Asia-Pacific. These discussions validated platform mix assumptions, average selling prices, expected retrofit cycles, and near-term order books, enabling us to tighten model confidence where public data proved thin.

Desk Research

Mordor analysts began by mapping open-source defense budget lines, trade association briefs from bodies such as SIPRI, Eurocontrol traffic data for civilian airspace, and customs shipment records detailing GaN T/R module flows. We then drew trend signals from peer-reviewed IEEE radar journals, patent filings tracked through Questel, and safety-certified component lists issued by the U.S. Federal Communications Commission. Financial benchmarks from D&B Hoovers and news archives housed on Dow Jones Factiva clarified company-level production runs and contract deliveries. Many other credible publications and datasets were referenced to verify, clarify, and enrich the evidence pool.

Market-Sizing & Forecasting

A top-down build anchored on 2024 defense appropriation totals, commercial fleet counts, and recorded radar import values was constructed first. Supplier roll-ups and sampled unit-price × volume checks formed the bottom-up overlay that adjusts for dual-use sales and classified programs. Key model drivers include: (1) annual defense capital outlay per region, (2) share of new combat aircraft fitted with AESA, (3) gallium nitride wafer output, (4) missile threat indices influencing surveillance range upgrades, and (5) average retrofit age of legacy PESA sets. Forecasts employ multivariate regression with defense spending, fleet growth, and semiconductor capacity as predictors, while scenario analysis tackles sudden embargo or conflict shocks. Data gaps in the supplier layer are bridged through analog benchmarks from similar platforms and confirmed with primary sources.

Data Validation & Update Cycle

Outputs pass variance checks against independent shipment logs and historical ASP curves, after which senior analysts review anomalies. Reports refresh each year, and we trigger interim updates if a material contract, regulation, or geopolitical event alters the demand trajectory. A final sense-check is completed just before client delivery.

Why Mordor's Electronically Scanned Array Radar Baseline Stays Dependable

Published estimates often differ; scope width, price assumptions, and refresh timing drive most gaps.

Key gap drivers here include whether civilian weather radars are bundled, the treatment of retrofit labor, the currency year chosen, and whether future multi-mission software revenue is front-loaded. Mordor's disciplined segmentation, annual refresh, and dual-layer modeling keep our baseline balanced and reproducible.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.29 B (2025) | Mordor Intelligence | - |

| USD 10.99 B (2025) | Global Consultancy A | Includes wider digital radar categories and counts announced but unfunded programs |

| USD 10.03 B (2024) | Industry Journal B | Uses list prices without retrofit discounts and excludes spaceborne platforms |

| USD 8.70 B (2025) | Regional Market Tracker C | Omits commercial ATC demand and applies conservative ASP deflation |

In sum, the strict scope, transparent variables, and frequent validation steps outlined above ensure Mordor Intelligence provides a reliable, decision-ready starting point for stakeholders sizing the ESA radar opportunity.

Key Questions Answered in the Report

What is the current electronically scanned array radar market size?

The market is valued at USD 11.02 billion in 2026 and is projected to reach USD 15.48 billion by 2031, advancing at a 7.05% CAGR.

Which platform segment will expand the fastest?

Naval platforms lead growth with an 10.62% CAGR to 2031, driven by fleet modernization and maritime ballistic-missile defense investments.

Why is GaN technology important for AESA radars?

GaN transmit/receive modules offer double the power density of GaAs, lower cooling needs and longer service life, which together cut lifecycle costs and enhance performance.

How significant is Asia-Pacific to future growth?

Asia-Pacific records a 9.61% CAGR thanks to sustained Chinese, Japanese and Indian procurement plus regional partnership programs.

What role does artificial intelligence play in next-generation radars?

AI enables real-time beamforming, threat prioritization and adaptive waveforms, boosting resilience against complex jamming and reducing operator workload.

How do export-control regulations affect international sales?

ITAR and other export rules extend approval timelines and restrict technology transfer, pushing some nations to source from non-US suppliers or develop indigenous solutions.

Page last updated on: